Cloud Radio Access Network Market Size 2026-2030

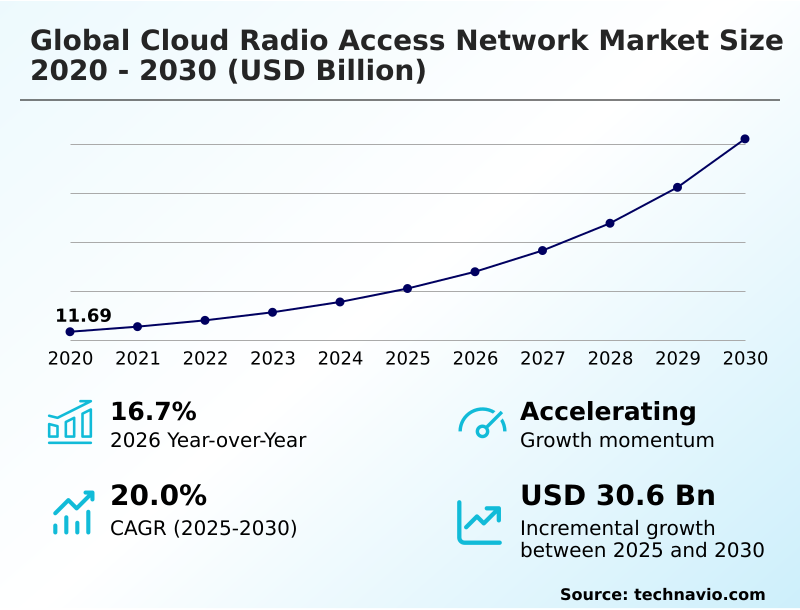

The cloud radio access network market size is valued to increase by USD 30.60 billion, at a CAGR of 20% from 2025 to 2030. Economic imperatives and total cost of ownership reduction will drive the cloud radio access network market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 33.8% growth during the forecast period.

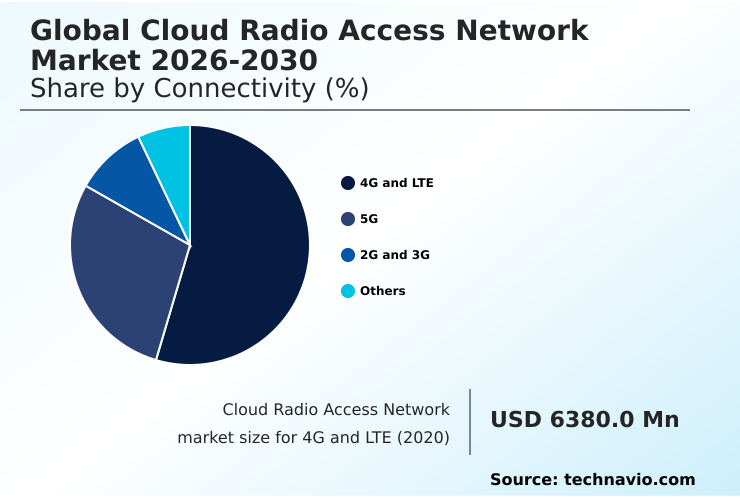

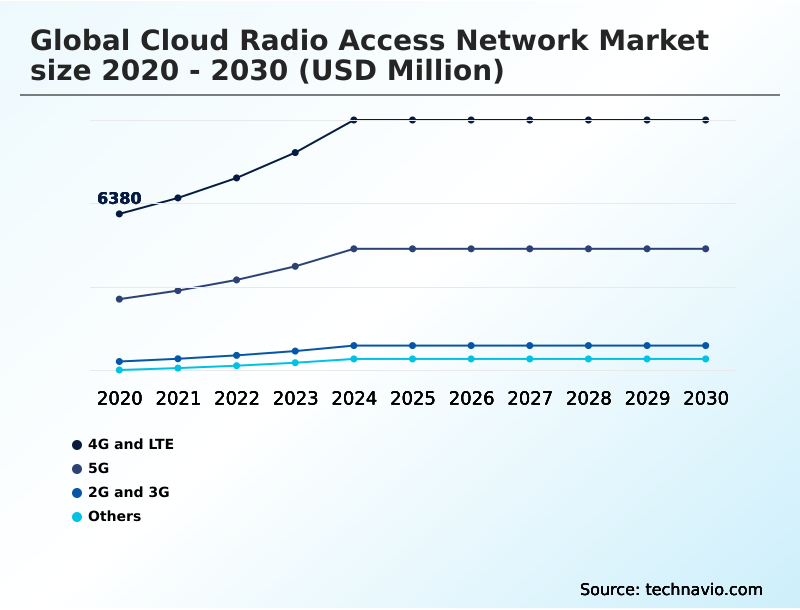

- By Connectivity - 4G and LTE segment was valued at USD 9.72 billion in 2024

- By Type - Centralised RAN segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 39.45 billion

- Market Future Opportunities: USD 30.60 billion

- CAGR from 2025 to 2030 : 20%

Market Summary

- The Cloud Radio Access Network market is undergoing a fundamental architectural shift, moving away from distributed, proprietary hardware toward centralized and virtualized models. This transformation is driven by the need for greater operational efficiency and the demanding performance requirements of 5G services.

- Key market drivers include significant total cost of ownership reduction and the strategic imperative to create a more diverse and competitive supplier ecosystem. Concurrently, the industry is navigating trends like the integration of artificial intelligence for network automation and the convergence of RAN with edge computing.

- However, this evolution is not without challenges; system integration complexity and ensuring performance parity with traditional systems are significant concerns for operators.

- For instance, a manufacturing enterprise implementing a private 5G network for factory automation relies on this architecture to achieve the ultra-low latency necessary for controlling autonomous guided vehicles and real-time quality control systems, a use case that is impossible with legacy network designs.

- The market's trajectory is defined by this balance between profound economic and technological benefits and the complex operational realities of deploying a disaggregated, software-defined network.

What will be the Size of the Cloud Radio Access Network Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Cloud Radio Access Network Market Segmented?

The cloud radio access network industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Connectivity

- 4G and LTE

- 5G

- 2G and 3G

- Others

- Type

- Centralised RAN

- Virtualised RAN

- Open RAN

- Hybrid cloud RAN

- Component

- Solution

- Services

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Connectivity Insights

The 4g and lte segment is estimated to witness significant growth during the forecast period.

The 4G and LTE segment remains a critical area for ran modernization. Operators are implementing a software-defined ran on a cloud-native architecture to virtualize baseband unit functions, ensuring carrier-grade performance as part of their telco digital transformation.

This approach, often a single ran deployment, uses commercial off-the-shelf servers to create a scalable foundation for a smooth 5G network evolution.

Centralizing processing with a virtualized baseband unit not only enhances dynamic resource allocation but also enables a significant total cost of ownership reduction.

This strategic shift prepares existing infrastructure for future demands, such as industrial automation connectivity, reducing operational resolution times by up to 25% and boosting overall network management efficiency.

The 4G and LTE segment was valued at USD 9.72 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 33.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cloud Radio Access Network Market Demand is Rising in APAC Get Free Sample

The geographic landscape is diverse, with APAC leading via deployments demonstrating a 35% total cost of ownership reduction. North America is driven by supply chain resilience and software-defined networking for flexibility.

European operators focus on energy efficient networking, with trials showing a 20% improvement in spectral efficiency. These regions are exploring dynamic spectrum sharing using both non-real-time ric and near-real-time ric for optimization.

In the Middle East, smart city projects demand massive mimo antenna systems to support vehicle-to-everything communication. Africa leverages baseband function virtualization for cost-effective coverage.

Across all regions, zero-touch network automation and digital twin simulation are becoming essential for managing these complex networks.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the Cloud Radio Access Network Market is defined by a complex interplay of technical hurdles and advanced solutions. Key among these are the significant c-ran fronthaul bandwidth requirements, which operators must address to support high-capacity services. This is compounded by open ran multi-vendor integration challenges, where ensuring seamless interoperability is paramount.

- A major focus for operators is validating vran performance vs traditional ran, a process often supported by hardware accelerators for vran optimization to handle intensive workloads. The business case is strengthened by the introduction of ai for ran energy efficiency management and the use of the ric for dynamic spectrum sharing, which optimizes network resources in real time.

- These capabilities are critical for emerging use cases, from private 5g for smart manufacturing to low latency applications with mec. As the architecture matures, security in virtualized ran environments becomes a top priority, requiring new strategies to protect disaggregated components.

- Early adopters of AI for RAN energy efficiency report a reduction in power consumption that is twice that of those using static power-saving modes. Ultimately, these developments represent the evolution from c-ran to 6g architecture, where networks will be fully automated and intelligent, driving the future of connectivity.

- Key strategies include automating c-ran lifecycle management, managing latency in c-ran deployments, and conducting thorough TCO analysis of vran vs dran. This transition is also influenced by the role of hyperscalers in c-ran and the need for robust cloud-native ran orchestration strategies.

What are the key market drivers leading to the rise in the adoption of Cloud Radio Access Network Industry?

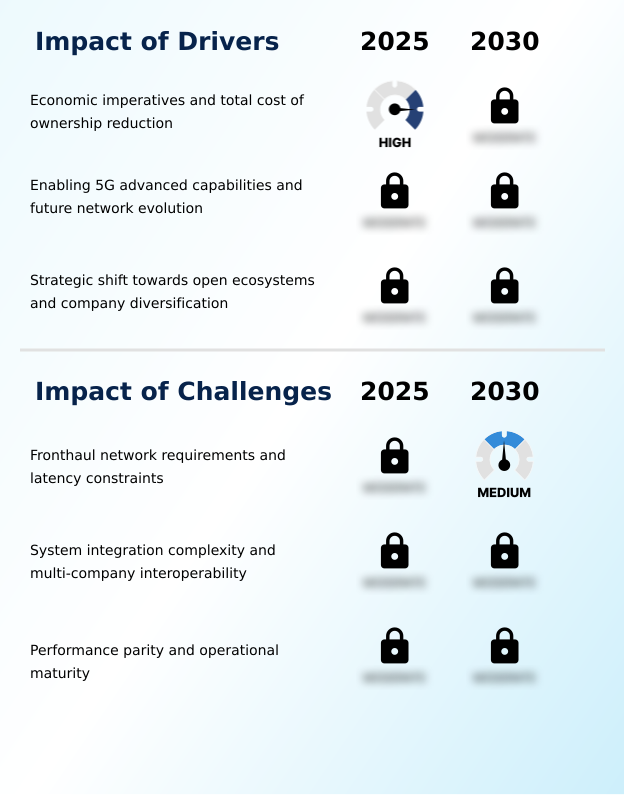

- Economic imperatives, particularly the significant reduction in total cost of ownership (TCO) for mobile network operators, serve as a primary driver for the global adoption of Cloud Radio Access Network architectures.

- Economic imperatives are a core driver, with the network disaggregation strategy enabling significant efficiencies through improved service management and orchestration. By moving to centralized baseband processing on a telco cloud platform, operators achieve vendor diversification and greater supply chain resilience.

- This shift away from purpose-built hardware toward virtualized network functions on a common network function virtualization infrastructure allows for energy savings up to 50%.

- The move toward an open ecosystem fosters competition, critical for enabling advanced features like coordinated multipoint transmission. This improves cell-edge performance by over 20% and supports demanding use cases from cloud gaming optimization to autonomous mobility infrastructure.

What are the market trends shaping the Cloud Radio Access Network Industry?

- The convergence of Cloud Radio Access Network (C-RAN) and Multi-Access Edge Computing (MEC) is a defining market trend. This synergy transforms the network edge into a distributed cloud environment for low-latency applications.

- A defining trend is deep convergence with multi-access edge computing, transforming the network edge into a distributed cloud for immersive extended reality support. This fusion enables new low-latency services, with some deployments reducing round-trip time by 75%. Concurrently, the proliferation of neutral host deployments and private 5g networks, connected via a fronthaul gateway, is expanding the market.

- The integration of ai-driven orchestration through the ran intelligent controller and its xapps and rapps is pivotal for intelligent ran automation. This allows for ue-centric traffic steering based on real-time radio protocols and predictive network maintenance, which reduces service-impacting faults by over 40%. The ecosystem is moving toward o-ran alliance standards to drive innovation across these models.

What challenges does the Cloud Radio Access Network Industry face during its growth?

- Stringent fronthaul network requirements, including massive bandwidth demands and ultra-low latency constraints, present a formidable technical and economic challenge affecting industry growth.

- Technical hurdles present significant challenges, especially the fronthaul latency budget required by the common public radio interface, where a single site can demand over 25 Gbps. Limited fronthaul fiber availability constrains deployments. Another challenge is the system integration complexity of connecting a radio unit (ru) to a distributed unit (du) and centralized unit (cu) from different vendors.

- This can increase initial testing efforts by over 50%. Operators are now responsible for performance parity assurance between open vran solutions and traditional systems, sometimes requiring hardware accelerator cards. This operational model transformation demands new skills to manage disaggregated network components and a different network security posture.

Exclusive Technavio Analysis on Customer Landscape

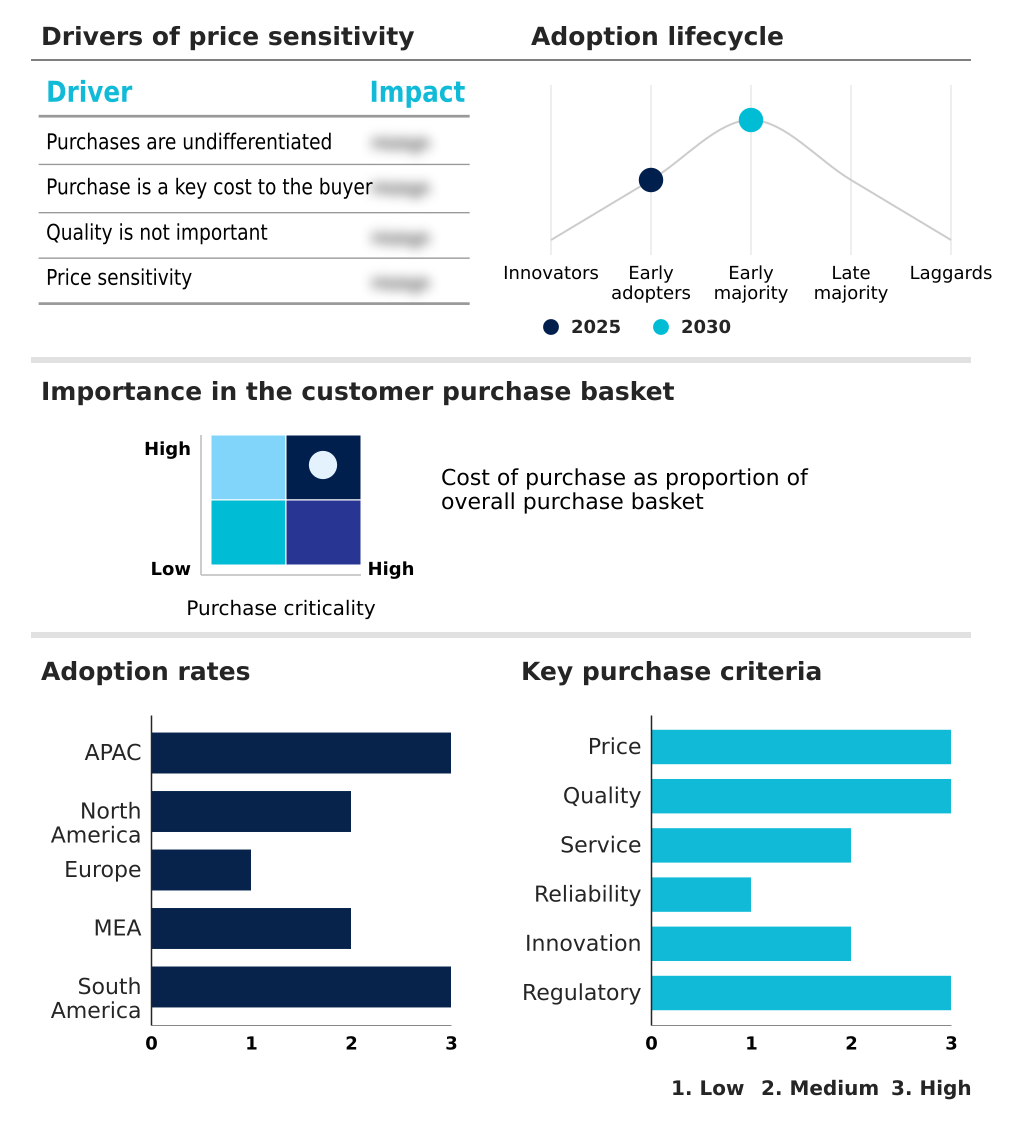

The cloud radio access network market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cloud radio access network market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cloud Radio Access Network Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cloud radio access network market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

6WIND SAS - Offers an AI-powered cloud RAN with a RAN Intelligent Controller, enabling xApps/rApps for real-time optimization, energy savings, and UE-centric traffic steering to boost network efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 6WIND SAS

- Airspan Networks Inc.

- Anritsu Corp.

- Capgemini Service SAS

- CommScope Holding

- Dell Technologies Inc.

- EXFO Inc.

- Fujitsu Ltd.

- Hewlett Packard

- Huawei Technologies Co. Ltd.

- Intel Corp.

- NEC Corp.

- Nokia Corp.

- Parallel Wireless Inc.

- Radisys Corp.

- Rakuten Group Inc.

- Samsung Electronics Co. Ltd.

- Telefonaktiebolaget Ericsson

- Viavi Solutions Inc.

- ZTE Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cloud radio access network market

- In September 2024, a major US telecom operator announces a strategic partnership with a hyperscale cloud provider to deploy distributed cloud edge solutions at its network locations, aiming to virtualize RAN functions and accelerate the rollout of network-as-a-service offerings.

- In November 2024, a leading European network equipment provider unveils its next-generation Cloud RAN software, incorporating native AI for real-time resource orchestration and achieving a 15% reduction in energy consumption in extensive trial environments.

- In February 2025, a prominent IT infrastructure company announces the acquisition of a specialized Open RAN software firm for approximately USD 800 million, a move designed to strengthen its portfolio of end-to-end virtualized network solutions.

- In April 2025, the European Commission, in collaboration with several member states, launches a EUR 500 million fund to fast-track the development and deployment of secure, multi-vendor Open RAN technologies across the continent.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cloud Radio Access Network Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 312 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 20% |

| Market growth 2026-2030 | USD 30602.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 16.7% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market represents a fundamental architectural shift, defined by the adoption of virtualized network functions running on commercial off-the-shelf servers. This model of baseband function virtualization connects remote radio heads over a high-capacity fronthaul transport network, enabling advanced capabilities like coordinated multipoint transmission and massive mimo antenna systems to ensure carrier-grade performance.

- Central to this evolution is the ran intelligent controller, featuring both non-real-time ric and near-real-time ric components that host xapps and rapps for ai-driven orchestration. This technology presents a critical boardroom decision: whether to invest in developing proprietary applications for ue-centric traffic steering or leverage an open ecosystem, impacting R&D budgets and service deployment agility.

- Deployments leveraging this software-defined ran and its predictive network maintenance capabilities have demonstrated the ability to provision new network slices in hours, a process that previously took weeks, representing over a 95% reduction in service deployment time. This highlights the move towards a more flexible and automated operational model based on telco cloud platforms.

What are the Key Data Covered in this Cloud Radio Access Network Market Research and Growth Report?

-

What is the expected growth of the Cloud Radio Access Network Market between 2026 and 2030?

-

USD 30.60 billion, at a CAGR of 20%

-

-

What segmentation does the market report cover?

-

The report is segmented by Connectivity (4G and LTE, 5G, 2G and 3G, and Others), Type (Centralised RAN, Virtualised RAN, Open RAN, and Hybrid cloud RAN), Component (Solution, and Services) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Economic imperatives and total cost of ownership reduction, Fronthaul network requirements and latency constraints

-

-

Who are the major players in the Cloud Radio Access Network Market?

-

6WIND SAS, Airspan Networks Inc., Anritsu Corp., Capgemini Service SAS, CommScope Holding, Dell Technologies Inc., EXFO Inc., Fujitsu Ltd., Hewlett Packard, Huawei Technologies Co. Ltd., Intel Corp., NEC Corp., Nokia Corp., Parallel Wireless Inc., Radisys Corp., Rakuten Group Inc., Samsung Electronics Co. Ltd., Telefonaktiebolaget Ericsson, Viavi Solutions Inc. and ZTE Corp.

-

Market Research Insights

- The market is characterized by a dynamic shift toward software-defined networking and disaggregated architectures. This evolution is enabling new business models such as neutral host deployments and private 5G networks, with enterprise adoption of the latter showing a 40% improvement in operational automation.

- The drive for intelligent RAN automation is pushing the industry toward zero-touch network automation, which reduces network configuration errors by over 60% compared to manual methods. This move toward an open ecosystem supports greater vendor diversification and accelerates innovation.

- The entire operational model transformation is geared toward enhancing performance and reducing the total cost of ownership, making networks more agile and responsive to changing service demands.

We can help! Our analysts can customize this cloud radio access network market research report to meet your requirements.

RIA -

RIA -