Cloud Artificial Intelligence (AI) Market Size 2025-2029

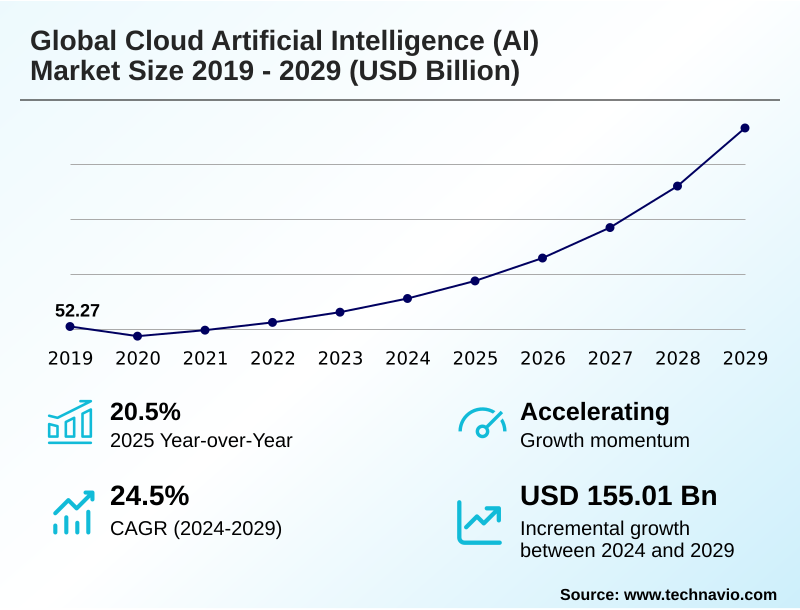

The cloud artificial intelligence (ai) market size is valued to increase by USD 155.01 billion, at a CAGR of 24.5% from 2024 to 2029. Proliferation of big data and the imperative for advanced analytics will drive the cloud artificial intelligence (ai) market.

Major Market Trends & Insights

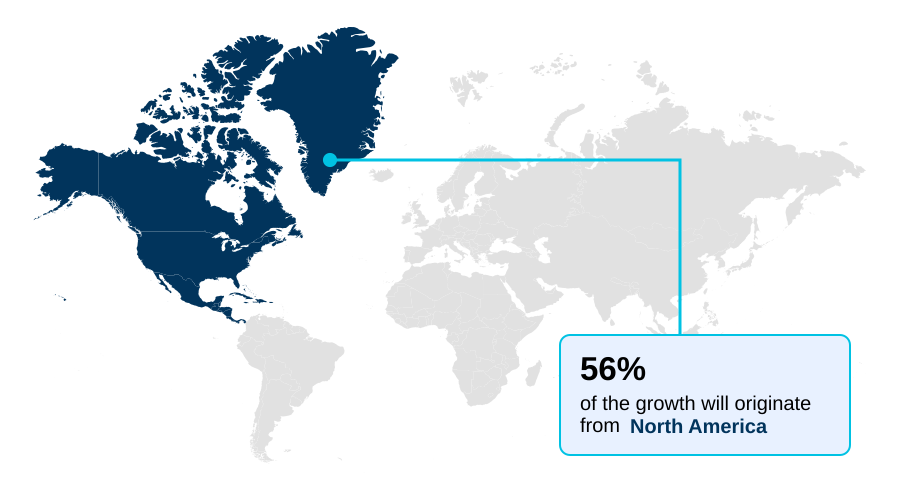

- North America dominated the market and accounted for a 55.6% growth during the forecast period.

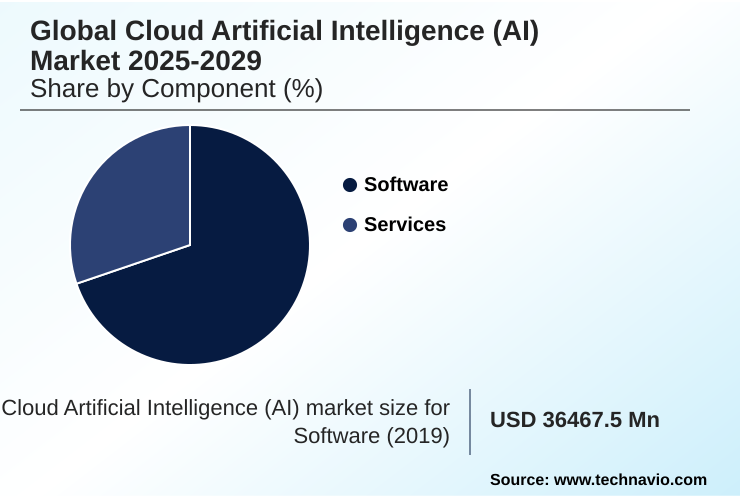

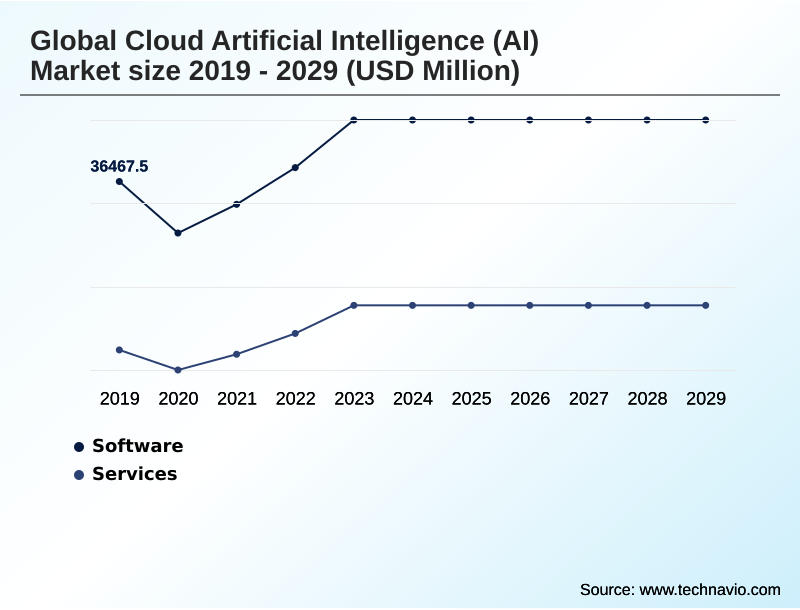

- By Component - Software segment was valued at USD 44.01 billion in 2023

- By Technology - Deep learning segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 180.48 billion

- Market Future Opportunities: USD 155.01 billion

- CAGR from 2024 to 2029 : 24.5%

Market Summary

- The Cloud Artificial Intelligence (AI) Market is characterized by the convergence of scalable computing infrastructure and advanced algorithms, enabling a paradigm shift in how businesses generate value from data. Key market drivers include the imperative for intelligent automation and the ability to derive ai-driven insights from massive datasets, which is unfeasible with traditional on-premise solutions.

- A dominant trend is the widespread adoption of generative ai and foundation models, which are increasingly offered through a foundation model as a service model, democratizing access to technologies like large language models. However, the market faces significant hurdles related to data privacy in ai and the need for robust ai governance.

- The challenge of algorithm bias and ensuring ai ethics in deployment remains a critical focus area. In a practical business scenario, a retail company might leverage cloud-native ai services to optimize its supply chain.

- By using predictive analytics to analyze real-time sales data and external factors, the system can automate inventory replenishment, reducing stockouts and improving operational efficiency by over 20% while enhancing the overall customer experience through more reliable product availability.

What will be the Size of the Cloud Artificial Intelligence (AI) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Cloud Artificial Intelligence (AI) Market Segmented?

The cloud artificial intelligence (ai) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Software

- Services

- Technology

- Deep learning

- Machine learning

- Nature language processing

- Others

- End-user

- IT and telecommunications

- BFSI

- Healthcare

- Retail and consumer goods

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The software segment is defined by a diverse array of cloud-native ai services that enable businesses to build and deploy intelligent systems without massive infrastructure overhead.

This includes powerful tools for natural language processing and computer vision, which are integral to modern ai application development. The accessibility of these platforms is fueling innovation across industries, from predictive maintenance ai in manufacturing to ai-enhanced cybersecurity in finance.

A critical component of this segment involves robust data governance frameworks embedded within the software, ensuring that data is managed securely and ethically.

The integration of AI has demonstrated tangible benefits, with some applications improving code generation capabilities by 15%, thereby accelerating development cycles and enhancing operational agility for enterprises.

The Software segment was valued at USD 44.01 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 55.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cloud Artificial Intelligence (AI) Market Demand is Rising in North America Get Free Sample

The market's geographic distribution is shaped by regional enterprise ai strategy and infrastructure maturity. North America leads, contributing over 55% of the incremental growth, driven by heavy investment in hybrid cloud ai and AIOps platforms that enhance operational oversight.

European regions are increasingly focused on sovereign ai initiatives to ensure data control, which influences ai model training methodologies. A data-centric ai approach is gaining global traction, emphasizing data quality as a prerequisite for successful ai operationalization.

In APAC, rapid adoption in sectors like ai in financial services is accelerating market expansion.

Across all regions, businesses are refining their strategies to leverage AI for a competitive advantage, with mature markets achieving up to a 15% reduction in IT incident resolution times.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Enterprises are strategically assessing the impact of generative ai on business operations, recognizing its potential to redefine productivity. A key enabler is the growing ecosystem providing benefits of foundation models as a service, which lowers the barrier to entry for sophisticated AI. However, this adoption necessitates implementing ai governance in enterprises to manage risks.

- Organizations are confronting the challenges of multimodal ai deployment, which require new infrastructure and skill sets. Central to this is developing strategies to mitigate algorithm bias, ensuring fairness and compliance. Many firms are focused on reducing ai integration complexity costs by adopting standardized platforms and best practices for ai model training.

- The debate over comparing on-premise vs cloud ai infrastructure continues, though cloud's scalability offers a distinct advantage for scaling ai applications for enterprises. A critical task is securing ai models in hybrid cloud environments to prevent data leakage. Simultaneously, businesses are leveraging ai for supply chain optimization, achieving better demand forecasting than legacy systems by a significant margin.

- The enterprise adoption of ai-powered chatbots has become standard for customer service. A core pillar for sustainable growth is developing a responsible ai framework, which guides all development and deployment. This includes managing data privacy in cloud ai and understanding the ethical considerations in ai deployment.

- The role of automl in democratizing ai is crucial for companies without large data science teams. Looking ahead, the future of sovereign ai initiatives will reshape data residency rules, while optimizing ai workloads for cost remains a constant operational goal.

- Finally, applying ai-driven predictive analytics for sales and using ai to improve operational efficiency are top priorities for achieving measurable ROI.

What are the key market drivers leading to the rise in the adoption of Cloud Artificial Intelligence (AI) Industry?

- The proliferation of big data, combined with the strategic imperative for advanced analytics, serves as a primary driver propelling market expansion.

- The demand for intelligent automation is a significant market driver, compelling organizations to invest in robust ai infrastructure.

- The use of deep learning and machine learning algorithms provides the foundation for advanced predictive analytics, with some sectors reporting a 30% improvement in forecasting accuracy.

- This is particularly evident in specialized fields such as ai for drug discovery, where complex data analysis is accelerated. To manage these intensive processes, ai workload optimization has become critical, reducing compute costs by up to 20%.

- The availability of scalable ai solutions and platforms featuring automated machine learning (automl) is lowering the barrier to entry, enabling more businesses to harness ai-driven insights for strategic decision-making and operational efficiency.

What are the market trends shaping the Cloud Artificial Intelligence (AI) Industry?

- The ubiquitous integration of generative AI represents a transformative market trend. Concurrently, the rise of foundation models delivered as a service is fundamentally reshaping enterprise capabilities.

- The market is rapidly evolving, driven by the integration of sophisticated technologies. A key trend is the adoption of generative ai, which is moving beyond text to include multimodal ai capabilities, enabling richer interactions. This has given rise to the foundation model as a service delivery model, democratizing access to powerful tools and expanding generative ai use cases.

- For example, ai-powered chatbots are becoming more advanced through context-aware computing, improving ai for customer experience by up to 25% by understanding user intent more deeply. These systems leverage real-time ai processing to deliver instant, relevant responses.

- Furthermore, techniques like federated learning are gaining traction, allowing models to be trained on decentralized data, which enhances privacy without sacrificing performance, reducing data transfer needs by 40%.

What challenges does the Cloud Artificial Intelligence (AI) Industry face during its growth?

- Significant concerns surrounding data privacy, security, and the ethical implications of AI deployment present a key challenge to the industry's growth.

- Despite rapid advancements, significant challenges persist. The complexity of large language models introduces issues like algorithm bias, which can lead to inequitable outcomes and requires rigorous oversight. AI security and data privacy in ai are paramount concerns, with the ai integration complexity of new systems often creating vulnerabilities.

- A major hurdle is the ai talent gap, which affects over 50% of organizations attempting to scale their initiatives. To address these issues, a focus on ai ethics and responsible ai deployment is crucial. This includes improving ai model interpretability to build trust and ensure transparent decision-making.

- Effective ai compliance management frameworks are essential for navigating the evolving regulatory landscape and mitigating risks associated with data handling and model behavior.

Exclusive Technavio Analysis on Customer Landscape

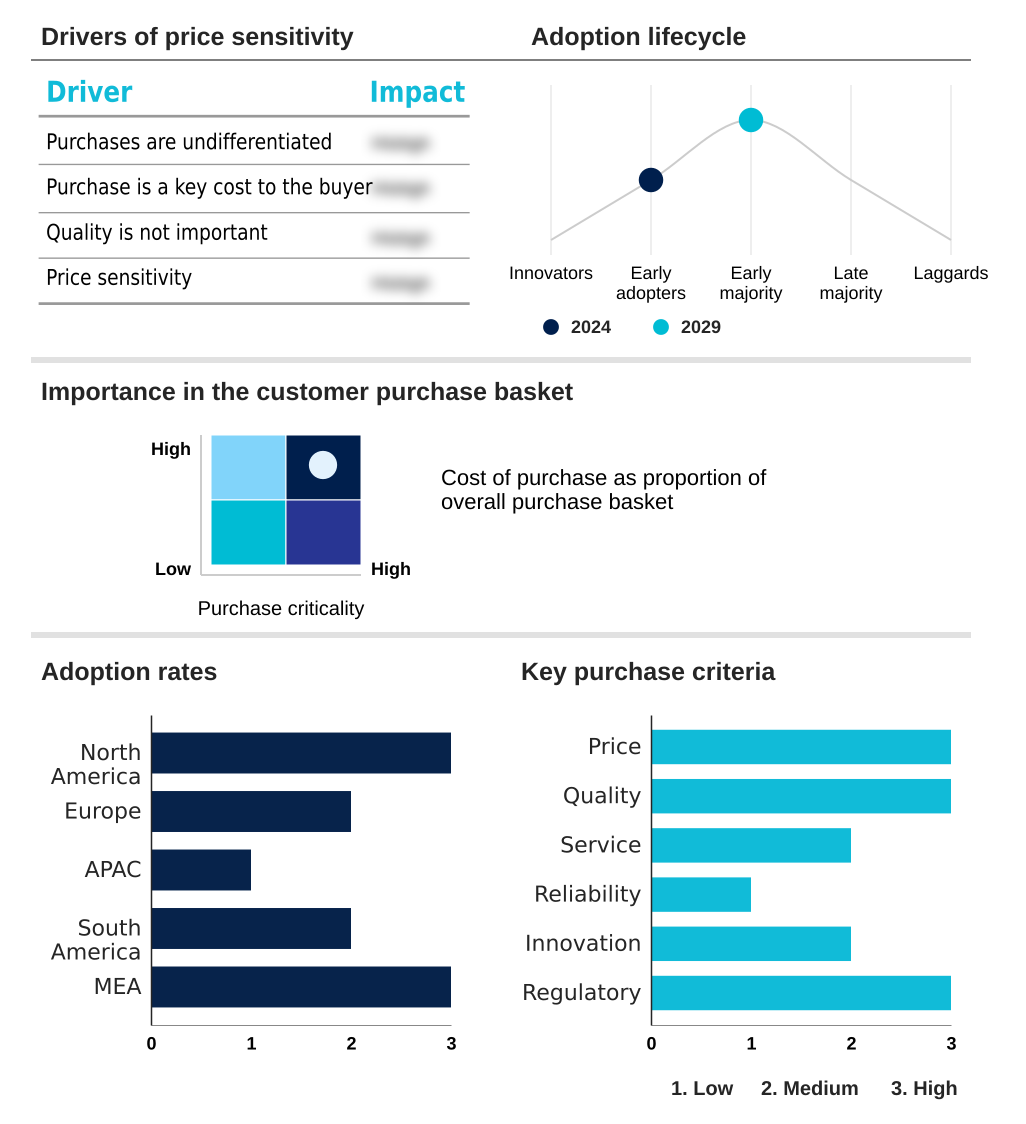

The cloud artificial intelligence (ai) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cloud artificial intelligence (ai) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cloud Artificial Intelligence (AI) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cloud artificial intelligence (ai) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon.com Inc. - Offers cloud AI products for text-to-speech, transcription, and an end-to-end machine learning platform for building, training, and deploying models at scale.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon.com Inc.

- AIBrain Inc.

- Baidu Inc.

- Cisco Systems Inc.

- Google LLC

- H2O.ai Inc.

- Informatica Inc.

- Infosys Ltd.

- Intel Corp.

- IBM Corp.

- Microsoft Corp.

- Nuance Communications Inc.

- NVIDIA Corp.

- Oracle Corp.

- Salesforce Inc.

- SoundHound AI Inc.

- Verint Systems Inc.

- VMware Inc.

- Wipro Ltd.

- ZTE Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cloud artificial intelligence (ai) market

- In August 2024, The European Union's AI Act came into force, establishing the world's first comprehensive legal framework for artificial intelligence with a stringent risk-based approach.

- In December 2024, The Government of Canada announced the Canadian Sovereign AI Compute Strategy, a plan to invest $2 billion in building the nation's domestic AI infrastructure.

- In January 2025, a report from the US government revealed that federal agencies have more than doubled their AI usage, with over 1,700 distinct use cases cataloged across departments.

- In March 2025, Canada's AI Compute Access Fund was launched to provide small and medium-sized enterprises with access to essential compute power for AI development and innovation.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cloud Artificial Intelligence (AI) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 310 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 24.5% |

| Market growth 2025-2029 | USD 155009.7 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 20.5% |

| Key countries | US, Canada, Mexico, UK, Germany, France, The Netherlands, Italy, Spain, China, Japan, India, South Korea, Australia, Singapore, Brazil, Argentina, Colombia, UAE, Saudi Arabia, South Africa, Israel and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's current state is defined by the pervasive influence of generative ai and the operationalization of foundation models. These large language models are the core of a technological shift toward intelligent automation and advanced predictive analytics. The synergy between deep learning and machine learning continues to evolve, now encompassing multimodal ai and context-aware computing.

- This evolution is enabled by scalable ai infrastructure, which supports complex ai model training on hybrid cloud ai platforms. However, this progress raises significant concerns regarding ai ethics, data privacy in ai, and the need to mitigate algorithm bias. Consequently, robust data governance frameworks and ai governance are becoming central to enterprise strategy.

- The deployment of ai-powered chatbots and solutions for computer vision and natural language processing is now mainstream, while AIOps delivers tangible efficiency gains, with some organizations reporting a 30% reduction in system downtime. As the landscape matures, ai security and the development of sovereign ai capabilities are becoming critical boardroom-level priorities.

What are the Key Data Covered in this Cloud Artificial Intelligence (AI) Market Research and Growth Report?

-

What is the expected growth of the Cloud Artificial Intelligence (AI) Market between 2025 and 2029?

-

USD 155.01 billion, at a CAGR of 24.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, and Services), Technology (Deep learning, Machine learning, Nature language processing, and Others), End-user (IT and telecommunications, BFSI, Healthcare, Retail and consumer goods, and Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Proliferation of big data and the imperative for advanced analytics, Data Privacy, security, and ethical Concerns

-

-

Who are the major players in the Cloud Artificial Intelligence (AI) Market?

-

Amazon.com Inc., AIBrain Inc., Baidu Inc., Cisco Systems Inc., Google LLC, H2O.ai Inc., Informatica Inc., Infosys Ltd., Intel Corp., IBM Corp., Microsoft Corp., Nuance Communications Inc., NVIDIA Corp., Oracle Corp., Salesforce Inc., SoundHound AI Inc., Verint Systems Inc., VMware Inc., Wipro Ltd. and ZTE Corp.

-

Market Research Insights

- A cohesive enterprise ai strategy is now essential for competitive advantage, moving beyond isolated projects to full ai operationalization. The focus on a data-centric ai approach improves ai model interpretability, a key factor in responsible ai deployment. Successful ai application development relies on scalable ai solutions and ai workload optimization to manage costs.

- The ai talent gap remains a challenge, driving adoption of automated machine learning (automl) platforms. Businesses leverage ai-driven insights for everything from predictive maintenance ai to ai for drug discovery, with generative ai use cases transforming content creation. The foundation model as a service trend simplifies access, but ai integration complexity persists.

- Robust ai governance solutions and ai compliance management are critical, especially for ai in financial services, while ai-enhanced cybersecurity protects assets. Ultimately, the goal is superior ai for customer experience through real-time ai processing and cloud-native ai services, with federated learning addressing privacy.

We can help! Our analysts can customize this cloud artificial intelligence (ai) market research report to meet your requirements.

RIA -

RIA -