Data Center Managed Services Market Size 2024-2028

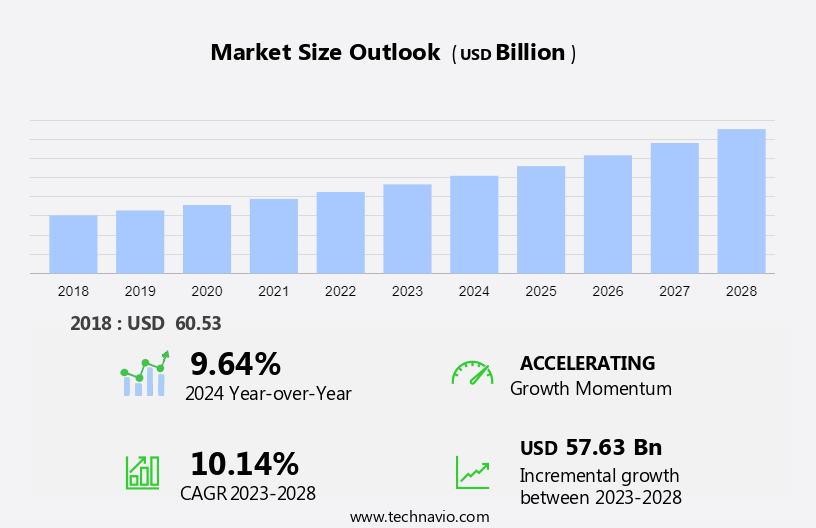

The data center managed services market size is forecast to increase by USD 57.63 billion at a CAGR of 10.14% between 2023 and 2028.

- The market is experiencing significant growth due to increasing demands for advanced computing capabilities and data storage solutions. With budgetary limits driving organizations to outsource IT infrastructure management, there is a rising need for managed services that can effectively manage computing machines, hardware equipment, IT systems, servers, data storage drives, and network equipment. The trend towards edge computing is also expanding the market, as businesses seek to process data closer to the source for faster response times. However, the integration of these services into existing data centers presents complex challenges, requiring expertise in both IT infrastructure and managed services. This market analysis report delves into these growth factors and the complexities of integrating data center-managed services, providing valuable insights for businesses looking to optimize their IT infrastructure.

What will the size of the market be during the forecast period?

- The market represents a significant segment of the IT infrastructure landscape, providing businesses with essential solutions for maintaining and optimizing their IT infrastructure. This market encompasses a range of offerings, including hardware services, network services, backup maintenance, and fault tolerance solutions, among others. A reliable third-party managed service platform plays a crucial role in ensuring the upkeep and maintenance of an organization's IT infrastructure. By outsourcing these tasks, businesses can focus on their core competencies while ensuring their IT infrastructure remains reliable and efficient. Cloud infrastructure has become a norm in today's business environment, and data center managed services have evolved to meet the demands of this technology.

- Furthermore, managed service providers offer expertise in managing complex IT networks, allowing businesses to leverage sophisticated technology without the need for extensive in-house IT resources. IT infrastructure is a foundational element of any growing business, and the need for reliable and efficient data center solutions is paramount. Managed services offer businesses the flexibility to scale their infrastructure as needed, without the logistical limits of managing hardware and software in-house. Network services are a critical component of data center managed services. External networks must be secure and reliable to ensure business continuity. Managed service providers offer solutions for upgrading and patching operating systems, disaster planning, and backup maintenance to mitigate potential risks and minimize downtime.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Retail

- Energy

- BFSI

- Healthcare

- Others

- Deployment

- Cloud

- On-premises

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- South America

- Middle East and Africa

- North America

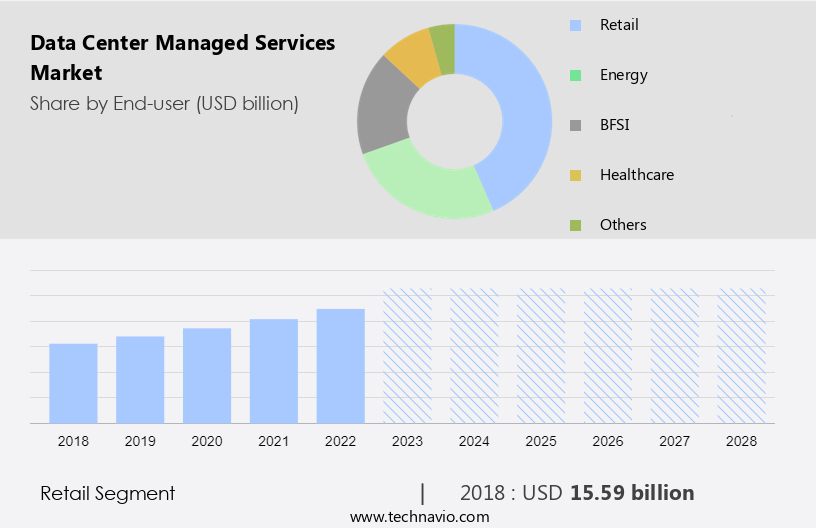

By End-user Insights

- The retail segment is estimated to witness significant growth during the forecast period.

The market caters to the management of digital data and computing equipment for various businesses, including those that run web applications and internal applications. This market is witnessing significant growth due to the increasing demand for efficient and reliable IT infrastructure management services. Customers across multiple industries, such as human resources and accounting, are turning to managed services to streamline their operations and focus on their core competencies. Managed services providers offer a range of solutions, including monitoring, maintenance, and security, ensuring that businesses can effectively manage their IT infrastructure and mitigate potential risks.

The integration of advanced technologies, such as artificial intelligence and machine learning, further enhances the value proposition of these services. The market is expected to continue its expansion as more businesses recognize the benefits of outsourcing their IT management needs.

Get a glance at the market report of share of various segments Request Free Sample

The retail segment was valued at USD 15.59 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

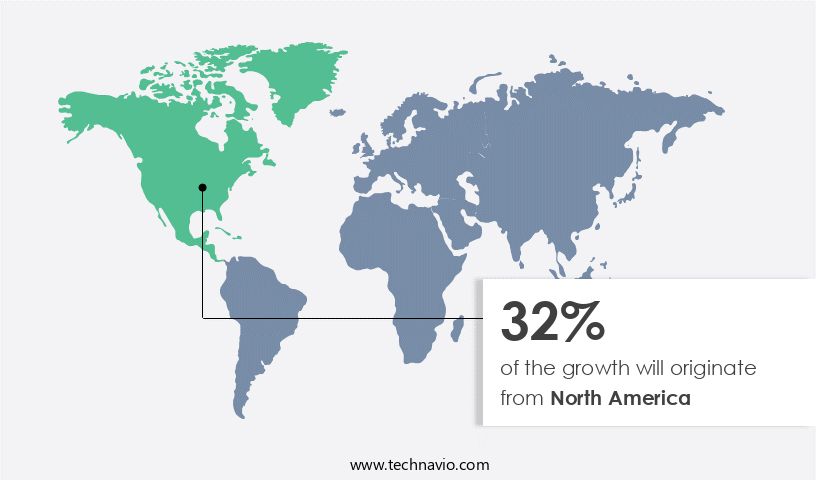

- North America is estimated to contribute 32% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

In the United States, the expanding business landscape is leading to an increased reliance on sophisticated technology and reliable third-party data center managed services to support IT infrastructure needs. The norm for IT networks is shifting towards cloud infrastructure, as more companies invest in advanced technology solutions to streamline operations and improve efficiency. The rise in data traffic from businesses and individual consumers necessitates the expansion of data centers and servers, making data center managed services an essential component of IT infrastructure. Industries across North America are embracing automation technologies to boost productivity and minimize errors, thereby driving the implementation of smart factory initiatives.

By partnering with experienced data center managed service providers, businesses can ensure their IT infrastructure remains efficient, secure, and scalable, enabling them to focus on their core competencies and drive growth.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Data Center Managed Services Market?

Growing data storage and processing needs is the key driver of the market.

- In today's digital economy, businesses require dependable and expandable solutions for their storage and processing infrastructure due to escalating data requirements. Key drivers behind this trend include digital transformation, the proliferation of data generation, and the emergence of data analytics. Across numerous industries such as healthcare, manufacturing, energy and utilities, transportation and logistics, banking, and others, organizations are embracing digital initiatives to remain competitive. The integration of advanced technologies like cloud computing, the Internet of Things (IoT), big data analytics, artificial intelligence (AI), and machine learning (ML) in these industries generates vast amounts of data that necessitate storage, processing, and analysis.

Consequently, the demand for data center-managed services is on the rise. These services offer administrative control, upkeep and maintenance, hardware services, and network services, among others, through a managed service platform. Third-party hosting providers offer these services, enabling businesses to focus on their core competencies while ensuring the optimal performance and security of their data.

What are the market trends shaping the Data Center Managed Services Market?

Expansion in edge computing is the upcoming trend in the market.

- The market is experiencing significant growth due to the increasing adoption of edge computing. Edge computing is a novel approach to computing that brings computation and data storage closer to the user, enabling industries such as telecommunications, healthcare, transport, and logistics to process data locally or in nearby data centers rather than relying solely on centralized cloud servers. This trend is driven by budgetary limits and the need for faster response times.

- As edge computing infrastructure is deployed closer to the point of data generation, the demand for edge data centers to support these distributed computing environments is increasing. Hardware equipment including Computing machines, Servers, Data storage drives, and Network equipment are essential components of these edge data centers. IT systems are being upgraded to accommodate this shift towards edge computing, making the market for data center managed services a promising one for providers.

What challenges does Data Center Managed Services Market face during its growth?

Complexities in the integration of data center-managed services is a key challenge affecting the market growth.

- Data center managed services play a crucial role in ensuring fault tolerance and disaster planning for businesses. However, integrating these services with existing IT environments can pose challenges due to legacy systems, heterogeneous infrastructure, and customization requirements. Outdated hardware, software, and protocols can create compatibility issues with modern technologies and standards. To facilitate communication and data exchange between disparate components, custom development or middleware solutions may be necessary. In a heterogeneous environment, integrating diverse systems, applications, and platforms requires complex processes to develop custom integrations, middleware, or connectors. Each organization's unique business processes, workflows, and requirements necessitate customization of managed services.

- Upgrading and patching operating systems and server installations are essential to maintain security and performance. Off-site maintenance is another critical aspect of managed services, which can help organizations overcome logistical limits and ensure business continuity. By addressing these challenges, businesses can effectively leverage data center managed services to enhance their IT infrastructure and improve overall operational efficiency.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market. The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture Plc

- Atos SE

- Capgemini Service SAS

- Cisco Systems Inc.

- Cognizant Technology Solutions Corp.

- Dell Technologies Inc.

- DXC Technology Co.

- Fujitsu Ltd.

- HCL Technologies Ltd.

- Hewlett Packard Enterprise Co.

- Huawei Technologies Co. Ltd.

- Infosys Ltd.

- International Business Machines Corp.

- Lumen Technologies Inc.

- Microsoft Corp.

- NTT DATA Corp.

- Tata Consultancy Services Ltd.

- Telefonaktiebolaget LM Ericsson

- Unisys Corp.

- Verizon Communications Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is witnessing significant growth as more businesses look to outsource their IT infrastructure needs to reliable third-party hosting providers. With the increasing sophistication of technology and the norms for IT infrastructure becoming more stringent, businesses are turning to managed service platforms for cost-effective management of their computing infrastructure. These third-party data centers offer a range of services including hardware and network services, backup maintenance, upkeep and maintenance, and fault tolerance. They provide customers with administrative control over their IT systems, servers, data storage drives, network equipment, and web applications. The managed services market caters to both internal applications and customer-facing web applications.

Furthermore, the use of backup power supplies, data replication, and disaster planning ensures business continuity during power outages and other disasters. Temperature-controlled facilities and strong security measures are essential elements of a reliable managed services platform. The data center store offers upgrading and patching of operating systems, server installations, and off-site maintenance. Logistical and budgetary limits often make it challenging for businesses to maintain their own IT infrastructure, making third-party hosting a cost-effective solution. Computing machines, hardware equipment, and computer hardware such as mainframes and IT complexity continue to drive the demand for managed services. Data laws and security concerns add to the importance of a managed services provider's ability to ensure fault tolerance and disaster planning.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

175 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.14% |

|

Market Growth 2024-2028 |

USD 57.63 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

9.64 |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -