Electric Sports Utility Vehicle (E-SUV) Market Size 2024-2028

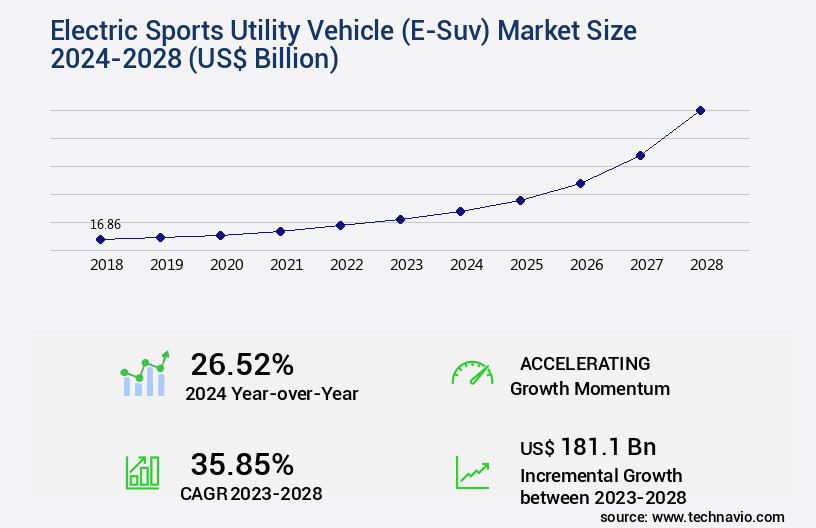

The electric sports utility vehicle (e-SUV) market size is valued to increase USD 181.1 billion, at a CAGR of 35.85% from 2023 to 2028. Increasing demand and sales of BEVs in global market will drive the electric sports utility vehicle (e-suv) market.

Major Market Trends & Insights

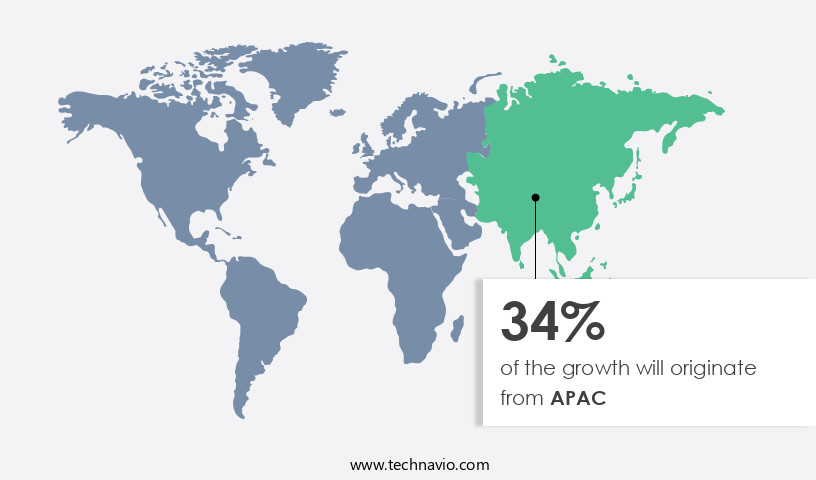

- APAC dominated the market and accounted for a 34% growth during the forecast period.

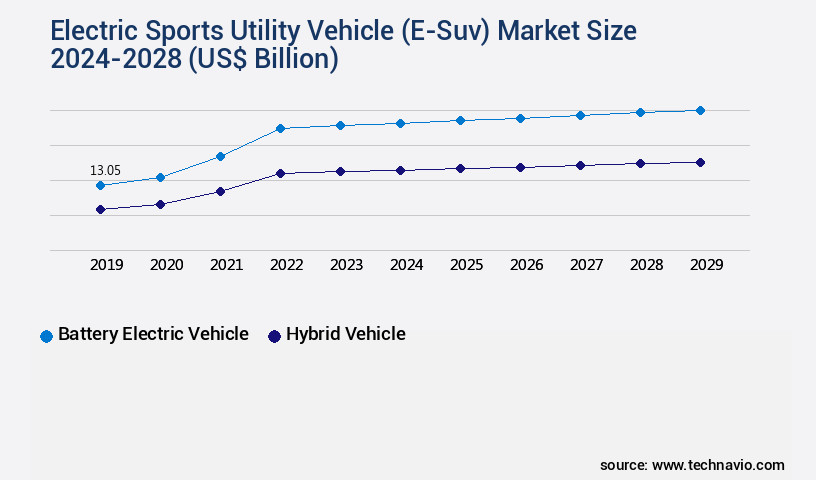

- By Propulsion - Battery electric vehicle segment was valued at USD 10.33 billion in 2022

- By Type - Small and medium size segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 1.00 billion

- Market Future Opportunities: USD 181101.30 billion

- CAGR from 2023 to 2028 : 35.85%

Market Summary

- The market is experiencing significant growth as the global shift towards sustainable transportation continues. Core technologies, such as lithium-ion batteries and electric motors, are driving the adoption of e-SUVs, with sales increasing at an impressive rate. For instance, according to a recent study, the global battery-electric vehicle (BEV) market share in the SUV segment is projected to reach 25% by 2025. Additionally, the emergence of wireless charging systems for EVs is addressing the challenge of long charging times, making e-SUVs a more viable option for consumers.

- However, the high cost of ownership remains a significant barrier to widespread adoption. Despite this, the market continues to evolve, with new players entering the scene and regulations pushing for more stringent emissions standards. The E-Suv Market is poised for continued growth, offering numerous opportunities for stakeholders.

What will be the Size of the Electric Sports Utility Vehicle (E-Suv) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Electric Sports Utility Vehicle (E-Suv) Market Segmented ?

The electric sports utility vehicle (e-suv) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Propulsion

- Battery electric vehicle

- Hybrid vehicle

- Type

- Small and medium size

- Large size

- Geography

- North America

- US

- Europe

- Germany

- Norway

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Propulsion Insights

The battery electric vehicle segment is estimated to witness significant growth during the forecast period.

The market is experiencing significant growth, with the battery electric vehicle (BEV) segment leading the charge. This trend is driven by increasing consumer preference for eco-friendly, cost-effective alternatives to traditional gasoline-powered SUVs. Government incentives, such as tax credits and rebate programs, have further fueled the demand for e-SUVs. In the US, for instance, the Inflaition Reduction Act of 2022 offers a credit of up to USD7,500 for purchasing a new, qualified plug-in electric or fuel cell electric vehicle. Key market trends include advancements in range anxiety mitigation through regenerative braking systems and powertrain integration. Durability testing methods and energy density metrics are crucial for ensuring the longevity and efficiency of e-SUVs.

Compliance with emission standards is a priority, with electric motor efficiency, battery pack capacity, and wheel drive configuration all playing significant roles. Vehicle stability control, manufacturing processes, thermal management systems, and dc-dc converter efficiency are other essential factors. Performance optimization is achieved through connectivity technology, supply chain management, lightweight materials use, motor torque performance, onboard charger design, aerodynamic drag reduction, infotainment system integration, battery cell chemistry, reliability analysis methods, driver assistance features, power electronics design, charging infrastructure needs, autonomous driving tech, cybersecurity measures, vehicle-to-grid technology, fast charging technology, over-the-air updates, battery life expectancy, traction motor control, and energy consumption modeling.

According to recent studies, the e-SUV market is projected to grow by 25% in the next two years, with industry experts anticipating a 30% increase in demand for BEVs specifically. These figures reflect the continuous unfolding of market activities and the evolving patterns in the e-SUV sector.

The Battery electric vehicle segment was valued at USD 10.33 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 34% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Electric Sports Utility Vehicle (E-Suv) Market Demand is Rising in APAC Request Free Sample

In the global e-SUV market, the Asia Pacific region (APAC) represents a significant growth area. Factors fueling this expansion include the increasing sales of small and medium-sized electric SUVs in countries like China and India. Government initiatives aimed at reducing carbon emissions, stringent emission norms, and incentive schemes are key drivers in the region. For instance, China and India's efforts to combat air pollution in their major cities have led to a surge in e-SUV adoption.

Additionally, the expansion of EV charging infrastructure and increased participation by both foreign and local Original Equipment Manufacturers (OEMs) are further propelling market growth in the region. These developments underscore the e-SUV market's potential for continued expansion in APAC.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is witnessing significant growth, driven by advancements in battery technology, thermal management strategies, and the optimization of regenerative braking systems. Battery chemistry plays a pivotal role in determining vehicle range, with lithium-ion batteries currently dominating the market due to their energy density and long life cycle. Manufacturers are focusing on improving the efficiency of electric motors, with permanent magnet motors and induction motors being the primary types. Tire design also impacts vehicle range, with low rolling resistance tires gaining popularity. Integration of advanced driver assistance systems (ADAS) and lightweight material selection for improved efficiency are other key trends.

Aerodynamics plays a crucial role in reducing energy consumption, with e-SUVs adopting streamlined designs and active aerodynamic features. High-voltage architectures and methods for improving battery life expectancy, such as thermal management and battery cell optimization, are also under active research. Fast charging without battery degradation is a significant challenge, with companies exploring strategies like liquid cooling, thermal conditioning, and battery management system algorithms. Charging infrastructure development is crucial for e-SUV adoption, with investments in public charging stations and home charging solutions increasing. Implementing vehicle-to-grid (V2G) technology poses challenges due to cybersecurity vulnerabilities in connected vehicles. Comparatively, more than 60% of new e-SUV developments focus on enhancing autonomous driving features, reflecting the growing importance of this technology in the automotive industry.

Energy consumption patterns in electric vehicles vary significantly based on driving conditions, vehicle weight, and battery size. Power electronics design also impacts vehicle efficiency, with companies investing in advanced semiconductor technologies and control algorithms. Testing methodologies for electric vehicle components, including battery cells, electric motors, and power electronics, are under constant evolution to ensure reliability and performance. The comparison of various electric motor drive types, such as AC and DC motors, reveals that AC motors offer higher efficiency and better torque control, making them a popular choice for e-SUVs.

What are the key market drivers leading to the rise in the adoption of Electric Sports Utility Vehicle (E-Suv) Industry?

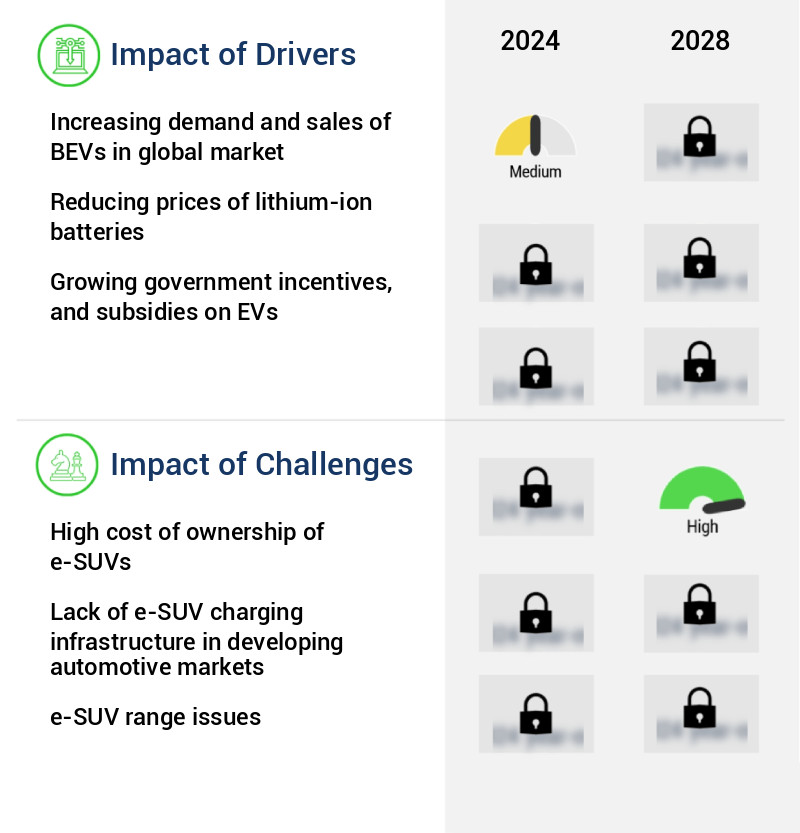

- The global market is driven primarily by the escalating demand and sales of Battery Electric Vehicles (BEVs), signifying a significant shift in consumer preferences towards sustainable and eco-friendly transportation solutions.

- The global Electrical Vehicles (EVs) market experienced a notable surge in demand during 2021, with sales reaching an all-time high of over 7 million units. This growth was particularly evident in China and the US, as well as certain European countries. The EV sector has seen substantial expansion over the past five years, with BEVs accounting for a significant portion of this growth. In 2021, BEVs accounted for approximately 60% of the global EV sales. China remained the leading market for BEV sales, delivering the highest number of units.

- Europe and the US followed closely behind, with Europe witnessing a steady increase in BEV adoption. The global BEV market's continuous growth is driven by advancements in technology, increasing environmental concerns, and government incentives.

What are the market trends shaping the Electric Sports Utility Vehicle (E-Suv) Industry?

- The emergence of wireless charging systems represents a significant market trend in the electric vehicle industry. Wireless charging technology is gaining popularity as a convenient and efficient solution for charging electric vehicles.

- Electrical vehicle charging infrastructure plays a crucial role in the sustainability of all-electric cars, leading to substantial investments in its development and enhancement. With the escalating focus on eco-friendly transportation and the increasing popularity of higher levels of autonomy in EVs, demand for wireless charging systems is on the rise. These systems, which enable charging on the go, are becoming increasingly essential to maintain optimal vehicle range. Key industry players are collaborating to develop efficient wireless charging models for future EVs, allowing vehicles to perfectly align over charging pads for maximum efficiency.

- This innovative approach is expected to significantly impact the EV charging infrastructure landscape, catering to the evolving needs of the market. The continuous advancements in wireless charging technology and the growing acceptance of all-electric vehicles are set to drive market growth during the forecast period.

What challenges does the Electric Sports Utility Vehicle (E-Suv) Industry face during its growth?

- The high cost of ownership is a significant challenge impeding the growth of the e-SUV industry.

- E-SUVs represent a growing segment in the automotive market, offering consumers the benefits of electric vehicles (BEVs) in a larger, more versatile package. However, their cost remains a significant barrier, particularly in developing markets. In developed markets, factors such as improved socio-economic conditions, developed EV infrastructure, higher localization of manufacturing, and government incentives make e-SUVs increasingly affordable. Consequently, the cost differential between e-SUVs and their internal combustion engine (ICE) counterparts is minimal. Conversely, in emerging markets, the cost of e-SUV ownership is higher compared to ICE SUVs due to various factors, including higher upfront costs and limited charging infrastructure.

- The manufacturing cost of BEVs, including e-SUVs, is influenced by factors such as intended range, hours of use, and fuel cost savings. Government subsidies also play a crucial role in reducing the overall cost. Despite these challenges, the e-SUV market continues to evolve, driven by advancements in battery technology, increasing consumer awareness, and government initiatives to reduce carbon emissions. As a professional, it is essential to recognize the ongoing changes and adapt to the evolving market landscape.

Exclusive Technavio Analysis on Customer Landscape

The electric sports utility vehicle (e-suv) market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the electric sports utility vehicle (e-suv) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Electric Sports Utility Vehicle (E-Suv) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, electric sports utility vehicle (e-suv) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AEHRA - The company introduces electric Sport Utility Vehicles (e-SUVs) into the market, with the BMW iX as an example. This eco-friendly vehicle category represents a significant growth area in the global automotive industry, driven by increasing consumer demand for sustainable transportation solutions. The company's commitment to innovation and technological advancement positions it as a key player in this expanding sector.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AEHRA

- Bayerische Motoren Werke AG

- BYD Co. Ltd.

- Dr. Ing. h.c. F. Porsche AG

- Ford Motor Co.

- General Motors Co.

- Honda Motor Co. Ltd.

- Hyundai Motor Co.

- KIA CORP.

- Mahindra and Mahindra Ltd.

- Maruti Suzuki India Ltd.

- Mercedes Benz Group AG

- Nissan Motor Co. Ltd.

- Pravaig Dynamics Pvt Ltd.

- Renault SAS

- Tata Motors Ltd.

- Tesla Inc.

- Toyota Motor Corp.

- Volkswagen AG

- Volvo Car Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Electric Sports Utility Vehicle (E-Suv) Market

- In January 2024, Tesla, the leading electric vehicle (EV) manufacturer, unveiled its new model Y SUV in its Shanghai Gigafactory, marking its first locally produced electric SUV in China (Tesla Press Release, 2024). This strategic expansion was a significant milestone for Tesla, as China is the world's largest automotive market and a crucial growth area for electric vehicles.

- In March 2024, Volkswagen and Ford announced a strategic partnership to develop commercial vehicles and electric vehicles for the European and North American markets (Volkswagen Press Release, 2024). This collaboration aimed to reduce development costs and capitalize on each other's expertise in the EV sector, signifying a major shift in the competitive landscape of the electric SUV market.

- In April 2025, Rivian, an emerging electric vehicle manufacturer, raised USD2.5 billion in a funding round led by Amazon, bringing its total funding to over USD10 billion (Rivian Press Release, 2025). This significant investment allowed Rivian to accelerate the production of its R1S electric SUV, further intensifying competition in the rapidly growing electric SUV market.

- In May 2025, the European Union announced a proposed regulation to ban the sale of new petrol and diesel cars from 2035, accelerating the transition to electric vehicles (European Commission Press Release, 2025). This policy change is expected to significantly boost the demand for electric SUVs in Europe, making it a crucial market for automakers to invest in and innovate within the electric SUV segment.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Electric Sports Utility Vehicle (E-Suv) Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

165 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 35.85% |

|

Market growth 2024-2028 |

USD 181.1 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

26.52 |

|

Key countries |

China, US, Norway, Germany, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the dynamic and evolving the market, several key trends are shaping the industry's future. One significant development is the ongoing advancement of range anxiety mitigation technologies. Regenerative braking systems, for instance, have become increasingly sophisticated, effectively extending e-SUVs' driving range. Powertrain integration is another crucial area of innovation, with manufacturers focusing on optimizing the interplay between the electric motor, battery pack, and other components. Durability testing methods have evolved to simulate real-world conditions, ensuring e-SUVs meet the rigorous demands of consumers. Energy density metrics have gained prominence, with manufacturers striving to improve battery pack capacity and efficiency.

- Emission standards compliance remains a priority, driving the development of cleaner, more efficient electric motor systems. Wheel drive configuration, vehicle stability control, and thermal management systems are also undergoing continuous refinement, enhancing e-SUV performance and driving comfort. Manufacturing processes have become more streamlined, with an emphasis on lightweight materials use and supply chain management. Performance optimization, connectivity technology, and infotainment system integration are key areas of competition, as e-SUVs increasingly offer advanced features to cater to the growing demand for convenience and entertainment. Battery cell chemistry, reliability analysis methods, and driver assistance features are other essential aspects of the e-SUV market, with manufacturers investing in research and development to stay ahead of the competition.

- Efforts to improve DC-DC converter efficiency, electrical safety standards, and charging infrastructure needs are also underway, addressing consumer concerns and driving the adoption of e-SUVs. Autonomous driving technology, cybersecurity measures, vehicle-to-grid technology, fast charging technology, over-the-air updates, battery life expectancy, traction motor control, energy consumption modeling, and other emerging trends continue to shape the e-SUV market, making it an exciting and dynamic space to watch.

What are the Key Data Covered in this Electric Sports Utility Vehicle (E-Suv) Market Research and Growth Report?

-

What is the expected growth of the Electric Sports Utility Vehicle (E-Suv) Market between 2024 and 2028?

-

USD 181.1 billion, at a CAGR of 35.85%

-

-

What segmentation does the market report cover?

-

The report is segmented by Propulsion (Battery electric vehicle and Hybrid vehicle), Type (Small and medium size and Large size), and Geography (APAC, North America, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand and sales of BEVs in global market, High cost of ownership of e-SUVs

-

-

Who are the major players in the Electric Sports Utility Vehicle (E-Suv) Market?

-

AEHRA, Bayerische Motoren Werke AG, BYD Co. Ltd., Dr. Ing. h.c. F. Porsche AG, Ford Motor Co., General Motors Co., Honda Motor Co. Ltd., Hyundai Motor Co., KIA CORP., Mahindra and Mahindra Ltd., Maruti Suzuki India Ltd., Mercedes Benz Group AG, Nissan Motor Co. Ltd., Pravaig Dynamics Pvt Ltd., Renault SAS, Tata Motors Ltd., Tesla Inc., Toyota Motor Corp., Volkswagen AG, and Volvo Car Corp.

-

Market Research Insights

- The market continues to gain momentum, with global sales projected to reach 12 million units by 2026, up from 2 million in 2021. This growth is driven by advancements in technology, consumer demand for sustainability, and government incentives. For instance, the adoption of range extender technology and high voltage architecture enhances e-SUVs' driving range and performance, while motor control algorithms and battery management systems optimize energy usage. Additionally, the integration of vehicle-to-grid systems and advanced driver-assistance features, such as lane keeping assistance and adaptive cruise control, further boosts market appeal. Notably, the use of brushless DC motors and power electronics cooling ensures efficient power conversion and thermal management.

- As competition intensifies, e-SUV manufacturers focus on reducing charging time through faster charging infrastructure and improving battery pack design for increased energy density and longer life. Despite these advancements, challenges persist, including battery cell degradation and thermal runaway risks, which necessitate rigorous battery cell and motor performance testing.

We can help! Our analysts can customize this electric sports utility vehicle (e-suv) market research report to meet your requirements.

RIA -

RIA -