Corrugated Box Market Size 2026-2030

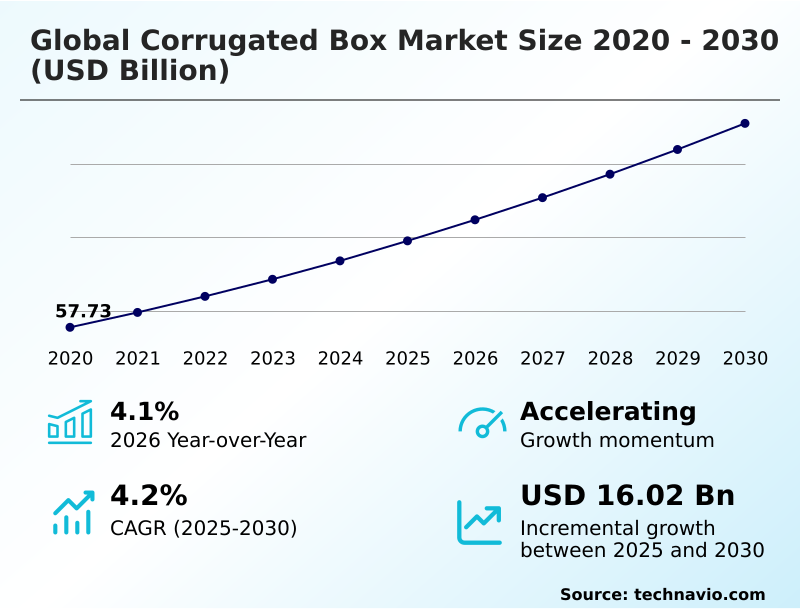

The corrugated box market size is valued to increase by USD 16.02 billion, at a CAGR of 4.2% from 2025 to 2030. Proliferation of global E-commerce and digital retail logistics will drive the corrugated box market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 60.8% growth during the forecast period.

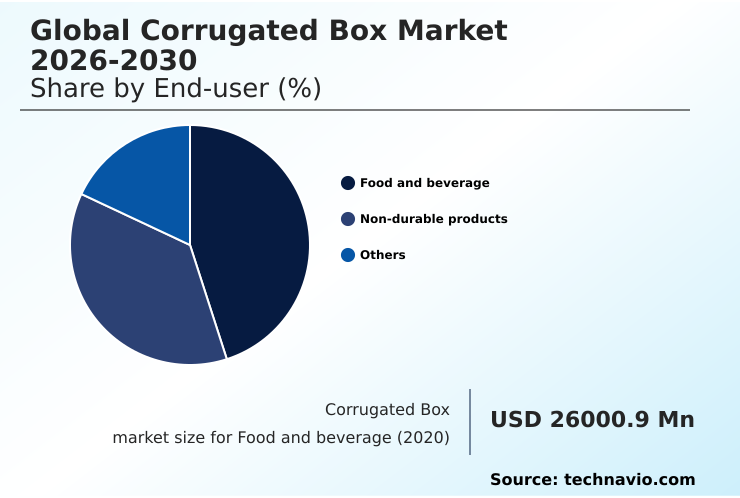

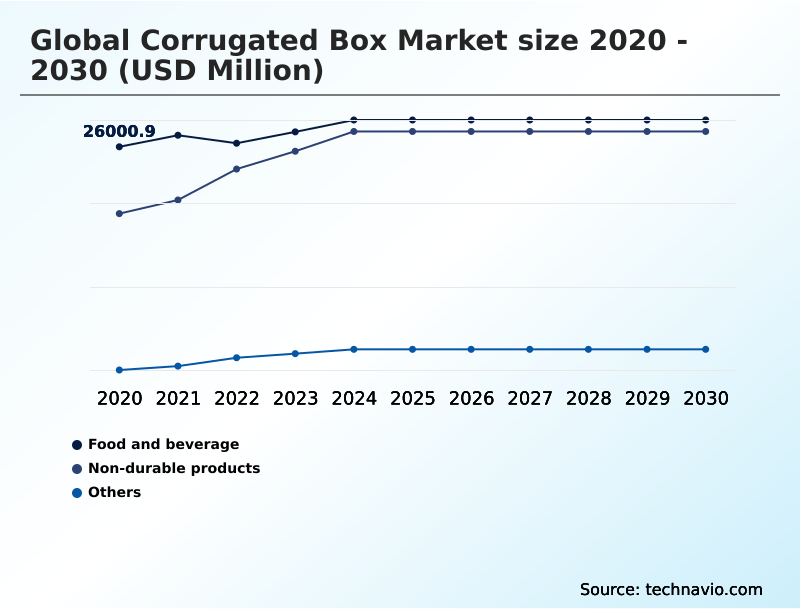

- By End-user - Food and beverage segment was valued at USD 27.87 billion in 2024

- By Application - Linerboard segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 27.80 billion

- Market Future Opportunities: USD 16.02 billion

- CAGR from 2025 to 2030 : 4.2%

Market Summary

- The corrugated box market is undergoing a significant transformation, driven by shifts toward circular economy models and advanced logistics. As a cornerstone of the global supply chain, this sector provides the essential medium for transporting everything from consumer electronics to perishable foods.

- The recyclability of fiber-based materials has made corrugated solutions a preferred alternative to plastic packaging, especially as regulations on single-use materials tighten. A key business scenario involves a large food distributor optimizing its cold chain logistics. By adopting corrugated boxes with advanced moisture-resistant coatings and integrating box-on-demand systems, the company can reduce material waste and achieve right-sizing for its shipments.

- This not only lowers dimensional weight and freight costs but also improves product protection, reducing spoilage rates. Innovations in linerboard quality and fluting designs allow for material lightweighting without sacrificing stacking strength.

- Furthermore, the integration of digital printing technologies is transforming the corrugated box from a simple container into a high-value marketing asset, enabling brands to customize packaging and enhance the consumer unboxing experience. This evolution reflects the market's adaptation to the dual demands of logistical efficiency and brand communication.

What will be the Size of the Corrugated Box Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Corrugated Box Market Segmented?

The corrugated box industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Food and beverage

- Non-durable products

- Others

- Application

- Linerboard

- Corrugating medium

- Grade type

- Lightweight grade

- Medium‑weight grade

- High‑burst grade

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By End-user Insights

The food and beverage segment is estimated to witness significant growth during the forecast period.

The food and beverage segment is a primary user of corrugated boxes, functioning as critical secondary packaging. The rise of e-commerce grocery services and the demand for high-graphic corrugated boxes for shelf-ready packaging are key factors.

Advanced moisture-resistant coatings have expanded the use of paper-based packaging into cold chain logistics, where a lightweight grade with a specialized corrugating medium can offer protection without adding significant dimensional weight.

These coatings have improved product integrity during transit by over 15%. This shift enhances the unboxing experience and supports the use of custom shipping boxes.

Innovations in micro-fluting technologies are growing for premium goods, while some bulk liquids utilize a form of triple-wall construction, replacing what was once a medium-weight grade application.

The Food and beverage segment was valued at USD 27.87 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 60.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Corrugated Box Market Demand is Rising in APAC Get Free Sample

The geographic landscape is dominated by the APAC region, accounting for over 60% of incremental growth due to its massive manufacturing base for industrial packaging and consumer goods packaging.

In contrast, Europe's market, focused on supply chain optimization, is driven by stringent regulations mandating sustainable packaging solutions; its high recycling rates provide a steady stream of material for testliner.

North America emphasizes performance, with a high demand for double-wall corrugated boxes with advanced fluting designs to ensure stacking strength for logistics networks. Innovations in aseptic packaging for food and beverage packaging are prominent in both Europe and North America.

The use of high-quality kraft linerboard is common for exports from all regions, while the push for returnable packaging systems is gaining traction globally.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The corrugated box market is advancing beyond standard containers, with innovation centered on specialized applications. The development of high-strength lightweight corrugated paper is critical for air freight and e-commerce, where every gram impacts cost. This pairs with right-sizing technology for packaging optimization, which uses automated fit-to-product packaging systems to minimize waste.

- For high-value goods, smart packaging for supply chain transparency is becoming standard, using embedded sensors for real-time tracking. Custom corrugated shipping containers design now incorporates advanced coatings for food contact safety and tamper-evident features for pharmaceutical security. The industry is also exploring bio-based resins for enhanced burst strength, improving the performance of multi-wall corrugated for heavy machinery without compromising sustainability.

- For agricultural exports, moisture-resistant corrugated board for agriculture is essential for corrugated packaging for cold chain integrity. From a material perspective, linerboard quality for high-resolution printing is a key differentiator, as is the corrugating medium for compression strength.

- The use of lightweight grade corrugated for e-commerce contrasts with medium-weight grade for industrial goods and high-burst grade for hazardous materials, demonstrating the market's segmentation. Across all grades, increasing recycled fiber content in containerboard and finding sustainable alternatives to plastic void-fill are universal goals, pushing the industry toward more advanced circular economy models in paper packaging.

- Companies adopting these technologies report a significantly higher product-in-transit survival rate compared to those using traditional, non-specialized packaging.

What are the key market drivers leading to the rise in the adoption of Corrugated Box Industry?

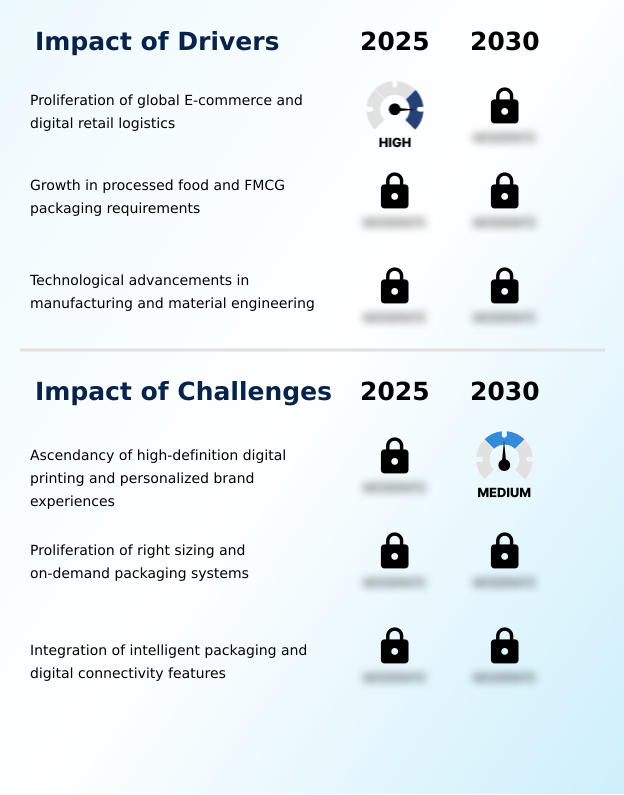

- The proliferation of global e-commerce and the intricate logistics of digital retail are primary drivers propelling market growth.

- The primary market driver is the relentless growth of e-commerce fulfillment and the direct-to-consumer business model, which demand efficient supply chain optimization.

- This has accelerated the adoption of on-demand packaging solutions like box-on-demand systems, which utilize right-sizing technology to reduce material use by an average of 30%.

- The focus on lightweighting, using high-performance liners in paper-based packaging, has lowered shipping costs for 65% of high-volume shippers.

- Technologically, advancements in die cutting and fiber recovery systems enhance the viability of using secondary fibers from old corrugated containers, making recycled content more cost-effective.

- These drivers converge to create a market focused on minimizing waste, reducing freight expenses, and maximizing the efficiency of packaging operations from the factory floor to the consumer's doorstep.

What are the market trends shaping the Corrugated Box Industry?

- The rapid expansion of e-commerce fulfillment is converging with the logistical complexities of omnichannel retail. This creates a significant, ongoing trend within the market.

- Market trends are driven by digitization and customization. The adoption of digital inkjet printing over traditional flexographic printing allows for cost-effective, short-run production of retail-ready packaging, reducing setup times by up to 90%. This enables brands to create modular designs for seasonal campaigns. Concurrently, smart packaging technology is gaining traction.

- The integration of quick response codes and radio frequency identification tags is improving traceability in the last-mile delivery stage, with some logistics firms reporting a 15% reduction in lost parcels. For product protection, there is a clear shift away from plastic void-fill materials toward sustainable inserts like molded pulp.

- These trends are supported by automated packaging systems that create tamper-evident designs and align with emerging digital product passport requirements, transforming the package into a data-rich asset.

What challenges does the Corrugated Box Industry face during its growth?

- The ascendancy of high-definition digital printing and the demand for personalized brand experiences present a significant challenge, driving capital investment and operational complexity.

- Significant challenges stem from raw material volatility and regulatory pressures. Fluctuating pulp prices and the consolidation of paper mills create an unpredictable cost environment for virgin kraft paper and containerboard. While recycled fiber technologies offer an alternative, inconsistent quality can affect performance metrics like the edge crush test and burst strength, compromising the reliability of protective packaging.

- This impacts supply chain resilience, as some manufacturers have reported a 10% failure rate increase when using lower-grade recycled content for heavy-duty corrugated containers. Furthermore, new extended producer responsibility laws in several regions are holding producers financially accountable for packaging waste, adding up to 5% to the cost of goods.

- This forces a difficult balance between meeting circular economy principles and maintaining profitability, especially when competing with single-use plastics alternatives on price.

Exclusive Technavio Analysis on Customer Landscape

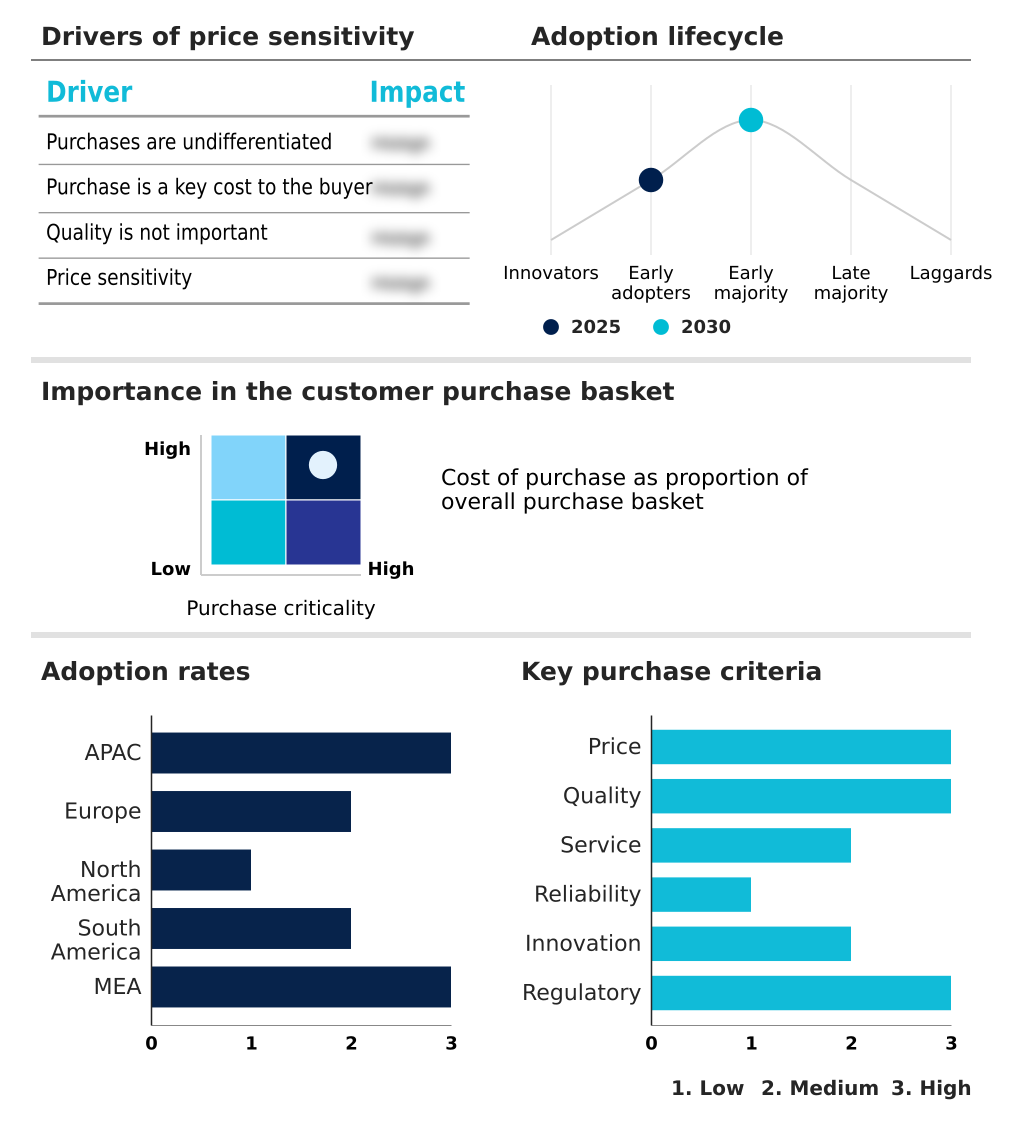

The corrugated box market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the corrugated box market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Corrugated Box Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, corrugated box market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alliance Packaging - Key offerings focus on integrated, sustainable packaging solutions, including custom corrugated containers, retail-ready displays, and advanced industrial packaging designed for comprehensive supply chain optimization.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alliance Packaging

- Bio pappel

- DS Smith Plc

- Georgia Pacific LLC

- Green Bay Packaging Inc.

- International Paper Co.

- Klabin S.A.

- Lee and Man Paper Manufacturing

- Menasha Corp

- Mondi Plc

- Nine Dragons Paper Holdings Ltd.

- Packaging Corp. of America

- Pratt Industries Inc.

- Rengo Co. Ltd.

- S.A Industrias Celulosa Aragonesa

- Shanying International Holding

- Smurfit Westrock plc

- Stora Enso Oyj

- THIMM Group GmbH plus Co. KG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Corrugated box market

- In January 2025, International Paper Co. completed its acquisition of DS Smith Plc for approximately $7.2 billion, creating a global leader in sustainable packaging with significant operations across North America and Europe.

- In November 2024, a leading multinational food and beverage corporation launched a sustainable packaging strategy to make its portfolio 100% recyclable or reusable, emphasizing a shift to paper-based and corrugated solutions.

- In August 2024, a major e-commerce retailer announced a 16% reduction in its global plastic packaging by expanding its use of 100% recycled paper fillers and paper-padded envelopes across its fulfillment network.

- In May 2025, leading Chinese packaging firms reported a strategic pivot to domestic production of high-strength, lightweight corrugated paper to reduce reliance on raw material imports following stricter environmental protocols.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Corrugated Box Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.2% |

| Market growth 2026-2030 | USD 16018.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.1% |

| Key countries | China, India, Japan, South Korea, Indonesia, Vietnam, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Egypt and Qatar |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The corrugated box market's evolution is driven by material science and process innovation. Central to this is the engineering of corrugated fiberboard, where linerboard provides burst strength and the corrugating medium offers cushioning through optimized fluting designs. Manufacturers balance the use of virgin kraft paper, specifically kraft linerboard, with testliner made from old corrugated containers.

- The push for lightweighting has spurred high-performance liners and micro-fluting technologies, reducing dimensional weight without sacrificing stacking strength. For heavy-duty applications, double-wall corrugated boxes and even triple-wall construction are standard.

- A key boardroom decision involves balancing the cost of pulp prices from paper mills against investments in recycled fiber technologies and fiber recovery systems to improve the quality of secondary fibers. Operationally, box-on-demand systems and automated packaging systems are improving efficiency in die cutting and assembly of modular designs.

- Digital inkjet printing and flexographic printing are transforming boxes into marketing tools, while moisture-resistant coatings and bio-based resins enhance physical properties, measured by the edge crush test.

- This focus on material innovation, such as using molded pulp for inserts instead of void-fill materials, has allowed some firms to improve their product protection efficiency by over 20%, impacting everything from tamper-evident designs in aseptic packaging to the overall integrity of containerboard.

What are the Key Data Covered in this Corrugated Box Market Research and Growth Report?

-

What is the expected growth of the Corrugated Box Market between 2026 and 2030?

-

USD 16.02 billion, at a CAGR of 4.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Food and beverage, Non-durable products, and Others), Application (Linerboard, and Corrugating medium), Grade Type (Lightweight grade, Medium‑weight grade, and High‑burst grade) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Proliferation of global E-commerce and digital retail logistics, Ascendancy of high-definition digital printing and personalized brand experiences

-

-

Who are the major players in the Corrugated Box Market?

-

Alliance Packaging, Bio pappel, DS Smith Plc, Georgia Pacific LLC, Green Bay Packaging Inc., International Paper Co., Klabin S.A., Lee and Man Paper Manufacturing, Menasha Corp, Mondi Plc, Nine Dragons Paper Holdings Ltd., Packaging Corp. of America, Pratt Industries Inc., Rengo Co. Ltd., S.A Industrias Celulosa Aragonesa, Shanying International Holding, Smurfit Westrock plc, Stora Enso Oyj and THIMM Group GmbH plus Co. KG

-

Market Research Insights

- Market dynamics are increasingly shaped by the push for greater efficiency and sustainability. The adoption of on-demand packaging solutions, which create custom-sized boxes for each order, has been shown to reduce material consumption by up to 40%. This right-sizing technology directly impacts supply chain optimization, as it can lower dimensional weight shipping costs by an average of 25%.

- Concurrently, the integration of smart packaging technology, such as RFID tags, is enhancing visibility. This allows companies to track assets through the supply chain with over 99% accuracy, improving inventory management and reducing losses, thereby providing a clear path to enhanced profitability and operational control.

We can help! Our analysts can customize this corrugated box market research report to meet your requirements.

RIA -

RIA -