Coal To Liquid (CTL) Market Size 2026-2030

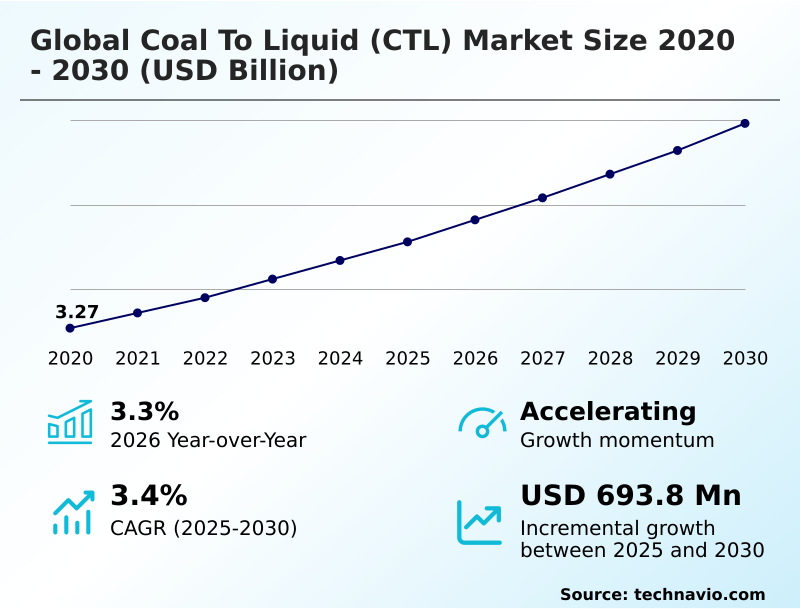

The coal to liquid (ctl) market size is valued to increase by USD 693.8 million, at a CAGR of 3.4% from 2025 to 2030. Abundant availability of coal will drive the coal to liquid (ctl) market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 78.6% growth during the forecast period.

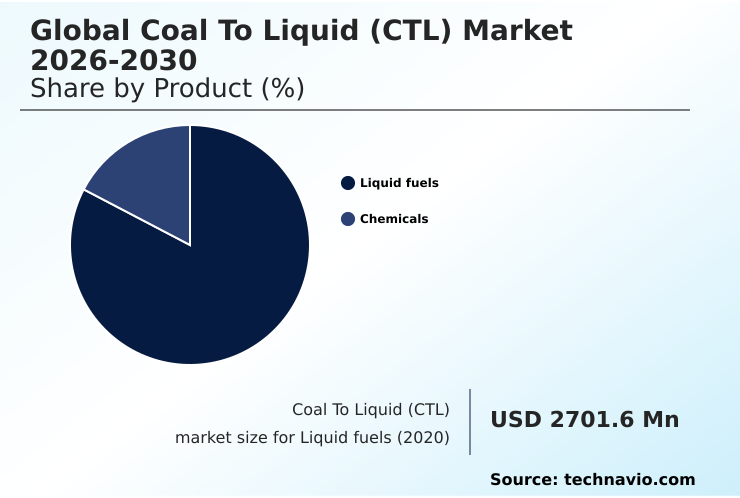

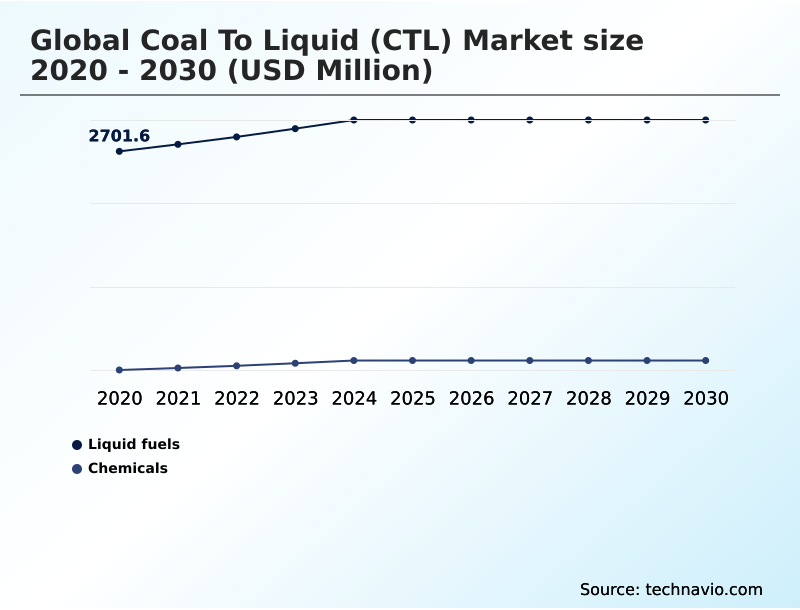

- By Product - Liquid fuels segment was valued at USD 3.01 billion in 2024

- By Technology - Direct coal liquefaction segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1.21 billion

- Market Future Opportunities: USD 693.8 million

- CAGR from 2025 to 2030 : 3.4%

Market Summary

- The coal to liquid (CTL) market revolves around the conversion of coal into liquid hydrocarbons, primarily serving as transportation fuels and chemical feedstocks. This industry is fundamentally driven by the pursuit of energy security, allowing nations with substantial coal reserves to decrease their reliance on imported crude oil.

- Key technologies such as direct coal liquefaction and indirect coal liquefaction, including fischer-tropsch synthesis, are central to this process. The market's trajectory is influenced by a dual dynamic: the strategic advantage of monetizing domestic resources versus significant headwinds from environmental concerns and high capital costs.

- For instance, a business scenario involves a state-owned enterprise evaluating a multi-billion dollar investment in an integrated gasification combined cycle (IGCC) plant. The decision hinges on long-term crude oil price forecasts, the availability of carbon capture and storage (CCS) infrastructure, and national mandates promoting fuel diversification strategy.

- The market's evolution is increasingly tied to advancements that improve coal conversion efficiency and mitigate the environmental footprint, making it a complex but strategically important sector for specific economies. The focus on producing high-cetane-number diesel and other synthetic fuels continues to be a major factor.

What will be the Size of the Coal To Liquid (CTL) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Coal To Liquid (CTL) Market Segmented?

The coal to liquid (ctl) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Liquid fuels

- Chemicals

- Technology

- Direct coal liquefaction

- Indirect coal liquefaction

- Hybrid CTL processes

- Application

- Transportation fuels

- Chemicals and petrochemicals

- Power generation

- Geography

- APAC

- China

- India

- Indonesia

- Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Colombia

- Argentina

- Rest of World (ROW)

- APAC

By Product Insights

The liquid fuels segment is estimated to witness significant growth during the forecast period.

The market is segmented by product, technology, and application. The liquid fuels segment, a key area of synthetic fuel production, is pivotal, driven by the strategic need for energy security solutions and alternative liquid fuels.

This segment focuses on converting coal into high-quality transportation fuels, primarily ultra-clean diesel and jet fuel. These products, resulting from processes like fischer-tropsch synthesis, offer superior combustion properties.

The economic case for this liquid hydrocarbon conversion strengthens during periods of high crude oil prices.

A dominant portion of output is directed toward mobility needs, with transportation applications consistently accounting for over 89% of the total product offtake, underscoring the segment's core role in the broader coal liquefaction technology landscape.

The Liquid fuels segment was valued at USD 3.01 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 78.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Coal To Liquid (CTL) Market Demand is Rising in APAC Get Free Sample

The geographic landscape is dominated by the APAC region, which is the largest and fastest-growing market, accounting for a majority of global growth, with a contribution of over 67%.

This is primarily driven by China and a rising interest in India, where national energy security agendas prioritize the use of vast domestic coal reserves for producing synthetic fuels and high-value aromatic chemicals.

In contrast, North America and Europe remain marginal markets due to the availability of cheaper hydrocarbons and stringent environmental regulations that create significant carbon-intensive project risks.

The Middle East and Africa present a bifurcated picture; while the Middle East has no strategic interest, South Africa is a historical pioneer in indirect coal liquefaction.

Development in other coal-rich African nations is constrained by high capital costs and water scarcity, highlighting the regionally fragmented nature of this industry and the importance of low-rank coal utilization technologies.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the global coal to liquid (CTL) market 2026-2030 requires a nuanced understanding of technical and economic trade-offs. A key consideration is the debate over direct vs indirect coal liquefaction, where the choice impacts both capital outlay and product slate. The fischer-tropsch process for diesel remains a cornerstone of ICL, prized for producing high-quality fuels.

- However, the overall economics of coal to liquid are highly sensitive to initial plant costs and feedstock prices. Stakeholders must also address the environmental impact of CTL plants, with a growing emphasis on carbon capture in CTL facilities to mitigate emissions. For those focused on diversification, CTL as a petrochemical feedstock offers a valuable alternative to crude oil derivatives.

- Success hinges on advancements in CTL catalyst technology to improve coal to liquid process efficiency. The high-ash coal CTL processing capabilities are crucial for countries like India. Comparing the bergius process vs fischer-tropsch reveals different strengths in syncrude composition.

- The development of hybrid CTL process designs and small-scale modular ctl plants is aimed at reducing the formidable coal to liquid plant cost, which can be over 30% higher when CCS is included. Furthermore, polygeneration in CTL plant design is becoming essential for economic resilience.

- Optimizing syngas quality for FT synthesis and managing water consumption in CTL production are critical operational challenges. For specialized needs, such as CTL for military jet fuel, performance and security of supply outweigh cost. The industry is also focused on upgrading ctl syncrude to gasoline and reducing emissions from ctl processes to ensure long-term viability amid a global energy transition.

What are the key market drivers leading to the rise in the adoption of Coal To Liquid (CTL) Industry?

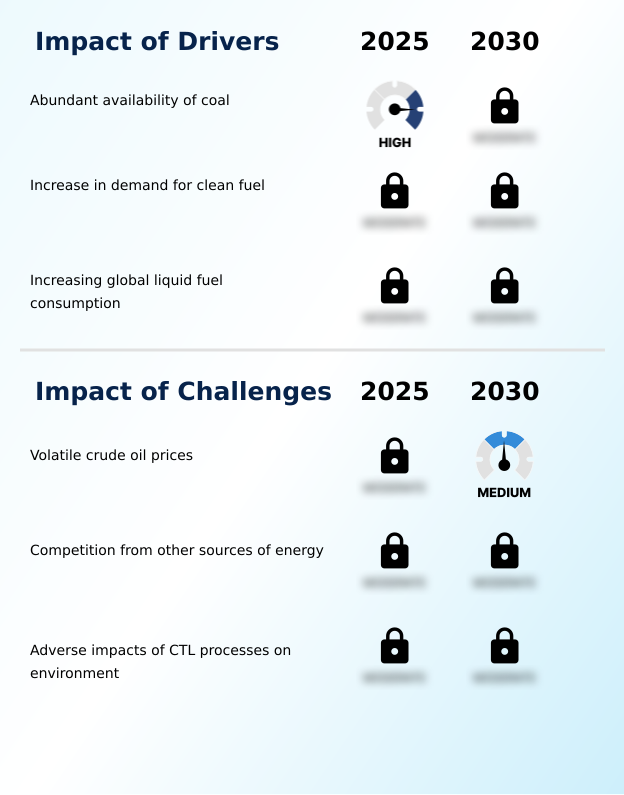

- The abundant availability of coal in several key regions is a primary driver, offering a strategic route to enhance domestic energy security and reduce dependence on imported crude oil.

- The market is primarily propelled by the abundant availability of coal, which underpins the strategic energy planning of nations seeking to reduce dependency on imported oil.

- This drive for energy security solutions is particularly strong in countries with vast domestic reserves.

- The increasing demand for cleaner fuels is another major driver, as advanced conversion technologies enable the production of low-sulfur fuel synthesis products that meet stringent environmental regulations. For instance, the resulting high cetane number diesel offers superior combustion performance.

- The integration of an integrated gasification combined cycle (IGCC) system can improve overall plant efficiency by more than 25% compared to separate power and fuel production units, creating a powerful economic incentive.

- Increasing global liquid fuel consumption further supports market expansion, positioning CTL as a vital component of a diversified energy portfolio.

What are the market trends shaping the Coal To Liquid (CTL) Industry?

- An emerging trend is the increasing demand for petrochemical feedstock, which provides an alternative pathway for producing essential chemical building blocks.

- Key market trends are centered on enhancing value and efficiency. The growing demand for petrochemical feedstock production is a significant development, allowing operators to diversify away from fuel markets and into higher-margin chemicals. This shift supports a more resilient business model less susceptible to oil price volatility.

- The rapid expansion of transportation globally, especially in APAC, continues to be a primary demand driver; this single application constitutes nearly 89% of market offtake. Concurrently, technological advancements in coal conversion efficiency are making operations more economically viable.

- The development of small-scale, modular plants is also gaining traction as a strategy to reduce massive upfront capital expenditures and target niche applications, reflecting a move toward more flexible and financially accessible clean coal technology.

What challenges does the Coal To Liquid (CTL) Industry face during its growth?

- Significant volatility in crude oil prices presents a key challenge, directly impacting the economic viability and competitive positioning of coal-to-liquid products against conventional petroleum-based fuels.

- The market faces substantial challenges, led by the high volatility of crude oil prices. A sudden drop in oil prices, such as the 10% surge seen in early 2025, can render capital-intensive CTL projects economically uncompetitive against traditional refining.

- Another significant hurdle is the intense competition from other energy sources, including renewables and abundant natural gas, which offer a cleaner and often cheaper non-petroleum based feedstock. The adverse environmental impact remains a primary constraint; CTL processes are notoriously water-intensive, consuming up to twice the water of conventional oil refining.

- Furthermore, the high carbon footprint necessitates costly mitigation measures, challenging the long-term sustainability and public acceptance of this technology without effective downstream refining requirements.

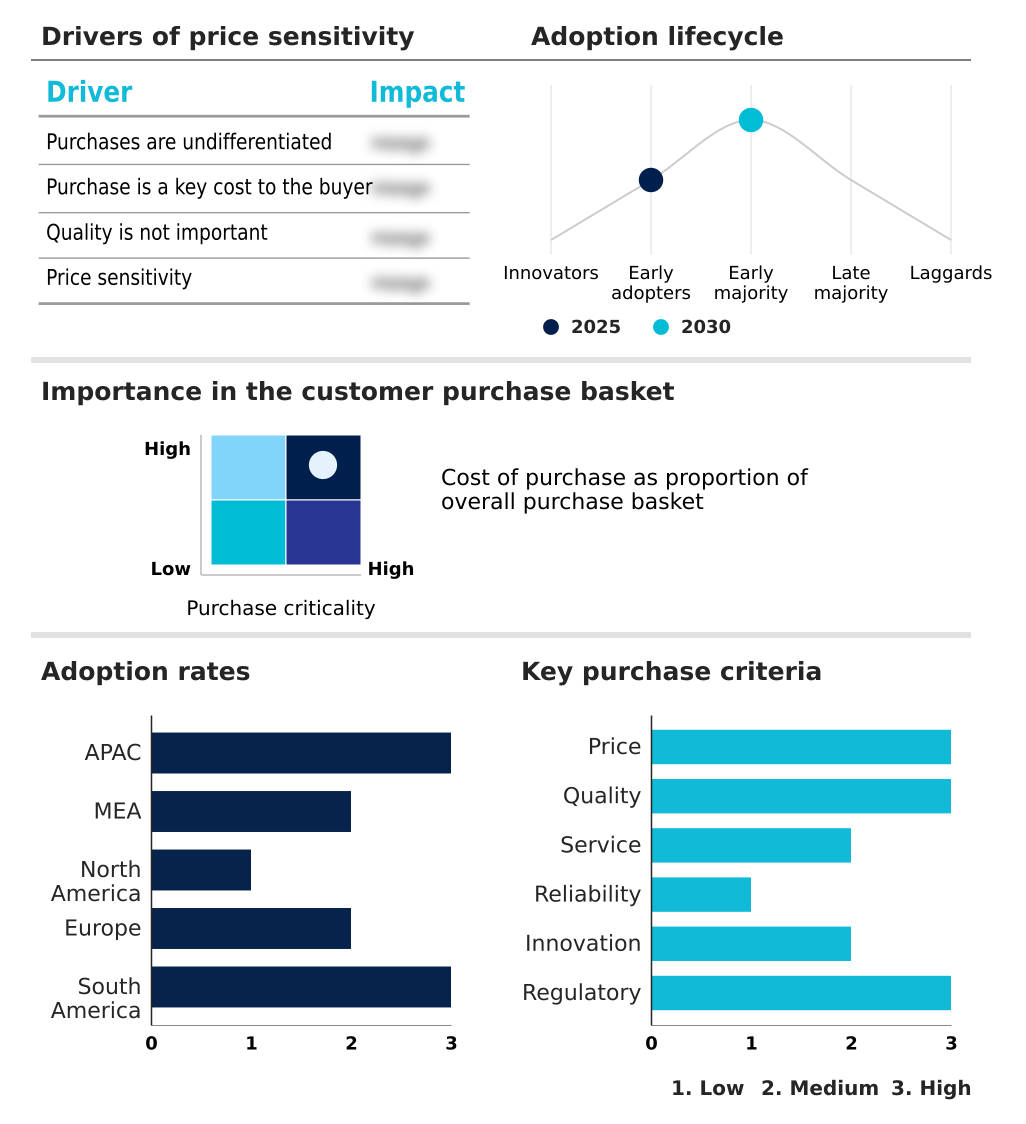

Exclusive Technavio Analysis on Customer Landscape

The coal to liquid (ctl) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the coal to liquid (ctl) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Coal To Liquid (CTL) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, coal to liquid (ctl) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Air Products and Chemicals Inc - Key offerings focus on converting coal resources into high-value liquid fuels and chemical feedstocks, enhancing energy security and enabling domestic resource monetization through advanced conversion technologies.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Air Products and Chemicals Inc

- Celanese Corp.

- China Shenhua Energy Co. Ltd.

- Pall Corp.

- Regius Synfuels Ltd.

- Sasol Ltd.

- Shandong Energy Group Co. Ltd.

- Synfuels China Technology Co

- Thyssenkrupp Uhde GmbH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Coal to liquid (ctl) market

- In May 2025, Bukit Asam, an Indonesian state-owned miner, announced intentions to proceed with a project valued at approximately USD 3.1 billion to construct a facility for converting coal into synthetic natural gas, advancing its downstream diversification strategy.

- In March 2025, Indonesia advanced its plans to resume the development of coal gasification facilities. These plants are designed to produce hydrogen and dimethyl ether as part of a national strategy to decrease reliance on imported liquefied petroleum gas.

- In October 2024, the Indian government announced the creation of a special purpose vehicle to oversee the development of three major coal-to-liquid plants. This initiative is designed to produce over five million tons of synthetic fuels annually by 2030, reducing the nation's oil import dependency.

- In October 2024, China Energy Investment Corporation revealed plans for a USD 24 billion investment in a new coal-to-liquid project in Hami, Xinjiang. The integrated plant is set to convert local coal into oil products, with the first phase targeted for operation in 2027.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Coal To Liquid (CTL) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 279 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 3.4% |

| Market growth 2026-2030 | USD 693.8 million |

| Market structure | Concentrated |

| YoY growth 2025-2026(%) | 3.3% |

| Key countries | China, India, Indonesia, Australia, Vietnam, Mongolia, South Africa, Saudi Arabia, UAE, Egypt, Turkey, US, Canada, Mexico, Russia, Poland, Germany, UK, France, Ukraine, Brazil, Colombia and Argentina |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The coal to liquid (CTL) market is defined by its strategic importance in energy security, balanced against significant economic and environmental hurdles. Core technologies, including direct coal liquefaction, indirect coal liquefaction, and hybrid CTL processes, form the industry's foundation.

- Processes like coal gasification and Fischer-Tropsch synthesis are central to converting coal into syngas and then into valuable products such as synthetic fuels and Fischer-Tropsch waxes. The viability of these operations depends on catalyst performance and the effective use of hydrogenation.

- A critical boardroom-level consideration is the commitment to carbon capture and storage (CCS) to mitigate the high emissions profile, a factor that can increase capital costs substantially. Modern facilities leverage polygeneration to produce a mix of ultra-clean diesel, paraffinic fuels, and aromatic chemicals, enhancing economic resilience. Innovations in hydrocracking and slurry Fischer-Tropsch technologies are crucial for improving efficiency.

- For example, next-generation entrained flow gasification systems have demonstrated the ability to increase syngas production efficiency by up to 15% compared to older designs, directly impacting plant profitability. The evolution toward cleaner liquefaction methods is essential for the market's future.

What are the Key Data Covered in this Coal To Liquid (CTL) Market Research and Growth Report?

-

What is the expected growth of the Coal To Liquid (CTL) Market between 2026 and 2030?

-

USD 693.8 million, at a CAGR of 3.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Liquid fuels, and Chemicals), Technology (Direct coal liquefaction, Indirect coal liquefaction, and Hybrid CTL processes), Application (Transportation fuels, Chemicals and petrochemicals, and Power generation) and Geography (APAC, Middle East and Africa, North America, Europe, South America)

-

-

Which regions are analyzed in the report?

-

APAC, Middle East and Africa, North America, Europe and South America

-

-

What are the key growth drivers and market challenges?

-

Abundant availability of coal, Volatile crude oil prices

-

-

Who are the major players in the Coal To Liquid (CTL) Market?

-

Air Products and Chemicals Inc, Celanese Corp., China Shenhua Energy Co. Ltd., Pall Corp., Regius Synfuels Ltd., Sasol Ltd., Shandong Energy Group Co. Ltd., Synfuels China Technology Co and Thyssenkrupp Uhde GmbH

-

Market Research Insights

- The market's dynamics are shaped by a complex interplay of strategic and economic factors. The pursuit of a robust fuel diversification strategy is a core motivator for national stakeholders, seeking to insulate economies from volatile energy markets. This has led to strategic energy planning that favors domestic resource monetization, particularly in coal-rich regions.

- However, the high price sensitivity of buyers, for whom fuel is a key cost, means that the economic viability of CTL operations is under constant pressure. The competitive landscape is influenced by the availability of substitutes, where a 10% swing in crude oil prices can dramatically alter the business case for synthetic fuel production.

- Concurrently, technological advancements are improving coal conversion efficiency, with modern plants demonstrating higher yields compared to legacy facilities, enhancing their value proposition in the energy mix.

We can help! Our analysts can customize this coal to liquid (ctl) market research report to meet your requirements.

RIA -

RIA -