Disposable Incontinence Products Market Size 2024-2028

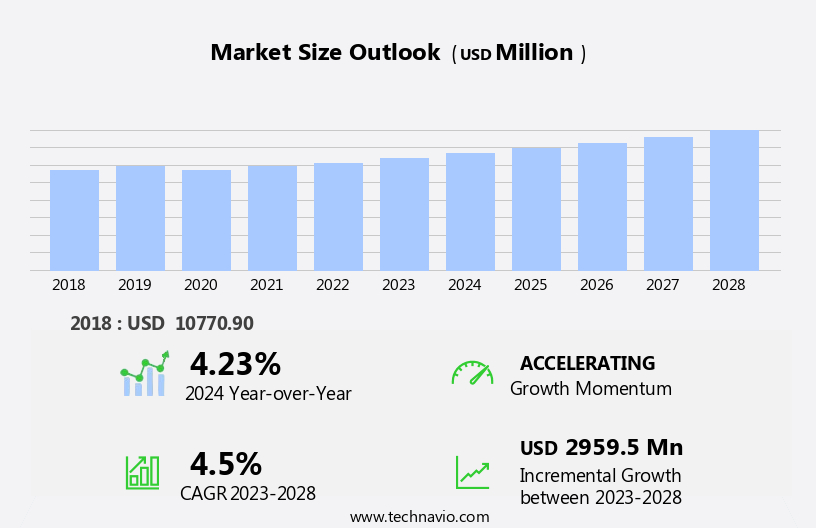

The disposable incontinence products market size is forecast to increase by USD 2.96 billion, at a CAGR of 4.5% between 2023 and 2028.

- The market is driven by the growing prevalence of physical and medical conditions resulting in urinary incontinence. This trend is expected to continue due to the increasing aging population and the rising incidence of chronic diseases, such as diabetes and neurological disorders. Product innovations are another key driver, as manufacturers introduce new and improved products to cater to diverse consumer needs and preferences. However, the market faces challenges from fluctuating raw material prices, which can impact profitability and product affordability.

- Companies must navigate these price fluctuations by implementing effective cost management strategies and exploring alternative raw material sources. To capitalize on market opportunities and navigate challenges effectively, strategic business decisions and operational planning should focus on product innovation, cost management, and supply chain optimization.

What will be the Size of the Disposable Incontinence Products Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, with innovations and advancements shaping its dynamics. Latex-free materials are increasingly utilized in the production of adult incontinence pads, ensuring accessibility for those with allergies or sensitivities. Hypoallergenic materials and moisture-wicking fabrics are integrated into soft, breathable topsheets, enhancing user comfort. Fluid retention capacity remains a crucial factor, with adjustable waistbands and pull-on pants catering to various user needs. Incontinence liners, equipped with wetness indicators and reliable containment systems, offer discreet solutions for light incontinence. Breathable outer layers and leak protection layers ensure both comfort and protection. Incontinence briefs feature tape closure systems and high absorbency cores, while reduced friction materials and elastic leg cuffs provide a secure fit.

Refastenable tapes and superabsorbent materials ensure optimal absorbency, while skin barrier creams and odor control technology maintain skin health and hygiene. Leak guards and comfort fit designs, featuring cloth-like surfaces and improved absorbency rates, offer enhanced comfort features. Odor neutralizers and reliable containment systems ensure peace of mind for users. Absorbent polymers and leg gathers contribute to enhanced breathability, catering to the evolving needs of the market.

How is this Disposable Incontinence Products Industry segmented?

The disposable incontinence products industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

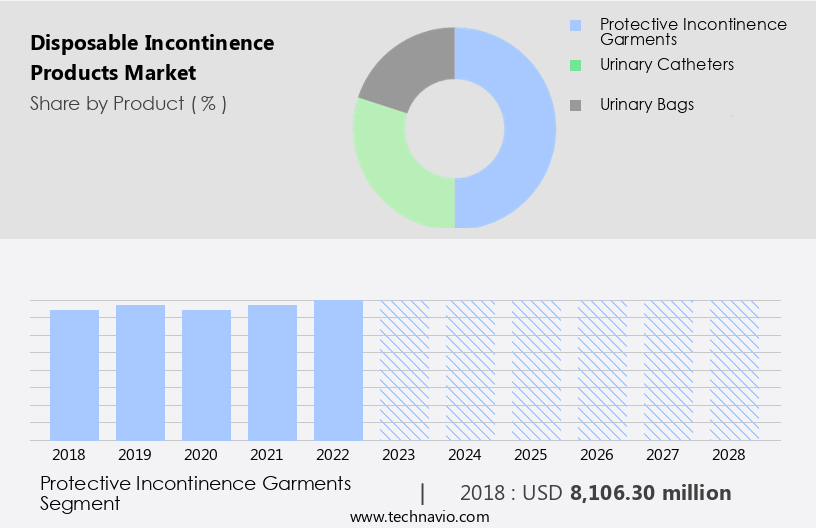

- Protective incontinence garments

- Urinary catheters

- Urinary bags

- Geography

- North America

- US

- Canada

- Europe

- Germany

- Italy

- APAC

- China

- Rest of World (ROW)

- North America

By Product Insights

The protective incontinence garments segment is estimated to witness significant growth during the forecast period.

The market encompasses a range of garments designed to collect urine and prevent leakage, including disposable underwear, panty shields, diapers, and other protective garments. In 2023, the protective incontinence garments segment dominated the market, driven by the growing geriatric population with medical conditions such as severe incontinence, diarrhea, mobility impairment, or dementia. Urbanization and heightened awareness of health and hygiene are also contributing factors. These garments are primarily made from medical-grade nonwovens, derived from fabrics like cotton, linen, or synthetic materials such as polypropylene and PTFE, which bond together to create a waterproof structure. Hospitals and medical centers utilize these diapers due to their leak prevention capabilities and comfort.

Additionally, the market trends toward hypoallergenic materials, moisture-wicking fabrics, soft breathable topsheets, high absorbency cores, and reduced friction materials. Comfort fit designs, cloth-like surfaces, and improved absorbency rates further enhance consumer appeal. Skin health materials, such as skin barrier creams and odor neutralizers, ensure user comfort and prevent skin irritation. Reliable containment systems, absorbent polymers, and leak guards provide enhanced protection. Incontinence liners, pull-on pants, adjustable waistbands, refastenable tapes, elastic leg cuffs, and tape closure systems cater to various user preferences. Enhanced breathability and leak protection layers are essential features in the market's evolution.

The Protective incontinence garments segment was valued at USD 8.11 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

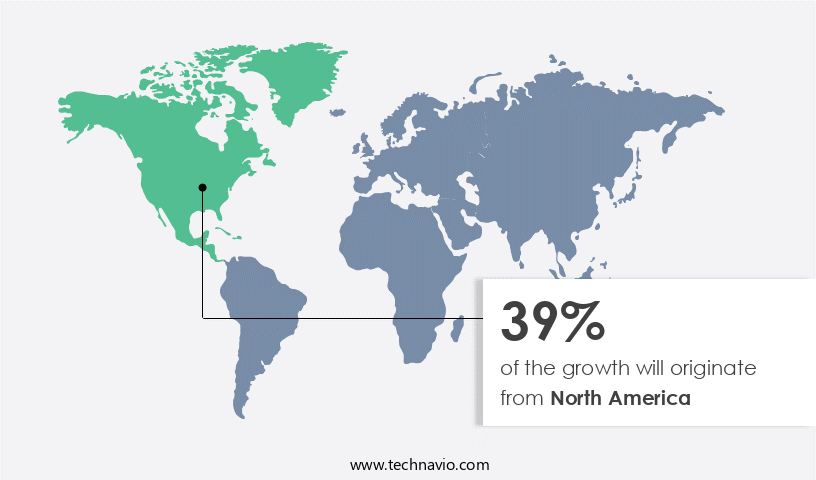

North America is estimated to contribute 39% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the North American market, disposable incontinence products experienced notable growth in 2023. Factors fueling this expansion included the aging population, heightened urinary incontinence diagnoses, escalating healthcare expenditures, rising diabetes cases, and increasing instances of urinary tract infections and pregnancies. Furthermore, the proliferation of urology specialized hospitals and clinics, as well as the emergence of both global and local companies, contributed to market growth. Additionally, the expansion of product offerings catering to specific consumer needs and the increasing disposable income of consumers were significant driving forces. The market's evolution showcased a focus on latex-free materials, hypoallergenic components, moisture-wicking fabrics, soft, breathable topsheets, and high fluid retention capacity.

Adjustable waistbands, pull-on pants, incontinence liners, and tape closure systems were popular choices, while incontinence briefs, leak guards, and improved absorbency rates were also in demand. Comfort fit designs, skin health materials, reliable containment systems, and odor control technology were essential features, ensuring enhanced comfort and protection. Disposable underpads, odor neutralizers, and absorbent polymers were also integral components of the market's offerings. Leg gathers and enhanced breathability further improved product functionality, making disposable incontinence products a vital solution for individuals requiring discreet, effective, and comfortable solutions.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Disposable Incontinence Products Industry?

- The increasing prevalence of physical and medical conditions, such as stroke, multiple sclerosis, and diabetes, is the primary driver of the market for urinary incontinence solutions, due to the significant impact these conditions have on individuals' bladder control.

- Disposable incontinence products, including underpads and adult diapers, cater to the growing need for reliable containment systems among individuals experiencing urinary incontinence. This condition, prevalent among older adults due to weakened pelvic and bladder muscles, affects millions worldwide. Neurological disorders such as Parkinson's disease, diabetes, arthritis, spinal injury, pregnancy, and menopause can also cause urinary incontinence by damaging the nerves responsible for bladder control. The aging population's significant presence in both developed and developing countries fuels the demand for these products.

- Enhanced features like odor neutralizers, absorbent polymers, and leg gathers contribute to the market's growth. Furthermore, the emphasis on enhanced breathability ensures user comfort, making disposable incontinence products an essential health and hygiene solution. The increasing prevalence of urinary incontinence, coupled with the advancements in product technology, is expected to drive market growth during the forecast period.

What are the market trends shaping the Disposable Incontinence Products Industry?

- Product innovations are currently shaping the market trend. It is essential for businesses to stay informed and adapt to the latest advancements in order to remain competitive.

- Disposable incontinence products have gained significant attention due to the increasing demand for more comfortable and effective solutions. companies continue to innovate, introducing products made with latex-free materials and hypoallergenic components to cater to sensitive skin. Moisture-wicking fabrics and soft, breathable topsheets enhance comfort and promote skin health. Product advancements include adjustable waistbands and pull-on pants, offering a more secure and discreet fit. Incontinence liners have also evolved, featuring superior fluid retention capacity and odor control. Traditional pads made of synthetic materials have been surpassed by these new offerings.

- One notable innovation is the magnetic pantyliner, which effectively neutralizes odors and is less harmful to the vaginal skin due to its non-chlorine bleaching process. These advancements contribute to the growing popularity of disposable incontinence products, providing consumers with increased comfort, reliability, and peace of mind.

What challenges does the Disposable Incontinence Products Industry face during its growth?

- The volatility of raw material prices poses a significant challenge to the industry's growth trajectory.

- Disposable incontinence products, including adult diapers and briefs, are manufactured using various raw materials such as fluff pulp, superabsorbent polymer, polypropylene polymer, elastic film, polypropylene fiber, polyester fiber, biocomponent fiber, rayon/lyocell fiber, and cotton. Petroleum-based raw materials, like polyethylene plastic, are also utilized in the production process. The cost of these materials is influenced by the volatility of petroleum prices, which in turn affects the transportation expenses of raw materials and finished goods. An escalation in transportation costs eventually leads to an increase in the final product's price. However, due to the highly competitive market landscape, companies are unable to pass on these price hikes to consumers, thereby compressing their profit margins.

- Key features of these products include wetness indicators, breathable outer layers, leak protection layers, tape closure systems, high absorbency cores, reduced friction materials, elastic leg cuffs, and refastenable tapes. These attributes cater to the comfort, convenience, and effectiveness requirements of consumers.

Exclusive Customer Landscape

The disposable incontinence products market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the disposable incontinence products market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, disposable incontinence products market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABENA AS - The company specializes in disposable incontinence products, utilizing advanced wetlaid nonwoven technology for sterile barrier systems (SBS).

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABENA AS

- Ahlstrom Munksjo Oyj

- Asahi Kasei Corp.

- Berry Global Inc.

- Cardinal Health Inc.

- ConvaTec Group Plc

- Domtar Corp.

- First Quality Enterprises Inc.

- Fujian Time and Tianhe Industrial Co. Ltd.

- Gottlieb Binder GmbH and Co. KG

- Kimberly Clark Corp.

- Koch Industries Inc.

- Kyna Healthcare Pvt. Ltd.

- Medline Industries LP

- New Yifa Group

- Oji Holdings Corp.

- Ontex BV

- Paul Hartmann AG

- Unicharm Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Disposable Incontinence Products Market

- In January 2024, major strategic collaboration was announced between leading diaper manufacturer, Kimberly-Clark, and healthcare technology company, Philips, to integrate Philips' smart sensors into Kimberly-Clark's diapers, creating a new generation of connected incontinence products (Kimberly-Clark press release).

- In March 2024, Ontex, a European producer of hygiene products, acquired the adult incontinence business of SCA Hygiene for ⬠810 million, significantly expanding its market share and product portfolio in the adult incontinence segment (Ontex press release).

- In April 2025, Tena, a subsidiary of Essity, received regulatory approval from the European Commission for its new line of eco-friendly, plant-based incontinence products, marking a significant step towards sustainable solutions in the market (Essity press release).

- In May 2025, Molnlycke Health Care, a Swedish medical solutions company, launched its new line of advanced wound care incontinence products, featuring a unique combination of super-absorbent polymers and antimicrobial technology, addressing the growing demand for advanced incontinence solutions (Molnlycke Health Care press release).

Research Analyst Overview

- The market is characterized by the utilization of diverse materials and technologies to enhance product performance and end-user comfort. Top sheet materials, such as perforated layers and skin-friendly fabrics, facilitate moisture wicking through wicking channels and odor absorption using odor-absorbing polymers. Regulatory compliance is paramount, with product testing standards ensuring quality assurance metrics, such as leakage protection and durability. Manufacturing processes employ non-woven materials and low-profile designs to create elastic leg openings and reinforced side panels. Back sheet materials, often featuring sap technology and an acquisition distribution layer, optimize product adhesion and moisture management. High-capacity cores and refastenable closures cater to varying user needs.

- Tapes and fasteners secure the product in place, while manufacturing processes prioritize sustainability and cost efficiency. Packaging design plays a crucial role in product differentiation and user convenience. Overall, the market continues to evolve, with innovation in material composition, regulatory compliance, and product performance driving growth.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Disposable Incontinence Products Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

134 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.5% |

|

Market growth 2024-2028 |

USD 2959.5 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.23 |

|

Key countries |

US, China, Germany, Canada, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Disposable Incontinence Products Market Research and Growth Report?

- CAGR of the Disposable Incontinence Products industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the disposable incontinence products market growth of industry companies

We can help! Our analysts can customize this disposable incontinence products market research report to meet your requirements.

RIA -

RIA -