Data Warehouse As A Service Market Size 2024-2028

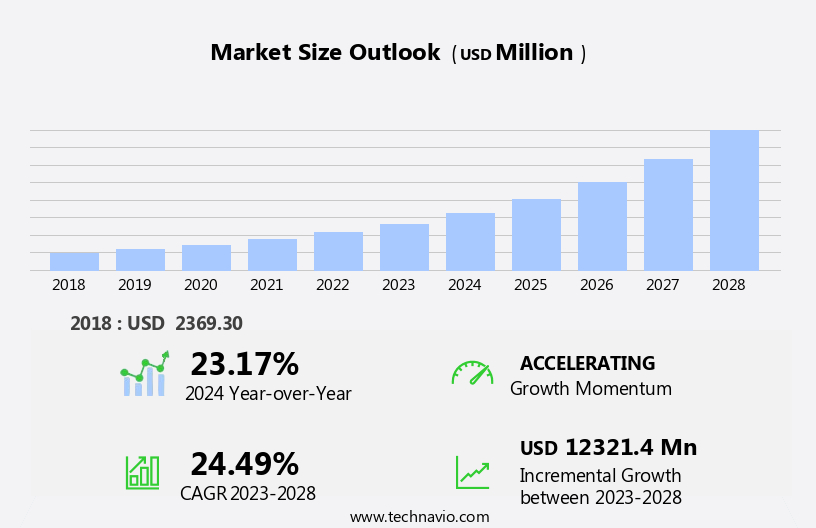

The data warehouse as a service market size is forecast to increase by USD 12.32 billion at a CAGR of 24.49% between 2023 and 2028.

- The market is experiencing significant growth due to several key trends. One major trend is the shift from traditional on-premises data warehouses to cloud-based DWaaS solutions. Advanced storage technologies, such as columnar databases, in-memory storage, and cloud storage, are also driving market growth.

- However, data privacy and security risks are challenges that need to be addressed, as organizations move their data to the cloud. DWaaS providers are responding by implementing data security and data encryption techniques to mitigate these risks. Overall, the DWaaS market is poised for continued growth as more businesses seek to leverage the benefits of cloud-based data warehousing solutions.

What will be the Size of the Data Warehouse As A Service Market During the Forecast Period?

- The market represents a significant shift in how businesses manage their data environments. DWaaS offers flexibility and scalability, enabling organizations to focus on their core competencies while leveraging cloud computing for their data warehousing needs. This market is driven by the increasing demand for Business Intelligence (BI) that can handle large data volumes and provide advanced analytics capabilities.

- Technological developments in cloud computing, software, computing, and storage have made DWaaS a viable alternative to traditional on-premises data warehouses. However, the adoption of DWaaS is not without challenges. Security issues and integration complexities are key concerns for businesses considering a move to the cloud.

- Restricted customization is another challenge, as some organizations require specific configurations for their data warehouses. Despite these challenges, the benefits of DWaaS, such as reduced IT infrastructure complexity and improved data accessibility, continue to drive market growth. The DWaaS market is expected to expand as more businesses seek to harness the power of their data for enterprise management, visualization, and data analytics.

How is this Data Warehouse As A Service Industry segmented and which is the largest segment?

The DWaaS industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- BFSI

- Government

- Healthcare

- E-commerce and retail

- Others

- Type

- Enterprise DWaaS

- Operational data storage

- Geography

- North America

- US

- Europe

- Germany

- France

- APAC

- China

- Japan

- Middle East and Africa

- South America

- North America

By End-user Insights

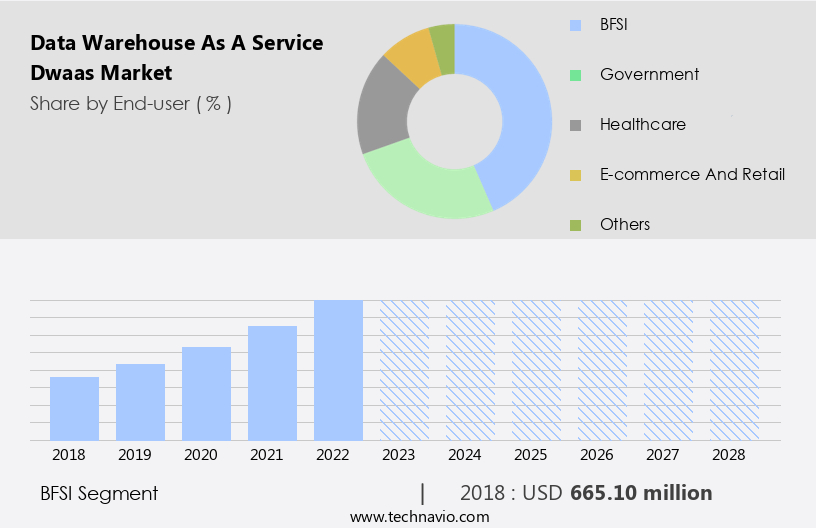

- The BFSI segment is estimated to witness significant growth during the forecast period.

The BFSI sector's reliance on managing and analyzing large financial data volumes has fueled the adoption of Data Warehouse as a Service (DWaaS) solutions. DWaaS offers flexibility and scalability, enabling BFSI companies to efficiently manage data from retail banking institutions, lending operations, credit underwriting procedures, and financial consulting firms. DWaaS solutions provide core competencies in cloud computing, business intelligence (BI), data analytics, enterprise management, visualization, and BI solutions. Technological developments, such as IoT technology and AI technology, further enhance DWaaS capabilities. However, challenges persist, including security issues, integration challenges, and restricted customization. Cloud solutions, including cloud data warehouses, offer a data environment that is software, computing, and storage-intensive.

DWaaS companies address concerns with service disruptions, latency, data integration, and data access. Security measures, such as data encryption and data masking, ensure data privacy. Despite these challenges, DWaaS adoption continues to grow, offering decision support services, data categorization, and data assessment to mid-size businesses and large enterprises.

Get a glance at the Data Warehouse As A Service Industry report of share of various segments Request Free Sample

The BFSI segment was valued at USD 665.10 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

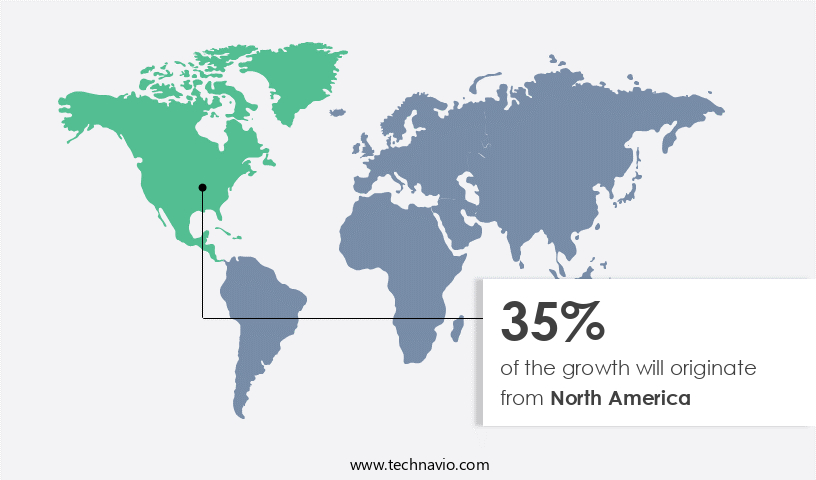

- North America is estimated to contribute 35% to the growth of the global market during the forecast period.

Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The North American market for Data Warehouse as a Service (DWaaS) is experiencing significant growth due to the region's early adoption of advanced technologies in industries such as manufacturing, retail, and banking, financial services and insurance (BFSI). The presence of leading companies In the region contributes to market expansion. Additionally, the integration of cloud-based services, automation solutions, and AI with operational and supply chain processes is driving the adoption of data warehousing in North America. With several advanced economies located In the region, the demand for data processing, outsourcing, and infrastructure services is increasing. Businesses in North America are leveraging DWaaS to manage and analyze large data volumes, improve enterprise management, and enhance business intelligence and data analytics capabilities.

Technological developments, including virtual data warehousing, IoT technology, and AI technology, are also fueling market growth. However, concerns around data security, service disruptions, and integration challenges persist, necessitating robust security measures, such as data encryption and masking, and effective data access management.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Data Warehouse As A Service (Dwaas) Industry?

Shift from on-premises to SaaS model is the key driver of the market.

- Cloud-based Data Warehouse as a Service (DWaaS) is transforming the business landscape by providing flexible and scalable data management solutions. companies offer intuitive services with drag-and-drop functionalities and mobile accessibility, catering to businesses of all sizes. The pay-per-use pricing model allows clients to pay only for their utilized resources, while the flexibility in deployment models enables clients to build customized cloud-based infrastructures. Cloud-based data warehouses reduce the Total Cost of Ownership (TCO) by eliminating the need for extensive IT infrastructure. Technological developments, such as Business Intelligence (BI), data analytics, virtual data warehousing, IoT technology, and AI technology, are seamlessly integrated into these solutions.

- However, concerns around security issues and integration challenges persist. Security measures, including data encryption and masking, are implemented by DWaaS companies to mitigate risks. Service disruptions, latency, and data access are addressed through reliable cloud solutions. Data integration is streamlined, enabling real-time decision support services. The adoption of cloud data warehouses is driven by the increasing data volumes and IT infrastructure complexity. Various industries, such as retail banking institutions, lending operations, credit underwriting procedures, financial consulting firms, e-commerce, and mid-size businesses, are leveraging these solutions for improved employee and organizational productivity. Despite these benefits, challenges remain, including data categorization, assessment, and the impact of consumerization trends, such as mobile devices, social networking, and data searches.

- Cyberattacks and data transmission concerns are also areas of focus for businesses considering DWaaS adoption.

What are the market trends shaping the Data Warehouse As A Service (Dwaas) Industry?

Emergence of advanced storage technologies is the upcoming market trend.

- Data Warehouse as a Service (DWaaS) has emerged as a significant solution for businesses seeking flexibility and scalability In their data storage needs. With the increasing reliance on business intelligence (BI), data analytics, and enterprise management, the data volumes and IT infrastructure complexity have grown exponentially. DWaaS offers cloud solutions that cater to these requirements, providing advanced software, computing, and storage capabilities. Technological developments in areas like IoT technology, AI technology, and virtual data warehousing have further fueled DWaaS adoption. However, concerns around security issues and integration challenges persist. DWaaS companies offer data encryption, data masking, and other security measures to mitigate risks.

- Service disruptions, latency, and data integration remain key areas of focus. Businesses in various sectors, including retail banking institutions, lending operations, credit underwriting procedures, financial consulting firms, mid-size businesses, and e-commerce, are adopting DWaaS to enhance decision support services. The cloud data warehouse market continues to grow, offering a data environment that can cater to the informational data needs of organizations. Moreover, consumerization trends, such as the use of mobile devices, social networking, and data searches, have led to increased employee and organizational productivity. DWaaS solutions enable seamless access to data from these devices, facilitating analytics solutions and improving overall productivity.

- Despite these benefits, challenges such as data categorization, data assessment, and data access remain. Cyberattacks pose a significant threat to data security, necessitating robust security measures. DWaaS companies play a crucial role in addressing these challenges and ensuring a secure and reliable data environment for their clients.

What challenges does the Data Warehouse As A Service (Dwaas) Industry face during its growth?

Data privacy and security risks is a key challenge affecting the industry growth.

- Data Warehouse as a Service (DWaaS) is a cloud-based solution that offers businesses flexibility and scalability in managing their data warehouses. This technological development enables organizations to focus on their core competencies while leveraging the benefits of cloud computing. However, the adoption of DWaaS is not without challenges. Security issues, such as data encryption, data masking, and data security measures, are major concerns for businesses. Service disruptions due to latency and data integration challenges can also impact decision-making processes. Moreover, the integration of DWaaS with IoT technology, AI technology, and virtual data warehousing requires careful consideration. Data transmission and cyberattacks pose significant risks to data security.

- Businesses must ensure that their chosen DWaaS company has robust security measures in place to mitigate these risks. The adoption of DWaaS is particularly relevant for industries such as retail banking institutions, lending operations, credit underwriting procedures, financial consulting firms, and mid-size businesses. These organizations generate vast amounts of informational data that require efficient management and analysis for improved employee and organizational productivity. However, the move towards DWaaS adoption also brings challenges such as data categorization, data assessment, and data access. On-premise software and IT infrastructure complexity can hinder the transition to cloud solutions. Additionally, consumerization trends, such as mobile devices and social networking, require businesses to adapt to new data searches and analytics solutions.

- In conclusion, the DWaaS market offers businesses significant benefits in terms of flexibility, scalability, and technological improvement. However, it also presents challenges related to security, integration, and data management. Businesses must carefully evaluate these factors before adopting DWaaS to ensure they reap the maximum benefits while mitigating potential risks.

Exclusive Customer Landscape

The data warehouse as a service (dwaas) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the data warehouse as a service (dwaas) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, data warehouse as a service (dwaas) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Alphabet Inc. - Data Warehouse as a Service (DWaaS) is a cloud-based data management solution that enables businesses to store, manage, and analyze large volumes of data without the need for on-premises infrastructure. Google BigQuery is an exemplary DWaaS offering from a leading technology company.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alphabet Inc.

- Amazon.com Inc.

- AtScale Inc.

- Cloudera Inc.

- HCL Technologies Ltd.

- International Business Machines Corp.

- Microsoft Corp.

- Netavis Software GmbH

- Open Text Corporation

- Oracle Corp.

- Panoply Ltd.

- Progress Software Corp.

- SAP SE

- Snowflake Inc.

- Solver Inc.

- Teradata Corp.

- Transwarp Information Technology Shanghai Co. Ltd.

- Veeva Systems Inc.

- VMware Inc.

- Yellowbrick Data Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Data warehouses have become an essential component of modern business intelligence (BI) and data analytics strategies. With the increasing adoption of cloud computing, Data Warehouse as a Service (DWaaS) has emerged as a popular solution for enterprises seeking flexibility and scalability In their data environments. DWaaS offers several core competencies that differentiate it from traditional on-premise data warehouses. These include the ability to quickly scale up or down based on business needs, reduced IT infrastructure complexity, and access to advanced BI solutions and analytics tools. Cloud computing has played a significant role In the growth of DWaaS. Cloud data warehouses provide enterprises with the benefits of cloud solutions, such as computing and storage resources on demand, without the need for extensive IT infrastructure.

Moreover, cloud data warehouses offer advanced features like virtualization, data categorization, and data assessment, enabling businesses to make informed decisions based on their data. However, the adoption of DWaaS is not without challenges. Security issues, such as data encryption, data masking, and data security measures, are critical concerns for businesses. Service disruptions, latency, and data integration challenges can also impact the effectiveness of DWaaS. Moreover, restricted customization can be a limitation for some businesses, particularly those with complex data environments. Integration with Internet of Things (IoT) technology and Artificial Intelligence (AI) solutions can also pose challenges. Despite these challenges, the DWaaS market continues to grow, driven by technological developments and the increasing demand for decision support services.

Retail banking institutions, lending operations, credit underwriting procedures, financial consulting firms, and mid-size businesses are among the sectors that have embraced DWaaS to enhance their BI capabilities. The use of DWaaS is also influenced by consumerization trends, such as the increasing use of mobile devices, social networking, and data searches. Employee and organizational productivity are other key drivers, as businesses seek to leverage their data to gain a competitive edge. E-commerce is another sector that has seen significant growth in DWaaS adoption. The ability to process large data volumes and provide real-time insights is crucial for businesses in this sector to remain competitive.

In conclusion, DWaaS offers several benefits, including flexibility, scalability, and access to advanced BI solutions and analytics tools. However, it also presents challenges related to security, integration, and customization. Despite these challenges, the DWaaS market continues to grow, driven by technological improvement and the increasing demand for data-driven decision making.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

177 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 24.49% |

|

Market growth 2024-2028 |

USD 12.32 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

23.17 |

|

Key countries |

US, Germany, France, China, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Data Warehouse As A Service (Dwaas) Market Research and Growth Report?

- CAGR of the Data Warehouse As A Service (Dwaas) industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the data warehouse as a service (dwaas) market growth of industry companies

We can help! Our analysts can customize this data warehouse as a service (dwaas) market research report to meet your requirements.

RIA -

RIA -