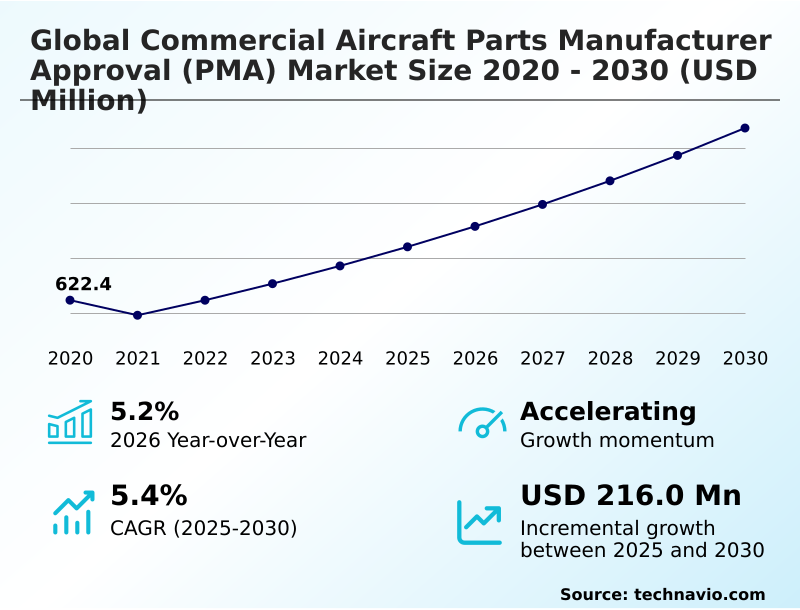

Commercial Aircraft Parts Manufacturer Approval (PMA) Market Size 2026-2030

The commercial aircraft parts manufacturer approval (pma) market size is valued to increase by USD 216 million, at a CAGR of 5.4% from 2025 to 2030. Escalating maintenance, repair, and overhaul expenditures and structural cost reduction pressures will drive the commercial aircraft parts manufacturer approval (pma) market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 43.5% growth during the forecast period.

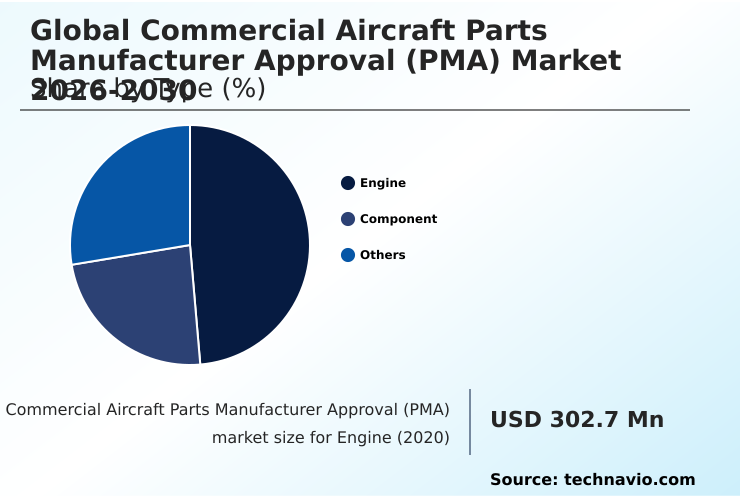

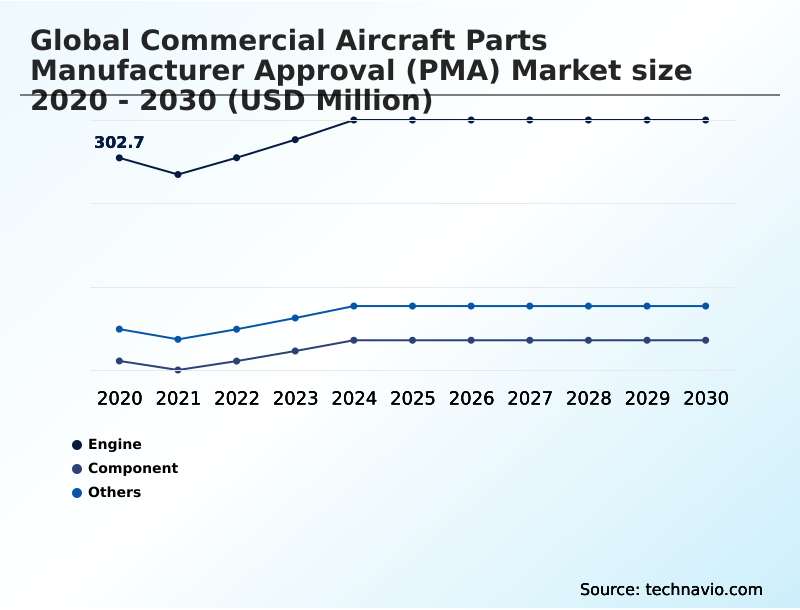

- By Type - Engine segment was valued at USD 331.6 million in 2024

- By Application - Small widebody segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 313 million

- Market Future Opportunities: USD 216 million

- CAGR from 2025 to 2030 : 5.4%

Market Summary

- The Commercial Aircraft Parts Manufacturer Approval (PMA) market is characterized by a dynamic interplay between cost optimization and stringent safety regulations. A core driver is the escalating pressure on airlines to reduce maintenance, repair, and overhaul (MRO) expenditures without compromising airworthiness. This has led to the strategic adoption of PMA components, which offer significant cost advantages over OEM parts.

- For instance, a mid-sized airline managing an aging fleet can implement a PMA-based procurement strategy to reduce its annual spend on expendable parts by a considerable margin, directly improving its cost per available seat kilometer. This is balanced by challenges, including navigating complex international certification processes and countering the narrative from OEMs regarding asset valuation.

- A prominent trend is the technological advancement within the PMA sector, particularly in reverse-engineering and additive manufacturing. These innovations are enabling third-party manufacturers to produce highly complex parts, such as turbine blades and flight control components, that were previously the exclusive domain of OEMs.

- This shift is expanding the addressable market for PMA providers and fostering a more competitive and resilient aerospace aftermarket ecosystem, pushing providers to innovate on material science and part longevity.

What will be the Size of the Commercial Aircraft Parts Manufacturer Approval (PMA) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Commercial Aircraft Parts Manufacturer Approval (PMA) Market Segmented?

The commercial aircraft parts manufacturer approval (pma) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Engine

- Component

- Others

- Application

- Small widebody

- Medium widebody

- Large widebody

- Service type

- Certification authority

- Aircraft OEM

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Middle East and Africa

- UAE

- Saudi Arabia

- Turkey

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Type Insights

The engine segment is estimated to witness significant growth during the forecast period.

The engine segment, a critical area of the market, focuses on high-value parts such as engine core components and turbine engine components.

This domain requires rigorous engineering to produce aftermarket replacement parts for hydraulic systems and fuel conveyance components, often leveraging predictive diagnostic tools. Manufacturers develop sophisticated avionics subsystems and parts for environmental control system parts that rival original equipment.

The technical complexity is high, with the failure rate for some new applications involving intricate aircraft electrical components rising by as much as 15% due to stringent stress and fatigue performance requirements.

Success hinges on advanced engineering and the integration of embedded sensor technology to meet airworthiness standards without compromising performance, addressing both used serviceable material and new fuel system innovations in fluid power technology.

The Engine segment was valued at USD 331.6 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 43.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Commercial Aircraft Parts Manufacturer Approval (PMA) Market Demand is Rising in APAC Get Free Sample

The market's geographic distribution reflects a mature landscape in North America and rapid expansion in APAC, where growth is outpacing the global average by nearly 2%.

In established regions, the focus is on optimizing dual-source inventory management and leveraging bilateral air safety agreements to streamline the use of line replaceable units and flight control components.

This practice can improve parts availability by up to 25%, directly impacting fleet readiness.

In contrast, emerging regions are building their aerostructure fabrication capabilities for parts like fuselage assemblies and structural castings, with a strong emphasis on PMA certification and airworthiness certification.

These regions are also addressing the complexities of aircraft asset valuation when integrating PMA parts for forged components, non-critical system parts, and cabin interior retrofits to support their growing fleets and MRO ecosystems.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic adoption of PMA components is reshaping airline maintenance budgets and supply chain architectures. A critical consideration for operators is the FAA approval process for PMA parts, which ensures compliance with airworthiness directives. The cost savings of PMA vs OEM components are a primary driver, with some carriers reporting double-digit reductions in MRO costs with PMA sourcing.

- However, fleet managers must also assess the impact of PMA parts on aircraft resale value. For operators of older planes, PMA solutions for legacy aircraft engines are essential for extending operational life economically. The industry is also navigating the challenges of reverse-engineering composite PMA parts, where the role of additive manufacturing in PMA production is becoming increasingly vital.

- Overcoming regulatory hurdles for international PMA certification is key to unlocking global market potential, while blockchain traceability for life-limited PMA parts addresses provenance concerns. Sustainability benefits of using PMA components are now a key part of ESG reporting.

- Market trends show strong demand for PMA for structural and aerostructure components in narrow-body aircraft, while PMA supply chain diversification benefits are critical for operational resilience. The future of PMA in next-generation aircraft will depend on solving complex issues related to PMA for high-value avionics systems and managing OEM resistance to PMA parts.

What are the key market drivers leading to the rise in the adoption of Commercial Aircraft Parts Manufacturer Approval (PMA) Industry?

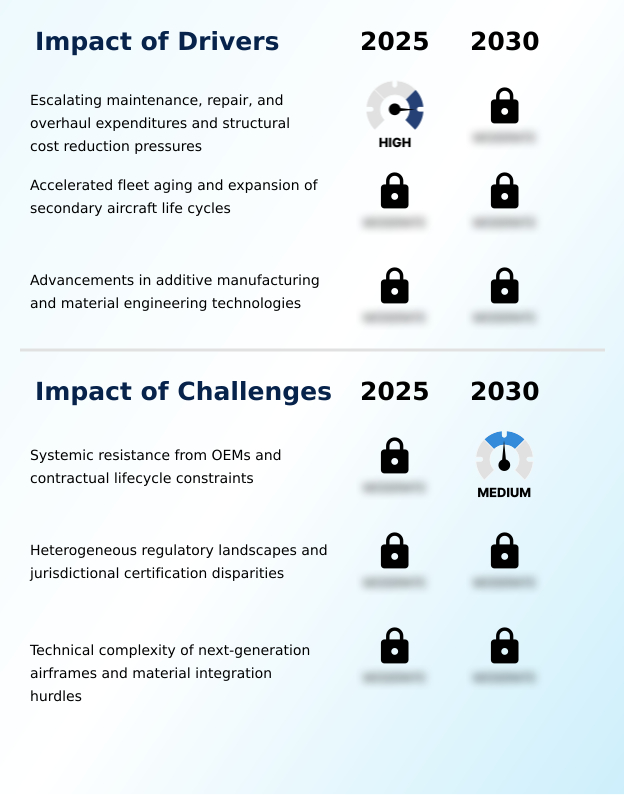

- Escalating maintenance, repair, and overhaul (MRO) expenditures, coupled with structural cost-reduction pressures on airlines, serve as the primary driver for market growth.

- Market growth is significantly propelled by economic and technological drivers. Airlines are focused on reducing MRO expenditures, with engine overhaul costs being a primary target.

- The adoption of parts made with high-performance alloys through additive manufacturing can reduce component weight by up to 15%, contributing to fuel savings. This is particularly relevant for secondary aircraft life cycles and legacy fleet maintenance.

- Furthermore, the use of predictive maintenance tools enhances the value of aeroderivative gas turbine parts and power transmission components by forecasting failures before they occur.

- Innovations in material engineering technologies are enabling the production of more durable aerospace bearings and cockpit hardware, directly addressing the demand for high-wear component replacement and extending the operational viability of aging aircraft, thus reducing total cost of ownership.

What are the market trends shaping the Commercial Aircraft Parts Manufacturer Approval (PMA) Industry?

- The digital transformation of the aviation aftermarket is accelerating. A key trend involves the integration of blockchain technology to enhance the traceability and provenance of life-limited parts.

- Key trends are reshaping the market, driven by digitalization and sustainability. The move toward green aftermarket solutions is compelling firms to adopt carbon-neutral manufacturing and align with sustainable procurement policies, which are increasingly tied to ESG compliance metrics. This has led to innovations in materials for parts like actuators and thermal barrier layers.

- Concurrently, blockchain traceability systems are revolutionizing life-limited part management and traceability, with early adopters reporting a 40% improvement in record accuracy. This technology, combined with digital twin modeling, allows for precise tracking of high-pressure turbine blades and other critical components, ensuring they are compatible with sustainable aviation fuel.

- These trends are not only enhancing safety and transparency but also providing verifiable data that supports a more circular and efficient aerospace economy.

What challenges does the Commercial Aircraft Parts Manufacturer Approval (PMA) Industry face during its growth?

- Systemic resistance from original equipment manufacturers (OEMs) and the imposition of contractual lifecycle constraints present a key challenge to the industry's growth.

- The market faces significant challenges from entrenched industry practices and technological hurdles. Persistent OEM pushback and the use of intellectual property constraints and bundled service agreements create substantial barriers to entry and adoption. Furthermore, the lack of harmonized regulatory standards across different jurisdictions complicates the certification of parts for next-generation airframes, which increasingly use proprietary data access models.

- The technical complexity of modern aircraft, featuring integrated fly-by-wire systems and structural assemblies made of carbon-fiber reinforced polymers, demands advanced reverse-engineering and non-destructive testing capabilities. Developing PMA for complex wing components and motion control subsystems is capital-intensive, with development cycles often exceeding 18 months, posing a risk in a rapidly evolving technological landscape.

Exclusive Technavio Analysis on Customer Landscape

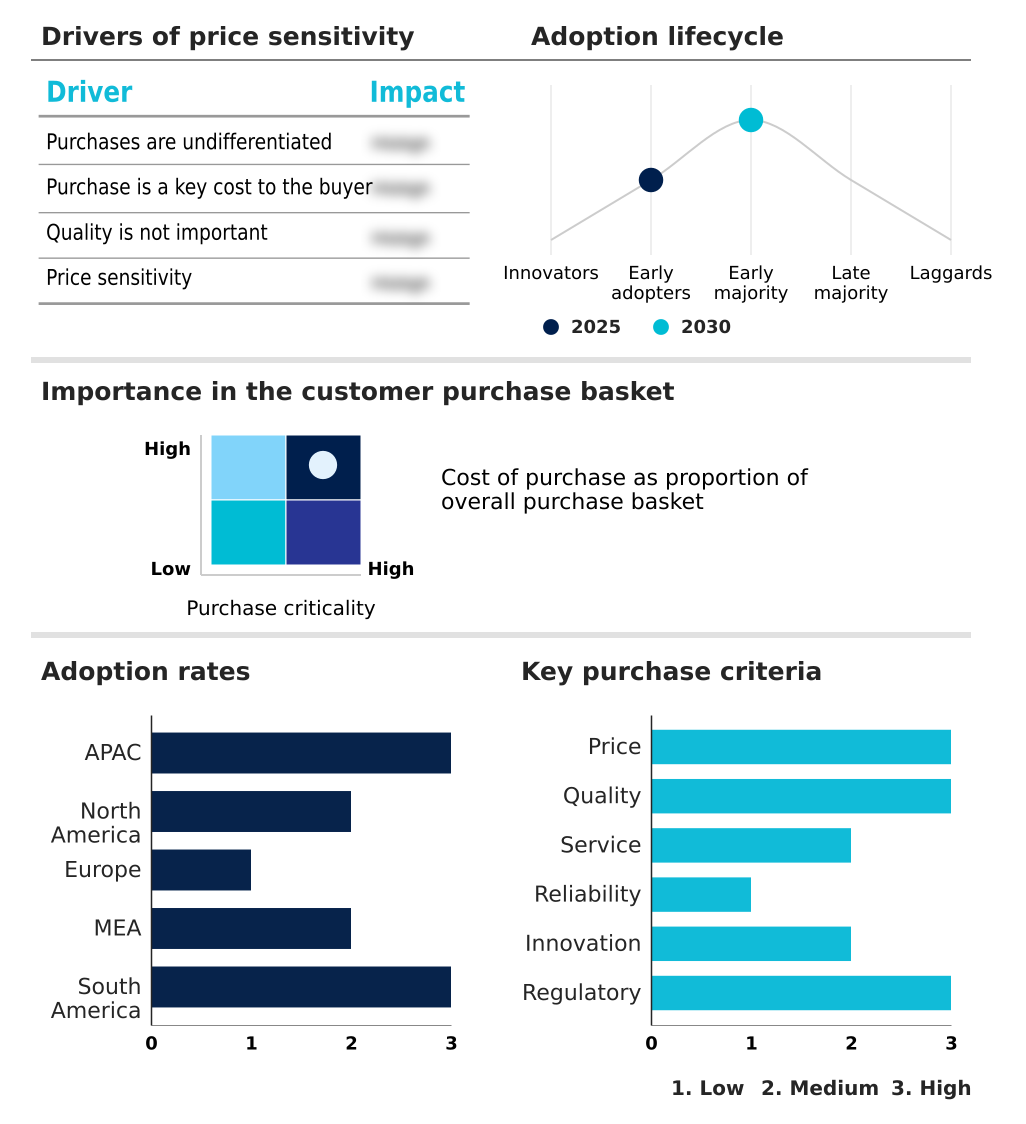

The commercial aircraft parts manufacturer approval (pma) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the commercial aircraft parts manufacturer approval (pma) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Commercial Aircraft Parts Manufacturer Approval (PMA) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, commercial aircraft parts manufacturer approval (pma) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ADPma LLC - Analysis focuses on the design, certification, and manufacture of proprietary precision aircraft parts for airframe and engine systems within the aerospace aftermarket.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ADPma LLC

- Aero Brake and Spares Inc.

- AMETEK Inc.

- BAE Systems Plc

- Chromalloy Gas Turbine LLC

- Eaton Corp. Plc

- General Electric Co.

- HEICO Corp.

- Honeywell International Inc.

- Kellstrom Aerospace

- Moog Inc.

- Parker Hannifin Corp.

- Precision Castparts Corp.

- RBC Bearings Inc.

- RTX Corp.

- Safran SA

- Spirit AeroSystems Inc.

- The Timken Co.

- TransDigm Group Inc.

- Wencor Group LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Commercial aircraft parts manufacturer approval (pma) market

- In October 2024, VSE Corp. announced a definitive agreement to acquire Kellstrom Aerospace Group for approximately $200 million, aiming to strengthen its position in the commercial aviation aftermarket.

- In January 2025, TransDigm Group Inc. announced the acquisition of a specialized Parts Manufacturer Approval (PMA) provider focused on complex hydraulic systems, enhancing its portfolio of line replaceable units.

- In April 2025, HEICO Corp. highlighted its continued operational safety (COS) and voluntary safety management systems (SMS) integration into PMA development and production processes across its FAA-PMA parts manufacturing.

- In May 2025, Parker Hannifin Corp. secured FAA approval for a new line of Parts Manufacturer Approval (PMA) components utilizing advanced composite materials designed for next-generation narrow-body aircraft fuel systems.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Commercial Aircraft Parts Manufacturer Approval (PMA) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 301 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.4% |

| Market growth 2026-2030 | USD 216.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.2% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, UAE, Saudi Arabia, Turkey, South Africa, Israel, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Commercial Aircraft Parts Manufacturer Approval (PMA) market is evolving from a cost-saving alternative to a strategic necessity for airline operations. The integration of advanced technologies such as additive manufacturing and predictive maintenance tools is enabling the production of high-value engine core components and parts for hydraulic systems.

- Boardroom-level decisions are increasingly influenced by the ability of PMA to ensure supply chain resilience, with some operators achieving a 30% reduction in lead times for critical turbine engine components. The development of high-performance alloys and sophisticated reverse-engineering techniques allows for the creation of complex flight control components, avionics subsystems, and environmental control system parts.

- This technological push is expanding the scope of PMA to include items like actuators, latching systems, and even cockpit hardware. As a result, PMA providers are not just replicating parts but are also innovating in areas like thermal barrier layers and high pressure turbine blades, offering enhanced performance and durability for the global fleet.

What are the Key Data Covered in this Commercial Aircraft Parts Manufacturer Approval (PMA) Market Research and Growth Report?

-

What is the expected growth of the Commercial Aircraft Parts Manufacturer Approval (PMA) Market between 2026 and 2030?

-

USD 216 million, at a CAGR of 5.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Engine, Component, and Others), Application (Small widebody, Medium widebody, and Large widebody), Service Type (Certification authority, and Aircraft OEM) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Escalating maintenance, repair, and overhaul expenditures and structural cost reduction pressures, Systemic resistance from OEMs and contractual lifecycle constraints

-

-

Who are the major players in the Commercial Aircraft Parts Manufacturer Approval (PMA) Market?

-

ADPma LLC, Aero Brake and Spares Inc., AMETEK Inc., BAE Systems Plc, Chromalloy Gas Turbine LLC, Eaton Corp. Plc, General Electric Co., HEICO Corp., Honeywell International Inc., Kellstrom Aerospace, Moog Inc., Parker Hannifin Corp., Precision Castparts Corp., RBC Bearings Inc., RTX Corp., Safran SA, Spirit AeroSystems Inc., The Timken Co., TransDigm Group Inc. and Wencor Group LLC

-

Market Research Insights

- Market dynamics are increasingly shaped by sophisticated sourcing strategies aimed at balancing cost and performance. The adoption of green aftermarket solutions aligns with ESG compliance metrics, a factor now influencing over 60% of procurement decisions in some carriers. Meanwhile, blockchain traceability systems are enhancing life-limited part management, reducing tracking errors by up to 95%.

- Airlines are leveraging these technologies to validate carbon-neutral manufacturing claims and support sustainable procurement policies. This data-driven approach to acquiring parts like actuators and thermal barrier layers provides a verifiable record of component history, which is critical for meeting stringent airworthiness standards and maintaining aircraft value.

- The ability to track a high pressure turbine blade from production to installation using an immutable ledger represents a significant leap in operational integrity.

We can help! Our analysts can customize this commercial aircraft parts manufacturer approval (pma) market research report to meet your requirements.

RIA -

RIA -