Organic Dairy Products Market Size 2024-2028

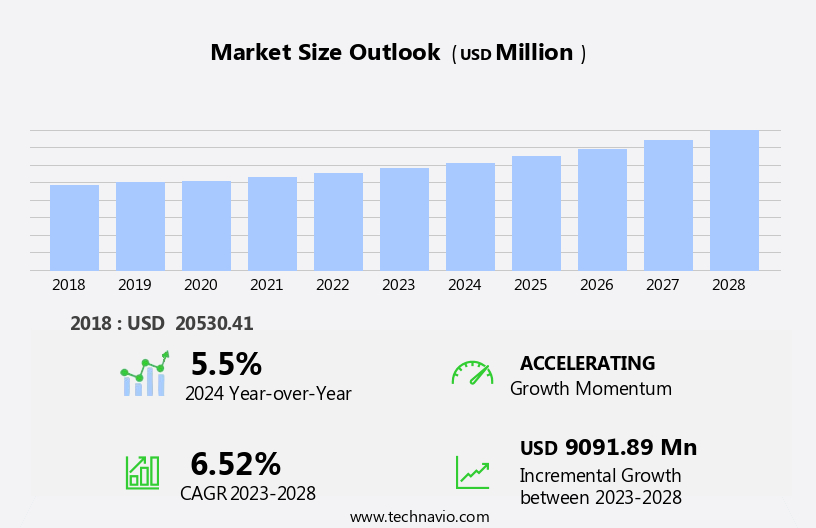

The organic dairy products market size is forecast to increase by USD 9.09 billion, at a CAGR of 6.52% between 2023 and 2028.

- The market is driven by the increasing awareness of the benefits associated with consuming organic dairy products. Consumers are increasingly seeking healthier and more natural food options, leading to a surge in demand for organic dairy products. Additionally, the growing use of clean and transparent packaging is a significant trend in the market, as consumers prioritize product safety and sustainability. However, the market faces challenges due to fluctuations in the supply of raw materials for organic dairy farming. These challenges include unpredictable weather patterns, which can impact crop yields and pasture growth, and the high cost of organic feed and fertilizers.

- To capitalize on market opportunities and navigate these challenges effectively, companies must focus on sustainable farming practices, efficient supply chain management, and innovative product development. By addressing these factors, they can meet the growing demand for organic dairy products and differentiate themselves in a competitive market.

What will be the Size of the Organic Dairy Products Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, with dynamic market activities shaping its landscape. Whey protein recovery and yogurt production are key processes undergoing constant advancements, driven by consumer preferences for nutritious and functional food options. Milk fat percentage and dairy farming practices, such as grass-fed and pasture-raised, are also influencing production methods. Butter manufacturing and ruminant nutrition are areas of focus, as producers seek to optimize milk production efficiency while adhering to animal welfare standards. Dairy traceability systems and marketing strategies are essential components, ensuring transparency and consumer trust. Bacterial culture identification and food safety regulations play a crucial role in maintaining product quality and safety.

Dairy product packaging and cheesemaking techniques are continually evolving to extend shelf life and enhance flavor profiles. Milk composition analysis, including milk protein content and somatic cell count, are essential for ensuring consistent product quality. Pasteurization techniques and sustainable dairy practices are also critical aspects, as producers aim to minimize waste and reduce environmental impact. Consumer preference trends and quality control measures are driving innovation in the organic dairy sector, with an increasing emphasis on farm-to-table sourcing and value-added products. Ultra-high temperature processing and forage quality assessment are among the areas of research to address evolving consumer demands and market dynamics.

How is this Organic Dairy Products Industry segmented?

The organic dairy products industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Organic milk

- Organic yogurt

- Organic cheese

- Others

- Distribution Channel

- Offline

- Online

- Source

- Cow Milk

- Buffalo Milk

- Other Animal Milk

- Application

- Children

- Adults

- Aged

- Packaging Type

- Pouches

- Cartons

- Bottles

- Cups

- Tubs

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

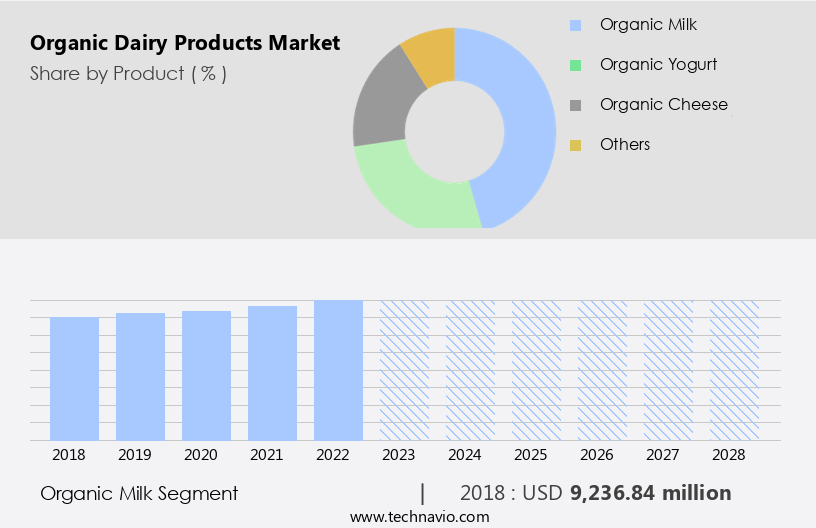

By Product Insights

The organic milk segment is estimated to witness significant growth during the forecast period.

The organic dairy market in the US is witnessing significant growth due to increasing consumer preference for sustainable dairy farming and production methods. Organic dairy farming involves raising livestock on organic feed, free from synthetic hormones and antibiotics, resulting in milk that is free from these substances. The environmentally-friendly organic farming practices, which exclude the use of chemicals and pesticides, further add to the appeal. Dairy processing technology plays a crucial role in maintaining the quality of organic dairy products. Homogenization methods ensure consistent milk fat percentage and milk protein content, while pasteurization techniques extend shelf life. Cheesemaking techniques and yogurt production processes are also essential to preserve the natural taste and texture of these products.

Food safety regulations are stringently enforced to ensure the highest standards of milk production efficiency and bacterial culture identification. Dairy product packaging is designed to maintain the quality and freshness of the products, while dairy marketing strategies focus on promoting the health benefits and sustainability of organic dairy. Animal welfare standards are a priority in organic dairy farming, with grass-fed and pasture-raised dairy cows being raised in humane conditions. Forage quality assessment and dairy herd management practices contribute to optimal milk production and efficient dairy waste management. Sustainable dairy practices, such as ruminant nutrition and dairy traceability systems, are integral to the organic dairy industry.

Consumer preference trends favor value-added dairy products, including whey protein recovery and butter manufacturing. Quality control measures, such as milk composition analysis and somatic cell count monitoring, ensure the purity and consistency of organic dairy products. Ultra-high temperature processing and farm-to-table dairy initiatives are innovative approaches to meet the growing demand for organic dairy products. Sustainability and transparency are key drivers in the organic dairy market, with consumers seeking assurance that their dairy products are produced using ethical and eco-friendly methods.

The Organic milk segment was valued at USD 9.24 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

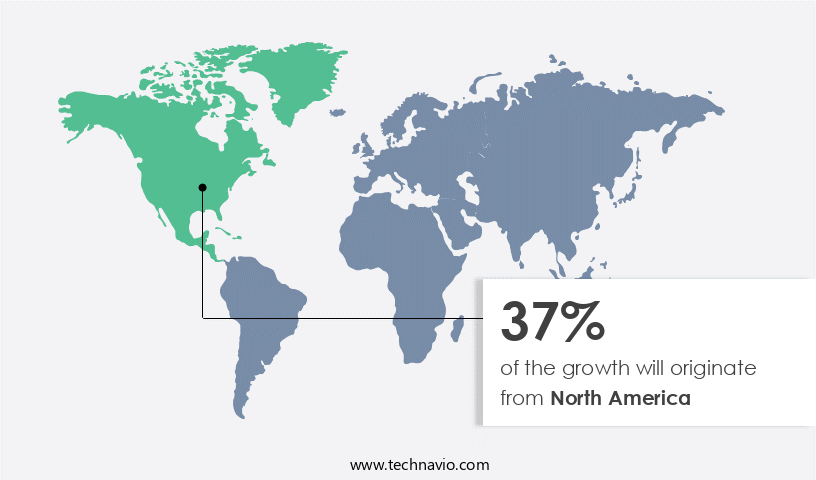

North America is estimated to contribute 37% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is experiencing growth due to the rising consumer preference for healthier and more natural food choices. With the absence of synthetic hormones, antibiotics, and pesticides in organic dairy products, they are perceived as a healthier alternative to conventional dairy offerings. The trend toward wellness and natural living has significantly driven demand for these products. Local dairy sourcing and farm-to-table practices are also gaining popularity, contributing to the market's expansion. Dairy processing technology plays a crucial role in maintaining the quality and consistency of organic dairy products. Homogenization methods ensure uniform milk composition, while food safety regulations safeguard consumer health.

Milk production efficiency is essential for maintaining profitability, and bacterial culture identification and milk composition analysis help ensure product purity and quality. Cheesemaking techniques, whey protein recovery, and yogurt production are key areas of innovation in the organic dairy industry. Milk fat percentage, grass-fed and pasture-raised dairy, and butter manufacturing cater to various consumer preferences. Ruminant nutrition, dairy herd management, and dairy waste management are essential aspects of sustainable dairy practices. Consumer trends favor value-added dairy products, such as flavored milk, organic butter, and organic cheese. Quality control measures, including pasteurization techniques and shelf life extension, are essential to maintain product integrity.

Dairy traceability systems and animal welfare standards are also critical factors in the market. Ultra-high temperature processing and somatic cell count are important considerations in organic dairy production. Forage quality assessment and mastitis detection methods help maintain herd health and productivity. Sustainable dairy practices, including the use of renewable energy and reduction of greenhouse gas emissions, are becoming increasingly important to consumers and stakeholders alike. In conclusion, the market in North America is growing due to consumer demand for healthier, more natural food choices. Innovation in processing technology, sustainable practices, and value-added products are key drivers of market growth.

Regulatory compliance, animal welfare, and sustainable production are essential considerations for market success.

Market Dynamics

The Organic Dairy Products Market is flourishing as demand for organic dairy products like organic milk, organic cheese, and organic yogurt grows among organic dairy for health-conscious consumers. Products such as organic dairy lactose-free milk benefits those with organic dairy for lactose intolerance, while organic dairy clean label and organic dairy probiotic products appeal to organic dairy for clean eating enthusiasts. Organic dairy sustainable production and organic dairy for sustainable farming align with organic dairy for ethical consumers, supported by organic dairy eco-friendly packaging and organic dairy processing advancements. Best organic dairy products for health, including organic dairy high-protein products and organic dairy for infant nutrition, drive market growth, catering to diverse dietary and ethical needs.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Organic Dairy Products Industry?

- The significant rise in consumer awareness regarding the health benefits associated with organic dairy products serves as the primary catalyst for market growth.

- Organic dairy farming has gained significant traction in the global market due to increasing consumer preference for healthier food options. The demand for organic dairy products is on the rise as consumers become more conscious of the potential health risks associated with conventional dairy farming practices. Organic dairy farming ensures the absence of synthetic hormones, pesticides, and antibiotics in milk production. Advancements in dairy processing technology have facilitated the production of organic dairy products with improved milk production efficiency and food safety regulations. Bacterial culture identification and homogenization methods ensure the preservation of nutrients and the elimination of harmful bacteria, respectively.

- Local dairy sourcing is another trend that has gained popularity in the organic dairy market. Consumers prefer locally sourced organic dairy products due to their freshness and the reduced carbon footprint. Dairy product packaging plays a crucial role in maintaining the quality and freshness of organic dairy products. Cheese making techniques are being refined to cater to the growing demand for organic cheese. The use of traditional methods and natural ingredients is a key focus area for producers to differentiate their products and cater to the evolving consumer preferences. Overall, the organic dairy market is expected to continue its growth trajectory due to increasing consumer awareness and the availability of advanced dairy processing technology.

What are the market trends shaping the Organic Dairy Products Industry?

- The increasing preference for clean and transparent packaging is a notable trend in the current market. This shift towards transparency aims to provide consumers with a clearer view of the product and its contents.

- Organic dairy products have gained significant traction in the market due to increasing consumer awareness and preference for healthier and more sustainable food options. The production of organic dairy items, such as yogurt and whey protein recovery, involves the use of grass-fed dairy cows raised in pastures. This farming practice ensures better ruminant nutrition and results in milk with a higher milk fat percentage, contributing to the superior taste and quality of organic dairy products. Transparency is a crucial factor in the organic dairy market. Dairy traceability systems are essential to ensure the authenticity and origin of organic dairy products.

- Consumers are more likely to choose products with clear and transparent packaging, as it provides a view of the product inside and allows them to check the quality and condition of the items. Additionally, eco-friendly, recyclable, or biodegradable packaging aligns with the broader trend of sustainability and appeals to environmentally-conscious consumers. Butter manufacturing is another segment of the organic dairy market that is growing in popularity. The production process for organic butter involves using milk from cows that have not been treated with antibiotics or growth hormones, ensuring a pure and natural product. The organic dairy industry continues to innovate and adapt to consumer demands, focusing on delivering high-quality, authentic, and sustainable products.

What challenges does the Organic Dairy Products Industry face during its growth?

- The organic dairy industry faces significant challenges due to the volatile supply of raw materials for production, which can negatively impact industry growth.

- The market experiences challenges due to the limited supply of organic raw materials, specifically organic milk. This scarcity is driving up demand for alternative organic dairy options, such as organic cane sugar, fruits, and other dairy-free products. The production of organic dairy items, including yogurts and ice creams, relies heavily on the availability of organic milk. As a result, inconsistent availability of these raw materials can significantly impact market growth. Animal welfare standards, forage quality assessment, and dairy herd management are crucial factors in organic milk production. Organic farming practices prioritize the well-being of the animals and the quality of the forage they consume.

- Dairy waste management is also essential to maintain the organic certification. Consumer preference trends lean towards organic dairy products due to their perceived health benefits and ethical production methods. Quality control measures and pasteurization techniques are employed to ensure the highest standards in the production process. Shelf life extension is another consideration for organic dairy manufacturers to maintain product freshness and meet consumer expectations. In conclusion, the market is subject to the availability of organic raw materials, primarily organic milk. Meeting the increasing demand for organic dairy items requires a focus on animal welfare, forage quality assessment, dairy herd management, and waste management.

- Consumer preference trends, quality control measures, and pasteurization techniques are essential in maintaining the market's growth and meeting the demands of health-conscious consumers.

Exclusive Customer Landscape

The organic dairy products market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the organic dairy products market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, organic dairy products market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Agropur Dairy Cooperative - This subsidiary of the company specializes in providing a range of organic dairy offerings through Whole Foods Market. The company's commitment to organic products aligns with consumer demand for healthier, sustainable food choices. Whole Foods Market's dairy selection caters to various dietary preferences and supports local farmers, contributing to the company's reputation as a leader in the natural and organic food industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agropur Dairy Cooperative

- Amazon.com Inc.

- Arla Foods amba

- Dairy Farmers of America Inc.

- DANA Dairy Group Ltd.

- Danone SA

- Fonterra Cooperative Group Ltd.

- General Mills Inc.

- Gujarat Cooperative Milk Marketing Federation Ltd.

- Land O Lakes Inc.

- Meiji Holdings Co. Ltd.

- MVM Pack Holding AG

- Nestle SA

- Royal FrieslandCampina NV

- Saputo Inc.

- Savencia SA

- Schreiber Foods Inc.

- Sodiaal

- The Kroger Co.

- Organic Valley

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Organic Dairy Products Market

- In January 2024, Danone, a leading organic dairy producer, announced the launch of a new line of organic plant-based milk alternatives, expanding its product portfolio beyond traditional organic dairy offerings (Danone Press Release, 2024).

- In March 2024, Lactalis, the world's largest dairy cooperative, entered into a strategic partnership with Organic Valley, the largest organic cooperative in the United States, to distribute Organic Valley's products in Europe (Organic Valley Press Release, 2024).

- In April 2025, Horizon Organic, a leading organic dairy brand in the US, raised USD150 million in a funding round led by BlackRock and Fidelity Investments to expand its production capacity and accelerate its growth (Horizon Organic Press Release, 2025).

- In May 2025, the European Commission approved the merger of two major organic dairy players, Arla Foods and Lactalis Organic, creating a larger entity to better compete in the global organic dairy market (European Commission Press Release, 2025).

Research Analyst Overview

- The market is experiencing dynamic shifts as producers focus on reducing methane emissions and carbon footprints through natural dairy ingredients and improved feed efficiency ratios. Environmental sustainability is a key driver, with manure management strategies and soil health improvement initiatives gaining traction. Milk yield improvement and dairy product innovation are also significant trends, as precision farming, genetic selection, and antibiotic usage reduction enhance herd health and profitability. Dairy business operations are increasingly adopting renewable energy sources and water usage efficiency measures.

- Consumer demand for hormone-free dairy, probiotic and functional products, and transparent labeling is shaping the market. Dairy industry regulations continue to evolve, influencing pricing strategies and sourcing of dairy ingredients. Land management practices and dairy herd health remain critical factors in ensuring long-term profitability and market competitiveness.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Organic Dairy Products Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

172 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.52% |

|

Market growth 2024-2028 |

USD 9091.89 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.5 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Organic Dairy Products Market Research and Growth Report?

- CAGR of the Organic Dairy Products industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the organic dairy products market growth of industry companies

We can help! Our analysts can customize this organic dairy products market research report to meet your requirements.

RIA -

RIA -