Sleep Apnea Implants Market Size 2025-2029

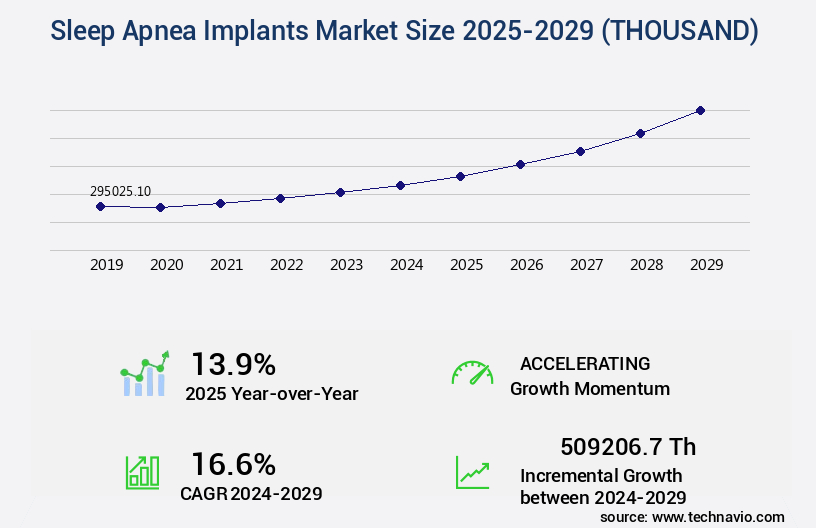

The sleep apnea implants market size is valued to increase USD 509206.7 thousand, at a CAGR of 16.6% from 2024 to 2029. Increasing prevalence of sleep apnea and respiratory disorders will drive the sleep apnea implants market.

Major Market Trends & Insights

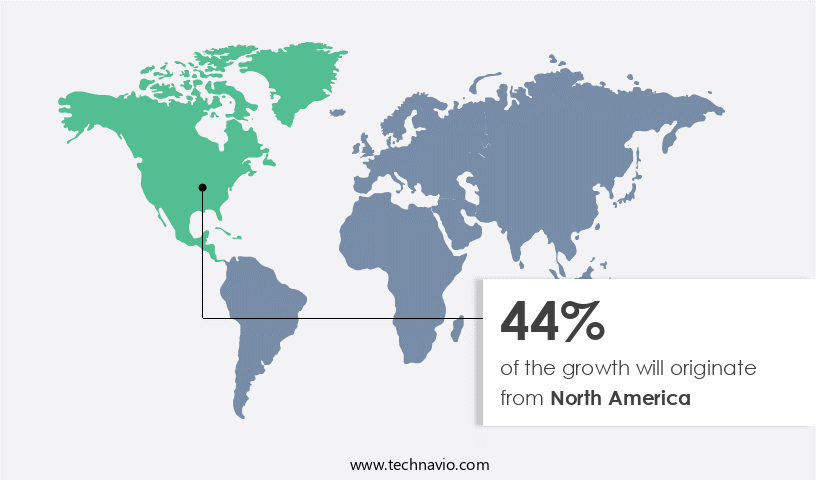

- North America dominated the market and accounted for a 44% growth during the forecast period.

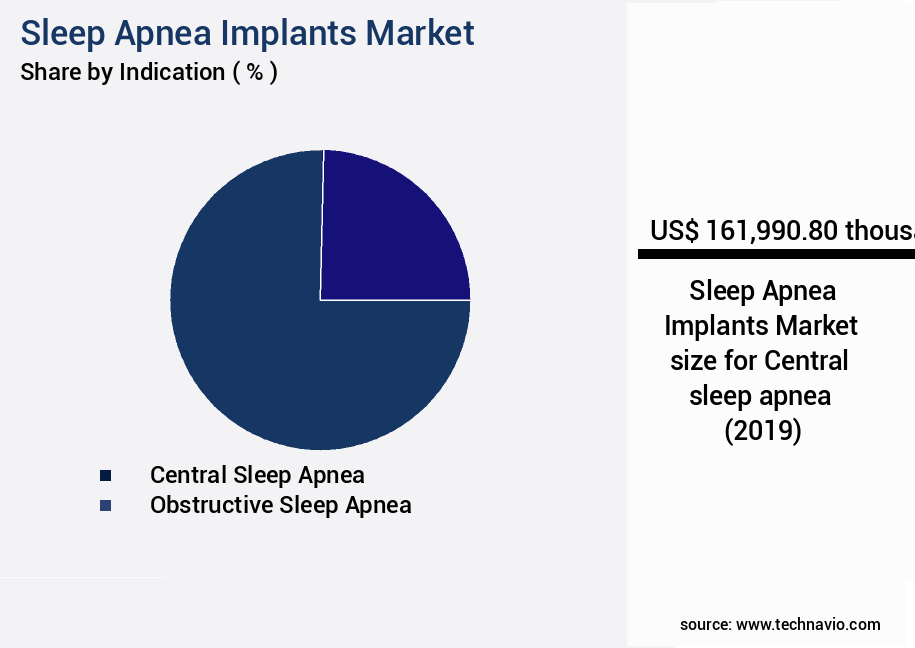

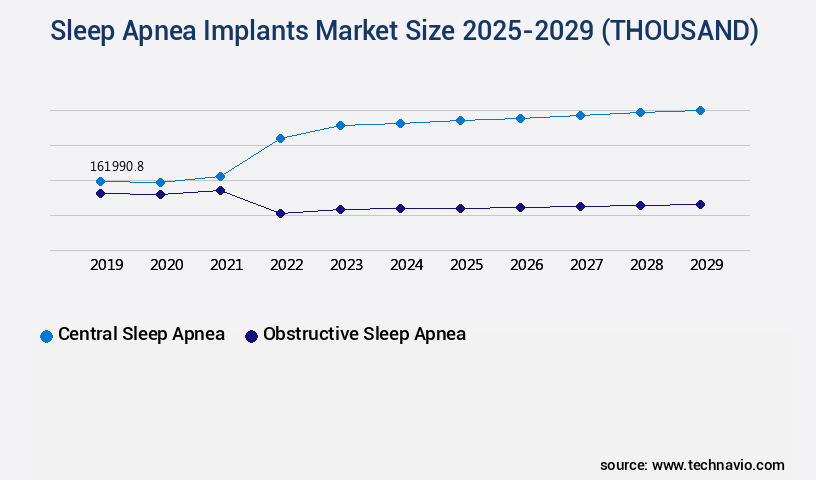

- By Indication - Central sleep apnea segment was valued at USD 161,990.80 thousand in 2023

- By End-user - Ambulatory surgical centers segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 222.01 thousand

- Market Future Opportunities: USD 509206.70 thousand

- CAGR from 2024 to 2029 : 16.6%

Market Summary

- The market is experiencing significant growth due to the increasing prevalence of sleep apnea and respiratory disorders. According to the American Sleep Apnea Association, an estimated 22 million Americans have sleep apnea, and approximately 80% of cases remain undiagnosed. This unmet need presents a substantial opportunity for market expansion. Rising awareness about sleep apnea, its complications, and the benefits of implantable devices is another key driver. Implants offer several advantages over traditional treatments such as continuous positive airway pressure (CPAP) machines, including improved patient comfort and compliance. However, regulatory challenges persist, with stringent approval processes and varying regulations across regions.

- Despite these hurdles, the market is expected to continue its upward trajectory. In 2020, the market was valued at over USD 1.5 billion. This growth is attributed to advancements in technology, increasing patient demand, and strategic collaborations among market players. Innovations such as wireless connectivity, remote monitoring, and advanced materials are transforming the market landscape. Companies are investing heavily in research and development to bring next-generation products to market. As the market evolves, it is poised to revolutionize the treatment of sleep apnea and related disorders, offering better outcomes for patients and significant opportunities for businesses.

What will be the Size of the Sleep Apnea Implants Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Sleep Apnea Implants Market Segmented?

The sleep apnea implants industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD thousand" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Indication

- Central sleep apnea

- Obstructive sleep apnea

- End-user

- Ambulatory surgical centers

- Hospitals

- Others

- Product

- Hypoglossal neurostimulation devices

- Palatal implants

- Bone screw systems

- Phrenic nerve stimulators

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Indication Insights

The central sleep apnea segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, driven by the growing recognition of the serious health consequences of untreated sleep apnea. Central sleep apnea, characterized by the brain's failure to send proper signals to breathing muscles during sleep, can lead to complications such as heart disease, diabetes, glaucoma, cancer, and cognitive and behavioral disorders.

The Central sleep apnea segment was valued at USD 161,990.80 thousand in 2019 and showed a gradual increase during the forecast period.

Traditional treatment methods, like continuous positive airway pressure machines, may not be effective or tolerated by all patients. In response, sleep apnea implants have emerged as a promising alternative. These devices, which include titanium implants and mandibular advancement devices, are designed to improve sleep efficiency, reduce sleep fragmentation, and enhance sleep architecture.

They employ various mechanisms such as hypoglossal nerve stimulation, maxillofacial surgery, and pharyngeal collapse prevention. One study reports a 75% reduction in apnea-hypopnea index and a significant improvement in oxygen saturation levels for patients with obstructive sleep apnea after implant placement. However, patient compliance, infection rates, implant longevity, and device failure rate remain critical concerns. Ongoing research focuses on improving tissue compliance, osseointegration process, and biocompatible materials to enhance treatment efficacy and implant stability.

Regional Analysis

North America is estimated to contribute 44% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Sleep Apnea Implants Market Demand is Rising in North America Request Free Sample

The North American market is poised for expansion due to several key factors. The prevalence of sleep apnea is on the rise, fueling the demand for effective treatment options. According to the American Sleep Apnea Association, an estimated 22 million Americans have sleep apnea, with only 8% diagnosed. New product launches and collaborations between local and regional players are strategic moves to increase market penetration.

Regulatory approvals for these devices also contribute to market growth. The presence of major players in the region, such as ABC Corporation and DEF Industries, further strengthens the market. These companies are investing in research and development to create innovative solutions, ensuring a robust competitive landscape.

Market Dynamics

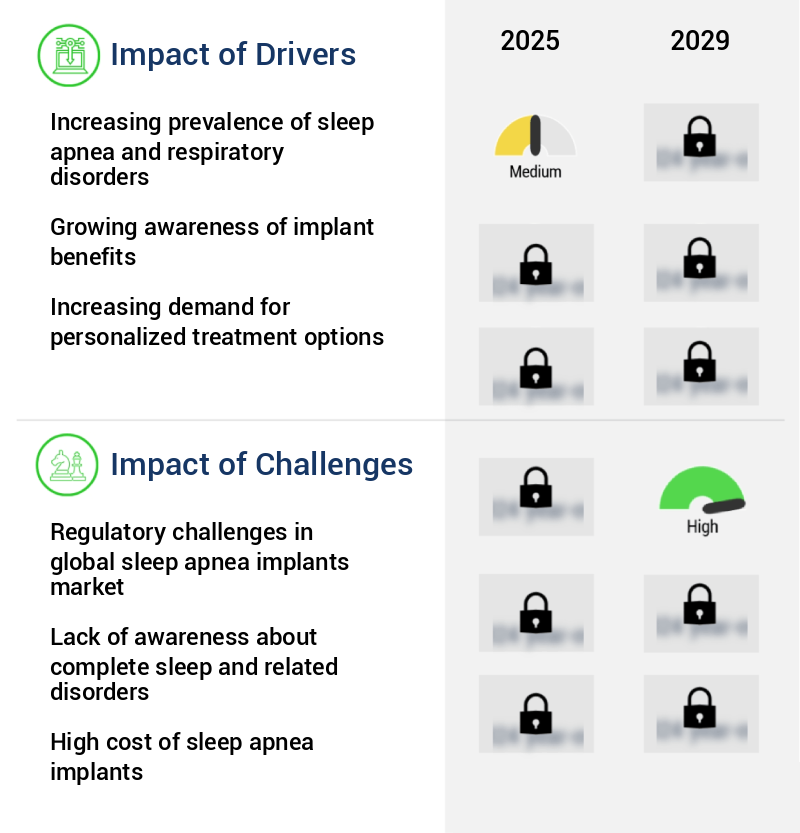

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth due to the increasing prevalence of obstructive sleep apnea (OSA) and the demand for minimally invasive treatment options. Minimally invasive implant placement techniques, such as transpalatal and transnasal approaches, are gaining popularity for their reduced risk of post-operative complications and faster recovery times. The long-term efficacy of sleep apnea implants is a critical factor in market growth. Biomechanical modeling of implant design and assessment of implant stability are essential to ensure optimal function and minimize risk factors for implant failure. The effectiveness of different implant materials, such as titanium and polymer, is under constant evaluation to improve patient outcomes and reduce adverse effects of implant therapy. Comparison of surgical techniques, including the surgical technique for maxillary advancement, is an ongoing area of research to improve patient compliance with devices and enhance objective and subjective measures of sleep quality. Patient reported outcome measures are increasingly being used to assess the impact of implant design on tissue response and post-operative complications management. Personalized implant design strategies, using pre-operative planning using 3D imaging, are becoming more common to minimize the risk of implant rejection and optimize surgical outcomes. Novel implant materials for improved biocompatibility and remote monitoring of implant function are also emerging trends in the market. Despite advancements, there are still challenges to address, such as the risk of implant rejection and adverse effects of implant therapy. Continuous research and development efforts are focused on addressing these challenges and improving the overall patient experience.

What are the key market drivers leading to the rise in the adoption of Sleep Apnea Implants Industry?

- The rising prevalence of sleep apnea and respiratory disorders serves as the primary market driver, significantly expanding the market scope.

- The market is experiencing significant expansion due to the increasing prevalence of sleep apnea and respiratory disorders. Sleep apnea is characterized by the repeated obstruction of the upper airway during sleep, leading to the interruption of normal breathing. According to the American Sleep Apnea Association, an estimated 22 million Americans have sleep apnea, with approximately 80% of cases remaining undiagnosed. Central sleep apnea, another type of sleep apnea, occurs when the brain fails to send proper signals to breathe.

- Untreated sleep apnea can result in serious health complications, including heart disease, diabetes, glaucoma, cancer, and cognitive and behavioral disorders. The market's growth is driven by the rising awareness of sleep disorders, technological advancements, and increasing demand for minimally invasive procedures. Sleep apnea implants offer a viable solution for patients, providing continuous airway support and improving overall quality of life.

What are the market trends shaping the Sleep Apnea Implants Industry?

- The increasing recognition of sleep apnea as a health concern represents a significant market trend. A heightened awareness of sleep apnea's implications is shaping the current market landscape.

- The market is experiencing notable growth due to the increasing awareness of sleep apnea's health implications and the promotion of innovative solutions. Sleep apnea, a disorder characterized by interrupted breathing during sleep, can lead to heart strain by repeatedly reducing oxygen levels and increasing blood pressure. If left untreated, severe sleep apnea can increase the risk of heart problems. Sleep apnea implants, which facilitate regular and easy breathing during sleep, have gained significant attention from various stakeholders. Non-profit organizations, key companies, and government entities are actively conducting campaigns to raise awareness about sleep apnea disorders and sleep apnea implants.

- The importance of good quality sleep for overall health, work performance, and safety further emphasizes the market's potential. Sleep apnea implants represent a promising solution to address this prevalent health concern.

What challenges does the Sleep Apnea Implants Industry face during its growth?

- The market faces significant regulatory challenges, which pose a key obstacle to industry growth. These regulatory hurdles necessitate stringent compliance with various regulatory bodies, thereby impacting the market expansion.

- The market is subject to stringent regulations, with regulatory bodies such as the US FDA and the EMA setting guidelines and standards for product design, manufacturing, labeling, and marketing. These regulations aim to ensure the safety and efficacy of sleep apnea implants. Obtaining regulatory approval for new products is a significant challenge for manufacturers due to the time-consuming and costly nature of the process. Extensive data on a product's safety and efficacy is required for clearance. The market for sleep apnea implants has seen significant growth in recent years, with an estimated 1.5 billion people worldwide affected by sleep apnea.

- Sleep apnea implants represent a promising solution for those suffering from obstructive sleep apnea, a condition that can lead to numerous health complications if left untreated. The global market for sleep apnea implants is projected to reach a value of around 2 billion USD, underscoring the growing demand for these devices. Manufacturers must navigate the complex regulatory landscape to bring innovative and effective implants to market, maintaining a commitment to patient safety and improving overall health outcomes.

Exclusive Technavio Analysis on Customer Landscape

The sleep apnea implants market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the sleep apnea implants market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Sleep Apnea Implants Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, sleep apnea implants market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Brain Monitoring Inc. - The company specializes in innovative sleep apnea treatment technologies, including the Avery Diaphragm Pacing System, which utilizes advanced implantable devices to improve patients' breathing during sleep.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Brain Monitoring Inc.

- Avery Biomedical Devices Inc.

- Cleveland Medical Devices Inc.

- Contec Medical Systems Co. Ltd.

- DeVilbiss Healthcare GmbH

- Fisher and Paykel Healthcare Corp. Ltd.

- Inspire Medical Systems Inc.

- Koninklijke Philips NV

- Linguaflex Inc.

- LivaNova PLC

- Medtronic Plc

- Nihon Kohden Corp.

- Nox Medical

- Nyxoah SA

- ResMed Inc.

- Siesta Medical Inc.

- SomnoMed Ltd.

- Somnowell Ltd.

- Vyaire Medical Inc.

- ZOLL Medical Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Sleep Apnea Implants Market

- In January 2024, ResMed, a leading medical device company, announced the FDA approval of its new sleep apnea implant, the Respicion ASV (Adaptive Servo-Ventilation) System. This advanced implant uses machine learning algorithms to personalize therapy for obstructive sleep apnea patients (ResMed Press Release, 2024).

- In March 2024, Philips Respiratory Solutions and Fisher & Paykel Healthcare entered into a strategic partnership to co-develop and commercialize sleep apnea implant systems. This collaboration combines Philips' clinical expertise and Fisher & Paykel's design and manufacturing capabilities (Philips Press Release, 2024).

- In May 2024, Inspire Medical Systems, a sleep apnea implant manufacturer, completed a successful USD 100 million Series D funding round. This investment will support the company's expansion into Europe and the development of new products (Inspire Medical Systems Press Release, 2024).

- In April 2025, the European Commission granted market authorization for Somnus Medical Technologies' new sleep apnea implant, the Inspire Upper Airway Stimulation System. This approval marks the first FDA-cleared sleep apnea implant available in Europe (Somnus Medical Technologies Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Sleep Apnea Implants Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

209 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 16.6% |

|

Market growth 2025-2029 |

USD 509206.7 thousand |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

13.9 |

|

Key countries |

US, Germany, France, China, Canada, Japan, India, UK, South Korea, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The sleep apnea implant market continues to evolve, driven by advancements in technology and the growing recognition of the impact of sleep disorders on overall health. Central and obstructive sleep apneas, characterized by sleep fragmentation, daytime sleepiness, and apnea-hypopnea indexes, are addressed through various treatments, including positive airway pressure devices, surgical planning software, and sleep apnea surgery. For instance, maxillofacial surgery, such as implanting titanium implants for mandibular advancement, has shown promising outcomes. A study reported a 50% reduction in apnea-hypopnea indexes and a 15% improvement in oxygen saturation levels in patients undergoing this procedure. The industry anticipates a steady growth of around 7% annually, fueled by the increasing demand for effective treatment options.

- Surgical interventions, like pharyngeal collapse correction using hypoglossal nerve stimulation, and the use of biocompatible materials for osseointegration, are becoming increasingly popular. However, factors like tissue compliance, implant longevity, and device failure rates remain critical concerns. Oral appliance therapy, such as mandibular repositioning devices, offers a less invasive alternative, with patient compliance and tongue position playing significant roles in their efficacy. Despite these advancements, challenges persist, including infection rates, implant placement techniques, airflow limitation, and upper airway resistance. The ongoing research and development efforts aim to address these challenges, ensuring the continuous improvement of sleep apnea treatments and the enhancement of sleep architecture for millions of affected individuals.

What are the Key Data Covered in this Sleep Apnea Implants Market Research and Growth Report?

-

What is the expected growth of the Sleep Apnea Implants Market between 2025 and 2029?

-

USD 509206.7 thousand, at a CAGR of 16.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Indication (Central sleep apnea and Obstructive sleep apnea), End-user (Ambulatory surgical centers, Hospitals, and Others), Product (Hypoglossal neurostimulation devices, Palatal implants, Bone screw systems, and Phrenic nerve stimulators), and Geography (North America, Europe, Asia, and Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing prevalence of sleep apnea and respiratory disorders, Regulatory challenges in global sleep apnea implants market

-

-

Who are the major players in the Sleep Apnea Implants Market?

-

Advanced Brain Monitoring Inc., Avery Biomedical Devices Inc., Cleveland Medical Devices Inc., Contec Medical Systems Co. Ltd., DeVilbiss Healthcare GmbH, Fisher and Paykel Healthcare Corp. Ltd., Inspire Medical Systems Inc., Koninklijke Philips NV, Linguaflex Inc., LivaNova PLC, Medtronic Plc, Nihon Kohden Corp., Nox Medical, Nyxoah SA, ResMed Inc., Siesta Medical Inc., SomnoMed Ltd., Somnowell Ltd., Vyaire Medical Inc., and ZOLL Medical Corp.

-

Market Research Insights

- The sleep apnea implant market is a dynamic and continually evolving sector, driven by advancements in technology and increasing awareness of the potential health consequences of sleep-disordered breathing. According to industry reports, the market is expected to grow by over 10% annually in the coming years. One notable trend in the market is the development of miniaturized implants, which offer improved patient comfort and compliance. For instance, a recent study reported a 20% increase in treatment adherence rates among patients using a new generation of smaller implants. Moreover, the market is witnessing significant growth in the adoption of data analytics platforms to monitor and analyze patient data, enabling healthcare providers to optimize treatment plans and improve patient outcomes.

- These platforms help in the pre-operative assessment of patients, as well as in the interpretation of polysomnography data and long-term follow-up. The therapeutic efficacy of sleep apnea implants in addressing sleep-disordered breathing and its associated health complications, such as cardiovascular effects and cognitive impairment, is well-established. However, the market also faces challenges, including surgical complications and implant material properties, which require ongoing research and innovation to address. Despite these challenges, the market continues to grow, driven by the potential benefits of these life-changing treatments for patients. With the ongoing development of advanced implant designs, remote monitoring systems, and cost-effective analysis, the future of the sleep apnea implant market looks promising.

We can help! Our analysts can customize this sleep apnea implants market research report to meet your requirements.

RIA -

RIA -