Disaster Recovery-as-a-service (draas) Market Size 2026-2030

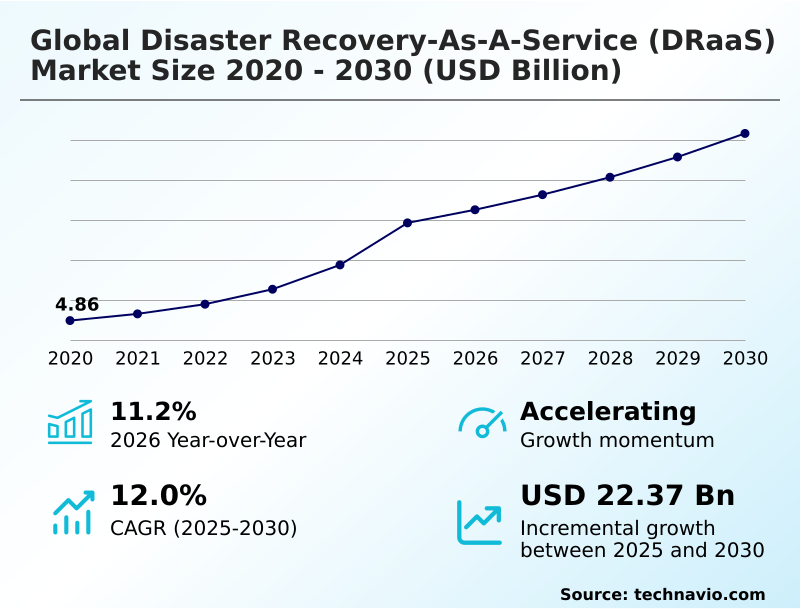

The disaster recovery-as-a-service (draas) market size is valued to increase by USD 22.37 billion, at a CAGR of 12% from 2025 to 2030. Digital transformation and cloud adoption as a foundation for business continuity will drive the disaster recovery-as-a-service (draas) market.

Major Market Trends & Insights

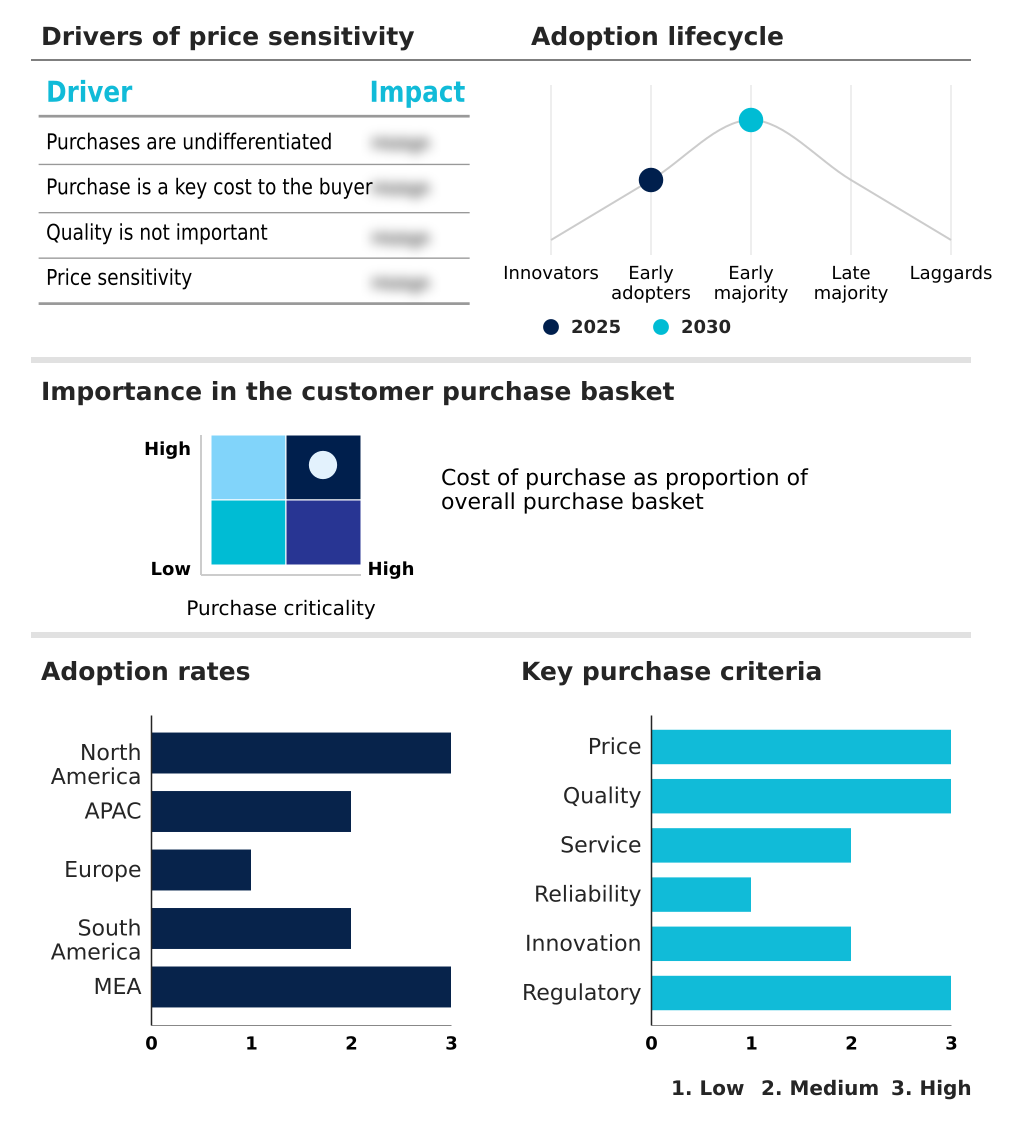

- APAC dominated the market and accounted for a 29.8% growth during the forecast period.

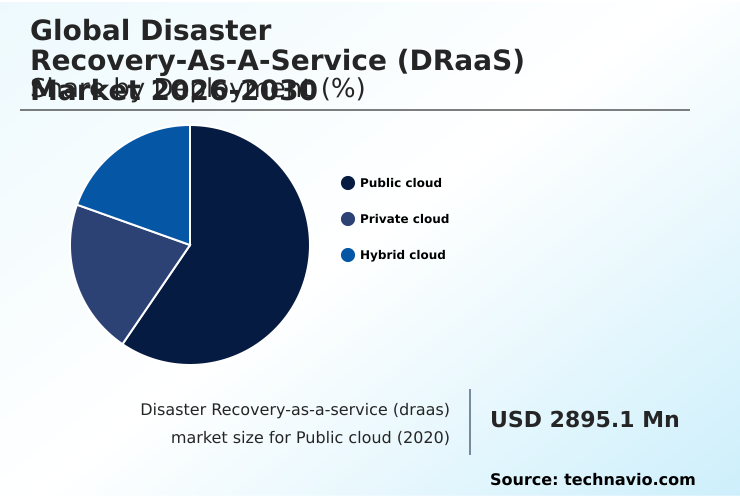

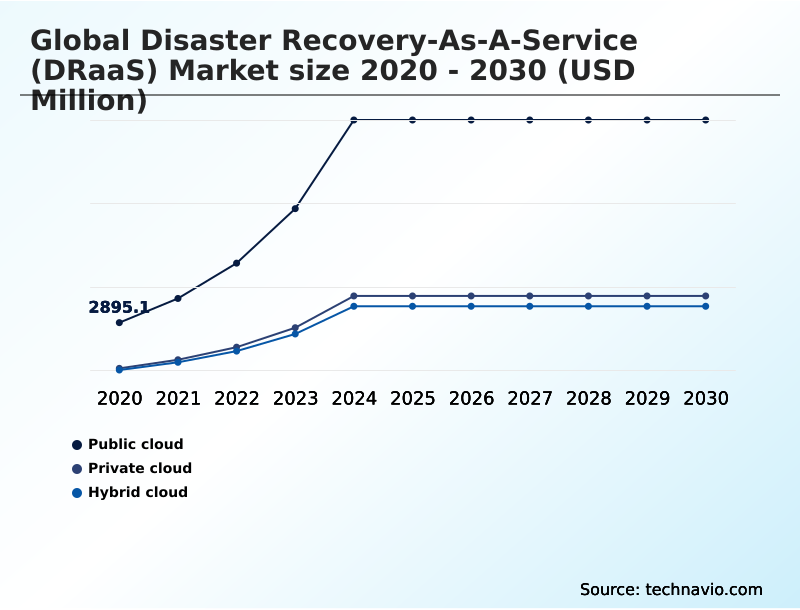

- By Deployment - Public cloud segment was valued at USD 11.22 billion in 2024

- By Service Type - Managed DRaaS segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 46.78 billion

- Market Future Opportunities: USD 22.37 billion

- CAGR from 2025 to 2030 : 12%

Market Summary

- The Disaster Recovery-as-a-Service (DRaaS) market is undergoing a significant transformation, moving beyond simple backup to become a cornerstone of enterprise resilience. Key market drivers include the widespread adoption of cloud-native architectures and the operational necessities of a distributed workforce, which demand sophisticated orchestration and high availability.

- A major trend is the integration of AI-driven cyber resilience, where predictive analytics are used to pre-empt system failures. At the same time, the market is shaped by the persistent challenge of ransomware mitigation, pushing providers to offer solutions like immutable storage and air-gapped immutable cloud vaults.

- For instance, a financial services firm, facing stringent regulatory requirements for data protection and operational continuity, may implement a zero-trust architecture for all recovery requests. This ensures that in the event of a breach, data is restored from a verified, untainted source within a clean room recovery environment, maintaining data integrity and compliance.

- This evolution highlights a shift from reactive recovery to a proactive, intelligent, and secure approach to business continuity.

What will be the Size of the Disaster Recovery-as-a-service (draas) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Disaster Recovery-as-a-service (draas) Market Segmented?

The disaster recovery-as-a-service (draas) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- Public cloud

- Private cloud

- Hybrid cloud

- Service type

- Managed DRaaS

- Assisted DRaaS

- Self-service DRaaS

- End-user

- Large enterprise

- SMEs

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- UK

- Germany

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Deployment Insights

The public cloud segment is estimated to witness significant growth during the forecast period.

The public cloud segment is central to the disaster recovery-as-a-service (DRaaS) market, offering inherent scalability and consumption-based pricing that eliminates large capital expenditures.

This model facilitates rapid deployment of resilient recovery solutions, allowing enterprises to leverage sophisticated orchestration for both failover and failback processes.

By using geographically dispersed regions, organizations can achieve robust data protection and maintain high availability, which is critical in today's digital economy.

The adoption of cloud-native recovery protocols within public cloud environments has improved recovery time objectives by over 30% for many firms.

This approach is key for maintaining operational continuity, especially for virtual desktop infrastructures that support a distributed workforce, and relies on automated runbooks to ensure consistency.

The Public cloud segment was valued at USD 11.22 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 29.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Disaster Recovery-as-a-service (draas) Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the disaster recovery-as-a-service market is defined by varied regional priorities and growth rates. North America remains the largest market, driven by mature cloud adoption and stringent regulations.

In contrast, the APAC region is the fastest-growing, expanding at 13.7% annually, fueled by rapid digitalization and the need to protect against both cyber threats and natural disasters.

Europe's market is heavily influenced by a focus on data sovereignty compliance and the demand for locally hosted recovery nodes.

The strategic need for power instabilities mitigation and protection against localized infrastructure failures is a significant factor in emerging markets across South America and Africa.

The adoption of hybrid solutions is common globally, with organizations leveraging policy-driven recovery to balance cost and performance across diverse geographic footprints.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- As organizations navigate increasingly complex digital ecosystems, the evolution of disaster recovery strategies has become paramount. Achieving compliance with data residency mandates in DRaaS is no longer a niche requirement but a standard for global operations, compelling a shift towards solutions that can guarantee data sovereignty. Concurrently, the challenge of managing DRaaS in hybrid cloud architectures demands advanced orchestration.

- The focus is now on achieving near-zero RTO and RPO with DRaaS, a goal made possible by automated failover triggers for workload migration. The threat of sophisticated cyberattacks has also redefined resilience, making ransomware mitigation using immutable storage a critical defense.

- This is often paired with clean room recovery for validated data restoration, ensuring that only untainted data is returned to production. A zero-trust architecture for recovery requests adds another layer of security. For businesses with advanced IT capabilities, using IaC for self-service DRaaS automation offers granular control, while others rely on managed clean room recovery services.

- We are also seeing specialized solutions emerge, such as assisted recovery for VMware environments and disaster recovery for virtual desktop infrastructures. Strategies now account for resilience against single-region cloud outages and protect backup repositories from targeted attacks. This comprehensive approach, which often includes AI-driven predictive analytics for system failures, ensures that organizations can maintain operations effectively.

- Firms that implement such tested, automated strategies report compliance audit pass rates more than double those of peers relying on outdated manual processes.

What are the key market drivers leading to the rise in the adoption of Disaster Recovery-as-a-service (draas) Industry?

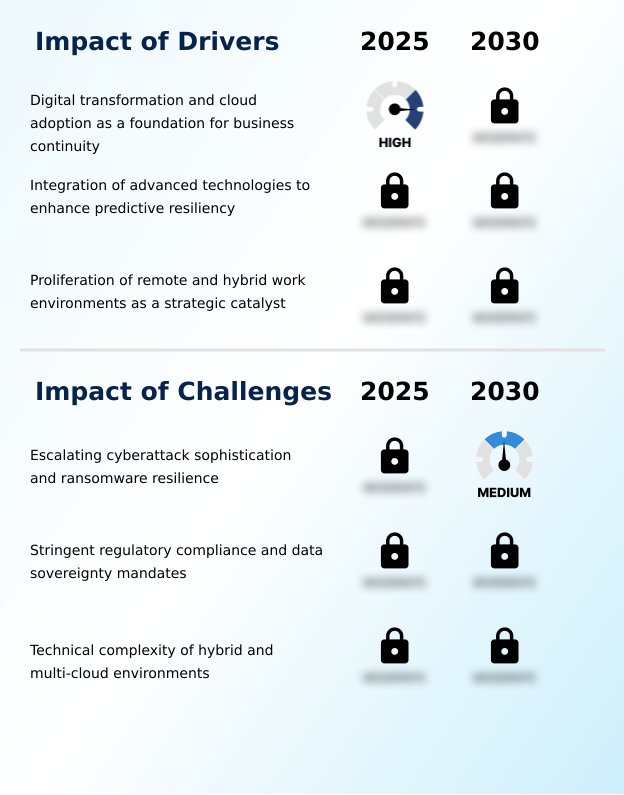

- Digital transformation and widespread cloud adoption serve as the foundational drivers for business continuity, propelling the growth of the disaster recovery-as-a-service market.

- The primary driver for the disaster recovery-as-a-service market is the enterprise-wide push for digital transformation and cloud adoption as core pillars of business continuity.

- As organizations transition from on-premises data centers to cloud-native architectures, the demand for specialized, resilient recovery solutions has surged.

- This shift allows businesses to move from a capital expenditure model to a more flexible operational expenditure model, reducing infrastructure overhead by up to 30%.

- The proliferation of remote and hybrid work environments has also catalyzed market growth, as a distributed workforce relies on the high availability of virtual desktop infrastructures and cloud applications.

- Ensuring operational continuity for a remote workforce has become a top priority, with downtime costs increasing by 25% year-over-year for many firms.

What are the market trends shaping the Disaster Recovery-as-a-service (draas) Industry?

- The integration of AI and ML for predictive resilience is an emerging market trend. This shift enables the proactive identification of potential system failures before they escalate into disasters.

- Key trends in the disaster recovery-as-a-service market are centered on proactive and intelligent resilience. The integration of AI and machine learning into recovery frameworks allows for predictive analytics that can identify potential system failures before they occur, improving threat detection accuracy by over 40%. This shift from reactive to proactive strategies is critical for managing complex, distributed environments.

- Another major trend is the focus on ransomware mitigation through technologies like immutable storage and clean room recovery, which ensures that restored data is free from malware. Organizations adopting immutable backups have reported a near-100% success rate in data restoration following an attack.

- The move towards multi-cloud strategies also drives the need for sophisticated orchestration and automated runbooks to ensure seamless failover across different platforms.

What challenges does the Disaster Recovery-as-a-service (draas) Industry face during its growth?

- The escalating sophistication of cyberattacks and the challenge of ensuring ransomware resilience present significant obstacles to industry growth.

- The disaster recovery-as-a-service market faces significant challenges from the escalating sophistication of cyber threats and the complexity of modern IT environments. Ransomware attacks now frequently target backup repositories, forcing providers to innovate with air-gapped storage and immutable data vaulting.

- The technical complexity of managing disaster recovery across hybrid and multi-cloud architectures is another major hurdle, where incompatible replication technologies can increase recovery times by over 50% if not properly orchestrated. Furthermore, navigating stringent regulatory frameworks and data residency mandates adds another layer of complexity.

- Failure to meet these compliance standards, which often require documented and tested recovery plans, can result in significant financial penalties, making robust compliance-mapping tools and automated runbooks essential.

Exclusive Technavio Analysis on Customer Landscape

The disaster recovery-as-a-service (draas) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the disaster recovery-as-a-service (draas) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Disaster Recovery-as-a-service (draas) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, disaster recovery-as-a-service (draas) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

11 11 Systems Inc. - Provides integrated data protection and disaster recovery solutions, ensuring robust cybersecurity and scalable backup for modern cloud and hybrid environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 11 11 Systems Inc.

- Acronis International GmbH

- Amazon Web Services Inc.

- Arcserve USA LLC

- Carbonite Inc.

- Commvault Systems Inc.

- Datto Holdings Corp.

- Druva Inc.

- Flexential Corp.

- Google LLC

- Hewlett Packard Enterprise Co.

- IBM Corp.

- Infrascale Inc.

- Lumen Technologies Inc.

- Microsoft Corp.

- Nippon Telegraph and Corp.

- Recovery Point Systems Inc.

- TierPoint LLC

- Veeam Software Group GmbH

- VMware Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Disaster recovery-as-a-service (draas) market

- In October 2024, Cohesity and 11:11 Systems expanded their partnership to introduce a managed Clean Room Recovery service, providing an isolated environment for secure data validation and ransomware response.

- In December 2024, Dell Technologies enhanced its PowerProtect portfolio with advanced machine learning capabilities to accelerate data recovery and improve the detection of sophisticated cyber threats in hybrid environments.

- In January 2025, Veeam Software released its new Data Platform, which incorporates advanced forensic analysis tools and intelligent automation to help organizations counter emerging data security threats.

- In March 2025, Microsoft deployed its Azure Site Recovery and Azure Local solutions for Publix Employees Federal Credit Union, significantly reducing virtual machine recovery times and enhancing resilience against regional disruptions.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Disaster Recovery-as-a-service (draas) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 296 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 12% |

| Market growth 2026-2030 | USD 22367.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 11.2% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Singapore, Australia, UK, Germany, France, The Netherlands, Spain, Italy, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Egypt and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Disaster Recovery-as-a-Service (DRaaS) market has matured from a simple backup function to a strategic imperative for ensuring enterprise resilience. The core of this evolution is the shift toward AI-driven cyber resilience and the adoption of cloud-native architectures. Businesses now demand sophisticated orchestration to manage complex, distributed environments, making high availability and effective failover and failback processes standard expectations.

- This trend is directly influencing boardroom decisions around cybersecurity insurance, as implementing advanced data protection measures like immutable storage and clean room recovery can significantly lower premiums. The market's technical landscape is defined by the integration of predictive analytics and automated failover triggers, which reduce human error during a crisis by up to 60%.

- As ransomware mitigation becomes a primary concern, features such as immutable data vaulting and zero-trust architectures are no longer optional. This push toward intelligent workload migration and resilient recovery solutions demonstrates that maintaining operational continuity in the face of both cyber threats and infrastructure failures is the market's fundamental value proposition.

What are the Key Data Covered in this Disaster Recovery-as-a-service (draas) Market Research and Growth Report?

-

What is the expected growth of the Disaster Recovery-as-a-service (draas) Market between 2026 and 2030?

-

USD 22.37 billion, at a CAGR of 12%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Public cloud, Private cloud, and Hybrid cloud), Service Type (Managed DRaaS, Assisted DRaaS, and Self-service DRaaS), End-user (Large enterprise, and SMEs) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Digital transformation and cloud adoption as a foundation for business continuity, Escalating cyberattack sophistication and ransomware resilience

-

-

Who are the major players in the Disaster Recovery-as-a-service (draas) Market?

-

11 11 Systems Inc., Acronis International GmbH, Amazon Web Services Inc., Arcserve USA LLC, Carbonite Inc., Commvault Systems Inc., Datto Holdings Corp., Druva Inc., Flexential Corp., Google LLC, Hewlett Packard Enterprise Co., IBM Corp., Infrascale Inc., Lumen Technologies Inc., Microsoft Corp., Nippon Telegraph and Corp., Recovery Point Systems Inc., TierPoint LLC, Veeam Software Group GmbH and VMware Inc.

-

Market Research Insights

- The dynamics of the disaster recovery-as-a-service market are increasingly shaped by a focus on proactive and verifiable resilience. Organizations are adopting assisted recovery services to achieve sub-minute recovery time objectives, a metric that has become a competitive differentiator.

- The implementation of zero-trust recovery protocols has been shown to reduce unauthorized recovery attempts by over 90%, a critical factor for securing hybrid-IT environments. Furthermore, firms utilizing managed cyber-resilience services restore critical operations 75% faster than those with self-managed plans. The move toward sovereign cloud recovery is also gaining traction as data sovereignty compliance becomes a non-negotiable boardroom issue.

- This is complemented by policy-driven recovery automation, which minimizes manual error and ensures consistent execution during a crisis.

We can help! Our analysts can customize this disaster recovery-as-a-service (draas) market research report to meet your requirements.

RIA -

RIA -