Clay Brick Market Size 2024-2028

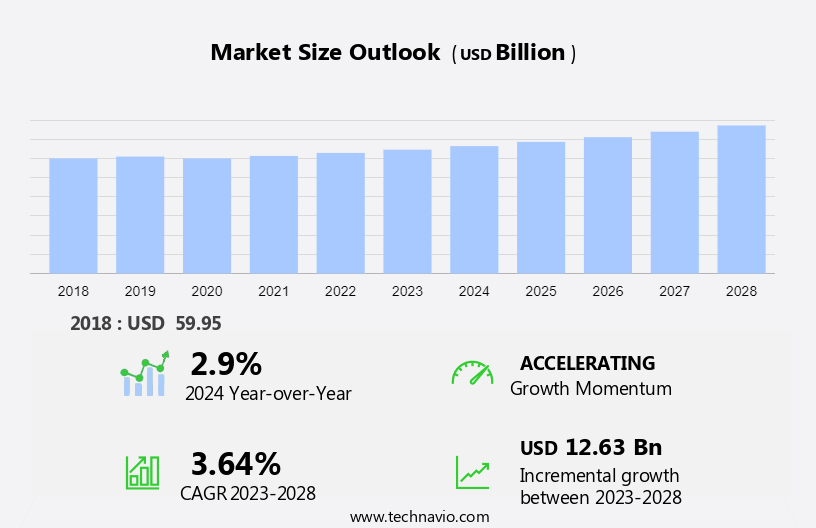

The clay brick market size is forecast to increase by USD 12.63 billion at a CAGR of 3.64% between 2023 and 2028.

- The market is experiencing significant growth, driven by the expansion of the construction industry and infrastructure development. Government policies promoting the use of load-bearing walls and BTK (Brick-on-Edge) techniques in construction further boost market demand. Engineered wood products, such as laminated veneer lumber (LVL), particleboard, and oriented strand board (OSB), are increasingly being adopted in the construction sector. Advanced firing technologies, such as German technology, are being adopted to enhance the strength and durability of clay bricks, making them a cost-effective and attractive option for builders. However, raw material scarcity poses a challenge to market growth. Several industry players are investing in innovative solutions to address this issue. This analytical depiction highlights investment opportunities in the market, with a focus on advanced technologies and sustainable production methods.

What will be the Size of the Market During the Forecast Period?

- The market plays a significant role in the building materials sector, contributing to various architectural styles and sustainable construction projects. This market encompasses the production and supply of clay bricks, which are eco-friendly materials, suitable for both residential and commercial applications. Clay bricks are produced using a traditional process that involves shaping and firing clay. This process is energy-efficient and results in a durable, long-lasting product. The versatility of clay bricks allows for size-based segmentation, including modular bricks, standard bricks, and jumbo bricks, catering to diverse project requirements.

- Clay bricks are increasingly being used in exterior facades, interior spaces, and functional landscapes due to their adaptability and aesthetic appeal. They are popular in residential properties, commercial buildings, infrastructure projects, pathways, and landscaping. Energy efficiency is a crucial factor driving the growth of the market. The thermal mass properties of clay bricks help regulate indoor temperatures, reducing the need for excessive heating or cooling. This contributes to the overall energy efficiency of buildings and aligns with the growing focus on sustainable construction. Sustainable construction and eco-friendly materials are key trends in the building industry. Clay bricks, being a natural and renewable resource, are an ideal choice for projects aiming to minimize their carbon footprint.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

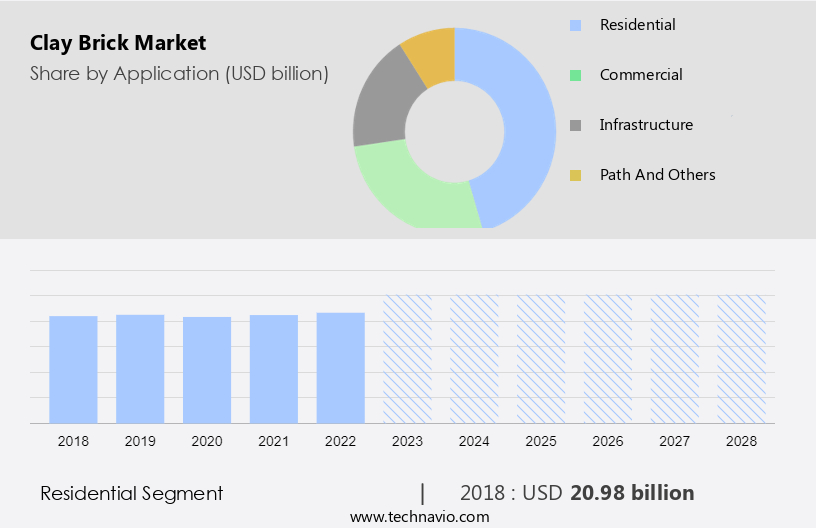

- Application

- Residential

- Commercial

- Infrastructure

- Path and others

- Type

- Solid

- Paver and facing

- Hollow

- Geography

- APAC

- China

- India

- Europe

- UK

- North America

- US

- Middle East and Africa

- South America

- APAC

By Application Insights

- The residential segment is estimated to witness significant growth during the forecast period.

Clay bricks continue to be a popular choice in the residential construction market due to their durability, strength, and insulation properties. These bricks are widely used in building single-family homes, apartments, and other housing structures. Their classic, earthy appearance adds to the visual appeal of residential properties. The clay brick industry in the US is expected to witness growth, particularly in the modular segment, as there is a rising demand for sustainable and cost-effective construction solutions. Competitive intensity in the market is high, with various firing technologies used to produce clay bricks. However, environmental concerns and the push for sustainable practices are driving the adoption of advanced technologies and methods in the production process.

Furthermore, these sustainable practices not only help reduce the carbon footprint but also offer cost savings in the long run. According to market estimations, the market is projected to expand in the coming years. The residential segment is expected to generate significant revenue due to the increasing preference for energy-efficient and durable building materials. Clay bricks' thermal properties help regulate indoor temperatures, making them an attractive option for homeowners seeking to reduce energy consumption and save on heating and cooling costs.

Get a glance at the market report of share of various segments Request Free Sample

The residential segment was valued at USD 20.98 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

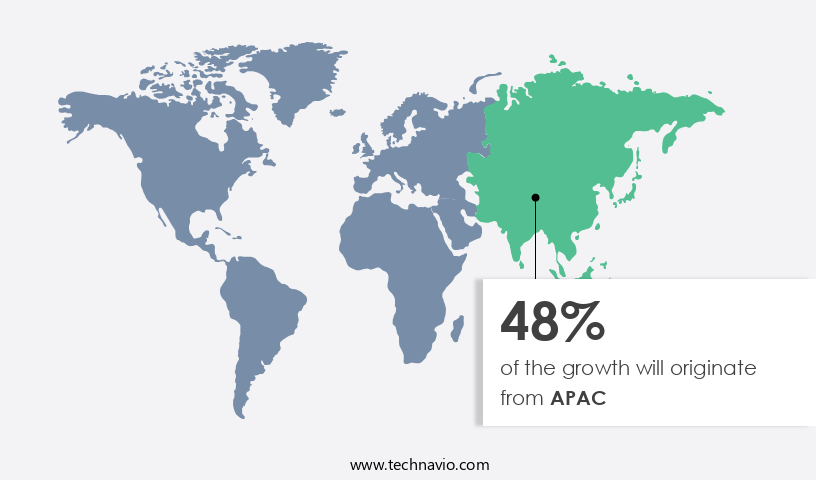

- APAC is estimated to contribute 48% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The construction sector in the Asia Pacific (APAC) region is experiencing substantial expansion, fueled by urbanization trends and the need for affordable housing solutions. This growth is driving demand in the market, as clay bricks remain a popular and cost-effective choice for residential construction. With increasing populations and urban migration, there is a heightened requirement for new housing and commercial spaces. Furthermore, governments in APAC countries, such as India and China, are investing significantly in infrastructure development, including roads, bridges, and public facilities, which in turn boosts the demand for clay bricks. The sustainable production process of clay bricks makes them an attractive option for the construction industry, as they offer a solution to habitat disruption caused by industrialization and project timelines.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Clay Brick Market?

The affordability and cost-effectiveness of clay bricks is the key driver of the market.

- Clay bricks are a popular and economical choice for builders and construction projects in the United States due to their competitive pricing. The affordability of clay bricks is primarily attributed to their low production costs and the abundance of clay as a primary raw material. This cost-effectiveness makes clay bricks an attractive option for builders seeking to minimize construction expenses without compromising quality. Clay bricks come in various sizes, including standard, modular, and jumbo, catering to diverse architectural styles and sustainable construction projects. The clay production process is energy-efficient, making clay bricks an eco-friendly building material.

- The size-based segmentation of clay bricks allows builders to select the most suitable option for their project, ensuring optimal use of resources and cost savings. In regions with easy access to clay deposits, the production of clay bricks is more cost-effective due to the reduced transportation costs of raw materials. The use of clay bricks contributes to energy efficiency and sustainable construction, making them an excellent choice for environmentally-conscious builders and homeowners. By incorporating clay bricks into their projects, builders can deliver durable and reliable structures while maintaining cost control.

What are the market trends shaping the Clay Brick Market?

The growing adoption of advanced firing technologies in clay brick production is the upcoming trend in the market.

- In the Construction Industry, the adoption of advanced firing technologies for clay brick manufacturing is a significant trend. These technologies, including high-efficiency kilns and firing processes, contribute to both cost savings and sustainability. By minimizing energy consumption during production, these methods align with environmental goals and help clay brick manufacturers comply with emissions standards. Advanced firing technologies enable precise control over temperature and atmosphere conditions, resulting in high-quality clay bricks with consistent properties.

- This level of optimization is crucial for meeting regulatory requirements and enhancing overall product quality. Infrastructure Development and Government Policies are driving the growth of the market, and companies are investing in German Technology to stay competitive. Despite raw material scarcity, the market presents numerous investment opportunities.

What challenges does Clay Brick Market face during the growth?

Competition from alternative building materials is a key challenge affecting the market growth.

- Concrete masonry units, or concrete blocks, serve as a viable alternative to clay bricks in the US construction industry. Manufactured from concrete, these blocks offer superior durability and strength. The adaptability of concrete blocks is evident in their extensive use in various building projects, including residential properties, commercial buildings, and infrastructure projects. Aerated Autoclaved Concrete (AAC) is a lightweight precast concrete option that boasts excellent insulation properties. Its low density, thermal efficiency, and ease of construction make it a preferred choice for modern building designs.

- These materials offer sustainability advantages and are versatile in their applications. The use of engineered wood products in exterior facades, interior spaces, functional landscapes, and pathways is on the rise, presenting competition for traditional clay bricks. In summary, concrete blocks and engineered wood products cater to the US construction industry's demand for durable, sustainable, and versatile building materials. AAC concrete blocks and engineered wood products, such as LVL, particleboard, and OSB, provide excellent insulation, lightweight properties, and ease of construction, making them popular alternatives to clay bricks in various applications.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market. The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Apollo Brick SA

- Berkshire Hathaway Inc.

- Bharat Bricks Co.

- Bowerston Shale Co.

- Brampton Brick Ltd.

- Brickworks Ltd.

- Ceramica Fanelli

- Forterra Building Products Ltd.

- Henry Brick

- Ibstock Plc

- Jindal Mechno Bricks Pvt. Ltd.

- Nitterhouse Masonry products LLC

- Pacific Clay Products Inc.

- Palmetto Brick Co.

- Ragland Clay Products LLC

- Rajasree Corp.

- Saudi Ceramic Co.

- Summit Brick Co.

- Taylor Clay Products Inc.

- The Belden Brick Co.

- US BRICK

- Vandersanden Steenfabrieken N.V.

- Wienerberger AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is a significant segment of the building materials industry, renowned for its versatility and eco-friendliness. Architectural styles ranging from contemporary to traditional continue to incorporate clay bricks in exterior facades, interior spaces, and functional landscapes. Sustainable construction and energy efficiency are key drivers, with clay bricks offering excellent thermal properties and emissions standards compliance. Size-based segmentation includes modular bricks, standard bricks, and jumbo bricks, catering to various construction projects, from residential properties to commercial buildings, infrastructure projects, pathways, and landscaping. Adaptability to diverse applications, load-bearing walls, and BTK techniques make clay bricks a competitive edge in the construction sector.

Furthermore, raw material scarcity and rising production costs have led to the adoption of advanced technologies, for optimization and emission reduction. Sustainable sourcing and recycling practices are essential for reducing waste and minimizing environmental impact. Competitive intensity in the market is high, with investment opportunities in the residential segment, particularly in revenue growth and affordable housing projects. Environmental concerns and sustainable practices are crucial factors, with cost savings, energy consumption, and concrete bricks growth driving the modular segment's expansion. Construction projects, urbanization trends, and industrial sector development continue to fuel market growth. Alternative materials and sustainable solutions are essential for a competitive advantage, with marketing strategies focusing on emission reduction, recycling efforts, and competitive edge.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

167 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.64% |

|

Market Growth 2024-2028 |

USD 12.63 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

2.9 |

|

Key countries |

US, China, India, Indonesia, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -