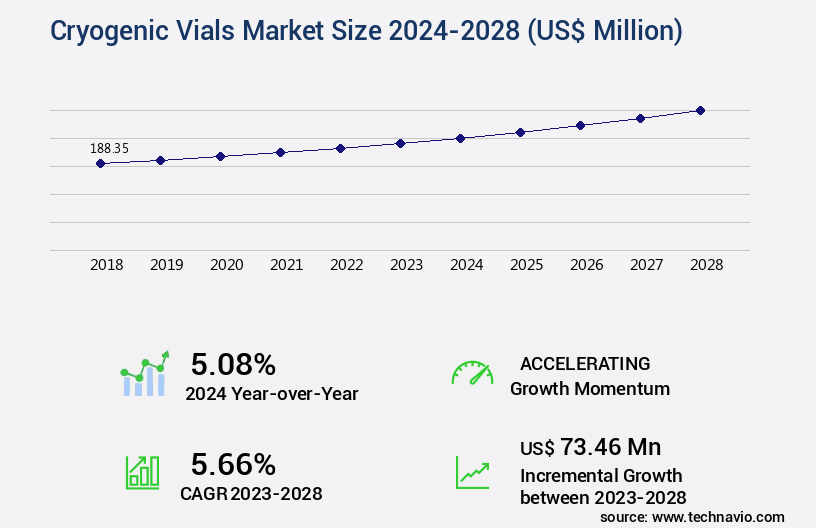

Cryogenic Vials Market Size 2024-2028

The cryogenic vials market size is valued to increase by USD 73.46 million, at a CAGR of 5.66% from 2023 to 2028. Increasing adoption of cryopreservation procedures will drive the cryogenic vials market.

Market Insights

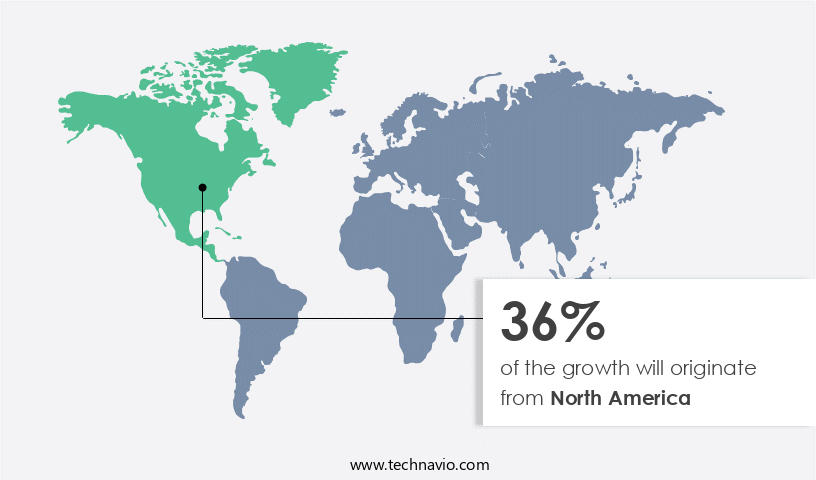

- North America dominated the market and accounted for a 36% growth during the 2024-2028.

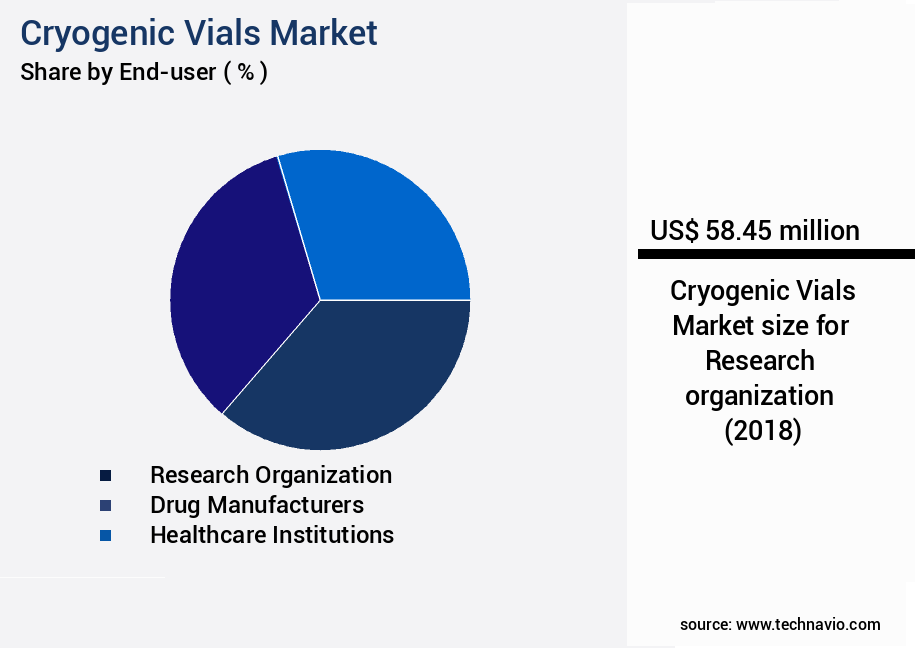

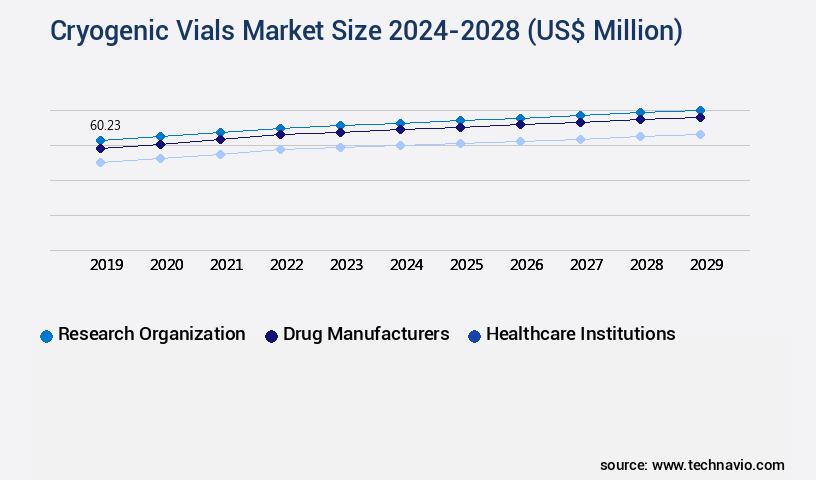

- By End-user - Research organization segment was valued at USD 58.45 million in 2022

- By Type - Internally threaded cryogenic vials segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 62.01 million

- Market Future Opportunities 2023: USD 73.46 million

- CAGR from 2023 to 2028 : 5.66%

Market Summary

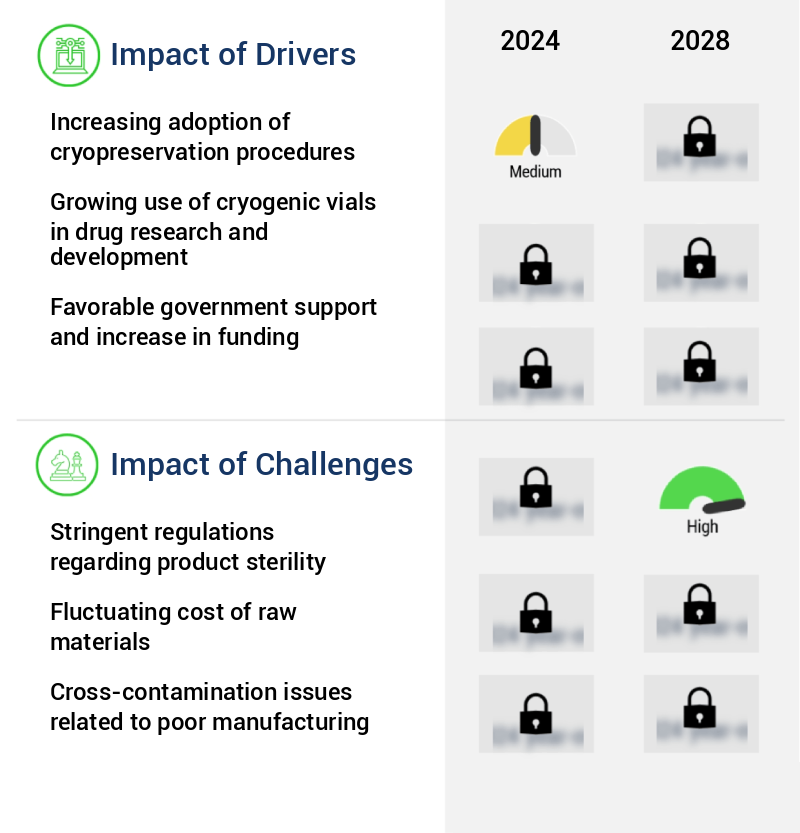

- The market witnesses significant growth driven by the increasing adoption of cryopreservation procedures in various industries, including healthcare and biotechnology. This trend is fueled by advancements in medical technology, leading to an increase in the number of cryopreserved specimens and samples. Furthermore, the growing preference for barcoded cryogenic vials to ensure traceability and improve supply chain management adds to the market's momentum. However, stringent regulations regarding product sterility pose a challenge to market participants. These regulations necessitate rigorous testing and adherence to quality standards, increasing the production costs and, subsequently, the selling price of cryogenic vials.

- For instance, a biotechnology company may optimize its operations by implementing a robust quality control system to ensure the production of sterile cryogenic vials, thereby maintaining regulatory compliance and enhancing customer trust. This scenario underscores the importance of maintaining stringent quality standards in the market.

What will be the size of the Cryogenic Vials Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, driven by advancements in technology and increasing applications across various industries. In the realm of vaccine development, cryogenic vials play a crucial role in storing and transporting vaccines at ultra-low temperatures. According to recent studies, the demand for cryogenic vials in the pharmaceutical sector is projected to grow by 15% annually, reflecting the market's dynamic nature. Moreover, in forensic science, cryogenic vials are used for DNA archiving, ensuring the preservation of crucial evidence for extended periods. In agricultural research, these vials are employed for storing plant samples at low temperatures, enhancing their longevity and viability.

- The integration of temperature sensors and cold chain management systems in cryogenic vials further bolsters their appeal, enabling precise temperature control and enhancing the quality assurance of stored samples. In the field of stem cell research, cryogenic vials are essential for preserving and transporting these valuable cells, contributing to significant breakthroughs in regenerative medicine. Additionally, in the areas of microbial preservation, protein stability, and RNA preservation, cryogenic vials offer optimal conditions for maintaining sample integrity. As businesses navigate the complexities of research workflows and compliance requirements, cryogenic vials have emerged as a critical investment for ensuring efficient sample handling and long-term storage.

- By integrating advanced features such as material science, vial design, and data management systems, manufacturers cater to the evolving needs of diverse industries, ultimately driving the growth of the market.

Unpacking the Cryogenic Vials Market Landscape

In the realm of low-temperature storage, cryogenic freezing emerges as a preferred method for preserving sensitive biological materials, surpassing traditional refrigeration techniques in terms of sample viability and long-term storage capabilities. Cryogenic freezing protocols, implemented in cryo-storage tanks, ensure optimal temperature uniformity, thereby enhancing inventory management and reducing potential contamination risks. Automated storage systems with barcode tracking facilitate efficient sample handling and ensure compliance with regulatory requirements. Cryopreservation methods, such as freezing rate control and vial sealing, safeguard sample integrity during the freezing and thawing processes. Insulation materials, like vapor shields, and temperature monitoring systems ensure consistent liquid nitrogen storage temperatures, preventing thermal shock and maintaining sample quality. Cryogenic transport solutions enable secure and efficient sample transportation, further expanding the reach and utility of cryopreservation techniques. Material compatibility and freezer maintenance are crucial aspects of cryogenic storage, ensuring the longevity of both the samples and the storage infrastructure. By implementing advanced cryoprotective agents and adhering to rigorous quality control measures, businesses can reap significant benefits, including improved ROI through extended sample lifespan and enhanced research capabilities.

Key Market Drivers Fueling Growth

The significant increase in the utilization of cryopreservation techniques is the primary growth factor for the market. This trend is driven by advancements in technology and growing acceptance of cryopreservation methods in various industries, including healthcare and biotechnology.

- The market encompasses the production and distribution of specialized containers used for cryopreservation, a procedure that employs ultra-low temperatures below 150 degrees Celsius to preserve biological samples. This technique is gaining traction in a multitude of sectors, including cell and organ preservation, molecular biology and biochemistry, cryosurgery, food sciences, and medical applications. By employing efficient cryopreservation methods, laboratories, clinics, and research institutions can significantly reduce costs associated with frequently ordering stock supplies. The demand for cryopreservation of cells, such as hepatocytes, cardiomyocytes, and neuronal cells, has surged due to their crucial role in neuroscience and cardiology research. The implementation of cryopreservation technology has led to a reduction in sample deterioration and an enhancement of consistency and reproducibility across various applications.

Prevailing Industry Trends & Opportunities

The increasing use of barcoded cryogenic vials represents a significant market trend. This innovation in laboratory technology enhances efficiency and accuracy in sample identification and storage.

- The market is experiencing significant growth due to the increasing adoption of automation technologies and laboratory information management systems (LIMS) in various sectors. The implementation of these systems necessitates the use of easily trackable and recordable supplies, leading to a surge in demand for advanced cryogenic vials. companies in the global market are responding by introducing 1D and 2D barcoded cryogenic vials to cater to this need. These technologically advanced vials have gained popularity among biobanks and cell banks, which handle large quantities and diverse types of biomaterials. By integrating these vials with LIMS and inventory management software, end-users can effortlessly maintain records and ensure efficient inventory management.

- This integration results in enhanced traceability, improved data accuracy, and streamlined operations.

Significant Market Challenges

Strict regulations concerning product sterility pose a significant challenge to the industry's growth. Adhering to these stringent guidelines adds complexity and cost to manufacturing processes, potentially hindering innovation and expansion within the sector.

- The market is a significant sector within the broader biotechnology industry, characterized by its evolving nature and diverse applications in highly regulated sectors such as medical, biotechnology, and pharmaceutical industries. These applications necessitate adherence to stringent regulatory requirements set forth by regulatory authorities like the US FDA, China Food and Drug Administration (CFDA), and the European Medicines Agency (EMA), ensuring the use of products and supplies of optimum quality standards. Cryopreservation technology, which relies on cryogenic vials, is crucial in maintaining the purity and integrity of stored products like antibodies, cell suspensions, proteins, and nucleic acids over extended periods.

- companies offering cryogenic vials are subjected to stringent quality, purity, and sterility standards to prevent contamination during long-term storage. This focus on maintaining high-quality standards translates into operational cost savings for end-users, with studies suggesting that effective cryopreservation can reduce downtime by up to 30% and improve product yield by approximately 15%.

In-Depth Market Segmentation: Cryogenic Vials Market

The cryogenic vials industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Research organization

- Drug manufacturers

- Healthcare institutions

- Others

- Type

- Internally threaded cryogenic vials

- Externally threaded cryogenic vials

- Geography

- North America

- US

- Europe

- France

- Germany

- UK

- APAC

- Japan

- Rest of World (ROW)

- North America

By End-user Insights

The research organization segment is estimated to witness significant growth during the forecast period.

The market is witnessing continuous growth due to the increasing demand for low-temperature storage solutions in various industries. Cryogenic vials are essential for cryogenic freezing and long-term storage of temperature-sensitive samples, such as cells, animal tissues, and proteins. In 2023, the research organization segment registered significant growth, driven by the rapid increase in global research and development activities. Cryogenic vials offer advantages like superior sealing performance, mobility, ease of sample collection, and viral protection. Temperature uniformity is crucial for maintaining sample viability, and automated storage systems with freezing rate control, contamination control, barcode tracking, and temperature monitoring are increasingly being adopted.

Cryogenic vials are also used in cryo-storage tanks, cryopreservation methods, and cryogenic transport. The market is further driven by the demand for advanced insulation materials, vapor shields, vial labeling, and data logging for quality control. The importance of temperature monitoring, freezer maintenance, and vial sealing in maintaining sample integrity is well-established. Cryogenic vials are a critical component of liquid nitrogen storage systems, and their demand is projected to increase due to the need for thermal shock prevention and rack systems. Cryoprotective agents and thawing protocols are also significant factors influencing market growth.

The Research organization segment was valued at USD 58.45 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cryogenic Vials Market Demand is Rising in North America Request Free Sample

The market is witnessing significant growth, with North America leading the charge. This region, home to the US, accounts for a substantial market share due to the increasing demand for cryopreservation of biomaterials in biopharmaceutical research. The growing volumes of cryopreserved samples are driving the need for cryogenic vials in North America. Notably, advanced features such as 1-D and 2-D barcoding and audit traceability offered by prominent companies like Avantor Inc., Brooks Automation Inc., Thermo Fisher Scientific Inc., and STEMCELL Technologies Inc., based in North America, are enabling data sharing and operational efficiency gains. These features are crucial for compliance with regulatory requirements and are contributing to the market's expansion.

According to industry reports, The market is projected to grow at a steady pace, with North America accounting for over 40% of the market share. This growth is attributed to the region's robust research sector and the increasing adoption of advanced technologies in the field of biopreservation.

Customer Landscape of Cryogenic Vials Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Cryogenic Vials Market

Companies are implementing various strategies, such as strategic alliances, cryogenic vials market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AHN Biotechnologie GmbH - The company specializes in manufacturing and supplying a range of cryogenic vials for various applications. Their product portfolio includes Freezing Tubes, Cryo Vial External Thread, and Cryo Coders for both External and Internal Threaded Vials. These high-quality vials cater to the demands of researchers and scientists in various industries.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AHN Biotechnologie GmbH

- Avantor Inc

- Azenta Inc.

- Azer Scientific Inc.

- Biologix Group Ltd.

- Corning Inc.

- Merck KGaA

- Pioneer Impex

- SARSTEDT AG and Co. KG

- Sumitomo Bakelite Co. Ltd.

- Thermo Fisher Scientific Inc.

- Abdos Labtech Private Limited

- DWK Life Sciences GmbH

- Wuxi NEST Biotechnology Co. Ltd.

- Antylia Scientific

- Eppendorf SE

- EZ BioResearch LLC

- LVL Technologies GmbH and Co. KG

- Narang Medical Ltd.

- Simport Scientific Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cryogenic Vials Market

- In August 2024, Thermo Fisher Scientific, a leading life sciences solutions provider, announced the launch of its new line of CryoOne cryogenic vials, designed for long-term storage of biological samples at ultra-low temperatures. These vials offer enhanced durability and improved sealing technology, ensuring sample integrity and reducing the risk of cross-contamination (Thermo Fisher Scientific Press Release, 2024).

- In November 2024, Corning Incorporated, a renowned specialty glass and ceramics manufacturer, entered into a strategic partnership with Cryoport, a leading provider of temperature-controlled logistics solutions for the life sciences industry. This collaboration aimed to develop and commercialize advanced cryogenic shipping solutions, combining Corning's expertise in glass and ceramics with Cryoport's logistics capabilities (Corning Inc. Press Release, 2024).

- In March 2025, Cryovac, a part of Sealed Air Corporation, completed the acquisition of Cryo-Tech, a leading manufacturer of cryogenic storage equipment and vials. This acquisition expanded Cryovac's product portfolio and strengthened its position in the cryogenic storage market (Sealed Air Corporation SEC Filing, 2025).

- In May 2025, the European Medicines Agency (EMA) approved the use of Cryo-Save's new cryopreservation solution for umbilical cord blood and tissue. This approval marked a significant milestone in the advancement of stem cell storage and regenerative medicine applications for cryogenic vials (Cryo-Save Press Release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cryogenic Vials Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

169 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.66% |

|

Market growth 2024-2028 |

USD 73.46 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.08 |

|

Key countries |

US, Germany, UK, France, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Cryogenic Vials Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market encompasses the production and distribution of specialized containers used for the cryogenic preservation of biological samples. These vials are essential in various industries, including biotechnology, pharmaceuticals, and clinical laboratories, where maintaining sample integrity is paramount. One critical aspect of the market is ensuring material compatibility for various samples. Compatibility testing is necessary to prevent sample degradation and ensure optimal cryogenic freezing protocols. The impact of freezing rates on cell viability is another significant consideration, with slower freezing rates often yielding better results. Automated cryogenic vial storage systems are increasingly popular in the market due to their ability to streamline operations and improve compliance. Validation of cryogenic storage procedures is essential to maintain sample integrity and reduce the risk of temperature fluctuations, which can negatively affect sample quality. Cryoprotective agents are commonly used in the cryogenic preservation of stem cells and other sensitive samples. Proper labeling and tracking of cryogenic vials is also crucial for inventory management best practices and regulatory compliance. Designing cryogenic storage containers that minimize thermal shock is essential for maintaining sample integrity. Quality control measures, such as automated sample identification and cryogenic vial sealing techniques, further enhance the reliability of the cryogenic storage process. In clinical laboratories, vapor phase liquid nitrogen storage systems are often used for cryogenic storage due to their ability to maintain consistent temperatures and reduce thermal shock. Implementing cryogenic storage procedures requires careful planning and adherence to transport and shipping protocols to ensure sample integrity during transit. Maintenance and calibration of cryogenic freezers are essential for maintaining optimal performance and reducing the risk of sample loss. Reducing thermal shock in cryogenic vial storage can lead to a 10% increase in sample survival rates, making it a significant business function for organizations relying on cryogenic storage for their operations.

What are the Key Data Covered in this Cryogenic Vials Market Research and Growth Report?

-

What is the expected growth of the Cryogenic Vials Market between 2024 and 2028?

-

USD 73.46 million, at a CAGR of 5.66%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Research organization, Drug manufacturers, Healthcare institutions, and Others), Type (Internally threaded cryogenic vials and Externally threaded cryogenic vials), and Geography (North America, Europe, Asia, and Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing adoption of cryopreservation procedures, Stringent regulations regarding product sterility

-

-

Who are the major players in the Cryogenic Vials Market?

-

AHN Biotechnologie GmbH, Avantor Inc, Azenta Inc., Azer Scientific Inc., Biologix Group Ltd., Corning Inc., Merck KGaA, Pioneer Impex, SARSTEDT AG and Co. KG, Sumitomo Bakelite Co. Ltd., Thermo Fisher Scientific Inc., Abdos Labtech Private Limited, DWK Life Sciences GmbH, Wuxi NEST Biotechnology Co. Ltd., Antylia Scientific, Eppendorf SE, EZ BioResearch LLC, LVL Technologies GmbH and Co. KG, Narang Medical Ltd., and Simport Scientific Inc.

-

We can help! Our analysts can customize this cryogenic vials market research report to meet your requirements.

RIA -

RIA -