Contact Center Market Size 2026-2030

The contact center market size is valued to increase by USD 259.3 billion, at a CAGR of 11.1% from 2025 to 2030. Focus on reducing operating costs of businesses will drive the contact center market.

Major Market Trends & Insights

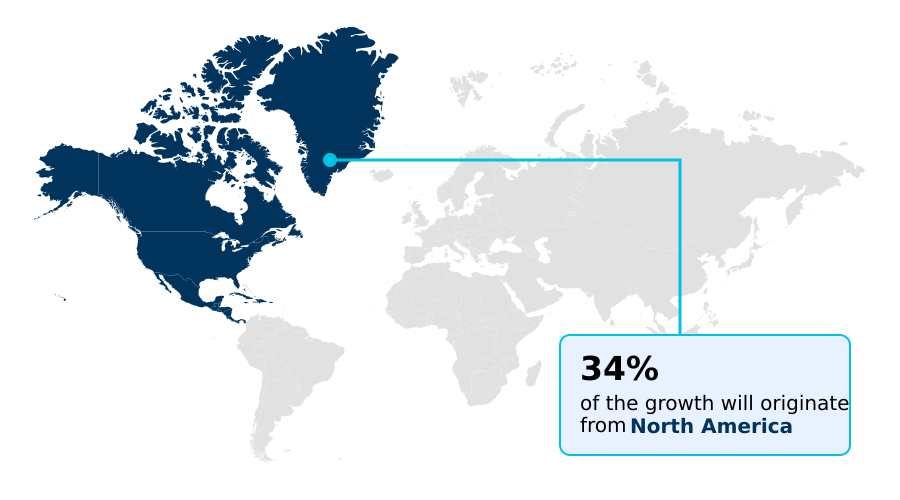

- North America dominated the market and accounted for a 34.2% growth during the forecast period.

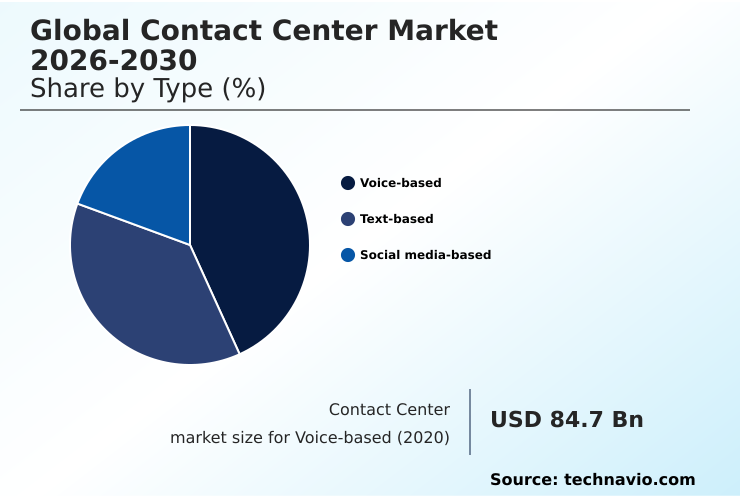

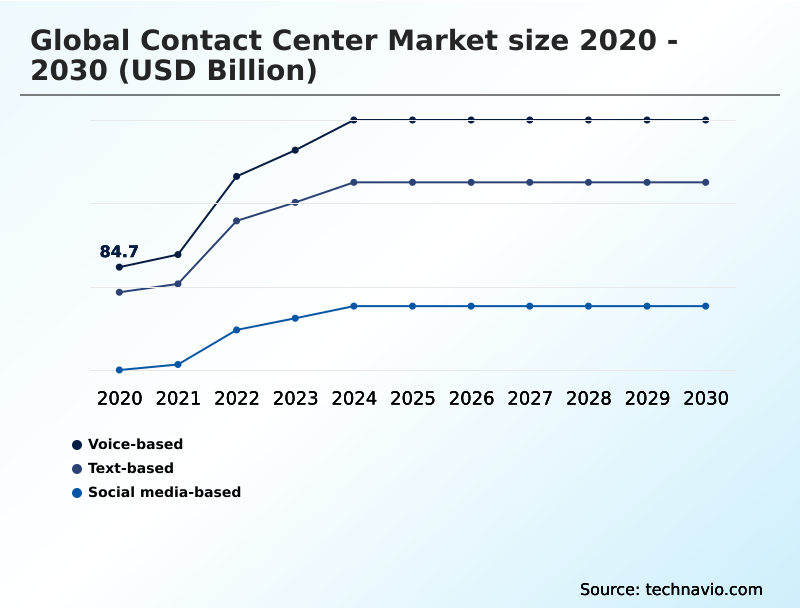

- By Type - Voice-based segment was valued at USD 151.5 billion in 2024

- By Deployment - On-premises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 437.6 billion

- Market Future Opportunities: USD 259.3 billion

- CAGR from 2025 to 2030 : 11.1%

Market Summary

- The contact center market is undergoing a fundamental transformation, shifting from a traditional cost center to a strategic hub for customer engagement and business intelligence. This evolution is propelled by the widespread adoption of cloud-native architecture and the sophisticated integration of artificial intelligence.

- AI-powered tools are now central to operations, enabling intelligent routing, predictive analytics, and advanced self-service portals that enhance customer satisfaction. A key business scenario involves retail enterprises leveraging omnichannel routing and workforce optimization tools to manage seasonal demand surges without compromising service quality.

- By creating a unified customer journey map across all touchpoints—from social media to voice—companies can deliver personalized and seamless experiences. This strategic focus on technology-driven customer experience, rather than just cost containment, defines the modern competitive landscape.

- The challenge remains in effectively managing data security and compliance within these increasingly complex, interconnected systems, which is critical for maintaining customer trust and ensuring long-term success.

What will be the Size of the Contact Center Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Contact Center Market Segmented?

The contact center industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Voice-based

- Text-based

- Social media-based

- Deployment

- On-premises

- Cloud-based

- Service

- Professional services

- Managed services

- Cloud-based contact center as a services

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- Germany

- France

- UK

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- South Africa

- UAE

- Saudi Arabia

- Rest of World (ROW)

- North America

By Type Insights

The voice-based segment is estimated to witness significant growth during the forecast period.

The voice-based segment is evolving from a universal channel to a premium touchpoint for high-value interactions. Despite the rise of digital engagement channels, voice remains critical for complex or sensitive issues where human empathy is vital.

The integration of advanced speech analytics and real-time transcription is transforming this space. Technologies like emotional intelligence AI are being used to guide agent performance, improving the customer effort score.

A key trend is the use of voice biometrics for secure authentication, which has shown to reduce average handling time by over 15%.

This shift toward AI-augmented voice interactions, supported by robust knowledge management systems, redefines its role, focusing on quality and resolution rather than just volume, making it a cornerstone of effective customer experience management.

The Voice-based segment was valued at USD 151.5 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 34.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Contact Center Market Demand is Rising in North America Get Free Sample

The global geographic landscape is characterized by diverse maturity levels and growth trajectories. North America remains the largest market, driven by heavy investment in agent empowerment tools and generative AI for agents to enhance customer experience.

In contrast, APAC is the fastest-growing region, with many enterprises leapfrogging legacy systems to adopt mobile-first, social media customer care strategies; this has led to a 40% increase in digital channel adoption over the past two years.

Europe's market is shaped by stringent compliance and data privacy regulations, pushing demand for secure, cloud-based IVR self-service automation and business intelligence integration.

Across regions, nearshoring to locations like South America and Eastern Europe is a prevalent strategy to manage costs, often reducing operational expenses by up to 30% while accessing skilled, multilingual talent pools for end-to-end journey orchestration.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the contemporary contact center environment requires a comprehensive evaluation of technology, operations, and security. A critical initial assessment involves weighing on-premise vs cloud contact center security, where cloud solutions now offer robust, certified environments that often exceed the capabilities of in-house teams.

- The focus then shifts to implementing AI for proactive customer service, which moves the organization from a reactive to a predictive engagement model. Key to this is understanding how to improve first call resolution rate, a metric directly impacted by technologies that provide agents with immediate access to relevant information.

- This is where the benefits of omnichannel customer engagement become clear, as a unified view of the customer journey provides essential context. Organizations are adopting best practices for workforce optimization, using AI for predictive call routing and scheduling to match agent skills with customer needs.

- Successfully integrating CRM with contact center platforms is fundamental, creating a single source of truth that enriches every interaction. To combat high turnover, a significant focus is placed on reducing agent attrition in call centers through better tools and career pathing.

- Many are using speech analytics for quality assurance, moving beyond random sampling to analyze 100% of interactions for compliance and training opportunities. This data-driven approach helps to clarify the role of IVR in modern contact centers, optimizing it for efficient self-service while ensuring seamless escalation.

- To justify investments, businesses are measuring ROI of conversational AI and leveraging customer journey analytics use cases to refine strategies. Ultimately, adopting technology for personalized customer interactions, supported by a cohesive unified communications platform benefits the entire enterprise, leading to efficiency gains that are often double that of siloed approaches.

What are the key market drivers leading to the rise in the adoption of Contact Center Industry?

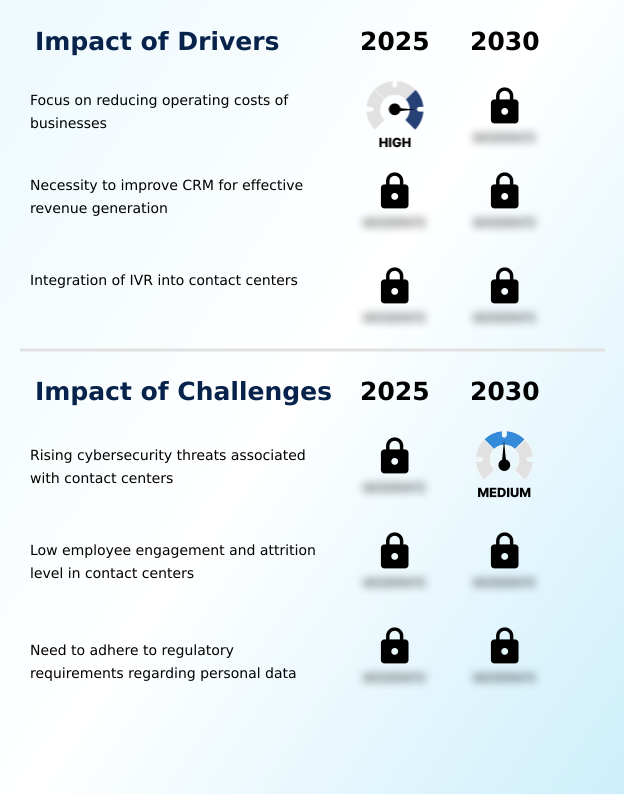

- A primary driver for the market is the sustained business focus on reducing operational costs while enhancing service quality.

- Market growth is primarily driven by the enterprise-wide mandate to enhance customer experience management while simultaneously reducing operational expenditures.

- The migration to cloud contact center platforms is a central driver, as these solutions can lower the total cost of ownership by up to 35% compared to maintaining on-premise infrastructure.

- This shift enables businesses of all sizes to access advanced capabilities like workforce management software and a unified agent desktop.

- The necessity to improve CRM for effective revenue generation is another powerful driver; deep customer relationship management integration allows for more personalized interactions and has been linked to a 25% increase in successful cross-sell and upsell opportunities.

- Furthermore, the relentless pursuit of efficiency through contact center automation and outbound dialing solutions continues to fuel investment in technologies that optimize agent productivity and resource allocation.

What are the market trends shaping the Contact Center Industry?

- The integration of chatbots into business operations represents an emerging market trend. This is primarily aimed at improving customer service turnaround times and operational efficiency.

- Key market trends revolve around the hyper-automation of customer interactions and the strategic use of AI-driven insights. The adoption of AI-powered chatbots and intelligent virtual agents continues to accelerate, with deployments successfully resolving up to 75% of tier-one inquiries without human intervention, directly improving turnaround times.

- There is a significant push towards true omnichannel customer engagement, where unified platforms that support end-to-end journey orchestration have been shown to increase customer retention by over 15% compared to multichannel approaches. Another dominant trend is the use of contact center analytics and real-time monitoring to inform business strategy.

- This data-driven approach, which includes customer sentiment tracking and post-call summarization, allows organizations to proactively identify service gaps and refine operations, driving continuous improvement and a more personalized customer experience.

What challenges does the Contact Center Industry face during its growth?

- Rising cybersecurity threats associated with the handling of sensitive customer data in contact centers present a key challenge to industry growth and stability.

- The market faces significant challenges, primarily centered on security, workforce stability, and regulatory adherence. The rising sophistication of cybersecurity threats necessitates constant investment in secure payment handling protocols and robust infrastructure, as a single data breach can have devastating financial and reputational consequences.

- Employee retention remains a critical issue, with contact centers experiencing attrition rates approaching 45% in some sectors, nearly double the average of other industries, which drives up recruitment and training costs. Navigating the complex web of compliance and data privacy regulations, such as GDPR and CCPA, is an ongoing operational burden.

- Failure to adhere to strict call recording and quality monitoring rules can result in substantial penalties. These challenges compel organizations to prioritize remote agent solutions and advanced security measures to ensure operational resilience and trustworthiness.

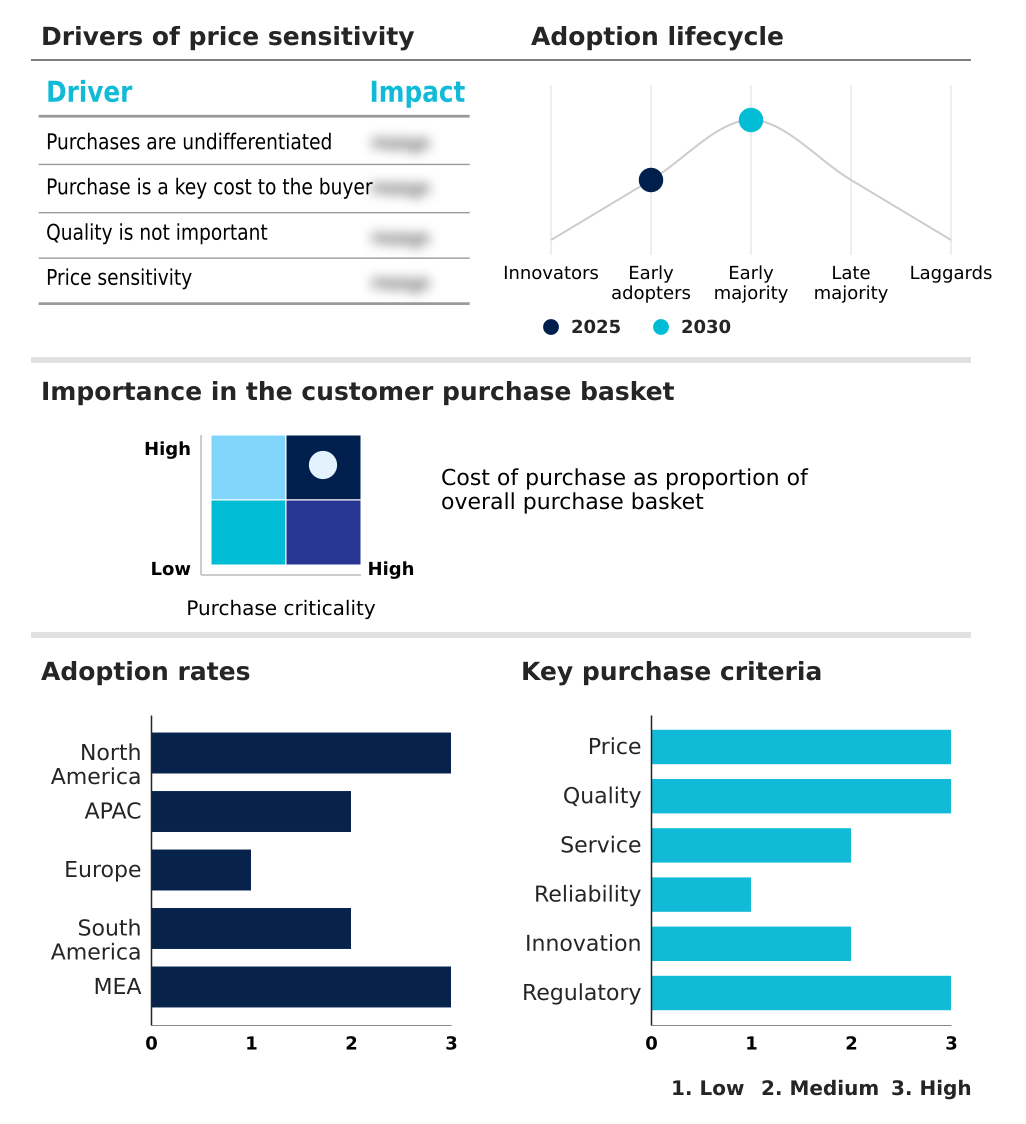

Exclusive Technavio Analysis on Customer Landscape

The contact center market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the contact center market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Contact Center Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, contact center market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

8x8 Inc. - Providers offer integrated, cloud-native contact center platforms designed to enhance customer engagement and operational efficiency through advanced, AI-powered automation and analytics.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 8x8 Inc.

- ALE International

- Alvaria Inc.

- Amazon.com Inc.

- Ameyo Pvt Ltd.

- Atos SE

- Avaya LLC

- Cisco Systems Inc.

- Enghouse Systems Ltd.

- Five9 Inc.

- Genesys Telecom Lab Inc.

- Google LLC

- Mitel Networks Corp.

- NEC Corp.

- NICE Ltd.

- SAP SE

- Vocalcom Group

- Vonage Holdings Corp.

- Zendesk Inc.

- ZTE Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Contact center market

- In August, 2025, Onix strengthened its market position through the acquisition of the UJET services business, a move designed to enhance its alignment with Google Cloud's Customer Engagement AI Suite and scale its capacity for deploying complex, AI-driven enterprise contact center solutions.

- In October, 2025, NICE introduced its AI Ops Center, a new operational control layer for the NICE Cognigy platform, providing a unified dashboard for monitoring AI agent performance, detecting bottlenecks, and ensuring system reliability across customer experience environments.

- In May, 2025, Genesys enhanced its Genesys Cloud platform by expanding its native cloud journey management capabilities, enabling organizations to gain deeper visibility into customer behavior and more effectively build, monitor, and analyze end-to-end customer interactions.

- In April, 2025, Google Cloud significantly upgraded its Contact Center AI Platform by integrating its Gemini models to power new functionalities, including an advanced Customer Engagement Suite and enhanced Agent Assist capabilities, focusing on augmenting agent performance and improving customer self-service.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Contact Center Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 11.1% |

| Market growth 2026-2030 | USD 259.3 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 10.0% |

| Key countries | US, Canada, Mexico, China, India, Japan, Philippines, Australia, Indonesia, Germany, France, UK, Spain, The Netherlands, Italy, Brazil, Argentina, Colombia, South Africa, UAE, Saudi Arabia, Egypt and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The contact center market is advancing beyond its traditional role, becoming a critical engine for enterprise-wide intelligence and customer loyalty. The pervasive integration of conversational AI and natural language processing is automating routine interactions and, more importantly, augmenting human agents.

- Boardroom decisions increasingly focus on balancing investments in workforce engagement management with robotic process automation to optimize both efficiency and employee satisfaction. The deployment of sophisticated agent assist tools, which provide real-time guidance and access to information, has demonstrated a 30% reduction in agent onboarding time and a notable improvement in net promoter score.

- This technological shift is underpinned by a transition to contact center as a service platforms built on cloud-native architecture. These platforms facilitate the use of advanced predictive analytics, speech analytics, and sentiment analysis to drive strategic initiatives. By leveraging technologies like computer telephony integration, voice biometrics, and intelligent routing, organizations are personalizing customer journey mapping.

- This focus on first call resolution and optimizing average handling time through skills-based routing and call deflection strategies is crucial for maintaining a competitive edge.

What are the Key Data Covered in this Contact Center Market Research and Growth Report?

-

What is the expected growth of the Contact Center Market between 2026 and 2030?

-

USD 259.3 billion, at a CAGR of 11.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Voice-based, Text-based, and Social media-based), Deployment (On-premises, and Cloud-based), Service (Professional services, Managed services, and Cloud-based contact center as a services) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Focus on reducing operating costs of businesses, Rising cybersecurity threats associated with contact centers

-

-

Who are the major players in the Contact Center Market?

-

8x8 Inc., ALE International, Alvaria Inc., Amazon.com Inc., Ameyo Pvt Ltd., Atos SE, Avaya LLC, Cisco Systems Inc., Enghouse Systems Ltd., Five9 Inc., Genesys Telecom Lab Inc., Google LLC, Mitel Networks Corp., NEC Corp., NICE Ltd., SAP SE, Vocalcom Group, Vonage Holdings Corp., Zendesk Inc. and ZTE Corp.

-

Market Research Insights

- Market dynamics are defined by a strategic shift toward data-driven customer insights and operational agility, powered by AI in customer service. The adoption of cloud contact center platforms is accelerating, with businesses achieving an average 20% improvement in agent productivity compared to legacy on-premise systems.

- This transition is not merely about infrastructure; it's about embedding intelligent virtual agents and contact center automation into core workflows. For instance, implementing AI-powered chatbots for initial query handling has proven to deflect up to 60% of routine inquiries, freeing human agents for more complex tasks.

- Furthermore, sophisticated contact center analytics, fueled by proactive customer outreach and customer sentiment tracking, improve first call resolution rates by more than 15%. This focus on agent performance metrics and omnichannel customer engagement is creating a more resilient and responsive service environment.

We can help! Our analysts can customize this contact center market research report to meet your requirements.

RIA -

RIA -