Cloud-based AI Model Training Market Size 2026-2030

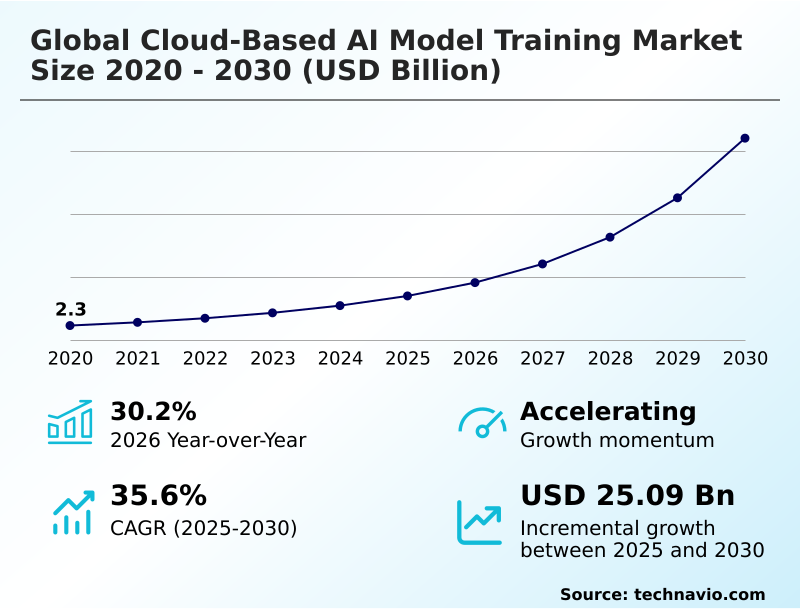

The cloud-based ai model training market size is valued to increase by USD 25.09 billion, at a CAGR of 35.6% from 2025 to 2030. Industrialization of sovereign AI and regional cloud ecosystems will drive the cloud-based ai model training market.

Major Market Trends & Insights

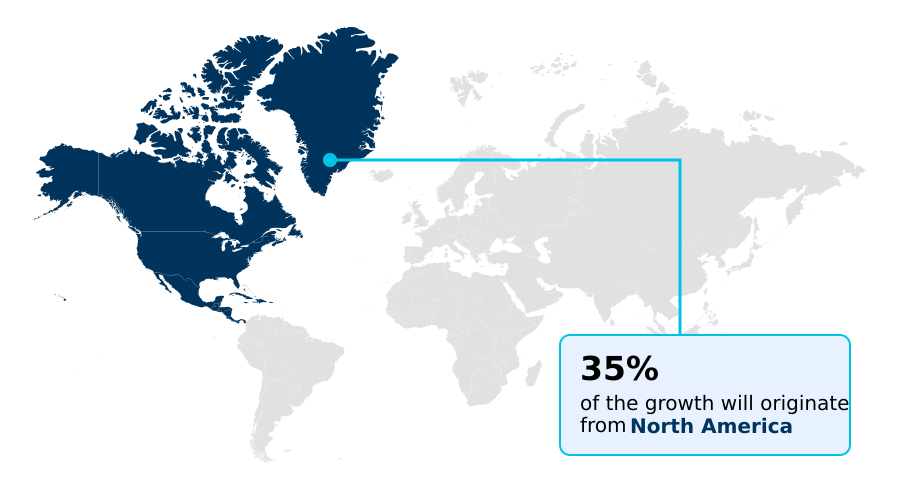

- North America dominated the market and accounted for a 35.3% growth during the forecast period.

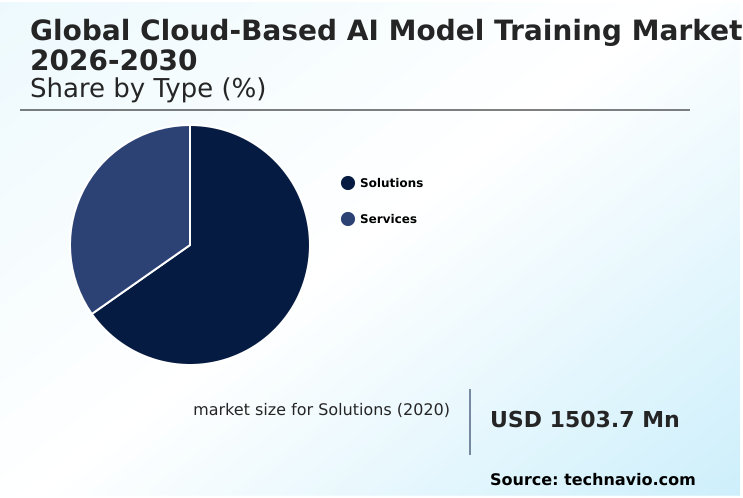

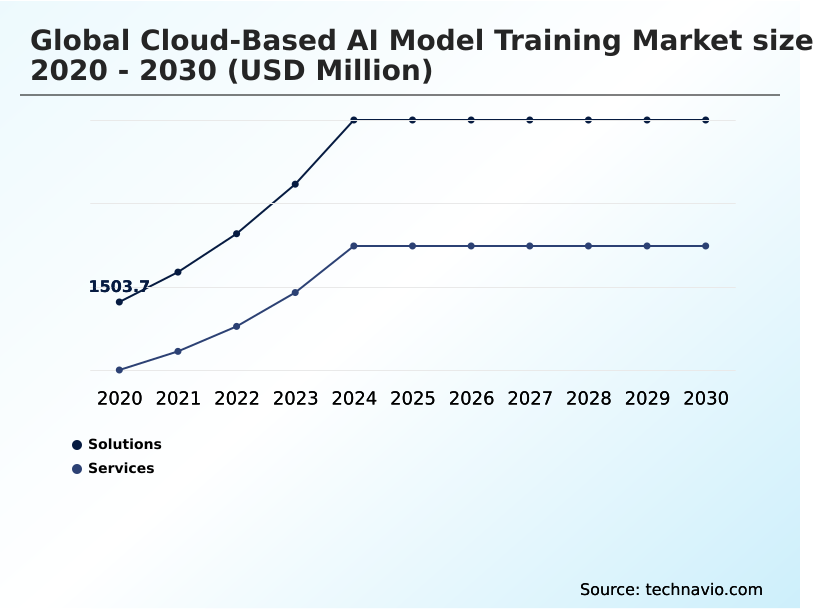

- By Type - Solutions segment was valued at USD 3.39 billion in 2024

- By Deployment - Public cloud segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 29.80 billion

- Market Future Opportunities: USD 25.09 billion

- CAGR from 2025 to 2030 : 35.6%

Market Summary

- The Cloud-Based AI Model Training Market is undergoing a significant transformation, driven by the need for immense computational intensity to power generative AI development. This shift requires high-performance computing clusters and elastic scaling capabilities beyond what traditional on-premise solutions can offer.

- A key driver is the rise of sovereign AI initiatives, compelling organizations to adopt regional cloud ecosystems to comply with strict data sovereignty mandates. For instance, a multinational logistics firm must leverage localized training farms to fine-tune its supply chain optimization models, ensuring that regional customer data adheres to data residency laws while still benefiting from advanced parallel computing.

- This scenario highlights the complex interplay between technological advancement and regulatory hurdles. Trends like multi-cloud orchestration and the use of containerization tools are emerging as solutions to mitigate vendor lock-in.

- However, the industry faces persistent challenges, including semiconductor supply fragility and the thermal management complexity of high-density GPU clusters, which strain power grid constraints and threaten to slow the pace of innovation.

What will be the Size of the Cloud-based AI Model Training Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Cloud-based AI Model Training Market Segmented?

The cloud-based ai model training industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Solutions

- Services

- Deployment

- Public cloud

- Private cloud

- Hybrid cloud

- Technology

- Machine learning

- Deep learning

- Natural language processing

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Type Insights

The solutions segment is estimated to witness significant growth during the forecast period.

The solutions segment is the market's technological core, offering integrated platforms and infrastructure defined by high-performance computing clusters and specialized AI accelerators like graphics processing units (GPUs).

A clear shift toward modular AI-native infrastructure is underway to manage increasing computational intensity and support complex generative AI development. These hardware-driven cloud solutions are essential for the elastic scaling required for modern workloads.

The expansion of sovereign AI initiatives and related data sovereignty mandates has compelled providers to establish localized solutions. Compliant organizations utilizing these regional platforms have reported up to a 45% reduction in training times.

This trend directly addresses the need for ethical AI governance while navigating the complexities of international supply chains for critical components and mitigating geopolitical tensions.

The Solutions segment was valued at USD 3.39 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cloud-based AI Model Training Market Demand is Rising in North America Get Free Sample

The geographic landscape is fragmenting due to stringent data residency laws, driving the creation of AI superfactories within national borders.

North America leads in deploying tensor processing units (TPUs) for mixture-of-experts (MoE) models, but Europe is pioneering sovereign infrastructure with neoclouds GPU clusters to ensure compliance.

These regional hubs leverage liquid-cooled server architectures and improved system-level power delivery to manage the intense energy demands, with some sustainable facilities reducing power consumption by 12%.

The use of differential privacy techniques and model interoperability frameworks allows for secure, cross-border collaboration.

In APAC, the focus is on MLOps automated retraining for mobile-first applications, with adoption rates for automated pipelines increasing by over 40% in the last year, showcasing a global move toward enterprise automation autonomy.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic imperative for enterprises is navigating the complex landscape of AI development, which requires a multifaceted approach. A primary focus is on cloud-based training for sovereign AI, a necessity driven by new regulations that mandate how data is handled. This intersects with the push toward the generative AI foundation model industrialization, where scale and efficiency are paramount.

- To support this, organizations are demanding real-time scaling for agentic AI, enabling autonomous systems to function effectively. Achieving this requires robust multi-cloud orchestration for model interoperability, which prevents vendor lock-in and optimizes costs. Concurrently, there is a strong push for energy-aware training with GreenOps metrics, as firms face pressure to build sustainable operations.

- Internally, data center operators are focused on managing thermal complexity in GPU clusters and managing power grid constraints for datacenters. These operational challenges are compounded by the difficulty of overcoming semiconductor supply chain fragility. Architecturally, a key goal is ensuring data residency with sovereign clouds, often achieved using federated learning for data privacy.

- The underlying technology relies on high-performance computing for parameter models and advanced CoWoS packaging for AI accelerators. For development teams, implementing MLOps for automated model retraining through containerization for workload portability is standard practice. Techniques like optimizing training with parallel computing and using infrastructure for mixture-of-experts models are critical for performance.

- The adoption of AI-native infrastructure for on-demand compute and serverless platforms for model fine-tuning provides flexibility, while bare-metal environments for training latency reduction, which can be 15% faster than virtualized instances for specific tasks, offer a competitive edge. This holistic strategy, from infrastructure choices like liquid cooling for server architecture to development practices, defines success in the current environment.

What are the key market drivers leading to the rise in the adoption of Cloud-based AI Model Training Industry?

- The industrialization of sovereign AI and the strategic growth of regional cloud ecosystems are key market drivers, addressing demands for data residency and national digital autonomy.

- A major driver is the industrialization of sovereign AI initiatives, compelling the construction of regional AI superfactories to ensure data compliance. This has led to a surge in demand for hardware-driven cloud solutions that support localized operations.

- The strategic evolution toward agentic AI systems is another powerful force, necessitating real-time infrastructure scaling and modular AI-native infrastructure.

- Businesses are achieving a new level of enterprise automation autonomy, with deployments of CI/CD pipelines for AI models growing by over 50% year-over-year.

- Despite international supply chains facing advanced packaging bottlenecks, the demand for elastic scaling continues to fuel market expansion, as companies seek the agility to train models on demand.

What are the market trends shaping the Cloud-based AI Model Training Industry?

- The development of multi-cloud orchestration and model interoperability frameworks is an upcoming market trend, driven by the need to prevent vendor lock-in and enhance operational resilience.

- A primary trend is the adoption of multi-cloud orchestration and containerization tools to mitigate geopolitical tensions and achieve national digital autonomy. This move toward AI-native infrastructure allows for generative AI development across various providers, with some firms seeing a 20% cost optimization through strategic workload placement.

- Another key development is the institutionalization of ethical AI governance and the use of integrated risk oversight tools, which are now a prerequisite for over 70% of enterprise AI projects. The proliferation of serverless training platforms is democratizing access to specialized AI accelerators and high-speed interconnect fabrics, enabling smaller firms to engage in foundation model development without massive upfront investment.

- These trends collectively foster a more resilient and accessible innovation ecosystem.

What challenges does the Cloud-based AI Model Training Industry face during its growth?

- The escalation of data sovereignty mandates, which contributes to regional training fragmentation, presents a key challenge affecting the cost and complexity of global market penetration.

- A primary challenge is the extreme thermal management complexity of high-density GPU clusters, where power requirements have escalated by over 800%, straining regional power grid constraints. This has forced providers to invest heavily in on-site renewable energy and advanced cooling, inflating costs by up to 25%.

- Another significant hurdle is persistent semiconductor supply fragility, particularly in the production of Chip-on-Wafer-on-Substrate (CoWoS) packages and high-bandwidth memory, leading to long lead times. Furthermore, data sovereignty mandates necessitate the creation of inefficient localized training farms, fragmenting jurisdictional infrastructure and hindering the economies of scale.

- Even with the adoption of GreenOps performance metrics, the sheer computational intensity of modern AI makes sustainable scaling a persistent challenge.

Exclusive Technavio Analysis on Customer Landscape

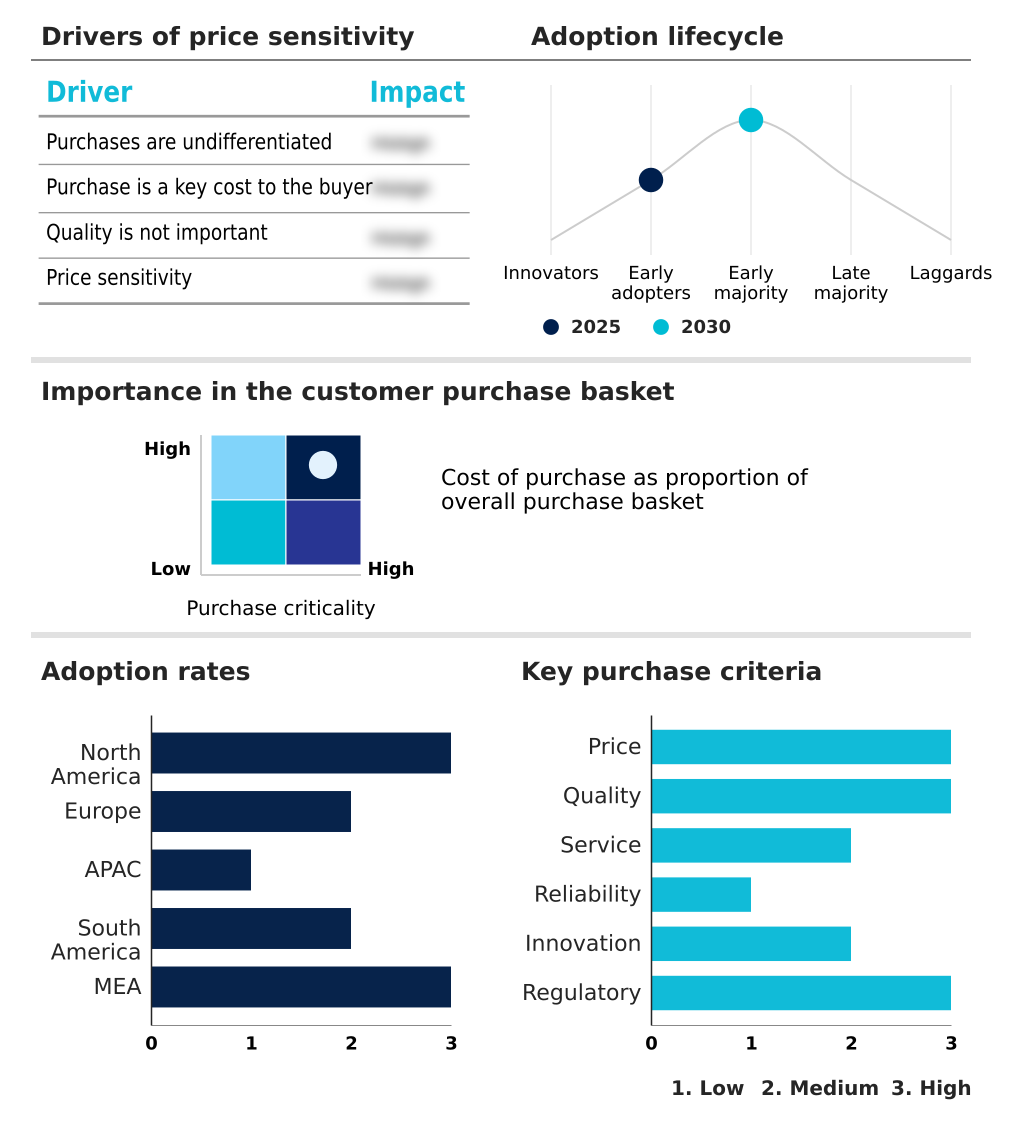

The cloud-based ai model training market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cloud-based ai model training market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cloud-based AI Model Training Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cloud-based ai model training market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alibaba Cloud - Offers elastic compute services and a machine learning platform, enabling scalable AI model development and training for enterprise-grade applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alibaba Cloud

- Amazon Web Services Inc.

- Baidu Inc.

- CoreWeave Inc

- Cyfuture India Pvt Ltd

- Databricks Inc.

- Fractal Analytics Pvt. Ltd.

- Google LLC

- Huawei Technologies Co. Ltd.

- Hugging Face Inc.

- IBM Corp.

- Infosys Ltd.

- Lambda Inc.

- Microsoft Corp.

- NVIDIA Corp.

- Oracle Corp.

- SenseTime Group Inc.

- Tata Elxsi Ltd.

- Tencent Holdings Ltd.

- V7 Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cloud-based ai model training market

- In May 2025, Hewlett Packard Enterprise launched HPE Private Cloud AI, a turnkey solution co-developed with NVIDIA to streamline secure, enterprise-grade AI workload deployment.

- In January 2026, Google Cloud advanced its offerings by expanding the Gemini Enterprise Agent Ready (GEAR) program, a service pathway for developing enterprise-grade autonomous agents.

- In March 2026, Amazon Web Services Inc. announced a major expansion of its NVIDIA-based infrastructure, with plans to deploy over one million GPUs, including Blackwell and Rubin architectures.

- In March 2026, CoreWeave expanded its global footprint with new high-performance data centers designed to support NVIDIA Blackwell architectures for large-scale training workloads.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cloud-based AI Model Training Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 294 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 35.6% |

| Market growth 2026-2030 | USD 25092.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 30.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's evolution is defined by a strategic pivot to hardware-driven cloud solutions to power industrial-scale generative AI development and the training of multi-trillion parameter models. Boardroom discussions now prioritize investment in sovereign AI initiatives and regional cloud ecosystems that ensure localized data residency through sovereign AI clouds and specialized neoclouds GPU clusters.

- Architecturally, this involves deploying high-performance computing clusters with graphics processing units (GPUs), tensor processing units (TPUs), and other specialized AI accelerators. Success hinges on techniques like advanced parallel computing, neural network optimization, and model sharding strategies, especially for complex mixture-of-experts (MoE) models. The emergence of agentic AI systems is driving demand for real-time infrastructure scaling via modular AI-native infrastructure.

- For developers, MLOps automated retraining and CI/CD pipelines, managed with containerization tools and universal management layers for multi-cloud orchestration, are now standard. These model interoperability frameworks are crucial for flexibility. Sustainability is addressed through energy-aware training protocols, GreenOps performance metrics, temporal-shifting, and liquid-cooled server architectures, while security is enhanced with federated learning and differential privacy techniques.

- Despite supply chain bottlenecks in CoWoS, high-bandwidth memory, and silicon interposer layers, the adoption of serverless training platforms is democratizing access, with some platforms reducing manual tuning for neural network optimization by over 30%.

What are the Key Data Covered in this Cloud-based AI Model Training Market Research and Growth Report?

-

What is the expected growth of the Cloud-based AI Model Training Market between 2026 and 2030?

-

USD 25.09 billion, at a CAGR of 35.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Solutions, and Services), Deployment (Public cloud, Private cloud, and Hybrid cloud), Technology (Machine learning, Deep learning, and Natural language processing) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Industrialization of sovereign AI and regional cloud ecosystems, Escalation of data sovereignty mandates and regional training fragmentation

-

-

Who are the major players in the Cloud-based AI Model Training Market?

-

Alibaba Cloud, Amazon Web Services Inc., Baidu Inc., CoreWeave Inc, Cyfuture India Pvt Ltd, Databricks Inc., Fractal Analytics Pvt. Ltd., Google LLC, Huawei Technologies Co. Ltd., Hugging Face Inc., IBM Corp., Infosys Ltd., Lambda Inc., Microsoft Corp., NVIDIA Corp., Oracle Corp., SenseTime Group Inc., Tata Elxsi Ltd., Tencent Holdings Ltd. and V7 Ltd.

-

Market Research Insights

- Market dynamics reflect a push toward national digital autonomy, fueled by data sovereignty mandates that necessitate jurisdictional infrastructure and create geopolitical tensions around international supply chains. This environment is strained by advanced packaging bottlenecks and semiconductor supply fragility.

- Operationally, the computational intensity of AI-native infrastructure leads to thermal management complexity and severe power grid constraints, driving demand for on-site renewable energy and energy-integrated computing. Solutions like advanced thermal interface materials and efficient system-level power delivery are critical.

- Organizations adopting managed machine learning services report a 30% reduction in training times, while hardware-driven cloud solutions now constitute over 63% of total market value.

- To navigate this, firms leverage risk oversight tools, automated model evaluation, and automated orchestration layers for real-time production inference and enterprise automation autonomy, sometimes utilizing bare-metal AI-optimized environments and high-speed interconnect fabrics to gain a competitive edge.

We can help! Our analysts can customize this cloud-based ai model training market research report to meet your requirements.

RIA -

RIA -