Clamshell Packaging Market Size 2025-2029

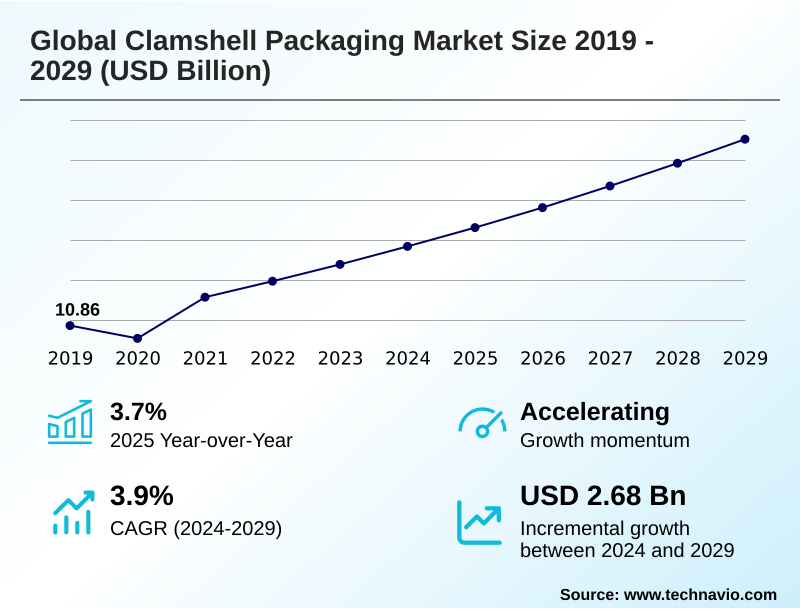

The clamshell packaging market size is valued to increase by USD 2.68 billion, at a CAGR of 3.9% from 2024 to 2029. Growth of multinational fast-food chains will drive the clamshell packaging market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 51.6% growth during the forecast period.

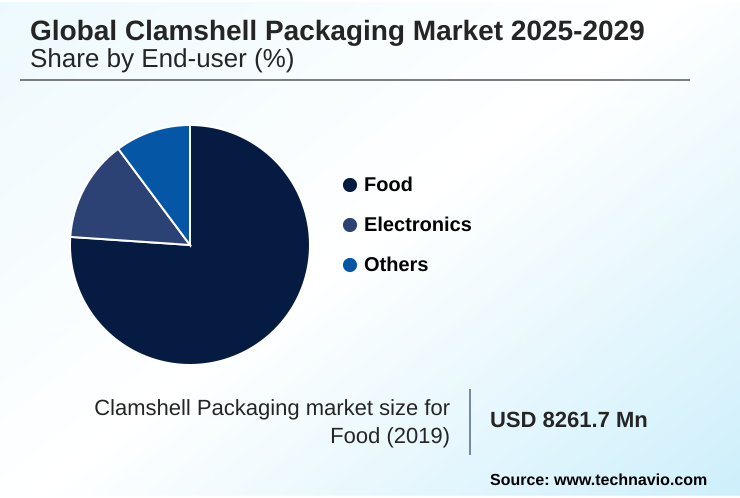

- By End-user - Food segment was valued at USD 9.55 billion in 2023

- By Type - 2-piece clamshells segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 4.66 billion

- Market Future Opportunities: USD 2.68 billion

- CAGR from 2024 to 2029 : 3.9%

Market Summary

- The clamshell packaging market is characterized by consistent growth, primarily fueled by consumer demand for convenience and product transparency, especially in the food and electronics sectors. The expansion of e-commerce and food delivery services relies heavily on tamper-evident packaging and robust designs to maintain supply chain integrity.

- A key dynamic is the industry's pivot toward sustainability, driven by regulatory pressure and consumer sentiment against single-use plastics. This has accelerated packaging material innovation, with a focus on biopolymer-based clamshells and increasing post-consumer recycled content.

- For instance, a food distributor aiming to reduce its environmental footprint must navigate the complexities of recycled material sourcing to meet both food safety compliance and sustainability goals.

- This involves validating that recycled polyethylene terephthalate (rPET) suppliers can provide consistent quality for rigid plastic thermoforming without compromising the protective qualities or clear plastic packaging that consumers expect, showcasing the balance between operational efficiency and market-driven environmental responsibility.

What will be the Size of the Clamshell Packaging Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Clamshell Packaging Market Segmented?

The clamshell packaging industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

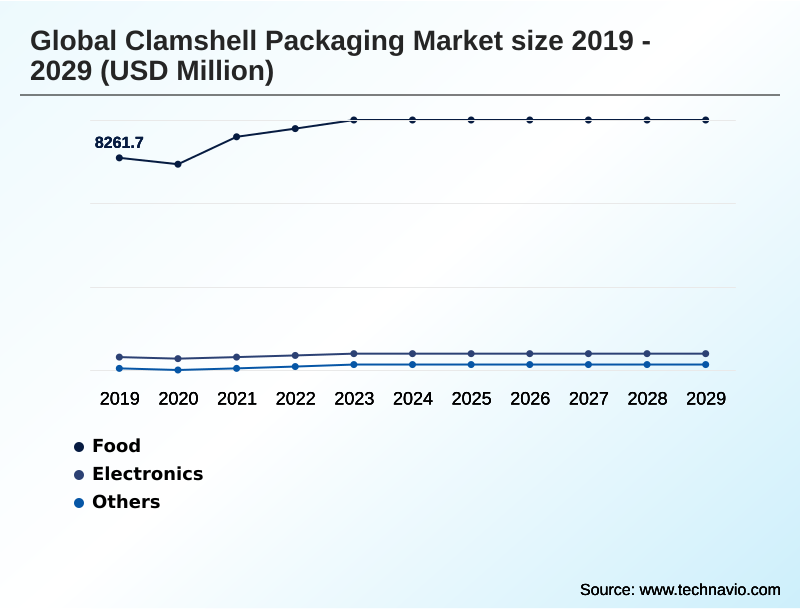

- End-user

- Food

- Electronics

- Others

- Type

- 2-piece clamshells

- Tri-fold clamshells

- Mock clamshells

- Others

- Product

- Trays

- Boxes and containers

- Bowls

- Others

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- Turkey

- Rest of World (ROW)

- APAC

By End-user Insights

The food segment is estimated to witness significant growth during the forecast period.

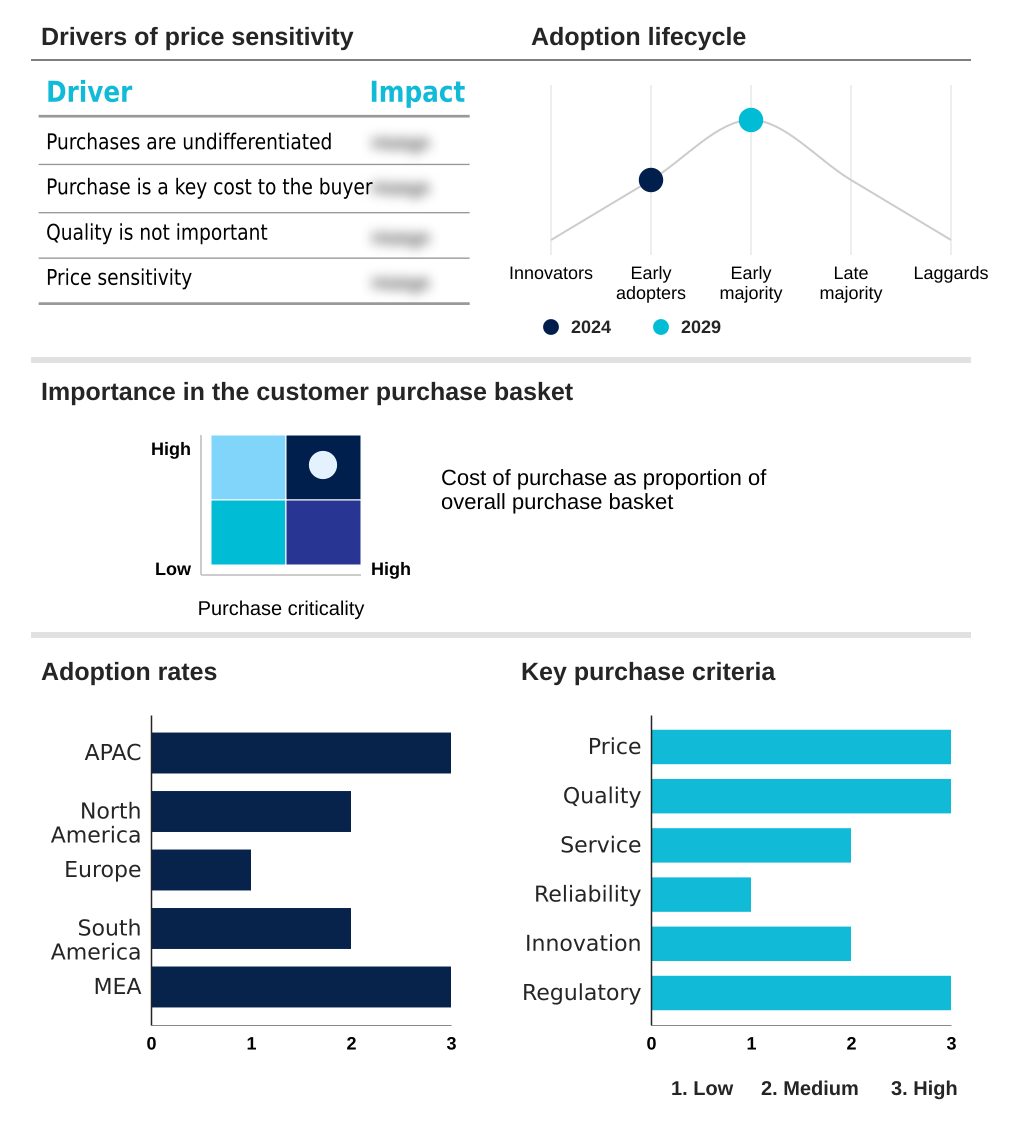

The food sector remains the principal end-user, accounting for over 62% of market volume. Demand is driven by the need for durable product protection in fresh produce packaging and packaging for convenience foods.

The format's inherent product visibility enhancement is a critical factor for consumers, directly influencing purchasing decisions and providing enhanced shelf appeal. For ready-to-eat meal packaging, clamshells offer food safety compliance and prevent food spoilage.

The use of clear plastic packaging and robust food-grade plastic containers ensures that items are protected from product damage throughout the supply chain, reinforcing consumer trust. This segment’s performance underscores the packaging’s vital role in both marketing and logistics.

The Food segment was valued at USD 9.55 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 51.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Clamshell Packaging Market Demand is Rising in APAC Get Free Sample

The geographic landscape is led by APAC, which contributes over 51% of the incremental growth, driven by rapid urbanization and the expansion of organized retail.

This region is a focal point for implementing circular economy principles to combat plastic waste reduction.

In North America, the market is mature, with growth influenced by stringent sustainable packaging regulations, including mandates for up to 25% post-consumer recycled content in certain applications. This has intensified the focus on sustainable sourcing practices and packaging lifecycle management.

Europe follows similar trends, emphasizing eco-friendly packaging options and investing in infrastructure for recyclable pet packaging to achieve environmental impact reduction. These regional dynamics highlight a global shift toward responsible packaging waste management and material circularity initiatives.

Market Dynamics

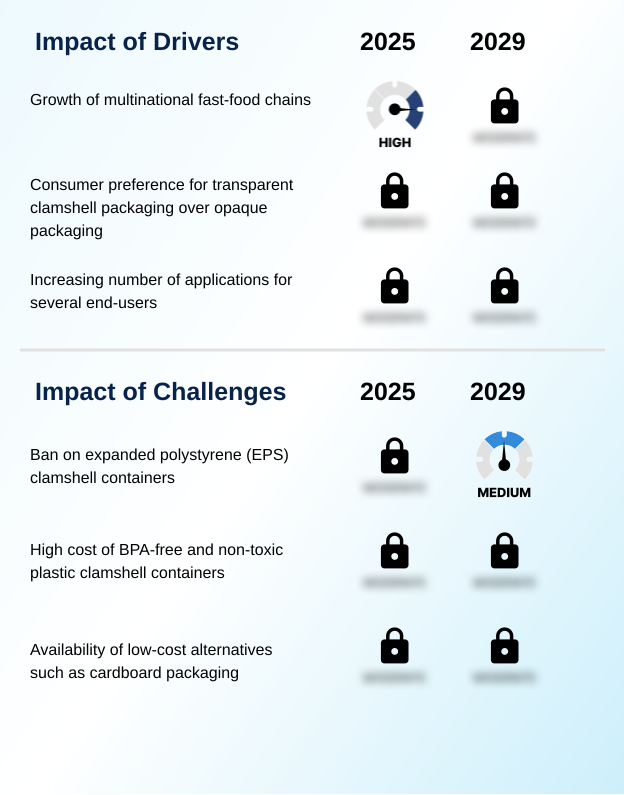

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic direction of the clamshell packaging market is increasingly shaped by complex cost-benefit analyses and regulatory pressures. The cost of bpa-free plastic clamshell containers is a significant consideration for manufacturers, weighed against the growing consumer preference for transparent vs opaque packaging.

- Concurrently, the impact of the eps foam ban on packaging choices has accelerated the demand for compostable clamshell containers in food service and innovations in bio-based and renewable packaging materials. This shift is not without its challenges, including challenges in recycling multi-material clamshells and supply chain challenges for pcr materials.

- Thermoformed plastic applications in electronics packaging continue to expand, while the growth of multinational fast-food chains' packaging needs drives demand for standardized, efficient solutions. The role of clamshell packaging in reducing food waste is a key value proposition, particularly with trends in sustainable packaging for fresh produce.

- Firms using lightweighting strategies for pet clamshells report material savings that are almost double those of five years ago. This optimization, alongside advancements in thermoforming for custom designs and integrating tamper-evident features in clamshell design, is critical for maintaining a competitive edge.

- The market is also exploring market opportunities for fiber-based clamshells to mitigate the environmental footprint of different clamshell materials.

What are the key market drivers leading to the rise in the adoption of Clamshell Packaging Industry?

- The market's growth is significantly driven by the ongoing global expansion of multinational fast-food chains.

- Market growth is strongly propelled by the demand for convenience and protection in high-volume sectors. The expansion of e-commerce packaging solutions and QSR food packaging relies heavily on the reliability of thermoformed plastic packaging.

- The inherent supply chain integrity provided by designs like the 2-piece clamshell construction with tamper-evident packaging features is critical.

- Furthermore, the push for operational efficiency is driving the adoption of high-speed thermoforming and packaging design for automation, with some companies reducing packaging labor costs by up to 30%.

- Lightweight packaging design initiatives not only reduce material usage but also lower freight expenses by as much as 15%. This combination of performance, security, and cost-effectiveness makes hinged container design and stock packaging options indispensable across multiple industries.

What are the market trends shaping the Clamshell Packaging Industry?

- The increasing demand for compostable clamshell containers, driven by heightened environmental awareness, is emerging as a significant market trend.

- Key market trends are centered on material innovation and circularity. The development of biopolymer-based clamshells and compostable packaging solutions is accelerating, driven by demand for sustainable fiber materials. Innovations in molded fiber technology are enabling the creation of plant-based fiber packaging that offers a viable alternative to plastic, with some new materials achieving over 95% compostability under industrial conditions.

- Concurrently, advancements in polymer science and chemical recycling processes are improving the viability of closed-loop recycling systems. Technologies like digital watermarking for recycling are being tested to enhance sorting accuracy, which could boost the supply of high-quality recycled materials by over 20%. These custom thermoformed solutions and smart packaging integrations are redefining what is possible in sustainable design.

What challenges does the Clamshell Packaging Industry face during its growth?

- Widespread bans on expanded polystyrene (EPS) clamshell containers present a key challenge that affects industry growth.

- A primary challenge is managing the complexities of incorporating post-consumer recycled content into rigid plastic thermoforming processes. While recycled polyethylene terephthalate is in high demand for products like bakery goods containers, inconsistent quality in feedstock from advanced sorting technologies can increase production defects by up to 10%.

- Ensuring compliance for food contact materials adds another layer of difficulty, as achieving the necessary purity standards with recycled inputs can raise processing costs by over 25%. This impacts the economic viability of using materials with high PCR content in applications like consumer electronics packaging or those requiring anti-fog packaging films.

- The need for thermoforming process optimization to handle material variability without compromising the integrity of mock clamshell design or tri-fold clamshell format remains a significant operational hurdle.

Exclusive Technavio Analysis on Customer Landscape

The clamshell packaging market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the clamshell packaging market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Clamshell Packaging Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, clamshell packaging market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amcor Plc - Vendors provide custom and stock thermoformed clamshells, emphasizing product visibility, protection, and increasingly sustainable materials to meet diverse industry requirements.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amcor Plc

- Blisterpak Inc.

- Clearpack Engineering Inc.

- Creative Plastics

- Dordan Manufacturing Co.

- Footprint

- Helmy Plastics

- Lacerta Group LLC

- Novolex

- Panic Plastics Inc.

- Parksons Packaging Ltd.

- Placon Corp.

- Plastic Ingenuity

- Prime Packaging LLC

- QPC Pack

- Sinclair and Rush Inc.

- Smurfit Kappa Group

- Sonoco Products Co.

- Universal Plastics Group Inc.

- WestRock Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Clamshell packaging market

- In September, 2024, Amcor Plc announced the launch of a new line of 100% rPET clamshells for fresh produce, achieving full circularity in partnership with a major grocery chain.

- In November, 2024, WestRock Co. completed its acquisition of a leading European molded fiber technology firm, expanding its portfolio of plastic-alternative clamshells for the food service sector.

- In February, 2025, Sonoco Products Co. unveiled a strategic partnership with a chemical recycling pioneer to create a closed-loop system for its food-grade thermoformed plastic containers, aiming to process over 50,000 tons annually.

- In April, 2025, Footprint announced it received regulatory approval in the European Union for its new plant-based, compostable material intended for frozen food clamshell applications, a major market entry milestone.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Clamshell Packaging Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 293 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 3.9% |

| Market growth 2025-2029 | USD 2682.9 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 3.7% |

| Key countries | China, Japan, India, South Korea, Australia, Singapore, US, Canada, Mexico, Germany, UK, France, Italy, Russia, Spain, Brazil, Argentina, Colombia, Saudi Arabia, UAE, Turkey, Egypt and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is undergoing a significant transformation driven by the dual pressures of performance and sustainability. Core functionalities like durable product protection and product visibility enhancement are now baseline expectations. The competitive frontier has shifted to material science, where innovations in biopolymer-based clamshells and plant-based fiber packaging are gaining traction.

- Adherence to circular economy principles is no longer optional; it is a central pillar of corporate strategy, forcing advancements in thermoforming process optimization and packaging lifecycle management. A key boardroom consideration is navigating the volatile landscape of food contact materials regulations, which directly impacts sustainable sourcing practices and the feasibility of using recycled polyethylene terephthalate.

- Firms that successfully integrate post-consumer recycled content into their food-grade plastic containers, with some achieving a 15% improvement in material efficiency through lightweight packaging design, are better positioned to capture market share. This pivot requires substantial investment in both technology and supply chain integrity to ensure food safety compliance while meeting environmental mandates.

What are the Key Data Covered in this Clamshell Packaging Market Research and Growth Report?

-

What is the expected growth of the Clamshell Packaging Market between 2025 and 2029?

-

USD 2.68 billion, at a CAGR of 3.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Food, Electronics, and Others), Type (2-piece clamshells, Tri-fold clamshells, Mock clamshells, and Others), Product (Trays, Boxes and containers, Bowls, and Others) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growth of multinational fast-food chains, Ban on expanded polystyrene (EPS) clamshell containers

-

-

Who are the major players in the Clamshell Packaging Market?

-

Amcor Plc, Blisterpak Inc., Clearpack Engineering Inc., Creative Plastics, Dordan Manufacturing Co., Footprint, Helmy Plastics, Lacerta Group LLC, Novolex, Panic Plastics Inc., Parksons Packaging Ltd., Placon Corp., Plastic Ingenuity, Prime Packaging LLC, QPC Pack, Sinclair and Rush Inc., Smurfit Kappa Group, Sonoco Products Co., Universal Plastics Group Inc. and WestRock Co.

-

Market Research Insights

- The market's dynamics are shaped by a strong consumer preference for transparency and the relentless growth of e-commerce packaging solutions, which demand robust protection. Firms leveraging advanced sorting technologies are improving material circularity initiatives, with some recycling facilities increasing PET recovery rates by over 15%. This push aligns with sustainable packaging regulations that often mandate minimum recycled content.

- Concurrently, advancements in polymer science are enabling designs that reduce material use without compromising integrity. This focus on efficiency and sustainability is evident as companies adopting these innovations report an average 10% reduction in packaging-related costs, demonstrating a clear link between environmental responsibility and financial performance in retail product display.

We can help! Our analysts can customize this clamshell packaging market research report to meet your requirements.

RIA -

RIA -