Drone Navigation System Market Size 2026-2030

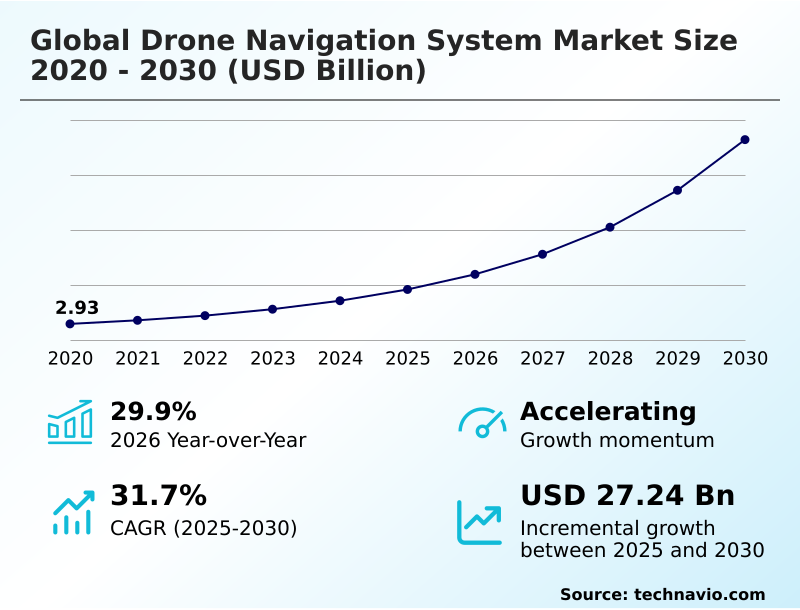

The drone navigation system market size is valued to increase by USD 27.24 billion, at a CAGR of 31.7% from 2025 to 2030. Rising need for resilient navigation in GNSS denied and contested zones will drive the drone navigation system market.

Major Market Trends & Insights

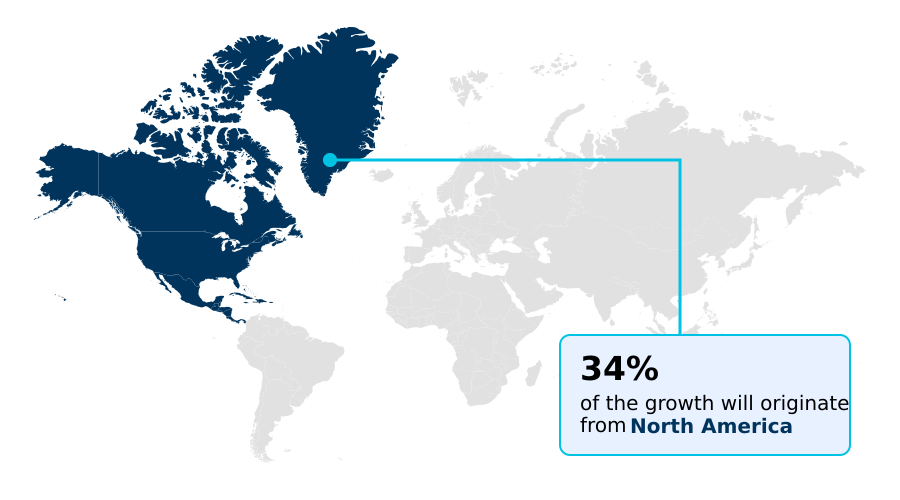

- North America dominated the market and accounted for a 34.3% growth during the forecast period.

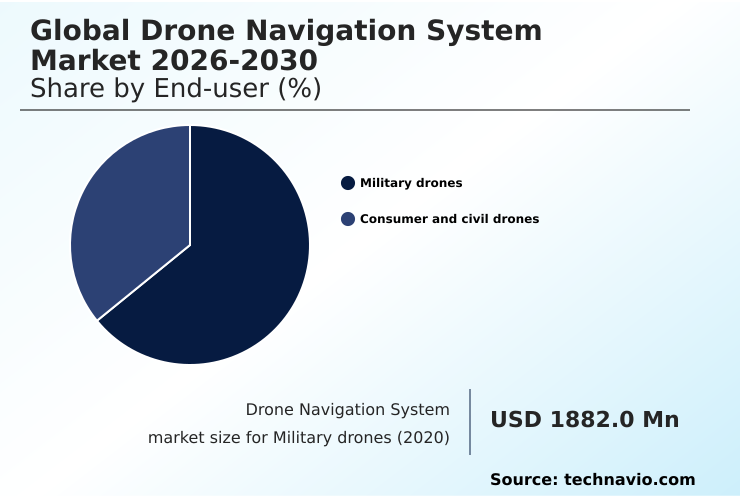

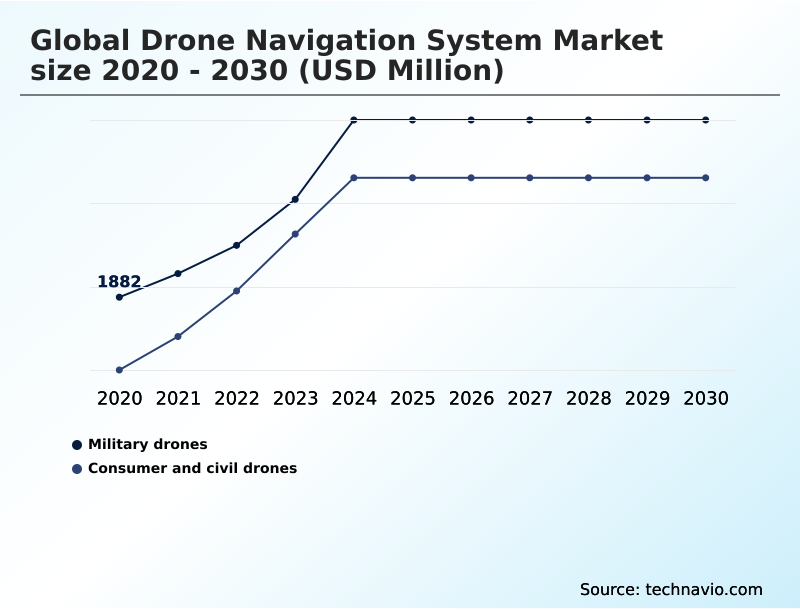

- By End-user - Military drones segment was valued at USD 3.90 billion in 2024

- By Type - Manually operated segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 33.49 billion

- Market Future Opportunities: USD 27.24 billion

- CAGR from 2025 to 2030 : 31.7%

Market Summary

- The Drone Navigation System Market is fundamentally transforming autonomous operations across defense, commercial, and industrial sectors. Growth is propelled by the increasing demand for reliable performance in environments where satellite signals are compromised, driving innovation in sensor fusion and AI-driven guidance.

- Key trends include the integration of swarm intelligence and edge computing to enable collaborative, real-time decision-making without reliance on ground stations. For instance, an infrastructure firm can deploy a fleet of drones for pipeline inspection, leveraging advanced navigation to autonomously map vast, remote areas, reducing manual survey times and enhancing worker safety.

- However, the industry faces challenges related to the high power consumption of advanced processing and fragmented regulatory frameworks that can slow the adoption of beyond-visual-line-of-sight operations. As technology matures, the focus remains on developing more resilient, accurate, and energy-efficient systems.

- The global drone navigation system market 2026-2030 is characterized by a push towards greater autonomy, where platforms can independently navigate complex, dynamic settings, underscoring the importance of robust drone navigation system.

What will be the Size of the Drone Navigation System Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Drone Navigation System Market Segmented?

The drone navigation system industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Military drones

- Consumer and civil drones

- Type

- Manually operated

- Autonomous

- Component

- Hardware

- Software

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By End-user Insights

The military drones segment is estimated to witness significant growth during the forecast period.

The military drones segment is driven by the imperative for unmanned systems autonomy in contested settings. Demand centers on sophisticated GNSS-denied navigation capabilities, where multi-sensor integration and AI-driven navigation are critical for mission success.

Systems employ tactical grade IMUs and fiber-optic gyros (FOG) for precise orientation, while autonomous path planning algorithms enable drones to operate without continuous operator input.

Investment focuses on developing robust anti-jamming technology and secure communication links to counter electronic warfare threats. Achieving this resilience often requires low SWaP-C solutions that incorporate GNSS spoofing detection, improving target acquisition accuracy by over 15%.

This reliance on real-time georeferencing and cooperative engagement capability ensures operational superiority in reconnaissance and surveillance missions, solidifying the need for advanced navigation hardware.

The Military drones segment was valued at USD 3.90 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 34.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Drone Navigation System Market Demand is Rising in North America Get Free Sample

The geographic landscape is characterized by distinct regional priorities. In North America, development is heavily influenced by defense-sector demands for resilient PNT and regulatory advancements supporting beyond visual line of sight (BVLOS) operations.

Widespread use in infrastructure inspection reduces manual survey times by over 50%.

Meanwhile, the APAC region leverages its manufacturing strength to produce scalable solutions for agriculture and logistics, with adoption in precision agriculture leading to a 15% improvement in crop yield consistency.

Europe focuses on collaborative, multinational projects emphasizing safety and interoperability, driving demand for detect and avoid (DAA) systems. Across all regions, the integration of autonomous flight controllers and sensor fusion algorithms is crucial for enabling applications like photogrammetry mapping.

This global diversification ensures that vision-based positioning and other GPS-independent navigation techniques continue to advance.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of drone navigation is increasingly specialized, addressing complex operational niches. Developing a robust GNSS denied navigation system design is paramount for ensuring mission continuity, particularly for resilient navigation for tactical UAVs operating in contested zones.

- In commercial sectors, achieving centimeter-level drone accuracy is a key objective, with firms integrating RTK in commercial drones for applications like UAV navigation for infrastructure inspection. This precise positioning is also essential for drone navigation for precision agriculture. The challenge of drone navigation in urban canyons has spurred innovation in AI-powered drone obstacle avoidance and sensor fusion for all-weather navigation.

- As operations scale up, BVLOS drone operation safety requirements and certification for autonomous drone systems become critical. The architecture for these systems must also consider the power consumption in drone navigation. For coordinated tasks, low latency swarm communication protocols are essential for multi-drone coordination and navigation.

- Comparing VIO and LiDAR for navigation helps determine the optimal technology for a given application, whether for autonomous drone inspection solutions or a navigation system for indoor drones. Advanced algorithms for drone swarms and onboard processing for autonomous flight are enabling new capabilities, while securing drone navigation from spoofing remains a persistent security concern.

- Firms specializing in these advanced systems report that integrating RTK can yield data accuracy twice as high as non-RTK methods, significantly reducing post-processing costs.

What are the key market drivers leading to the rise in the adoption of Drone Navigation System Industry?

- A key market driver is the rising need for resilient navigation systems that ensure operational continuity for drones in GNSS-denied and contested zones.

- Market growth is significantly driven by the expanding need for resilient PNT and the progressive regulatory frameworks enabling beyond visual line of sight (BVLOS) operations.

- The demand for reliable performance in signal-denied areas accelerates the adoption of advanced sensor fusion algorithms and vision-based positioning. These technologies, supported by autonomous flight controllers, are critical for applications like photogrammetry mapping and ensure high-integrity navigation.

- Systems equipped with sophisticated detect and avoid (DAA) systems can reduce mission failures by over 90% in contested environments.

- Furthermore, the integration of UAS traffic management (UTM) frameworks, which rely on GPS-independent navigation and precise flight path optimization, unlocks new commercial opportunities.

- The use of AI-driven navigation for collision avoidance systems improves obstacle detection accuracy by 75%, enhancing safety and enabling complex autonomous mission planning.

What are the market trends shaping the Drone Navigation System Industry?

- The expansion of hybrid and multi-sensor fusion capabilities is emerging as a prominent market trend. This approach enhances navigational resilience and accuracy in environments where satellite signals are unreliable.

- Key market trends are converging to enable higher levels of drone autonomy and operational efficiency. The adoption of swarm intelligence algorithms, powered by edge computing for drones, allows for collaborative drone operations where multiple platforms can map large areas or perform complex tasks in unison. This approach increases area coverage efficiency by 40% compared to single-drone missions.

- Concurrently, advancements in multi-sensor data fusion, incorporating techniques like extended Kalman filtering and LiDAR SLAM, provide robust dead reckoning capabilities. These systems are crucial for precision landing systems and maintaining accuracy in signal-denied environments.

- The use of a digital twin for navigation in simulation environments accelerates the development of automated flight path generation, with onboard processing reducing decision latency by up to 60%, paving the way for sophisticated 4D trajectory planning.

What challenges does the Drone Navigation System Industry face during its growth?

- Persistent vulnerabilities in global navigation satellite systems to interference like jamming and spoofing present a key challenge affecting industry growth and operational reliability.

- Key challenges constrain the market, primarily stemming from hardware limitations and regulatory fragmentation. The high computational demands of advanced navigation algorithms strain flight control computers and onboard power systems, with power-intensive processing reducing drone flight times by up to 20%. This necessitates ongoing innovation in low-power GPS modules and energy-efficient MEMS inertial sensors.

- Furthermore, the persistent threat of signal interference drives the need for robust anti-spoofing modules and redundant navigation architecture. However, the lack of globally harmonized standards for certified avionics software and counter-UAS technology creates significant hurdles for large-scale deployment.

- This complex landscape requires mission management software that is adaptable, yet the high cost of developing and certifying such systems can be a barrier for many operators, slowing the adoption of solutions like drone-in-a-box platforms.

Exclusive Technavio Analysis on Customer Landscape

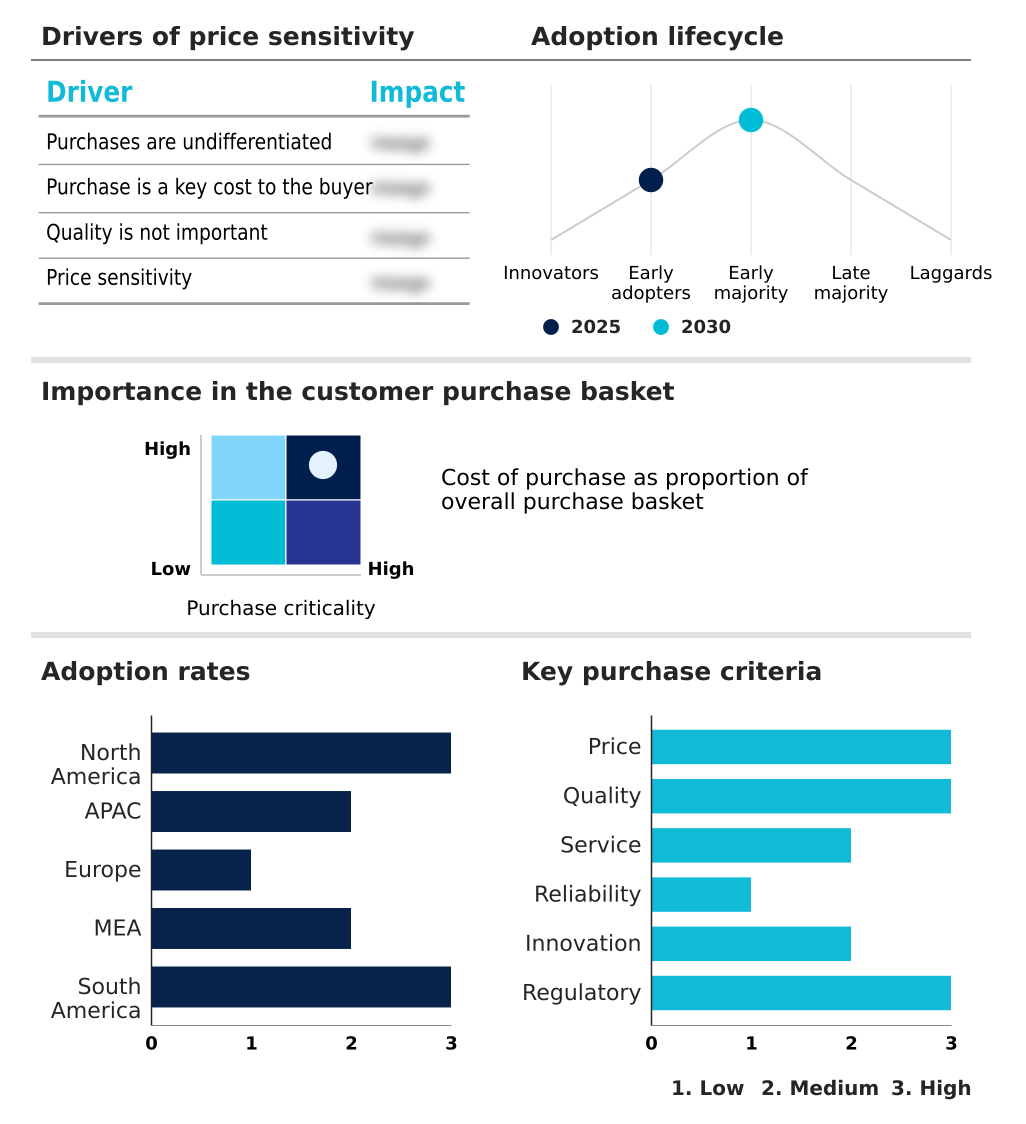

The drone navigation system market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the drone navigation system market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Drone Navigation System Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, drone navigation system market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Navigation Pty Ltd. - The company specializes in developing compact, high-precision GNSS-aided inertial navigation systems, crucial for enabling robust autonomy in unmanned platforms across diverse operational environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Navigation Pty Ltd.

- AeroVironment Inc.

- Elbit Systems Ltd.

- Gladiator Technologies Inc.

- Hexagon AB

- Honeywell International Inc.

- Inertial Labs

- Inertial Sense LLC

- MicroPilot Inc.

- Northrop Grumman Corp.

- Oxford Technical Solutions Ltd.

- Parker Hannifin Corp.

- Parrot Drones SAS

- Sagetech Avionics Inc.

- SBG Systems SAS

- SZ DJI Technology Co. Ltd.

- Trimble Inc.

- uAvionix Corp.

- UAVOS Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Drone navigation system market

- In August 2024, UAVOS Inc. evaluated computer vision within its autopilot systems for unmanned helicopters, aiming to advance autonomous navigation standards and safety protocols.

- In February 2025, engineers at the Massachusetts Institute of Technology introduced MiFly, a low-power edge system using millimeter-wave radars and backscatter tags for centimeter-level localization in GPS-denied environments.

- In May 2025, the German government launched the 'Fully Autonomous Flight 2.0 Challenge,' offering significant funding to develop precise drone navigation solutions without reliance on satellite systems.

- In May 2025, uAvionix Corp. launched skyAlert, a wearable device designed to provide operators with enhanced situational awareness by delivering alerts during unmanned aircraft system flights.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Drone Navigation System Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 293 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 31.7% |

| Market growth 2026-2030 | USD 27237.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 29.9% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The drone navigation system market has evolved from basic guidance to enabling sophisticated autonomy, driven by the integration of advanced technologies. The development of resilient PNT and GNSS-denied navigation capabilities is now central to system design, utilizing visual-inertial odometry and terrain-referenced navigation to operate in contested environments.

- Innovations in hardware, including tactical grade IMUs, MEMS inertial sensors, and multi-constellation GNSS receivers, are complemented by software advancements like sensor fusion algorithms and extended Kalman filtering. This synergy facilitates autonomous path planning and real-time kinematic (RTK) positioning. Anti-jamming technology and flight control computers are becoming standard for ensuring operational integrity.

- The push toward beyond visual line of sight (BVLOS) operations necessitates robust detect and avoid (DAA) systems and remote ID broadcast modules. Platforms integrating advanced photogrammetry mapping and LiDAR SLAM report a 30% reduction in positional drift during sustained signal denial, influencing boardroom decisions on investing in resilient, autonomous fleets that can deliver reliable performance and a competitive edge.

What are the Key Data Covered in this Drone Navigation System Market Research and Growth Report?

-

What is the expected growth of the Drone Navigation System Market between 2026 and 2030?

-

USD 27.24 billion, at a CAGR of 31.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Military drones, and Consumer and civil drones), Type (Manually operated, and Autonomous), Component (Hardware, and Software) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Rising need for resilient navigation in GNSS denied and contested zones, Persistent vulnerability in global navigation satellite systems

-

-

Who are the major players in the Drone Navigation System Market?

-

Advanced Navigation Pty Ltd., AeroVironment Inc., Elbit Systems Ltd., Gladiator Technologies Inc., Hexagon AB, Honeywell International Inc., Inertial Labs, Inertial Sense LLC, MicroPilot Inc., Northrop Grumman Corp., Oxford Technical Solutions Ltd., Parker Hannifin Corp., Parrot Drones SAS, Sagetech Avionics Inc., SBG Systems SAS, SZ DJI Technology Co. Ltd., Trimble Inc., uAvionix Corp. and UAVOS Inc.

-

Market Research Insights

- Market dynamics are increasingly shaped by the need for high-integrity navigation and certified avionics software to meet stringent safety and regulatory requirements. The integration of UAS traffic management (UTM) frameworks is paving the way for scalable commercial drone operations, where autonomous mission planning and flight path optimization are critical.

- Implementing precision landing systems has been shown to reduce landing errors by up to 40%, enhancing safety for drone-in-a-box solutions. Furthermore, adopting GPS-independent navigation techniques enables operational continuity, while the use of certified avionics software can cut compliance validation cycles by 25%.

- This focus on safety, efficiency, and autonomy is driving investment in advanced collision avoidance systems and redundant navigation architectures to ensure reliable performance.

We can help! Our analysts can customize this drone navigation system market research report to meet your requirements.

RIA -

RIA -