Condition Monitoring Sensors For Heavy Industry Market Size and Growth Forecast 2026-2030

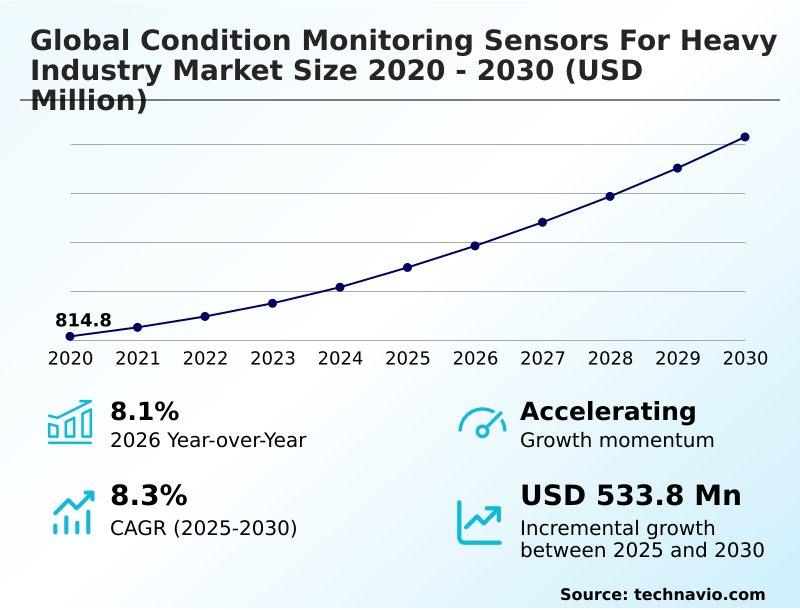

The Condition Monitoring Sensors For Heavy Industry Market size was valued at USD 1.10 billion in 2025 growing at a CAGR of 8.3% during the forecast period 2026-2030.

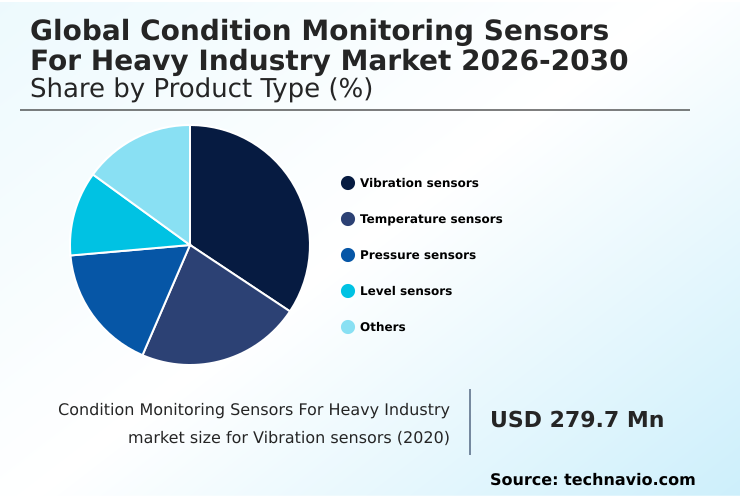

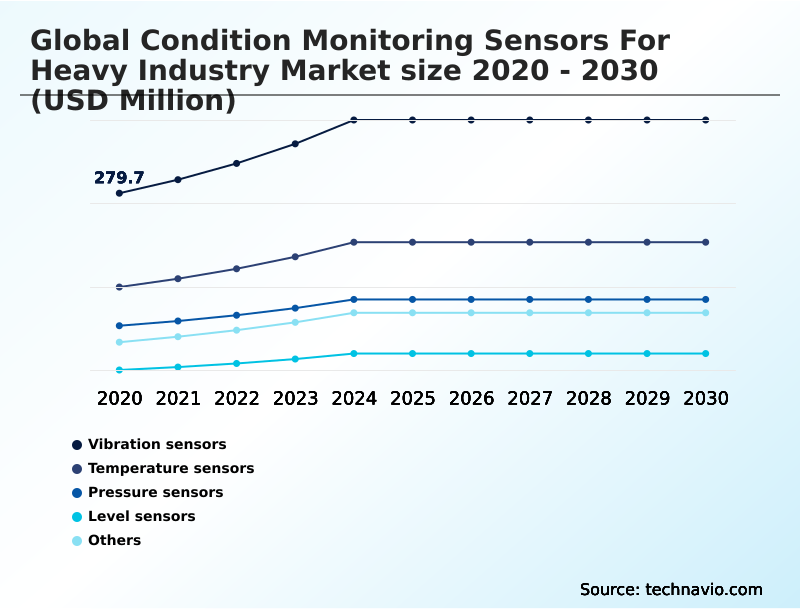

APAC accounts for 43.6% of incremental growth during the forecast period. The Vibration sensors segment by Product Type was valued at USD 357.1 million in 2024, while the Oil and gas segment holds the largest revenue share by End-user.

The market is projected to grow by USD 815.7 million from 2020 to 2030, with USD 533.8 million of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Condition Monitoring Sensors For Heavy Industry Market Overview

The condition monitoring sensors for heavy industry market is driven by the industrial imperative to maximize asset performance management and achieve greater operational efficiency improvement. With APAC poised to contribute over 43% of the market's incremental growth, the shift towards data-driven maintenance strategy optimization is a global phenomenon. In a typical integrated steel mill, for instance, the deployment of an automated diagnostic tools on continuous casting lines allows for the pre-emptive detection of roll misalignment, preventing costly production halts and improving final product quality. This real-time data acquisition feeds into digital twin integration models, enabling engineers to simulate stress conditions and refine operational parameters without physical intervention. This strategic pivot away from reactive repairs facilitates significant unplanned downtime reduction, directly impacting bottom-line profitability and reinforcing the business case for investment in advanced sensing and analytics platforms that comply with standards like ISO 50001.

Drivers, Trends, and Challenges in the Condition Monitoring Sensors For Heavy Industry Market

The strategic adoption of condition monitoring is becoming a prerequisite for competing in capital-intensive sectors, with the market expected to expand by nearly 50% during the forecast period.

The deployment of a wireless vibration sensor for pumps or an oil analysis sensor for gearboxes is no longer a niche practice but a core component of a modern ai-based predictive maintenance platform.

A key driver is compliance with standards like ISO 50001, which compels facilities to optimize energy use, making temperature monitoring for electric motors and motor current analysis for fault diagnosis essential. In practice, a large-scale iiot solution for oil refineries integrates thousands of sensors, including those for high-temperature industrial environments and pressure sensors for hydraulic systems.

This enables edge analytics for rotating machinery and facilitates prescriptive maintenance for power turbines, averting failures before they occur. The process of retrofitting legacy assets with sensors, while complex, is critical for achieving the cost of unplanned downtime reduction. Overcoming challenges related to cybersecurity in industrial sensor networks and ensuring seamless data integration with cmms software are key hurdles.

Furthermore, addressing the need for specialized training for reliability engineers is vital to translate sensor data from a non-contact sensor for steel rolling or an acoustic sensor for bearing fault into actionable intelligence. This is especially true for remote monitoring for offshore wind turbines and condition monitoring for mining conveyors or bulk material silos, where on-site expertise is scarce.

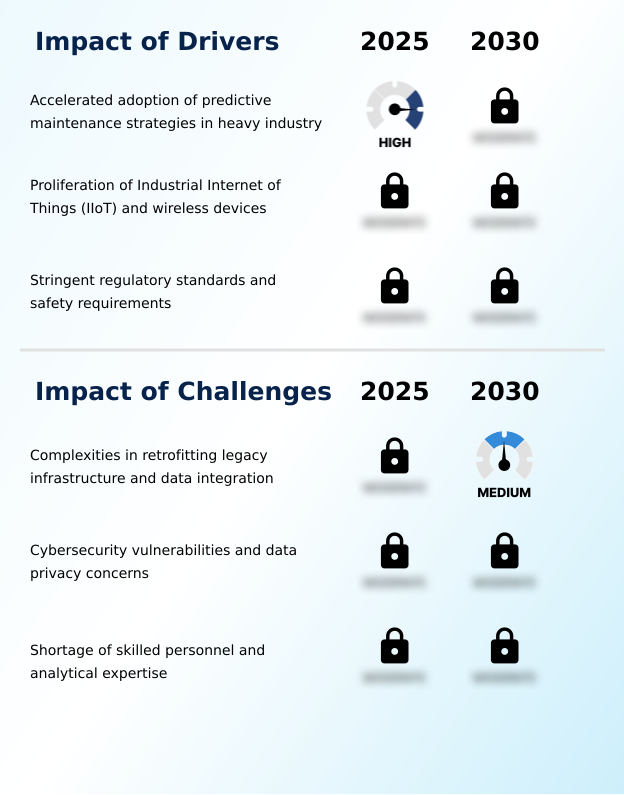

Primary Growth Driver: The accelerated adoption of predictive maintenance strategies across heavy industries is the primary driver for market expansion.

The market is primarily driven by the accelerated adoption of predictive maintenance strategies to achieve significant operational efficiency improvement and asset lifecycle extension.

With heavy industries in APAC contributing over 43% of incremental market growth, the business case for preventing unplanned downtime reduction is clear.

The widespread proliferation of IIoT and wireless devices has dramatically lowered the cost and complexity of instrumenting assets, making comprehensive monitoring economically viable.

Furthermore, increasingly stringent regulatory standards, such as those governing emissions and worker safety, compel operators to invest in high-fidelity sensing technologies.

This creates a powerful incentive to deploy systems that not only enhance productivity but also ensure compliance and mitigate operational risk, solidifying the role of condition monitoring as an essential industrial technology.

Emerging Market Trend: A defining market trend is the integration of edge computing and artificial intelligence directly onto sensor hardware, enabling real-time, on-device analytics and decision-making.

Key market trends are centered on the integration of edge computing and AI on sensor hardware, enabling autonomous industrial operations. This shift moves processing from the cloud to the device, allowing machine learning models to perform real-time analytics directly on IIoT gateway devices.

The evolution toward prescriptive analytics is another significant trend, where systems not only predict failures but also recommend specific corrective actions, maximizing operational uptime. The proliferation of private 5G networks is facilitating the deployment of thousands of wireless sensors in dense industrial environments, providing the high-bandwidth, low-latency communication required for critical control loops.

These advancements are transforming condition monitoring from a diagnostic tool into a strategic pillar of asset management, with the vibration sensors segment alone accounting for a significant portion of the market.

Key Industry Challenge: Complexities in retrofitting legacy infrastructure and ensuring seamless data integration across disparate systems present a significant challenge to market growth.

A primary market challenge is the complexity of retrofitting legacy infrastructure, which often involves custom engineering and significant downtime. The subsequent data integration challenges of creating a unified view from disparate, proprietary systems hinder the realization of holistic asset health monitoring.

Furthermore, the convergence of IT-OT systems expands the threat surface, making cybersecurity for OT systems a major concern for operators, with compliance frameworks like NERC CIP adding layers of complexity. This fear of cyber threats can slow the adoption of cloud-connected sensors.

Finally, a persistent shortage of skilled personnel capable of managing and interpreting complex data streams creates a bottleneck, increasing the total cost of ownership and limiting the return on investment from advanced sensor deployments.

Explore Full Market Dynamics Analysis Request Free Sample

Condition Monitoring Sensors For Heavy Industry Market Segmentation

The condition monitoring sensors for heavy industry industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Product Type Segment Analysis

The vibration sensors segment is estimated to witness significant growth during the forecast period.

Vibration sensors represent the most significant segment, commanding approximately 31% of the market, due to their unmatched capability for early bearing fault detection in rotating equipment.

These devices, including advanced piezoelectric accelerometers and MEMS-based units, are the foundation of machinery protection systems.

In heavy industrial environments, where assets like turbines and compressors are mission-critical, high-frequency data sampling from triaxial vibration sensors provides the granular data needed for precise rotating equipment diagnostics.

The integration of this technology into a broader maintenance strategy optimization plan allows operators to identify issues such as imbalance or misalignment, which are precursors to catastrophic failure.

This focus on proactive gearbox health assessment and asset integrity underscores the segment's critical role in modern industrial operations.

The Vibration sensors segment was valued at USD 357.1 million in 2024 and showed a gradual increase during the forecast period.

Condition Monitoring Sensors For Heavy Industry Market by Region: APAC Leads with 43.6% Growth Share

APAC is estimated to contribute 43.6% to the growth of the global market during the forecast period.

The geographic landscape is dominated by APAC, which is set to account for 43.6% of the market's incremental growth, driven by massive industrialization and greenfield projects.

In this region, the adoption of wireless sensor nodes and lorawan connectivity is accelerating to instrument vast manufacturing facilities in China and India. In contrast, North America and Europe, which represent mature markets, focus on retrofitting aging infrastructure.

Here, demand is strong for high-temperature accelerometers and submersible pressure sensors to modernize power generation and chemical processing plants. These regions prioritize industrial accelerometer technology that complies with stringent environmental and safety regulations.

The deployment of harsh environment sensors is a common requirement across all geographies, especially in the mining sectors of Australia and South America, where equipment reliability is paramount.

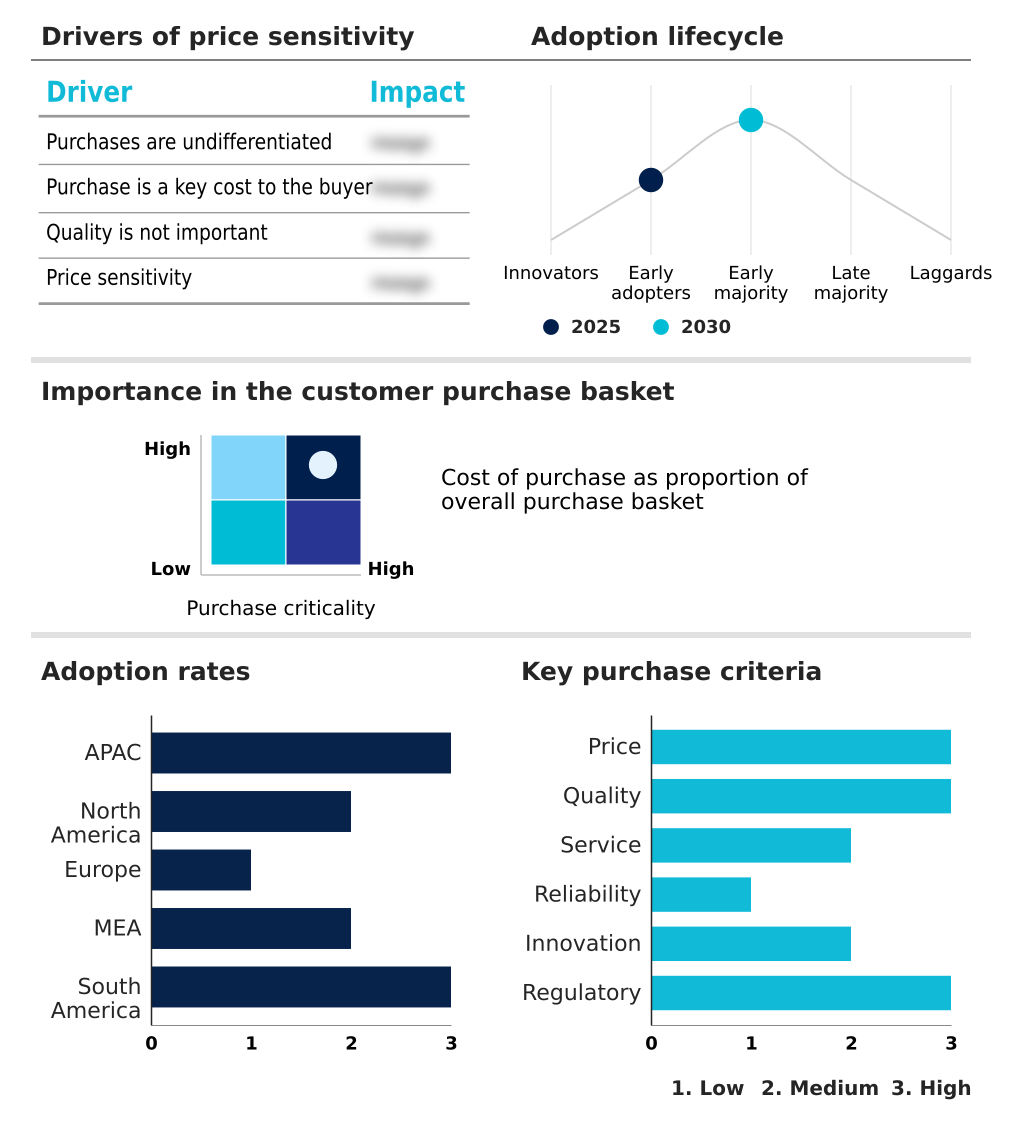

Customer Landscape Analysis for the Condition Monitoring Sensors For Heavy Industry Market

The condition monitoring sensors for heavy industry market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the condition monitoring sensors for heavy industry market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Condition Monitoring Sensors For Heavy Industry Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the condition monitoring sensors for heavy industry market industry.

AB SKF - Offers specialized vibration sensors and handheld data collectors, leveraging deep bearing expertise integrated with proprietary monitoring systems for comprehensive machine health assessment.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AB SKF

- ABB Ltd.

- Amphenol Corp.

- Baker Hughes Co.

- Balluff GmbH

- Banner Engineering Corp.

- Baumer Holding AG

- Emerson Electric Co.

- Fluke Corp.

- Hansford Sensors Ltd.

- Honeywell International Inc.

- Keyence Corp.

- Kistler Group

- PCB Piezotronics Inc.

- Rockwell Automation Inc.

- Schaeffler AG

- Siemens AG

- SPM Instrument

- TE Connectivity plc

- Teledyne FLIR LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Condition Monitoring Sensors For Heavy Industry Market

- In April 2025, Waites Sensor Technologies Inc. launched PiezoNode, an advanced quad-channel condition monitoring device designed for high-heat, high-stress rotating equipment like turbines and generators in heavy industrial operations.

- In March 2025, Etop launched its Wireless Humidity and Temperature Sensor, engineered for precise environmental monitoring in industrial settings and agriculture, providing a complete solution for tracking ambient conditions.

- In May 2025, ABB Ltd. introduced an upgraded NINVA TSP341-N non-invasive temperature sensor, facilitating safer and simpler temperature measurement for chemical and oil and gas applications.

- In January 2025, Rockwell Automation Inc. announced a strategic partnership with a major cloud provider to integrate its Dynamix monitoring modules with AI-driven analytics, enabling a scalable prescriptive maintenance-as-a-service offering.

Research Analyst Overview: Condition Monitoring Sensors For Heavy Industry Market

Boardroom decisions regarding capital expenditure are increasingly tied to asset performance management, with the market showing an 8.1% year-over-year growth. The focus is on deploying advanced industrial accelerometer technology, including piezoelectric accelerometers and MEMS vibration sensors, for high-frequency data sampling to enable precise bearing fault detection.

This strategic shift is compelling investment in prescriptive analytics software and predictive maintenance algorithms that leverage machine learning models for superior rotating equipment diagnostics. The integration of thermal imaging cameras and non-contact infrared sensors provides a multi-parameter view, enhancing the accuracy of remote diagnostics platforms.

The adoption of intrinsically safe sensors is non-negotiable in environments governed by ATEX directives, driving demand for certified hydraulic system monitoring and pneumatic system diagnostics. This requires a robust data normalization architecture to manage IT-OT convergence securely.

As such, the selection of wireless sensor nodes, IIoT gateway devices, and private 5G or LoRaWAN connectivity is now a critical infrastructure decision, impacting everything from pump performance monitoring to comprehensive structural health monitoring.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Condition Monitoring Sensors For Heavy Industry Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 312 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.3% |

| Market growth 2026-2030 | USD 533.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.1% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, UAE, Saudi Arabia, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Condition Monitoring Sensors For Heavy Industry Market: Key Questions Answered in This Report

-

What is the expected growth of the Condition Monitoring Sensors For Heavy Industry Market between 2026 and 2030?

-

The Condition Monitoring Sensors For Heavy Industry Market is expected to grow by USD 533.8 million during 2026-2030, registering a CAGR of 8.3%. Year-over-year growth in 2026 is estimated at 8.1%%. This acceleration is shaped by accelerated adoption of predictive maintenance strategies in heavy industry, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Product Type (Vibration sensors, Temperature sensors, Pressure sensors, Level sensors, and Others), End-user (Oil and gas, Power generation, Mining and mineral processing, Steel and iron manufacturing, and Cement manufacturing), Type (Wired sensors, and Wireless sensors) and Geography (APAC, North America, Europe, Middle East and Africa, South America). Among these, the Vibration sensors segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC, North America, Europe, Middle East and Africa and South America. APAC is estimated to contribute 43.6% to market growth during the forecast period. Country-level analysis includes China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, UAE, Saudi Arabia, South Africa, Israel, Turkey, Brazil, Argentina and Colombia, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is accelerated adoption of predictive maintenance strategies in heavy industry, which is accelerating investment and industry demand. The main challenge is complexities in retrofitting legacy infrastructure and data integration, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Condition Monitoring Sensors For Heavy Industry Market?

-

Key vendors include AB SKF, ABB Ltd., Amphenol Corp., Baker Hughes Co., Balluff GmbH, Banner Engineering Corp., Baumer Holding AG, Emerson Electric Co., Fluke Corp., Hansford Sensors Ltd., Honeywell International Inc., Keyence Corp., Kistler Group, PCB Piezotronics Inc., Rockwell Automation Inc., Schaeffler AG, Siemens AG, SPM Instrument, TE Connectivity plc and Teledyne FLIR LLC. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Condition Monitoring Sensors For Heavy Industry Market Research Insights

The market's dynamics are shaped by the critical need for harsh environment sensors and explosion-proof enclosures, particularly in sectors governed by strict OSHA mandates. Procurement decisions are increasingly influenced by the total cost of ownership, where the initial expense of legacy equipment retrofitting is weighed against the long-term return on investment calculation from averted failures.

A key challenge remains the data integration challenges associated with connecting disparate OT systems, which can complicate deployment. For instance, in an offshore oil and gas facility, the use of remote monitoring services is essential for assets in hazardous or inaccessible locations.

The high cost of sensor failure in such settings elevates the importance of reliability and durability over initial purchase price, driving demand for premium, certified solutions.

We can help! Our analysts can customize this condition monitoring sensors for heavy industry market research report to meet your requirements.

RIA -

RIA -