Diagnostic Wearable Medical Devices Market Size 2024-2028

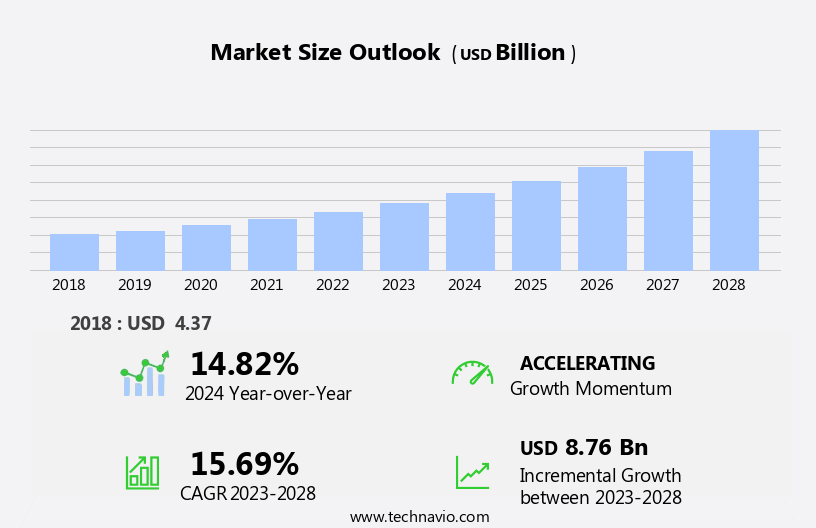

The diagnostic wearable medical devices market size is forecast to increase by USD 8.76 billion, at a CAGR of 15.69% between 2023 and 2028.

- The market is experiencing significant growth, driven by the increasing prevalence of chronic diseases and the expanding utilization of these devices in the medical sector. The integration of advanced technologies, such as machine learning and artificial intelligence, is enabling these devices to deliver accurate and timely diagnoses, enhancing their appeal to both healthcare providers and patients. However, the market faces challenges related to user acceptance and adherence to diagnostic wearable medical devices. Patients may find the devices intrusive or uncomfortable, leading to reluctance to use them consistently.

- Additionally, concerns regarding data privacy and security can hinder adoption. To capitalize on market opportunities and navigate these challenges effectively, companies must focus on designing user-friendly devices, addressing privacy concerns, and providing clear communication regarding the benefits and importance of consistent usage. By addressing these factors, they can foster trust and confidence in the technology, ultimately driving growth in the market.

What will be the Size of the Diagnostic Wearable Medical Devices Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, integrating advanced technologies to monitor and analyze various health parameters. Blood oxygen saturation, electrocardiogram analysis, patient data encryption, electrodermal activity, sleep apnea detection, muscle activity monitoring, skin conductance, gyroscope data, temperature sensing, vital signs monitoring, body composition analysis, heart rate variability, and pulse oximetry are among the key features. Wearable sensors, wireless communication, and mobile app integration enable real-time data acquisition and analysis. Diagnostic algorithms and machine learning models facilitate accurate interpretation of the data, while telemedicine integration and remote patient monitoring expand access to healthcare services.

ECG monitoring, insulin delivery systems, drug delivery patches, and respiratory rate monitoring are some applications. Continuous innovation drives the market, with new technologies and applications unfolding, ensuring a dynamic and evolving landscape.

How is this Diagnostic Wearable Medical Devices Industry segmented?

The diagnostic wearable medical devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Device

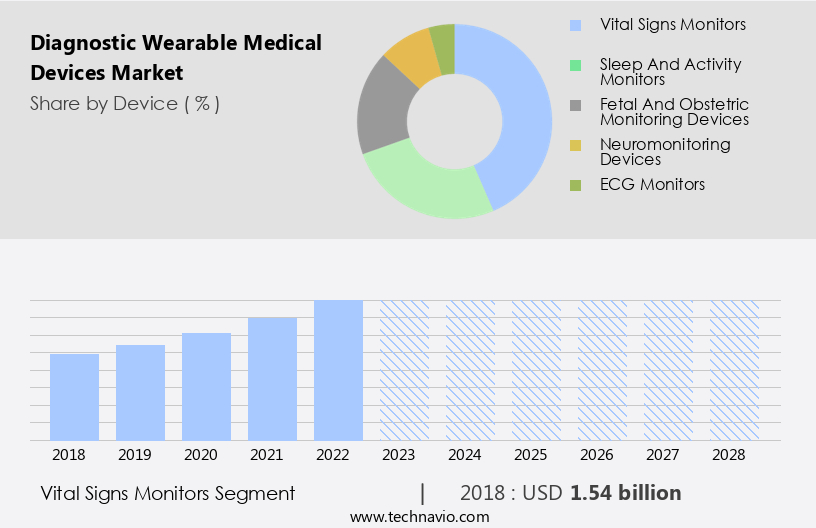

- Vital signs monitors

- Sleep and activity monitors

- Fetal and obstetric monitoring devices

- Neuromonitoring devices

- ECG monitors

- Application

- Home healthcare

- Sports and fitness

- Remote patient monitoring

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Device Insights

The vital signs monitors segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant growth, driven by the increasing preference for proactive health monitoring. Vital signs monitors, as a leading device type sub-segment, continuously track essential indicators like heart rate, blood pressure, oxygen saturation, and more. Market leaders, such as Apple and Fitbit, are introducing advanced diagnostic wearables with integrated vital signs monitoring capabilities, fueling market expansion. Consumers' growing demand for real-time health information is a primary growth driver. However, data privacy concerns, legal constraints, and accuracy limitations pose challenges. To address these concerns, the industry is transitioning towards customized healthcare, advanced sensor technology, and AI for data analysis.

Wearable sensors, including ECG monitors, respiratory rate monitors, and biometric data acquisition devices, are integral to this evolution. Additionally, telemedicine integration, insulin delivery systems, activity tracking, and machine learning models are revolutionizing healthcare, enabling remote patient monitoring and early disease detection. Wireless communication, cloud data storage, and health data analytics further enhance the value proposition of these devices. In conclusion, the market is poised for continued growth, driven by advancements in technology, consumer demand, and the shift towards personalized healthcare.

The Vital signs monitors segment was valued at USD 1.54 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

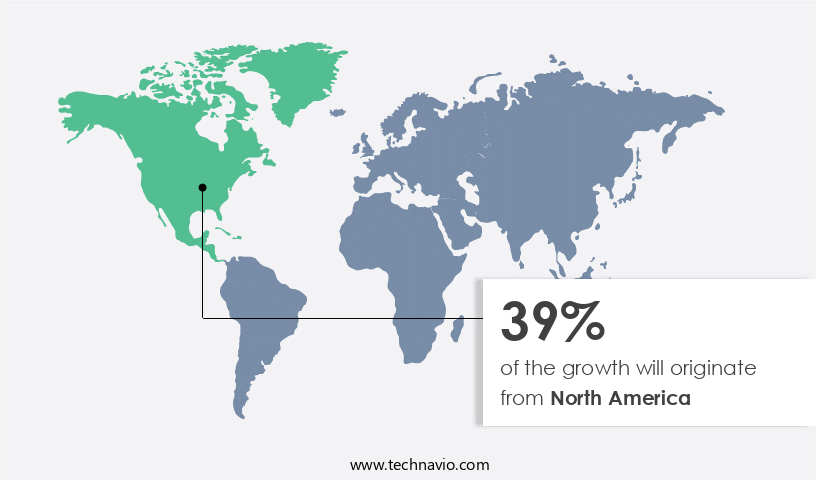

North America is estimated to contribute 39% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the dynamic landscape of healthcare technology, diagnostic wearable medical devices have emerged as a game-changer. These devices, which integrate fall detection, Bluetooth connectivity, data security protocols, mobile app integration, diagnostic algorithms, insulin delivery systems, activity tracking, telemedicine integration, ECG monitoring, remote patient monitoring, wearable sensors, respiratory rate monitoring, biometric data acquisition, drug delivery patches, cloud data storage, continuous glucose monitoring, blood oxygen saturation, electrocardiogram analysis, patient data encryption, electrodermal activity, sleep apnea detection, muscle activity monitoring, skin conductance, gyroscope data, temperature sensing, vital signs monitoring, body composition analysis, wireless communication, machine learning models, heart rate variability, pulse oximetry, health data analytics, and accelerometer data, are revolutionizing disease management and prevention.

The North American market, spearheaded by the US, dominates this sector due to a rising incidence of chronic diseases, increased prevalence of heart and respiratory disorders, and a growing awareness of health concerns. The future promises continuous diagnosis, seamless integration with healthcare systems, and personalized treatment plans.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth as technology advances and the need for remote patient monitoring increases. Wearable sensors, a key component of these devices, collect valuable health data that can be interpreted to improve diagnostic accuracy. However, ensuring the accuracy of continuous glucose monitoring and other health readings is crucial, as patient data privacy and security are paramount. Remote monitoring systems must be integrated seamlessly to allow real-time analysis, while machine learning algorithms, such as those used for ECG analysis, can enhance diagnostic capabilities. Energy efficiency is another essential factor in wearable devices, as is telemedicine platform compatibility and biometric data encryption protocols. Patient compliance is improved through user-friendly designs, including those tailored to elderly patients, and algorithm bias mitigation techniques. Sensor miniaturization technologies enable more discreet and comfortable devices, while clinical validation and regulatory requirements ensure their effectiveness and safety. Data visualization and mobile app integration facilitate effective data management, and data interoperability and standardization enable seamless information exchange between devices and healthcare providers. Optimizing wearable device battery life and improving diagnostic algorithm accuracy through machine learning further enhance their value. As the market continues to evolve, these advancements will contribute to improved patient outcomes and more efficient healthcare systems.

What are the key market drivers leading to the rise in the adoption of Diagnostic Wearable Medical Devices Industry?

- The rising incidence of chronic diseases serves as the primary catalyst for market growth.

- Diagnostic wearable medical devices have gained significant attention in the healthcare industry due to their ability to monitor and manage various chronic conditions in real-time. These devices, which include fall detection systems, insulin delivery systems, and activity trackers, among others, leverage Bluetooth connectivity and mobile app integration for seamless data transfer and analysis. Diagnostic algorithms integrated into these devices enable early detection and intervention, improving patient outcomes and reducing hospitalizations. The importance of data security protocols is paramount in this context, ensuring patient privacy and data confidentiality. Telemedicine integration further enhances the capabilities of these devices, enabling remote consultations and real-time monitoring, thereby improving accessibility and convenience.

- Chronic diseases such as cardiovascular diseases (CVDs), chronic respiratory diseases, and diabetes continue to pose significant health challenges worldwide. According to the World Health Organization (WHO), nearly 1 billion people live with elevated blood pressure, resulting in approximately 9.4 million deaths annually, with over 50% attributable to stroke and the remaining to cardiac disorders. The global impact of CVDs is comparable to that of Alzheimer's disease, breast, cervical, prostate, and colorectal cancers combined. In response to these health concerns, diagnostic wearable medical devices are increasingly being adopted to improve patient care and reduce healthcare costs.

- These devices offer a non-invasive, cost-effective, and convenient solution for managing chronic conditions, ultimately leading to better health outcomes.

What are the market trends shaping the Diagnostic Wearable Medical Devices Industry?

- The use of diagnostic wearable medical devices is gaining significant traction in the medical sector, representing an emerging market trend. This technology enables continuous health monitoring and early detection of various health conditions, offering numerous benefits to both patients and healthcare providers.

- The market is experiencing significant growth due to the integration of advanced technologies and increasing consumer demand for remote health monitoring. Companies are developing innovative solutions to cater to this trend, focusing on enhancing the functionality and usability of their devices. For instance, ECG monitoring wearables, such as those offered by Philips, utilize digital biosensors to record and transmit real-time biometric data to cloud-based platforms for remote patient monitoring. Similarly, wearable sensors for respiratory rate monitoring and continuous glucose monitoring enable individuals and healthcare professionals to closely monitor health conditions.

- Furthermore, drug delivery patches and biometric data acquisition devices offer convenience and precision in managing various health issues. The market's future potential lies in the ability to provide accurate, real-time health information, enabling early intervention and improved patient outcomes.

What challenges does the Diagnostic Wearable Medical Devices Industry face during its growth?

- The growth of the diagnostic wearable medical devices industry is significantly impacted by challenges related to user acceptance and adherence. This issue, which is of great concern, hinders the industry's expansion and underscores the need for effective strategies to address user apprehensions and ensure consistent use of these devices.

- The market faces acceptance challenges due to user discomfort and social stigma. Continuous monitoring devices, such as those for blood oxygen saturation or electrocardiogram analysis, may cause discomfort, leading to noncompliance. Individuals with chronic conditions, like diabetes, may avoid wearing continuous glucose monitoring devices due to persistent skin penetration. Wearable devices for mental health conditions can raise social and psychological concerns due to their visible nature.

- Patient data encryption is crucial to address privacy concerns and build trust in the market. Advanced technologies like electrodermal activity, sleep apnea detection, muscle activity monitoring, skin conductance, and gyroscope data contribute to the market's growth. Ensuring user comfort and addressing privacy concerns are essential to drive market acceptance and growth.

Exclusive Customer Landscape

The diagnostic wearable medical devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the diagnostic wearable medical devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, diagnostic wearable medical devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Activinsights Ltd. - This company specializes in medical wearable technology, producing devices like GENEActiv and Activinsights for monitoring and analyzing health data.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Activinsights Ltd.

- AliveCor Inc.

- Alphabet Inc.

- Apple Inc.

- Boyd Corp.

- BTS Bioengineering Corp.

- Cleveland Medical Devices Inc.

- Dragerwerk AG and Co. KGaA

- Johari Digital India Ltd.

- Koninklijke Philips N.V.

- Medtronic Plc

- Meril Life Sciences Pvt. Ltd.

- Molex LLC

- Murata Vios, Inc.

- OMRON Corp.

- ResMed Inc.

- Sanmina Corp.

- VitalConnect Inc.

- Wellue Health

- Intelesens Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Diagnostic Wearable Medical Devices Market

- In January 2024, Fitbit, a leading wearable technology company, announced the launch of its newest product, Fitbit Sense 2, featuring advanced health monitoring capabilities, including an Electrocardiogram (ECG) app and a Blood Oxygen Saturation (SpO2) sensor (Fitbit Press Release, 2024).

- In March 2024, Apple and Abbott, a global healthcare leader, announced a strategic partnership to integrate Abbott's FreeStyle Libre glucose monitoring system with Apple Watch, enabling real-time glucose monitoring for diabetes patients (Apple Newsroom, 2024).

- In April 2025, Siemens Healthineers, a leading medical technology company, completed the acquisition of Caradigm, a health analytics and population health management company, to expand its diagnostic and digital health offerings (Siemens Healthineers Press Release, 2025).

- In May 2025, the U.S. Food and Drug Administration (FDA) granted clearance to Dexcom, a diabetes care company, for its G6 CGM system, which is the first continuous glucose monitoring system with a 10-day wear duration (Dexcom Press Release, 2025).

Research Analyst Overview

- The market is experiencing significant advancements, driven by device miniaturization and the integration of algorithm validation for personalized healthcare. Chronic disease management is a primary focus, with data visualization tools and interoperability enabling seamless information exchange between devices and healthcare providers. Risk mitigation strategies, such as sensor calibration and data transmission protocols, ensure accurate and reliable data. Power consumption optimization and wearable comfort are essential considerations for patient compliance. FDA approval processes and clinical validation studies ensure regulatory compliance and patient safety features.

- Medical grade materials and accuracy assessment are crucial for medical-grade devices, while predictive analytics and patient engagement tools facilitate early disease detection. Data privacy regulations and user interface design are essential for maintaining patient trust and ensuring healthcare data standards. Regulatory compliance, battery life extension, signal processing techniques, remote diagnostics, and precision medicine applications further expand the market's potential.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Diagnostic Wearable Medical Devices Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

174 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 15.69% |

|

Market growth 2024-2028 |

USD 8.76 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

14.82 |

|

Key countries |

US, UK, Germany, China, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Diagnostic Wearable Medical Devices Market Research and Growth Report?

- CAGR of the Diagnostic Wearable Medical Devices industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the diagnostic wearable medical devices market growth of industry companies

We can help! Our analysts can customize this diagnostic wearable medical devices market research report to meet your requirements.

RIA -

RIA -