Distributed AI Computing Market Size 2025-2029

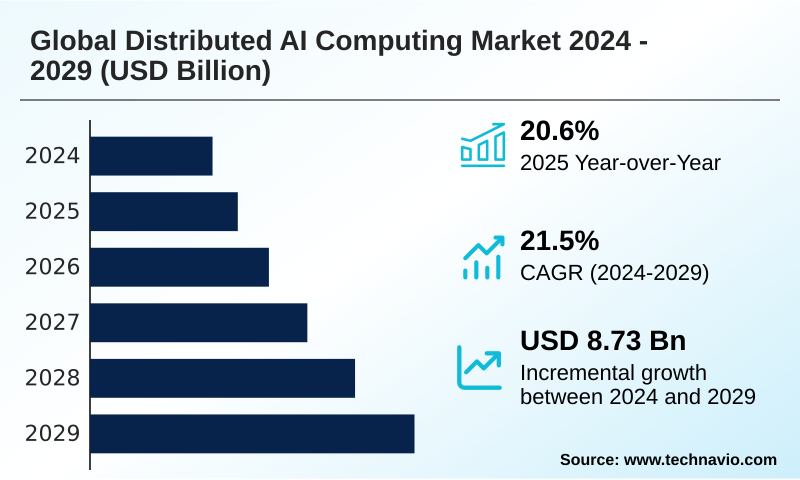

The distributed ai computing market size is valued to increase by USD 8.73 billion, at a CAGR of 21.5% from 2024 to 2029. Proliferation of generative AI and Large Language Models (LLM) demands unprecedented computational scale will drive the distributed ai computing market.

Major Market Trends & Insights

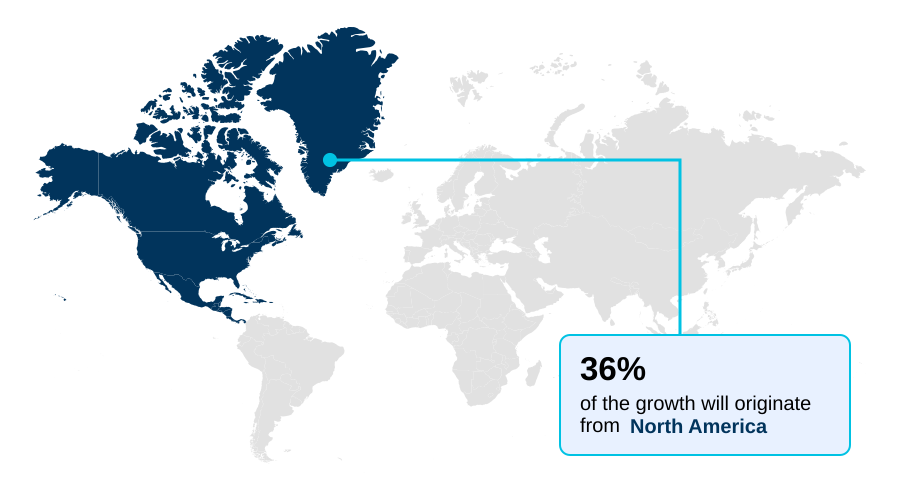

- North America dominated the market and accounted for a 36.1% growth during the forecast period.

- CAGR from 2024 to 2029 : 21.5%

Market Summary

- The distributed AI computing market is defined by its architectural shift away from centralized processing toward decentralized, interconnected nodes. This paradigm enables the execution of AI workloads across cloud servers, on-premises data centers, and edge devices, facilitating parallel processing and enhanced scalability.

- A key driver is the expansion of IoT, where real-time analytics and predictive maintenance demand low-latency communication that centralized models cannot provide. In a business scenario, a logistics company uses on-device AI for real-time decision making in its warehouses, optimizing routes for autonomous systems and improving operational efficiency.

- A defining trend is the move toward a hybrid AI model and the edge-to-cloud continuum, where workload orchestration is managed by an MLOps platform. This approach uses techniques like model quantization to run sophisticated AI on resource-constrained devices. However, this distribution introduces challenges in data governance and system integration.

- Organizations must navigate the complexity of managing a heterogeneous computational infrastructure while ensuring security, a critical factor for successful digital transformation initiatives and achieving scalable AI infrastructure across the enterprise.

What will be the Size of the Distributed AI Computing Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Distributed AI Computing Market Segmented?

The distributed ai computing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029.

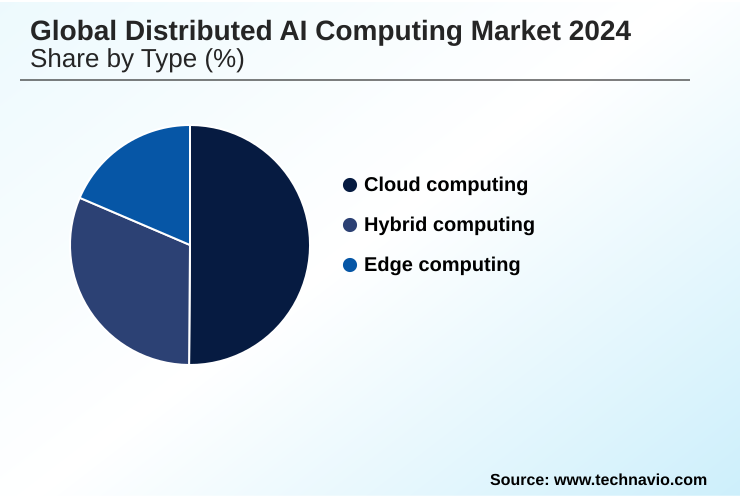

- Type

- Cloud computing

- Hybrid computing

- Edge computing

- Software

- TensorFlow

- PyTorch

- ONNX

- Application

- Predictive analytics

- Natural language processing

- Autonomous systems

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Type Insights

The cloud computing segment is estimated to witness significant growth during the forecast period.

The cloud computing segment provides the foundational computational infrastructure for the distributed AI computing market. It enables organizations to execute large-scale distributed training and complex model inference without incurring prohibitive hardware investment.

This architecture is essential for developing sophisticated autonomous systems, where vast datasets are processed using parallel computing techniques. Modern platforms leverage AI accelerator resources and methods like knowledge distillation for AI model optimization.

By utilizing scalable cloud resources for tasks like AI workload partitioning, organizations can achieve significant efficiencies, with some reporting a reduction in model training times by up to 60%.

This approach supports both real-time decision making and the underlying processes of distributed machine learning and federated averaging.

Regional Analysis

North America is estimated to contribute 36.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Distributed AI Computing Market Demand is Rising in North America Get Free Sample

The geographic landscape of the distributed AI computing market is characterized by distinct regional priorities and growth trajectories.

North America, contributing over 36% of the market's incremental growth, leads in foundational model development, leveraging its robust ecosystem of cloud-native services and advanced tensor processing unit infrastructure.

Europe is concentrating on industrial applications, deploying edge AI for predictive maintenance and collaborative robotics, driven by data sovereignty regulations.

In APAC, which is forecast to be the fastest-growing region, the focus is on smart city projects and scalable AI infrastructure, with widespread adoption of distributed data processing for public services.

Emerging applications in South America and the Middle East, such as remote patient monitoring and smart grid management, showcase the technology's expanding global footprint.

Across all regions, data preprocessing at the edge and on-premises AI deployment are becoming standard practices to enhance efficiency.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic implementation of distributed AI is becoming a critical differentiator for businesses. Evaluating the benefits of federated learning in healthcare reveals a clear path to developing robust predictive models without compromising patient data privacy, a significant advantage over centralized training methods.

- However, enterprises must assess the cost of on-device AI model deployment, which involves not just hardware but also specialized talent. In industrial sectors, distributed AI for predictive maintenance is a primary use case, though success depends on overcoming security risks in edge AI networks.

- Financial services firms are exploring the hybrid AI model for financial services to balance low-latency fraud detection with large-scale risk analytics. For autonomous systems, addressing edge AI latency in autonomous driving is paramount for safety and reliability.

- Successfully scaling MLOps for distributed systems requires a sophisticated approach to optimizing workload orchestration in AI and managing resource allocation in distributed computing, a challenge that is more complex than in centralized environments. This is evident as organizations deploying distributed machine learning frameworks see a nearly 2x increase in management overhead compared to monolithic systems.

- The rise of on-device generative AI use cases and TinyML for industrial IoT sensors is pushing the boundaries of what is possible on resource-constrained hardware. Concurrently, data governance in distributed AI and the challenges in hybrid AI implementation require careful architectural planning to ensure compliance and maintainability.

What are the key market drivers leading to the rise in the adoption of Distributed AI Computing Industry?

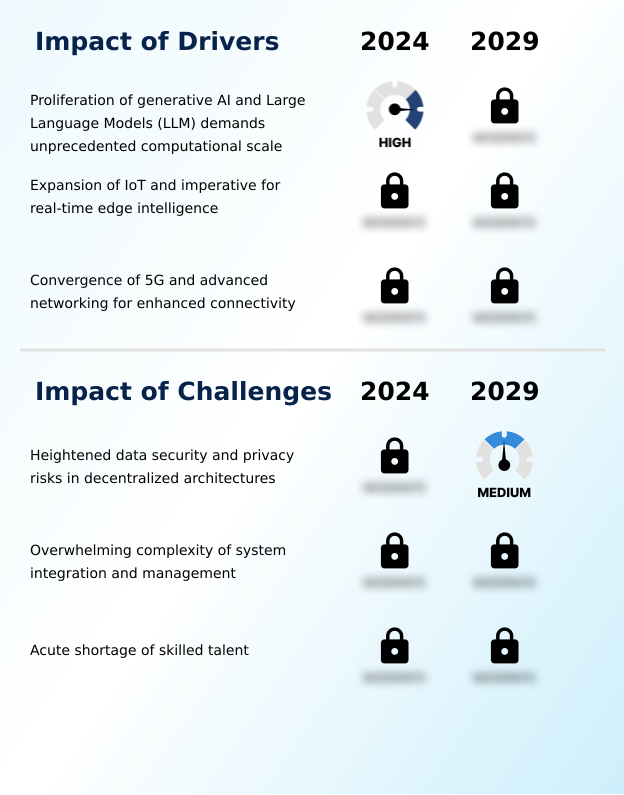

- The proliferation of generative AI and large language models (LLMs) is a key market driver, demanding unprecedented computational scale that only distributed architectures can provide.

- The market's primary driver is the demand for real-time intelligence at scale. The expansion of IoT and industrial automation fuels the need for real-time analytics and intelligent automation, where decisions must be made in milliseconds.

- This is enabled by a robust computational infrastructure that combines powerful AI accelerators for parallel processing with advanced, low-latency communication networks like 5G, which provide 99.9% reliability.

- In sectors like manufacturing and logistics, this translates to smart factory integration and the operation of autonomous mobility platforms. For instance, AI-powered computer vision systems on production lines can identify defects with greater than 98% accuracy.

- This convergence of technologies is also critical for emerging applications like smart grid management, where distributed intelligence is essential for optimizing energy distribution and ensuring grid stability.

What are the market trends shaping the Distributed AI Computing Industry?

- A strategic shift toward a hybrid AI and edge-to-cloud continuum is emerging as a defining market trend. This approach treats edge and cloud as a fluid computational spectrum for intelligent workload allocation.

- Key market trends are converging around efficiency and privacy. The strategic shift toward a hybrid AI model reflects a maturation from a simple cloud-versus-edge debate to a sophisticated edge-to-cloud continuum. This hybrid computing approach allows for intelligent partitioning of tasks, with on-device AI handling immediate processing while the cloud manages intensive training.

- This is amplified by the proliferation of on-device generative AI, made possible by advanced model quantization techniques that reduce model sizes by up to 75%. Furthermore, the rise of federated learning as a leading form of privacy-preserving AI is critical, especially in regulated industries.

- By training on decentralized data, organizations can improve model accuracy without centralizing sensitive information, unlocking new TinyML applications while adhering to strict data policies.

What challenges does the Distributed AI Computing Industry face during its growth?

- Heightened data security and privacy risks inherent in decentralized architectures present a key challenge to industry growth and adoption.

- The primary challenges in the market stem from operational complexity and security vulnerabilities. The decentralized nature of the network architecture creates an expanded attack surface, with some analyses suggesting a 500% increase in potential entry points compared to centralized systems, complicating data governance.

- System integration is another significant hurdle, as orchestrating a heterogeneous mix of hardware and software requires a sophisticated MLOps platform and expertise in AI algorithm deployment. Managing MLOps for edge environments is particularly difficult, as it involves continuous monitoring and updating of models on thousands of resource-constrained devices.

- This complexity is compounded by a severe talent shortage, with hiring cycles for engineers skilled in workload orchestration and secure multi-party computation often exceeding 120 days, slowing down digital transformation initiatives.

Exclusive Technavio Analysis on Customer Landscape

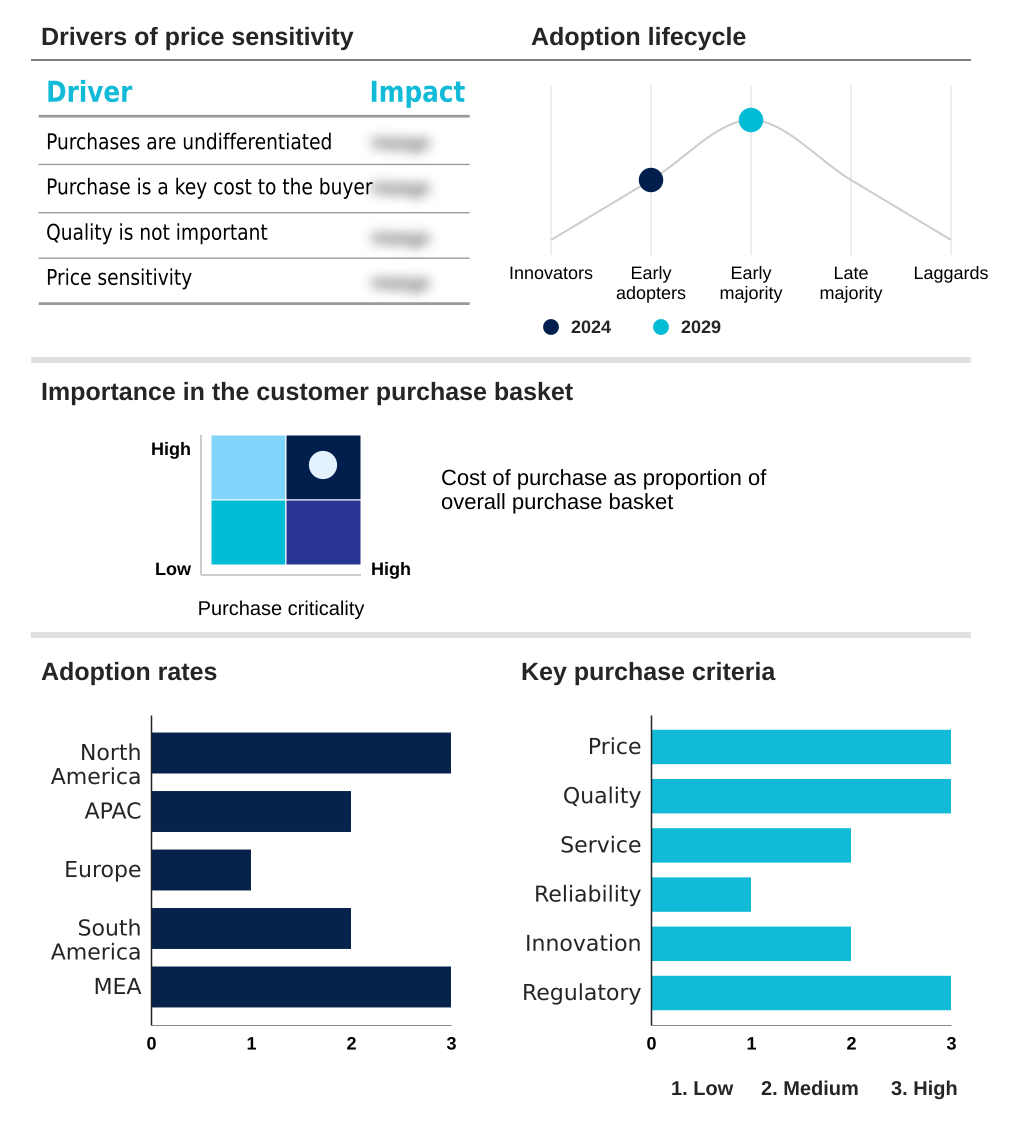

The distributed ai computing market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the distributed ai computing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Distributed AI Computing Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, distributed ai computing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Micro Devices Inc. - The company delivers specialized GPU and CPU architectures optimized for parallel processing, enabling scalable, large-scale distributed AI computing workloads for advanced enterprise applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Micro Devices Inc.

- Alibaba Cloud

- Amazon.com Inc.

- Baidu Inc.

- Fujitsu Ltd.

- Google LLC

- Graphcore Ltd.

- Hewlett Packard

- Huawei Technologies Co. Ltd.

- Infosys Ltd.

- Intel Corp.

- IBM Corp.

- Meta Platforms Inc.

- Microsoft Corp.

- NEC Corp.

- NVIDIA Corp.

- Oracle Corp.

- Samsung Electronics Co. Ltd.

- SAP SE

- Siemens AG

- Tencent Holdings Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Distributed ai computing market

- In September 2024, A leading European automotive consortium launched a cross-border initiative to standardize federated learning protocols for developing advanced driver-assistance systems (ADAS), aiming to improve vehicle safety without centralizing sensitive driving data.

- In January 2025, A major cloud service provider unveiled a new suite of tools for its distributed cloud platform, specifically designed to simplify MLOps for hybrid AI models, reducing deployment complexity by an estimated 40% for enterprise users.

- In March 2025, The South Korean government announced plans to establish a USD 34 billion fund to support companies in strategic technology sectors, including semiconductors and AI, to bolster its sovereign capabilities.

- In May 2025, Qualcomm announced its latest AI Engine offers native, hardware-accelerated support for a wider range of ONNX operators, improving efficiency for complex models on battery-powered mobile platforms.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Distributed AI Computing Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 289 |

| Base year | 2024 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 21.5% |

| Market growth 2025-2029 | USD 8733.7 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 20.6% |

| Key countries | US, Canada, Mexico, China, India, Japan, Australia, South Korea, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The distributed AI computing market is driven by the imperative to process data closer to its source, fundamentally reshaping computational infrastructure. The adoption of a hybrid AI model, which intelligently partitions workloads between the cloud and edge, is now a mainstream strategy.

- This is enabled by federated learning and other techniques for handling decentralized data, allowing for complex model inference and distributed training without centralizing sensitive information. Key components facilitating this shift include the neural processing unit and the tensor processing unit, which serve as powerful AI accelerators for both on-device AI and large-scale parallel processing.

- Managing these complex ecosystems requires a sophisticated MLOps platform for continuous workload orchestration, deployment, and robust data governance. For boardroom consideration, the choice of network architecture directly impacts the efficacy of low-latency communication, a critical factor for real-time analytics in autonomous systems. For example, systems leveraging optimized architectures have demonstrated a 30% reduction in decision-making latency.

- As models become more complex, techniques like model quantization, knowledge distillation, and efficient data preprocessing, managed through a high-performance inference engine, are essential for deploying AI on resource-constrained devices for applications such as predictive maintenance.

What are the Key Data Covered in this Distributed AI Computing Market Research and Growth Report?

-

What is the expected growth of the Distributed AI Computing Market between 2025 and 2029?

-

USD 8.73 billion, at a CAGR of 21.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Cloud computing, Hybrid computing, Edge computing), Software (TensorFlow, PyTorch, ONNX), Application (Predictive analytics, Natural language processing, Autonomous systems) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Proliferation of generative AI and Large Language Models (LLM) demands unprecedented computational scale, Heightened data security and privacy risks in decentralized architectures

-

-

Who are the major players in the Distributed AI Computing Market?

-

Advanced Micro Devices Inc., Alibaba Cloud, Amazon.com Inc., Baidu Inc., Fujitsu Ltd., Google LLC, Graphcore Ltd., Hewlett Packard, Huawei Technologies Co. Ltd., Infosys Ltd., Intel Corp., IBM Corp., Meta Platforms Inc., Microsoft Corp., NEC Corp., NVIDIA Corp., Oracle Corp., Samsung Electronics Co. Ltd., SAP SE, Siemens AG and Tencent Holdings Ltd.

-

Market Research Insights

- The dynamics of the distributed AI computing market are shaped by the strategic need for real-time decision making and operational resilience. Adoption of hybrid computing models is accelerating, with enterprises that partition AI workloads between edge and cloud reporting up to a 40% reduction in data transmission costs.

- Furthermore, the integration of on-device generative AI into consumer electronics is a significant factor, with such devices demonstrating a 3X faster response time compared to cloud-dependent alternatives. This shift is enabled by advancements in AI model optimization and TinyML applications.

- In industrial settings, smart factory integration driven by AI-powered computer vision and intelligent automation is delivering measurable ROI, with some facilities achieving a 15% improvement in production throughput by deploying privacy-preserving AI for quality control directly on the assembly line.

We can help! Our analysts can customize this distributed ai computing market research report to meet your requirements.

RIA -

RIA -