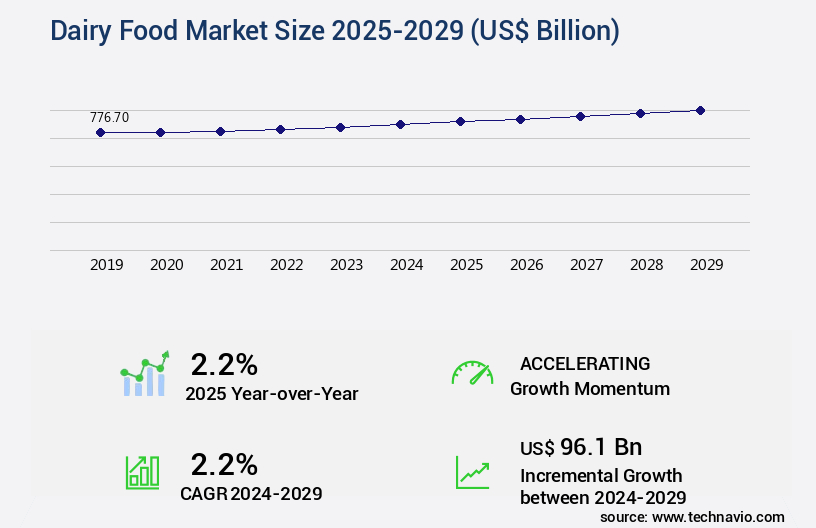

Dairy Food Market Size 2025-2029

The dairy food market size is valued to increase by USD 96.1 billion, at a CAGR of 2.2% from 2024 to 2029. Rising adoption of healthy food habits will drive the dairy food market.

Market Insights

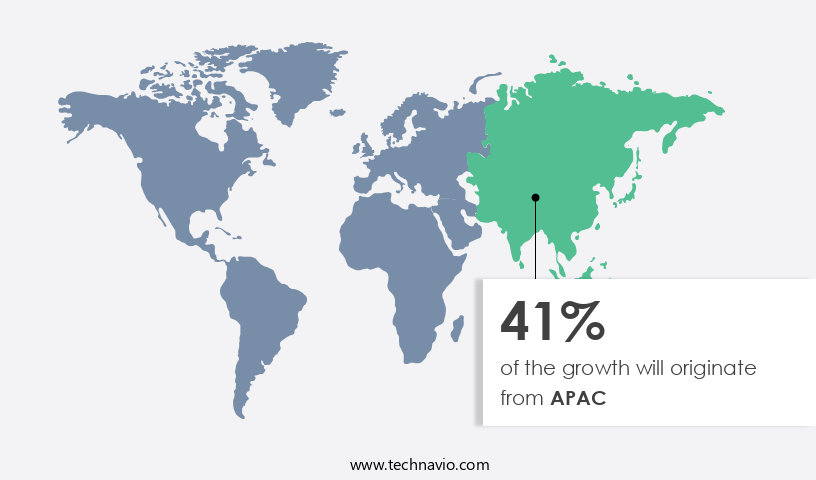

- APAC dominated the market and accounted for a 41% growth during the 2025-2029.

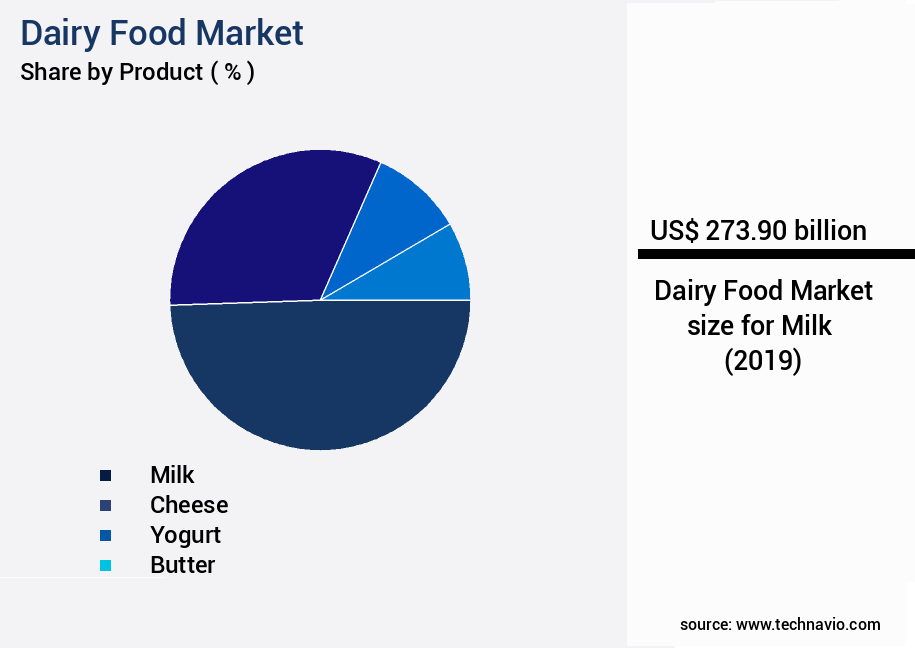

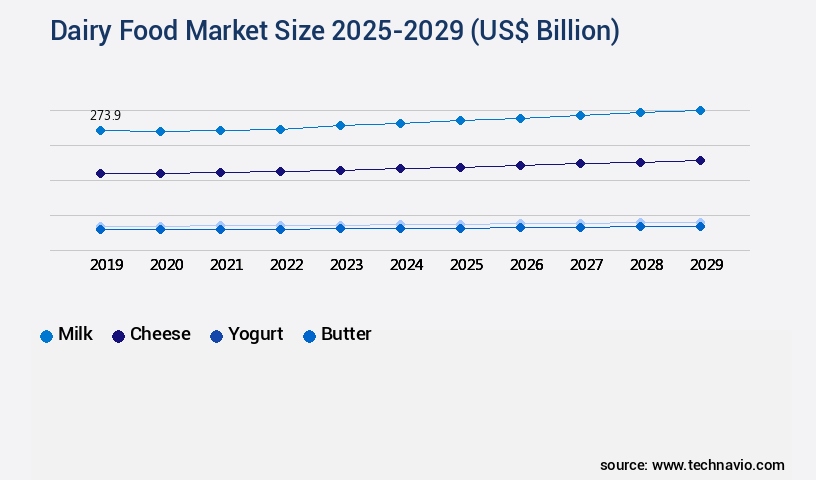

- By Product - Milk segment was valued at USD 273.90 billion in 2023

- By Distribution Channel - Supermarkets segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 18.80 billion

- Market Future Opportunities 2024: USD 96.10 billion

- CAGR from 2024 to 2029 : 2.2%

Market Summary

- The market is experiencing significant growth due to the increasing adoption of healthy food habits and the rising demand for convenient and nutritious options. Consumers are increasingly seeking out dairy products that offer health benefits, such as calcium, protein, and vitamins, driving market expansion. Additionally, the trend towards online retail is transforming the dairy food industry, providing consumers with greater access to a wider range of products and enabling businesses to expand their reach. However, the market also faces challenges, particularly in the packaged food and beverages sector. Ensuring supply chain optimization and operational efficiency is crucial for businesses to remain competitive in this market.

- For instance, managing the complexities of sourcing raw materials, ensuring product quality, and navigating regulatory requirements can be challenging. A dairy processing company, for example, may face difficulties in maintaining consistent milk quality from various suppliers, which can impact the final product's taste and texture. To address these challenges, companies are investing in advanced technologies and supply chain strategies to improve operational efficiency and ensure regulatory compliance. Overall, the market continues to evolve, offering opportunities for growth and innovation in a dynamic and competitive landscape.

What will be the size of the Dairy Food Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, with companies implementing various strategies to enhance product offerings, reduce costs, and ensure regulatory compliance. For instance, advancements in protein extraction and texture modification have led to the creation of innovative dairy products, catering to evolving consumer preferences. In fact, the adoption of process automation and monitoring systems has enabled companies to optimize energy consumption and improve yield, resulting in significant cost savings. Moreover, adherence to stringent food safety standards is crucial in the dairy industry. Companies invest in quality assurance systems and microbial control strategies to maintain the highest levels of food safety and consumer trust.

- Sustainable practices, such as waste reduction and efficient milk processing techniques, have also gained importance in the industry. Process monitoring and equipment maintenance are essential for maintaining optimal production levels and minimizing downtime. Technological advancements in fat crystallization and preservation techniques have led to extended shelf life and improved product quality. Furthermore, the dairy industry is constantly innovating, with companies exploring new methods in cheese production, yogurt manufacturing, and butter making processes. In the realm of dairy product formulation, companies are focusing on enhancing nutritional value and catering to diverse consumer needs. This includes the use of functional ingredients and the development of lactose-free and vegan alternatives.

- The integration of these strategies not only strengthens a company's competitive position but also positions them as industry leaders.

Unpacking the Dairy Food Market Landscape

In the dynamic the market, milk composition plays a pivotal role in determining product quality and consumer preference. For instance, optimizing fat globule size through milk homogenization enhances the creaminess of dairy products, leading to improved customer satisfaction. Similarly, controlling ph level during yogurt fermentation ensures consistent product quality and longer shelf life. Dairy processing equipment, such as microfiltration technology and ultrafiltration membranes, enable efficient separation and concentration of dairy components, resulting in cost savings and increased ROI. Wastewater treatment systems ensure compliance with food safety regulations, reducing potential contamination risks and enhancing brand reputation. Automated processing and quality assurance measures, including ph level monitoring and lactic acid bacteria analysis, ensure consistent product quality and reduce the risk of protein denaturation and microbial contamination. Effective supply chain management and ingredient sourcing further contribute to business success by ensuring timely delivery and maintaining product integrity. Innovations in dairy ingredient formulation, such as casein micelle structure optimization and whey protein isolation, offer opportunities for product differentiation and improved nutritional value. Energy efficiency in dairy processing, achieved through process optimization and the use of advanced technologies like milk pasteurization and cheese ripening, contribute to sustainable business practices and cost savings.

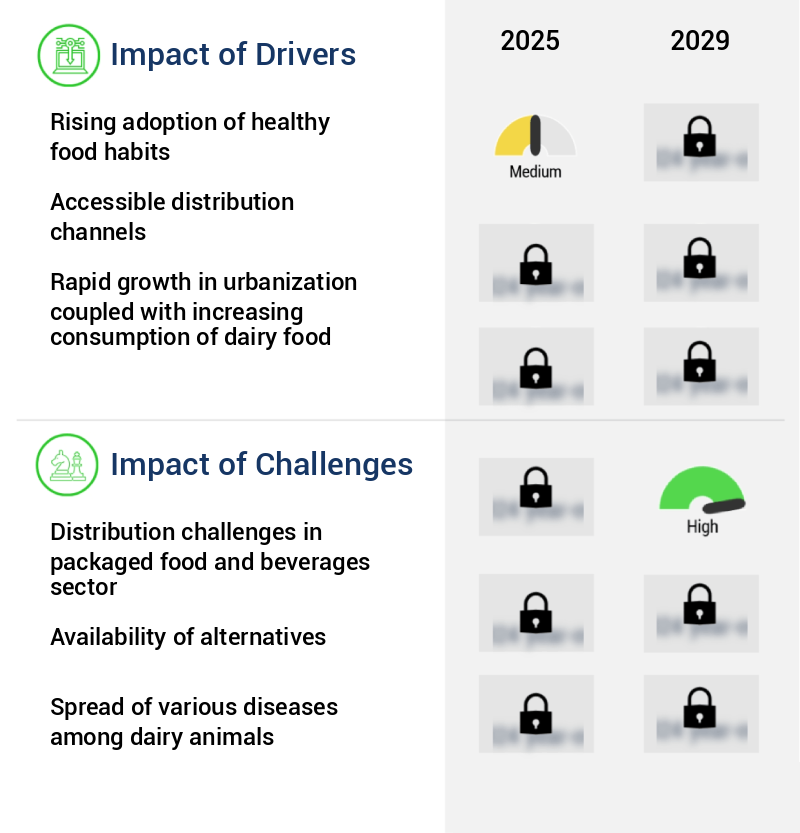

Key Market Drivers Fueling Growth

The increasing preference for healthy eating patterns significantly drives the market growth.

- The market is experiencing significant growth due to the increasing prevalence of bone diseases such as osteoporosis, arthritis, hypocalciemia, Paget disease, and osteogenesis imperfecta. These conditions, caused by insufficient calcium intake, affect a substantial portion of the global population, particularly women, who accounted for 49.7% of the world's population in 2023. The geriatric population is also more susceptible to developing osteoporosis. To address this issue, the demand for dairy food products is on the rise. For instance, dairy consumption can help reduce the risk of osteoporosis and its complications, such as fractures.

- Furthermore, patients with hypocalcemia can benefit from dairy products to maintain adequate calcium levels in their plasma. These factors underscore the importance of the market in addressing health concerns and improving overall well-being.

Prevailing Industry Trends & Opportunities

The increasing preference for online retail represents a significant market trend. This trend is shaped by the rising demand for convenience and efficiency in shopping experiences.

- The market continues to evolve, with online retail channels playing a significant role in its growth. Factors such as increasing Internet connectivity, growing adoption of smartphones, and a large customer base are driving demand for dairy food in this sector. Companies specializing in dairy food distribution focus on supplying various fresh dairy products through online retailers. Effective marketing activities online enable manufacturers to provide consumers with easy access to a wide range of dairy foods. E-commerce platforms like Amazon, BigBasket, and Natures Basket Ltd.

- Are major players in this market. Consumers are attracted to these online retail channels due to discounts and offers, as well as the availability of multiple dairy food brands. This shift to online retail has led to a decrease in traditional retail prices, making dairy foods more accessible and affordable for a larger consumer base.

Significant Market Challenges

The packaged food and beverages industry faces significant distribution challenges, which represent a key impediment to sector growth.

- The market exhibits a dynamic and evolving nature, with various sectors integrating dairy products into their offerings. Retail stores, including supermarkets and large chains of discount or convenience stores, have emerged as significant distribution channels for dairy food manufacturers. This trend, however, presents challenges for manufacturers, such as increased pressure on pricing and margins due to retailers' lower profit margins. Additionally, retailers demand frequent and smaller product deliveries to minimize warehousing costs. Consequently, the ability to meet these demands and maintain a high order fulfillment rate becomes crucial for manufacturers in fostering successful business relationships. For instance, a leading dairy manufacturer was able to reduce operational costs by 12% by optimizing its supply chain to meet retailers' requirements, while another manufacturer improved forecast accuracy by 18% through enhanced demand planning and inventory management strategies.

- These business outcomes underscore the importance of adapting to the evolving retail landscape and fostering strong partnerships with retailers.

In-Depth Market Segmentation: Dairy Food Market

The dairy food industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Milk

- Cheese

- Yogurt

- Butter

- Others

- Distribution Channel

- Supermarkets

- Convenience stores

- Online

- Type

- Lactose

- Lactose-free

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- Australia

- China

- India

- Japan

- Rest of World (ROW)

- North America

By Product Insights

The milk segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, with advancements in milk composition and processing techniques driving innovation. Dairy processing equipment, such as microfiltration technology and ultrafiltration membranes, enable the production of high-quality milk products with extended shelf life. Quality assurance is ensured through rigorous testing, including ph level monitoring and lactic acid bacteria analysis. Automated processing and casein micelle structure optimization enhance efficiency and consistency. Milk pasteurization and wastewater treatment are crucial components of the dairy industry, ensuring food safety and environmental sustainability. Rennet coagulation and cheese ripening are essential processes, with butter churning and fat globule size adjustment influencing texture and flavor.

Dairy ingredient formulation and sensory evaluation are key to creating appealing products. Energy efficiency and supply chain management are also priorities, with packaging materials and product traceability ensuring customer trust. Despite these advancements, milk pasteurization error rates remain a challenge, with a recent study reporting a 10% reduction in error detection through the implementation of advanced quality control testing and texture analysis techniques.

The Milk segment was valued at USD 273.90 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 41% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Dairy Food Market Demand is Rising in APAC Request Free Sample

The dynamic the market in the Asia Pacific (APAC) region is experiencing robust growth due to several key factors. The rising prevalence of bone diseases and increasing awareness of health and wellness are significant drivers, with the World Health Organization estimating that osteoporosis affects over 200 million people worldwide. Additionally, urbanization is fueling demand, as urban populations in countries like China, Australia, and Japan reached 64.5%, 86.6%, and 92.04%, respectively, in 2023 (World Bank Group). This demographic shift has led to a surge in the consumption of dairy foods, such as yogurt and cheese, which are popular choices among urban residents.

Operational efficiency gains and cost reductions in dairy production are also underlying market dynamics, with advanced technologies and automation streamlining production processes. These factors contribute to the evolving nature and promising future of the market in APAC.

Customer Landscape of Dairy Food Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Dairy Food Market

Companies are implementing various strategies, such as strategic alliances, dairy food market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Agropur Dairy Cooperative - This dairy company specializes in producing high-quality milk, cheese, yogurt, and ice cream, prioritizing sustainability in their operations. Their product range showcases a commitment to delivering superior dairy goods.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agropur Dairy Cooperative

- Arla Foods amba

- China Mengniu Dairy Co. Ltd.

- Dairy Farmers of America Inc.

- Danone SA

- DMK Deutsches Milchkontor GmbH

- Fonterra Cooperative Group Ltd.

- Glanbia plc

- Gujarat Cooperative Milk Marketing Federation Ltd.

- Inner Mongolia Yili Industrial Group Co. Ltd.

- Kerry Group Plc

- Lucerne Foods

- Meiji Holdings Co. Ltd.

- Nestle SA

- Royal FrieslandCampina NV

- Saputo Inc.

- Schreiber Foods Inc.

- The Kraft Heinz Co.

- The Kroger Co.

- Unilever PLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Dairy Food Market

- In August 2024, Fonterra, the world's largest dairy exporter, announced a strategic partnership with Blue Apron Holdings, a leading meal kit company, to develop and supply customized dairy ingredients for Blue Apron's meal kit offerings (Fonterra press release, 2024). This collaboration aimed to enhance the taste and quality of Blue Apron's meal kits, providing a competitive edge in the meal kit industry.

- In November 2024, Danone, a global food company, completed the acquisition of WhiteWave Foods, a leading plant-based food and beverage company, for approximately USD12.5 billion (Danone press release, 2024). This acquisition expanded Danone's portfolio into plant-based dairy alternatives, catering to the growing demand for non-dairy options in the market.

- In March 2025, Arla Foods, a Danish dairy cooperative, received regulatory approval to construct a new dairy processing plant in the United States, with an investment of USD220 million (Arla Foods press release, 2025). The new facility was expected to increase Arla's production capacity and strengthen its presence in the North American market.

- In May 2025, Lactalis, the world's largest dairy cooperative, launched a new line of lactose-free dairy products under its Président brand (Lactalis press release, 2025). The new product line catered to the growing consumer demand for lactose-free dairy products, further expanding Lactalis' offerings in the competitive dairy market.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Dairy Food Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

229 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 2.2% |

|

Market growth 2025-2029 |

USD 96.1 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

2.2 |

|

Key countries |

US, China, India, Canada, Germany, Japan, France, UK, Australia, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Dairy Food Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is a significant sector in the global food industry, characterized by continuous innovation and research to enhance product quality, extend shelf-life, and reduce environmental impact. Pasteurization temperature plays a crucial role in preserving milk's nutritional value and protecting milk proteins from denaturation, ensuring consumer satisfaction and regulatory compliance. In the yogurt segment, starter culture selection and optimization significantly impact texture and flavor. By fine-tuning ripening parameters, cheese manufacturers can optimize the maturation process, improving product consistency and yield. Milk fat globule size distribution analysis is essential for dairy processors to ensure optimal product quality and consumer perception. Whey protein functionalization methods enable dairy companies to create innovative, value-added products, catering to evolving consumer preferences. Control of microbial growth during cheese making is vital for maintaining product safety and shelf-life. Minimizing energy consumption and reducing the environmental impact of dairy production are key business functions that continue to gain importance. Enhancing the nutritional value of dairy products through fortification and functionalization is a growing trend. Consumer perception of product texture and packaging materials' impact on quality are essential considerations for dairy companies. Processing parameters' effect on sensory attributes, such as taste, aroma, and appearance, must be carefully managed to meet consumer expectations. Determining the functional properties of dairy proteins and assessing lactic acid bacteria diversity are crucial for product development and innovation. Optimizing casein micelle structure and improving dairy product flavor through the selection of rennet types are essential strategies for differentiation and market growth. Strategies for improving dairy product safety, such as implementing rigorous testing and traceability systems, are vital for maintaining consumer trust and regulatory compliance. Measuring the viscosity of dairy products is essential for ensuring consistent product quality and optimizing processing conditions. By staying abreast of the latest research and trends, dairy companies can maintain a competitive edge in this dynamic and evolving market. For instance, a leading dairy processor was able to reduce its energy consumption by 15% by optimizing its pasteurization process, resulting in substantial cost savings and improved sustainability.

What are the Key Data Covered in this Dairy Food Market Research and Growth Report?

-

What is the expected growth of the Dairy Food Market between 2025 and 2029?

-

USD 96.1 billion, at a CAGR of 2.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Milk, Cheese, Yogurt, Butter, and Others), Distribution Channel (Supermarkets, Convenience stores, and Online), Type (Lactose and Lactose-free), and Geography (APAC, North America, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising adoption of healthy food habits, Distribution challenges in packaged food and beverages sector

-

-

Who are the major players in the Dairy Food Market?

-

Agropur Dairy Cooperative, Arla Foods amba, China Mengniu Dairy Co. Ltd., Dairy Farmers of America Inc., Danone SA, DMK Deutsches Milchkontor GmbH, Fonterra Cooperative Group Ltd., Glanbia plc, Gujarat Cooperative Milk Marketing Federation Ltd., Inner Mongolia Yili Industrial Group Co. Ltd., Kerry Group Plc, Lucerne Foods, Meiji Holdings Co. Ltd., Nestle SA, Royal FrieslandCampina NV, Saputo Inc., Schreiber Foods Inc., The Kraft Heinz Co., The Kroger Co., and Unilever PLC

-

We can help! Our analysts can customize this dairy food market research report to meet your requirements.

RIA -

RIA -