Food Service Market Size 2026-2030

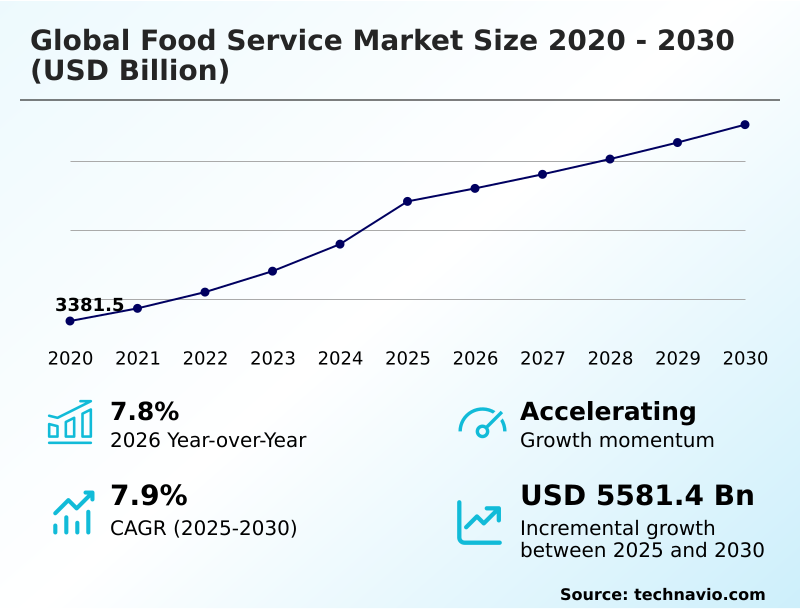

The Food Service Market size was valued at USD 12080.7 billion in 2025, growing at a CAGR of 7.9% during the forecast period 2026-2030.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 50.1% growth during the forecast period.

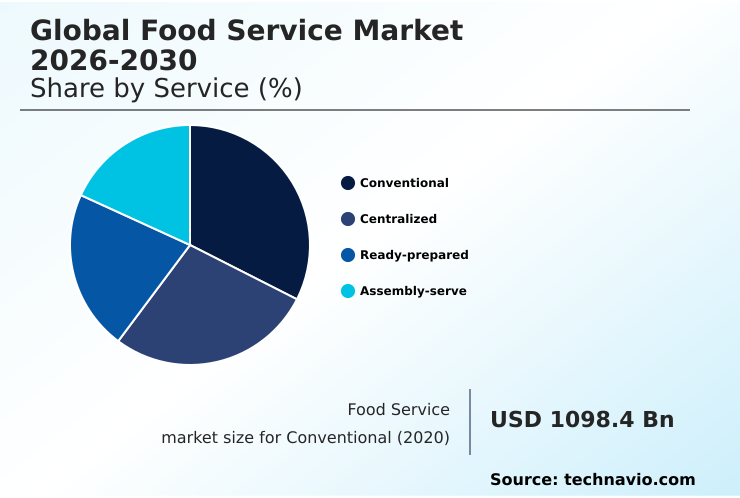

- By Service - Conventional segment was valued at USD 2783.3 billion in 2024

- By Sector - Commercial segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 14280.6 billion

- Market Future Opportunities 2025-2030: USD 5581.4 billion

- CAGR from 2025 to 2030 : 7.9%

Market Summary

- The food service market is defined by a strategic pivot towards operational efficiency, where the integration of kitchen management systems has shown to improve order accuracy by over 25%. In parallel, the adoption of contactless payment systems has accelerated, with transaction speeds increasing by 40% compared to traditional methods.

- A primary driver for this evolution is the ongoing digital transformation, which enables a data-driven approach to understanding consumer behavior and personalizing the omnichannel experience. For instance, a restaurant chain can analyze purchasing patterns from its loyalty programs to optimize menu engineering and reduce food waste.

- However, the industry grapples with the persistent challenge of chronic supply chain disruption and commodity price volatility. This forces operators to build greater supply chain resilience through supplier diversification and advanced inventory management software to mitigate the impact on food cost percentages and maintain profitability.

What will be the Size of the Food Service Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Food Service Market Segmented?

The food service industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

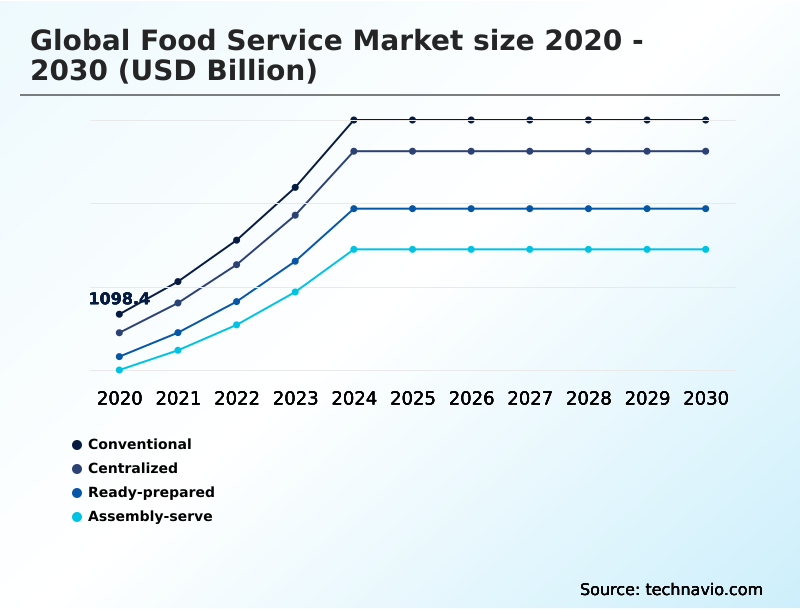

- Service

- Conventional

- Centralized

- Ready-prepared

- Assembly-serve

- Sector

- Commercial

- Non-commercial

- Type

- Full service restaurants

- Quick service restaurants

- Institutes

- Others

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- France

- UK

- Germany

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- Turkey

- UAE

- Rest of World (ROW)

- APAC

How is the Food Service Market Segmented by Service?

The conventional segment is estimated to witness significant growth during the forecast period.

The conventional service segment, where food production and service occur at the same facility, saw on-site food preparation errors decrease by 15% with the adoption of simplified menu engineering.

This model, which emphasizes made-to-order freshness, faces challenges in operational efficiency, particularly during peak hours, where labor costs are 20% higher than in centralized models.

It relies heavily on skilled culinary staff for both front-of-house and back-of-house automation, making it ideal for fine dining and full-service restaurants where customization and culinary innovation are key differentiators. The commercial segment is a key user of this model.

The Conventional segment was valued at USD 2783.3 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the Food Service market is rising in the leading region?

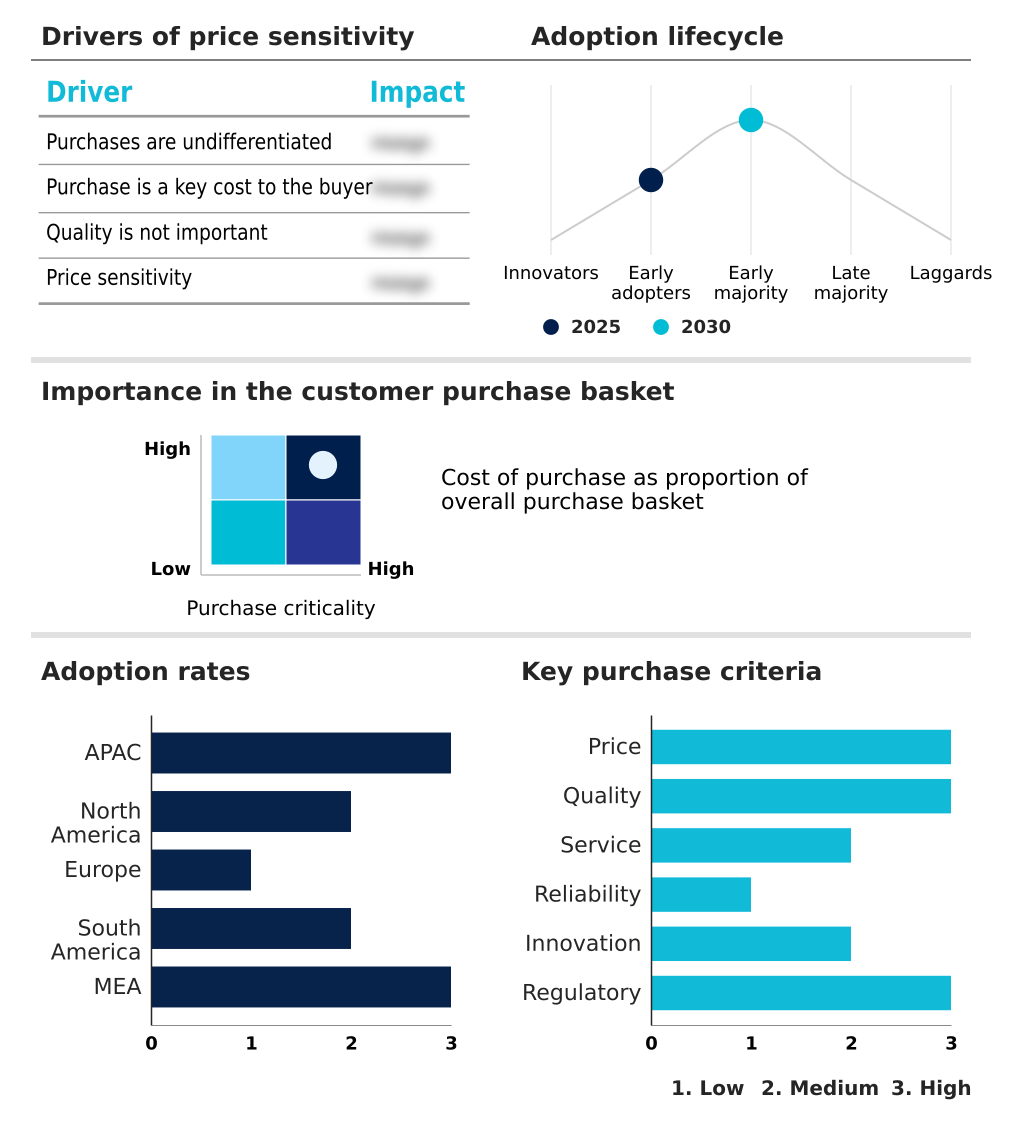

APAC is estimated to contribute 50.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Food Service Market demand is rising in APAC Request Free Sample

The global food service market exhibits significant regional disparity, with APAC poised to contribute approximately 50% of the market's incremental growth, a figure more than double that of North America's projected 20.7%.

This rapid expansion is led by countries like China, where the market size is forecast to be substantially larger than in Japan, driven by a massive consumer base and rapid urbanization.

In contrast, the mature North America market, led by the US, focuses on operational efficiency and technology adoption, such as front-of-house automation, to manage high labor costs.

This regional divergence in consumer behavior and market maturity necessitates distinct strategies for customer acquisition and supply chain management.

For instance, the demand for food to go is expanding faster in APAC's urban centers, influencing restaurant design and investment in digital storefronts and third-party delivery aggregators.

What are the key Drivers, Trends, and Challenges in the Food Service Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Understanding what is contract foodservice management has become crucial for institutions looking to streamline operations, as outsourcing can reduce food service-related capital expenditures by up to 30% compared to in-house management.

- Simultaneously, operators are exploring the benefits of virtual kitchens for restaurants, which offer a low-cost entry point into new markets with operating overheads that are often 40% lower than traditional brick-and-mortar locations.

- The operational shift is supported by technology, with inquiries into how food traceability platforms work becoming more common as businesses aim to enhance food safety and build consumer trust. This focus on backend systems underscores the importance of supply chain resilience in food service, a factor that has become as critical as menu innovation.

- The strategic discussions around the impact of off-premises dining on restaurant design are reshaping physical layouts to optimize workflows for a business model where delivery and takeaway now represent a significant and growing revenue stream.

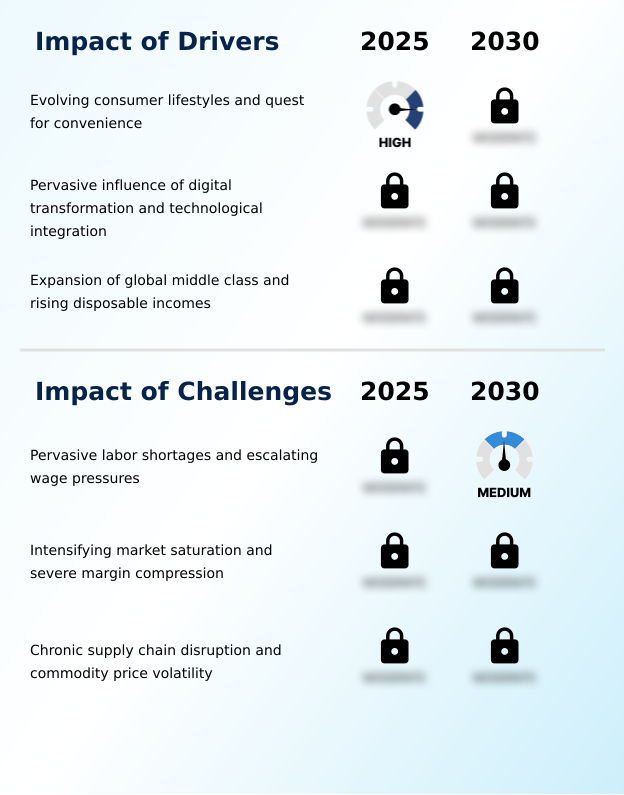

What are the key market drivers leading to the rise in the adoption of Food Service Industry?

- Evolving consumer lifestyles and the corresponding quest for convenience serve as a fundamental driver propelling market expansion.

- The pervasive influence of digital transformation is a primary driver, with the adoption of an omnichannel experience leading to a 25% increase in customer retention for early adopters.

- The integration of self-service kiosks and digital menu boards in quick service restaurants has reduced order times by an average of 30%, directly enhancing operational efficiency.

- This data-driven approach allows for hyper-personalization through loyalty programs and customer relationship management, shaping everything from menu engineering to customer acquisition strategies.

- The expansion of third-party delivery aggregators has further fueled this growth, creating new revenue streams and expanding the market for meal solutions and casual dining beyond physical locations.

- This technological integration is critical for managing food cost percentages and optimizing profitability.

What are the market trends shaping the Food Service Industry?

- The ascendancy of health, wellness, and sustainability represents a fundamental shift in consumer consciousness, establishing them as core value propositions within the industry.

- A defining trend in the food service market is the structural shift toward off-premises dining, a segment that has seen a 40% increase in volume in some urban markets, fundamentally altering operational models.

- This pivot is enabled by the adoption of virtual kitchens and ghost kitchen operations, which reduce real estate costs by up to 60% compared to traditional dining establishments. This business model relies heavily on a sophisticated technology stack, including digital storefronts and efficient supply chain management.

- Consequently, operators are investing heavily in sustainable food packaging and plant-based menu options to differentiate their brand identity in a crowded digital marketplace. The focus on prepared food and ready-to-eat meals delivered directly to consumers underscores a permanent change in consumer behavior.

What challenges does the Food Service Industry face during its growth?

- Pervasive labor shortages and escalating wage pressures present a systemic challenge that significantly impacts the industry's financial and operational stability.

- Pervasive labor shortages are a critical challenge, with turnover rates in some segments exceeding 100% annually, leading to a 15% increase in training and recruitment costs. This instability is compounded by escalating wage pressures that directly compress profit margins, a significant issue in an industry where food cost percentages are already high.

- Operators are responding by accelerating investments in front-of-house automation and back-of-house automation to mitigate labor dependency, though the initial capital outlay can be substantial. Furthermore, chronic supply chain disruption and commodity price volatility add another layer of complexity, making inventory management software and flexible menu planning essential tools for survival.

- The reliance on a strained workforce directly impacts service quality and the ability to provide a consistent dining out experience.

Exclusive Technavio Analysis on Customer Landscape

The food service market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the food service market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Food Service Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, food service market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abela and Co. LLC - The market features diverse solutions, including contract foodservice management, quick-service restaurant operations, and specialized institutional catering, addressing both commercial and non-commercial sector needs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abela and Co. LLC

- Aramark

- Compass Group Plc

- Costa Coffee

- Delaware North Companies Inc.

- Dominos Pizza Inc.

- Eurest USA

- Honeybee Foods Corp.

- Maschio Food Services Inc.

- McDonald Corp.

- MOS Food Services Inc.

- Papa Johns International Inc.

- Performance Food Group Co.

- Restaurant Brands Inc.

- SGS SA

- Sodexo SA

- Starbucks Corp.

- Sysco Corp.

- The Wendys Co.

- Tim Hortons USA Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the hotels, resorts and cruise lines industry, the widespread adoption of AI-powered smart room technology, enabling voice-controlled amenities, has created new opportunities for integrated in-room food service ordering, impacting menu engineering and delivery logistics.

- The increasing consumer interest in cruise travel as a primary vacation choice has spurred demand for diverse and high-quality onboard dining options, driving growth for contract foodservice management providers specializing in maritime hospitality.

- A growing number of quick service restaurants being established within resort properties and travel hubs is expanding the footprint of casual dining options, directly influencing consumer dining out habits during leisure travel.

- The rise in online travel agencies and digital booking platforms has led to hotels and resorts bundling accommodation with dining packages and loyalty programs, requiring sophisticated customer relationship management to personalize food service offers.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Food Service Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 309 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.9% |

| Market growth 2026-2030 | USD 5581.4 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.8% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, France, UK, Germany, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, Turkey, UAE, South Africa and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The food service market ecosystem is a complex network where raw material suppliers provide commodities to centralized production units, which achieve up to 35% cost savings through economies of scale. These goods are then distributed through channels to commercial and non-commercial operators. The commercial segment, comprising 80% of the market, includes everything from quick service restaurants to fine dining establishments.

- Regulatory bodies enforce stringent food safety standards, while technology providers offer solutions like point of sale systems and kitchen management software that are integral to operational efficiency. The value chain culminates with end-users whose preferences for convenience and digital integration drive innovation.

- Supporting entities, including logistics firms and R&D organizations, are crucial for supply chain resilience and culinary innovation, ensuring the industry can adapt to evolving consumer demands.

What are the Key Data Covered in this Food Service Market Research and Growth Report?

-

What is the expected growth of the Food Service Market between 2026 and 2030?

-

The Food Service Market is expected to grow by USD 5581.4 billion during 2026-2030, registering a CAGR of 7.9%. Year-over-year growth in 2026 is estimated at 7.8%%. This acceleration is shaped by evolving consumer lifestyles and quest for convenience, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Service (Conventional, Centralized, Ready-prepared, and Assembly-serve), Sector (Commercial, and Non-commercial), Type (Full service restaurants, Quick service restaurants, Institutes, and Others) and Geography (APAC, North America, Europe, South America, Middle East and Africa). Among these, the Conventional segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC, North America, Europe, South America and Middle East and Africa. APAC is estimated to contribute 50.1% to market growth during the forecast period. Country-level analysis includes China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, France, UK, Germany, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, Turkey, UAE, South Africa and Egypt, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is evolving consumer lifestyles and quest for convenience, which is accelerating investment and industry demand. The main challenge is pervasive labor shortages and escalating wage pressures, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Food Service Market?

-

Key vendors include Abela and Co. LLC, Aramark, Compass Group Plc, Costa Coffee, Delaware North Companies Inc., Dominos Pizza Inc., Eurest USA, Honeybee Foods Corp., Maschio Food Services Inc., McDonald Corp., MOS Food Services Inc., Papa Johns International Inc., Performance Food Group Co., Restaurant Brands Inc., SGS SA, Sodexo SA, Starbucks Corp., Sysco Corp., The Wendys Co. and Tim Hortons USA Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The global food service market's competitive landscape is highly fragmented, with the top ten players, including McDonald Corp. and Starbucks Corp., accounting for less than 20% of the total market share. This environment fosters intense rivalry, compelling vendors to innovate continuously.

- A key development is the strategic partnership between major chains and technology firms, such as the collaboration to deploy generative AI and cloud solutions across thousands of restaurants, aiming to boost operational efficiency by 15%. Simultaneously, sustainability has become a critical differentiator.

- Leading coffeehouse chains are driving this shift by becoming the first to accept reusable cups for all order types, a move projected to divert millions of cups from landfills. These initiatives reflect a broader industry adaptation to challenges like market saturation and evolving consumer values, pushing companies like Compass Group Plc and Sodexo SA to refine their service models.

We can help! Our analysts can customize this food service market research report to meet your requirements.

RIA -

RIA -