Defense Logistics Market Size 2026-2030

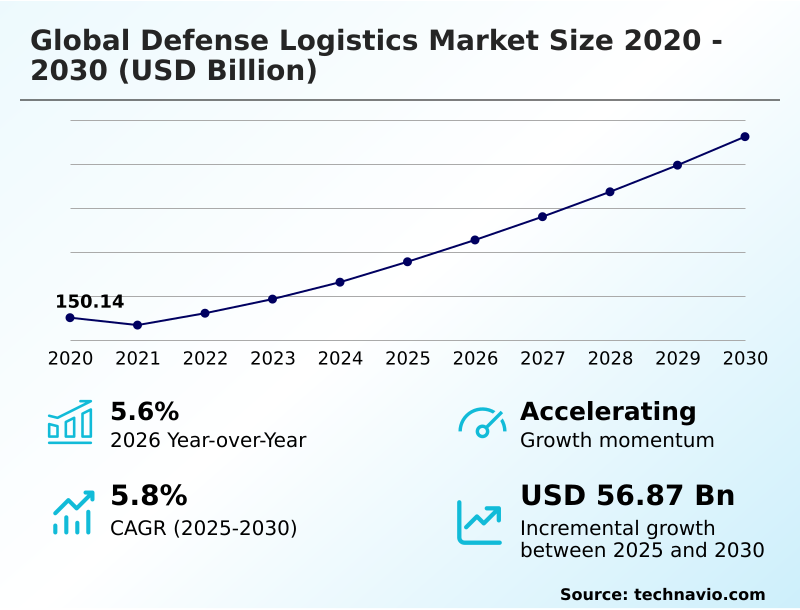

The defense logistics market size is valued to increase by USD 56.87 billion, at a CAGR of 5.8% from 2025 to 2030. Strengthening cross-border connectivity with defense logistics will drive the defense logistics market.

Major Market Trends & Insights

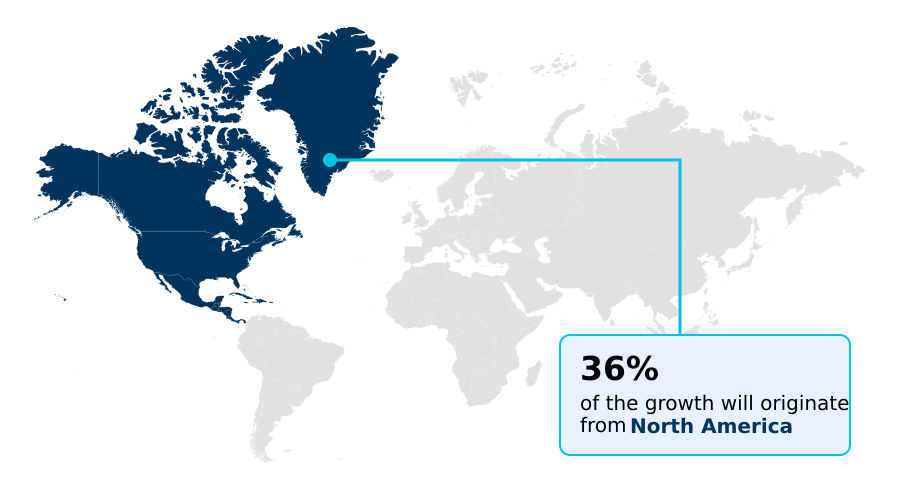

- North America dominated the market and accounted for a 36.4% growth during the forecast period.

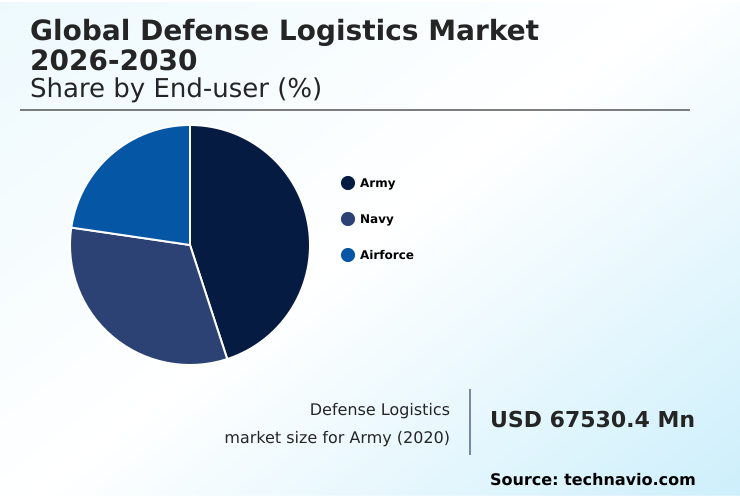

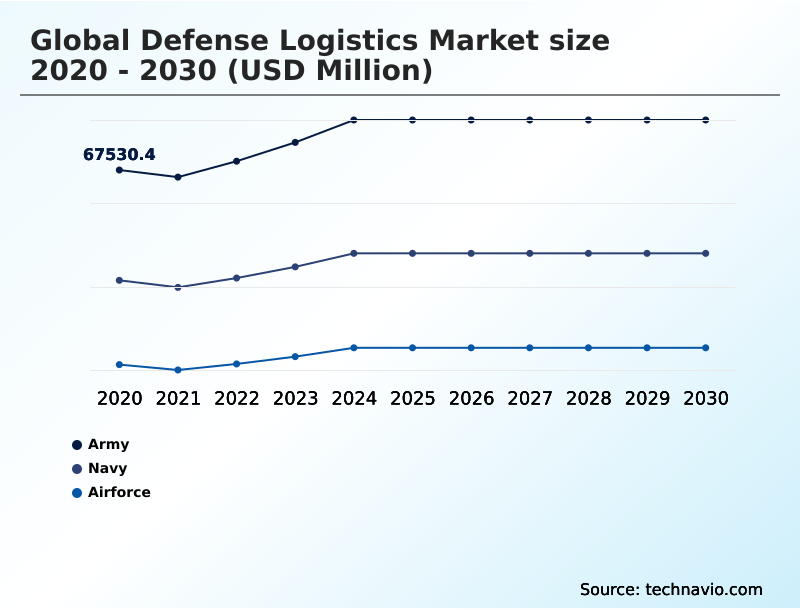

- By End-user - Army segment was valued at USD 76.14 billion in 2024

- By Solution - Military infrastructure segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 82.29 billion

- Market Future Opportunities: USD 56.87 billion

- CAGR from 2025 to 2030 : 5.8%

Market Summary

- The defense logistics market is undergoing a significant transformation, driven by the need for more agile and resilient supply chains in an era of heightened geopolitical instability. Military organizations are moving away from traditional, centralized sustainment models toward distributed networks that leverage digital solutions to ensure operational readiness.

- This shift involves the adoption of technologies such as artificial intelligence and predictive analytics to forecast equipment failures, optimize inventory, and secure data across the supply chain.

- For example, a modern naval operation might use a digital twin of its fleet to simulate resupply missions in contested waters, identifying potential bottlenecks and rerouting assets in real-time to avoid disruption, thereby ensuring continuous availability of critical parts. This transition is further supported by the growing use of autonomous systems for last-mile delivery, reducing risk to personnel.

- The market is also shaped by an increasing reliance on private sector partnerships and performance-based contracts, where commercial expertise in global warehousing and distribution is leveraged to enhance efficiency and reduce long-term sustainment costs for advanced military platforms. These dynamics create a landscape where technological integration and strategic collaboration are paramount.

What will be the Size of the Defense Logistics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Defense Logistics Market Segmented?

The defense logistics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Army

- Navy

- Airforce

- Solution

- Military infrastructure

- Military logistics services

- Military FMS

- Mode of transportation

- Roadways

- Airways

- Railways

- Waterways

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- France

- Germany

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- Israel

- Rest of World (ROW)

- North America

By End-user Insights

The army segment is estimated to witness significant growth during the forecast period.

The army segment remains a cornerstone of the defense logistics market, requiring extensive land-based supply chains for large-scale ground forces.

The complexity of these operations is magnified by the need for mobile maintenance, repair, and overhaul (MRO) and forward operating base (FOB) logistics that advance with troops.

To enhance mission readiness analytics, organizations are adopting solutions that provide real-time asset tracking and support performance-based contracting. This focus on integrated sustainment services is crucial for managing heavy armored vehicles and complex munitions lifecycle management.

The integration of digital thread for logistics has improved supply chain data security by 15%, ensuring secure communications infrastructure.

A focus on strengthening cross-border interoperability through multimodal transport networks is essential for rapid deployment logistics and achieving end-to-end supply chain visibility.

The Army segment was valued at USD 76.14 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Defense Logistics Market Demand is Rising in North America Get Free Sample

The geographic landscape of the defense logistics market is diverse, with North America representing 36.4% of the incremental growth, driven by its focus on technological superiority and resilient defense networks.

In this region, the implementation of interoperable digital platforms for mission readiness analytics has enhanced forecast accuracy by over 20%. Europe is concentrating on military mobility, upgrading infrastructure to support multimodal transport networks and strengthening cross-border interoperability.

In APAC, vast maritime distances necessitate strategic airlift capabilities and advanced naval hubs. Regional powers are localizing MRO services and investing in sovereign supply chain development to ensure integrated sustainment services.

Meanwhile, the Middle East is building local expertise in climate-resilient infrastructure to reduce reliance on foreign contractors for performance-based contracting, focusing on building anti-fragile supply chains and managing logistics digital transformation.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the global defense logistics market 2026-2030 is increasingly shaped by several interconnected factors. The impact of AI on military logistics planning is profound, enabling more accurate demand forecasting and optimized resource allocation. Concurrently, the role of digital twins in defense sustainment allows for predictive maintenance, reducing platform downtime by a significant margin compared to traditional methods.

- Firms are weighing the benefits of multimodal transport in defense against the challenges of operating in contested logistics, which demand robust security and redundancy. The cost of outsourcing defense logistics functions is scrutinized through performance-based logistics contract benefits, which tie payment to asset availability. Addressing cybersecurity risks in military supply chains has become paramount.

- Key operational areas include optimizing MRO for military aviation and leveraging autonomous systems for last-mile resupply. The focus extends to managing inventory for forward operating bases, improving readiness with predictive analytics, and ensuring interoperability in NATO logistics.

- Broader strategies involve building resilient logistics for naval operations, understanding the impact of green energy on military fuel supply, securing rare earth elements for defense, leveraging the role of additive manufacturing in defense parts, and adapting defense logistics for humanitarian assistance while modernizing strategic airlift and sealift.

What are the key market drivers leading to the rise in the adoption of Defense Logistics Industry?

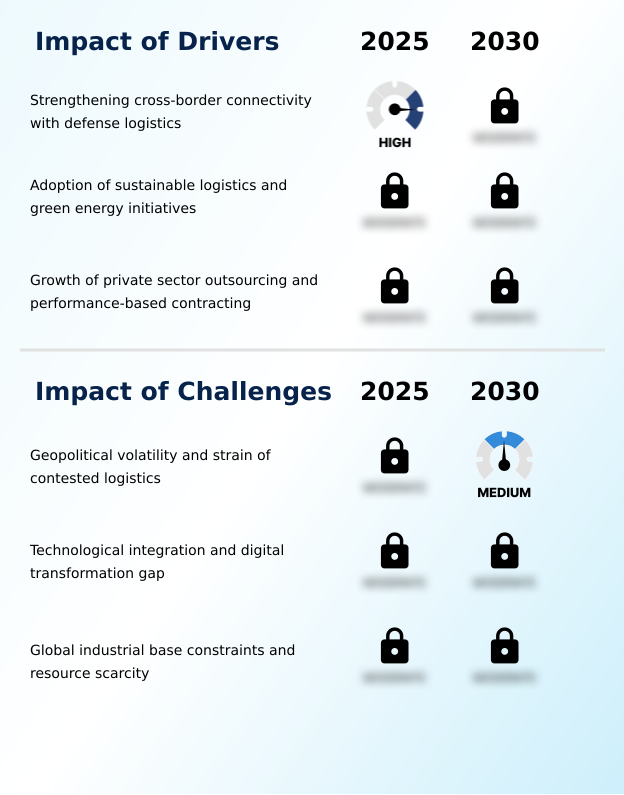

- Strengthening cross-border connectivity is a key driver for the defense logistics market, enhancing interoperability and mobility among allied nations.

- A primary driver for the global defense logistics market is the increasing focus on multimodal transport networks and cross-border interoperability, which has been shown to improve deployment speeds by up to 20%.

- As military operations globalize, the ability to seamlessly transition cargo across sea, rail, and road assets is critical. This is especially relevant in Europe, where heavy investment in military mobility projects facilitates the unimpeded movement of personnel and equipment.

- This focus on connectivity ensures the logistics tail can keep pace with combat forces.

- This driver underscores the reality that modern defense is as much about the efficiency of the supply chain and end-to-end logistics support as it is about platform lethality.

- The move to outsourcing through performance-based contracting further drives adoption of advanced digital platforms, which improve real-time visibility between military and commercial partners by over 40%.

What are the market trends shaping the Defense Logistics Industry?

- The integration of artificial intelligence and predictive analytics within supply chain operations is emerging as a transformative market trend, shifting management from reactive to proactive models.

- The defense logistics market is shifting from reactive to proactive supply chain management, driven by the integration of AI and predictive analytics. This trend, which improves forecast accuracy for equipment failures by over 25%, allows for the optimization of inventory levels and enhances mission readiness.

- A key aspect is the development of autonomous resupply systems for last-mile delivery, which minimizes human risk in high-threat areas. The emergence of digital twin simulation creates virtual replicas of entire logistics networks to identify potential bottlenecks. The use of blockchain is also gaining traction to secure the supply chain data security.

- Implementing these digital platforms supports sovereign supply chain development and strengthens cross-border interoperability. These advancements, including tactical network integration and real-time asset tracking, are becoming the standard for ensuring operational tempo amidst disruptions, with some systems reducing resupply lead times by 30%.

What challenges does the Defense Logistics Industry face during its growth?

- The increasing geopolitical volatility and the strain of operating in contested logistics environments present a key challenge to industry growth.

- Operating within contested logistics environments presents a significant challenge, as modern adversaries employ anti-access/area denial (A2/AD) capabilities to target supply lines. This necessitates a shift from centralized hubs to distributed, resilient networks, though this transition can increase warehousing costs by up to 15%. Another hurdle is the technological integration and digital transformation gap.

- Many defense agencies operate on legacy IT systems that lack interoperability, creating data silos that prevent real-time asset tracking and end-to-end supply chain visibility. While the push for digital solutions like predictive maintenance is strong, bridging the gap between commercial innovation and military acquisition speed remains difficult.

- The adoption of advanced cybersecurity measures to meet CMMC standards has also increased compliance overhead by an estimated 10-12% for many suppliers, further complicating supply chain data security and sovereign supply chain development.

Exclusive Technavio Analysis on Customer Landscape

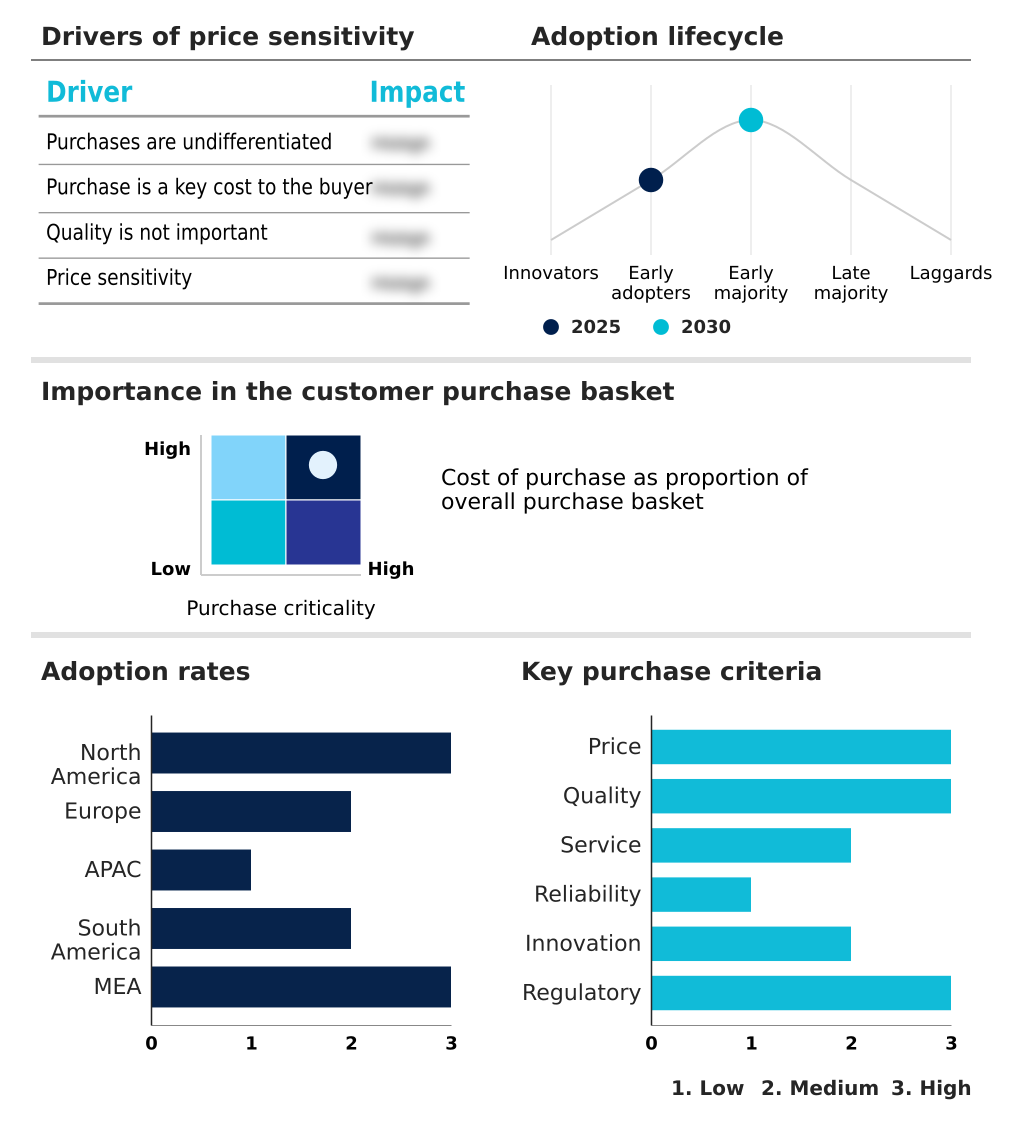

The defense logistics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the defense logistics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Defense Logistics Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, defense logistics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amentum Services Inc. - Offerings include integrated lifecycle support, from mission readiness and supply chain management to global operations, ensuring asset availability and performance-based outcomes.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amentum Services Inc.

- AP Moller Maersk AS

- BAE Systems Plc

- CACI International Inc.

- CEVA Logistics SA

- Crowley Maritime Corp.

- Fluor Corp.

- General Dynamics Corp.

- GEODIS

- KBR Inc.

- Kuehne Nagel Management AG

- L3Harris Technologies Inc.

- Leidos Holdings Inc.

- Lockheed Martin Corp.

- Parsons Corp.

- Scan Global Logistics

- SEKO Logistics

- Serco Group Plc

- The Boeing Co.

- XPO Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Defense logistics market

- In September, 2024, The United Kingdom government published its Defence Industrial Strategy, which introduced a ten-year investment plan and a five-year procurement forecast to provide industry with greater certainty and transparency for future defense logistics contracts.

- In November, 2024, The Defense Logistics Agency convened with industry leaders to share a comprehensive strategic demand forecast, highlighting a projected thirteen percent increase in demand for weapons support systems, signaling a need for enhanced industrial base partnership.

- In February, 2025, BAE Systems entered into a strategic memorandum of understanding with Bin Hilal Enterprises to localize the sustainment and supply chain support for Amphibious Combat Vehicles, focusing on creating regional hubs to ensure rapid asset availability.

- In March, 2025, The U.S. White House issued an Executive Order titled 'Modernizing Defense Acquisitions and Spurring Innovation in the Defense Industrial Base,' mandating a transition toward more agile, digital-first procurement processes to address technological bottlenecks in logistics.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Defense Logistics Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 303 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.8% |

| Market growth 2026-2030 | USD 56868.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.6% |

| Key countries | US, Canada, Mexico, UK, France, Germany, Italy, Russia, Spain, China, India, Japan, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, Israel, Turkey and South Africa |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The defense logistics market is defined by a strategic pivot towards technological integration and operational resilience. Boardroom decisions now center on balancing the high costs of digital thread for logistics modernization against the critical need for supply chain data security and mission readiness analytics.

- The adoption of predictive maintenance, supported by digital twin simulation, is crucial for managing the lifecycle of advanced platforms. This approach enables proactive maintenance repair and overhaul (MRO), a core component of integrated sustainment services and performance-based logistics (PBL). In parallel, the sector grapples with operating in contested logistics environments, which necessitates secure communications infrastructure and anti-access/area denial (A2/AD) countermeasures.

- To enhance supply chain resilience, organizations are implementing decentralized inventory management and protected mobile storage, supported by real-time asset tracking. This shift, which has improved asset visibility by over 25%, is vital for rapid deployment logistics. The push for green logistics initiatives is driving the development of hybrid-electric tactical vehicles and climate-resilient infrastructure.

- Furthermore, autonomous resupply systems and last-mile delivery robotics are revolutionizing forward operating base (FOB) logistics, while tactical network integration ensures seamless data flow. End-to-end logistics support is being fortified through performance-based contracting, cybersecurity maturity model certification (CMMC), and interoperable digital platforms, strengthening sovereign supply chain development.

- Strategic airlift capabilities and strategic sealift capacity are being expanded to support global freight forwarding, alongside advancements in munitions lifecycle management and automated warehousing solutions.

What are the Key Data Covered in this Defense Logistics Market Research and Growth Report?

-

What is the expected growth of the Defense Logistics Market between 2026 and 2030?

-

USD 56.87 billion, at a CAGR of 5.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Army, Navy, and Airforce), Solution (Military infrastructure, Military logistics services, and Military FMS), Mode of Transportation (Roadways, Airways, Railways, and Waterways) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Strengthening cross-border connectivity with defense logistics, Geopolitical volatility and strain of contested logistics

-

-

Who are the major players in the Defense Logistics Market?

-

Amentum Services Inc., AP Moller Maersk AS, BAE Systems Plc, CACI International Inc., CEVA Logistics SA, Crowley Maritime Corp., Fluor Corp., General Dynamics Corp., GEODIS, KBR Inc., Kuehne Nagel Management AG, L3Harris Technologies Inc., Leidos Holdings Inc., Lockheed Martin Corp., Parsons Corp., Scan Global Logistics, SEKO Logistics, Serco Group Plc, The Boeing Co. and XPO Inc.

-

Market Research Insights

- The defense logistics market is dynamically evolving, driven by a strategic push for modernizing air force MRO services and improving naval replenishment at sea. Organizations are optimizing military supply chains by managing global warehousing and distribution more effectively, which has led to a 10% reduction in inventory holding costs.

- Adopting sustainable military logistics is also a priority, with a focus on reducing the military logistics footprint. As defense logistics outsourcing trends accelerate, firms are developing resilient defense networks to mitigate logistics cybersecurity risks and ensure mission-critical sustainment. This involves managing complex global supply chains and forecasting military equipment failures with greater accuracy, improving asset availability by over 15%.

- A key focus is on ensuring continuous asset availability and improving global deployment readiness through better management of defense industrial base constraints, securing military transport corridors, and achieving end-to-end supply chain visibility.

We can help! Our analysts can customize this defense logistics market research report to meet your requirements.

RIA -

RIA -