Energy Drinks Market Size 2026-2030

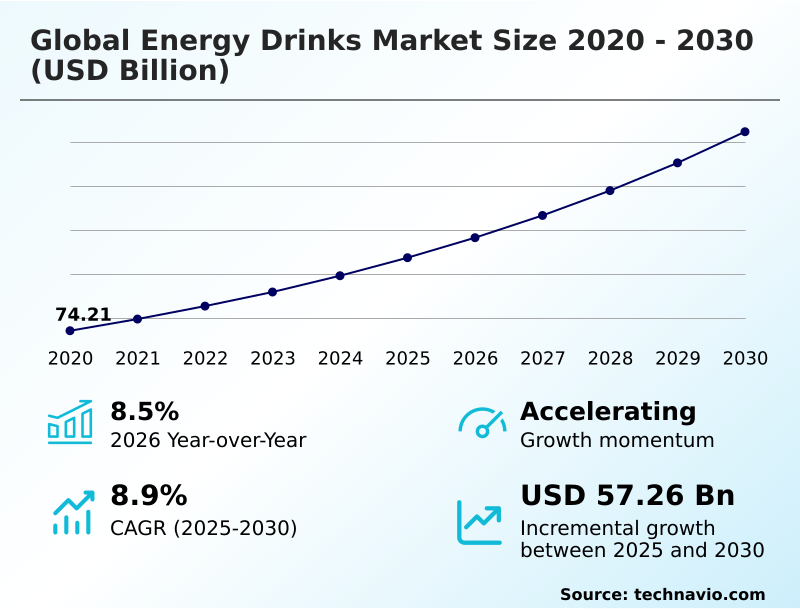

The energy drinks market size is valued to increase by USD 57.26 billion, at a CAGR of 8.9% from 2025 to 2030. Rising demand for functional and health-oriented formulations will drive the energy drinks market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 38.8% growth during the forecast period.

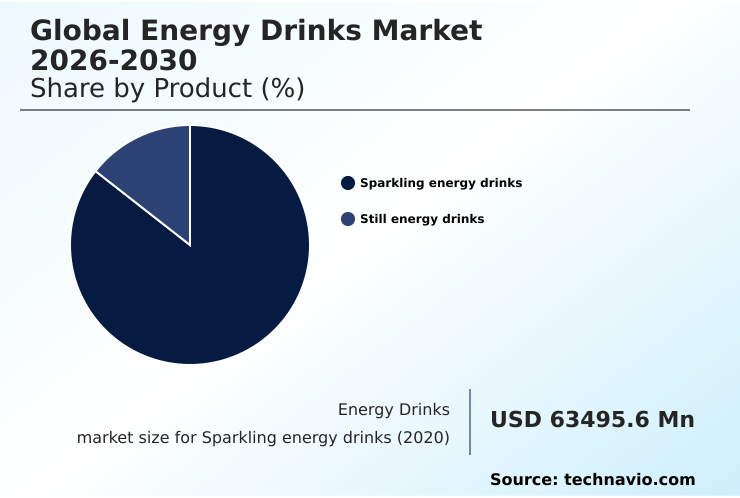

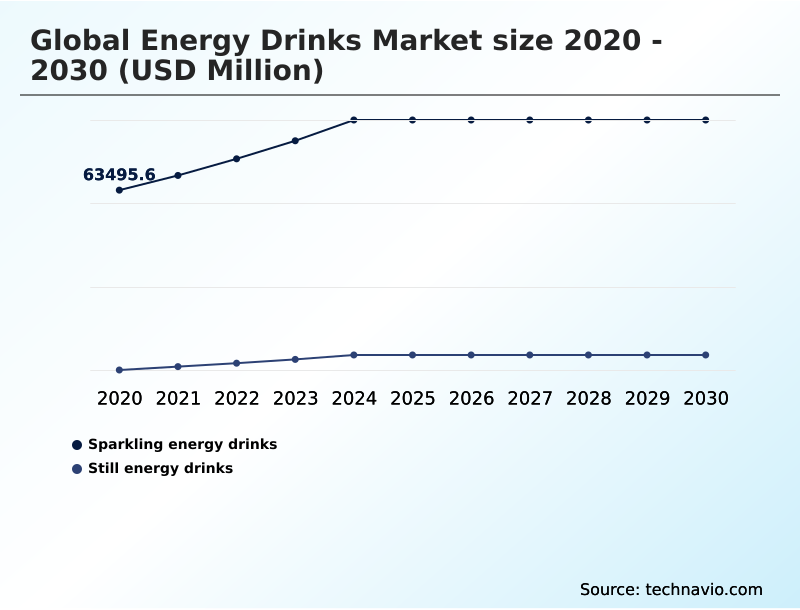

- By Product - Sparkling energy drinks segment was valued at USD 84.08 billion in 2024

- By Distribution Channel - Offline segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 90.46 billion

- Market Future Opportunities: USD 57.26 billion

- CAGR from 2025 to 2030 : 8.9%

Market Summary

- The energy drinks market is undergoing a significant metamorphosis, moving beyond its traditional athletic and nightlife associations to embrace a broader wellness-oriented identity. This evolution is driven by a profound shift in consumer preferences toward clean-label products featuring natural caffeine sources, nootropics for cognitive enhancement, and adaptogens for stress management.

- Manufacturers are responding by reformulating portfolios to eliminate synthetic stimulants and artificial sweeteners, aligning with the demand for metabolic health and ingredient transparency. For instance, a beverage company facing new tiered sugar tax regulations might reformulate its flagship product with stevia and monk fruit.

- This not only ensures compliance, reducing excise tax liability by up to 20%, but also creates a new marketing angle, positioning the drink as a healthier choice for productivity-focused professionals and fitness enthusiasts.

- This strategic pivot from high-impact stimulation to sustained, functional energy is essential for navigating an increasingly competitive and health-conscious landscape, where success depends on catering to diversified consumption occasions, from e-sports to corporate wellness programs. The rise of direct-to-consumer models and quick-commerce platforms further disrupts traditional retail, enabling niche brands to reach global audiences and intensify market innovation.

What will be the Size of the Energy Drinks Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Energy Drinks Market Segmented?

The energy drinks industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Sparkling energy drinks

- Still energy drinks

- Distribution channel

- Offline

- Online

- Product type

- Natural

- Conventional

- Geography

- APAC

- Japan

- China

- India

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- APAC

By Product Insights

The sparkling energy drinks segment is estimated to witness significant growth during the forecast period.

The sparkling energy drinks segment remains the market cornerstone, driven by consumer perception linking carbonation with refreshment. This category is pivoting toward clean-label products, using carbonated spring water and natural essences.

Innovations in flavor diversification are moving beyond standard profiles to include botanical stimulants and adaptogenic herbs for a holistic energy lift. These functional ingredients appeal to modern consumer demographics seeking wellness-oriented drinks.

The format's success is also tied to advancements in aluminum can technology, which ensures superior carbonation retention and supports sustainable packaging goals.

Brands leveraging seasonal flavor releases within this segment have noted a 15% increase in repeat purchases, underscoring the value of experiential marketing. This is complemented by the growth of functional beverages as a whole.

The Sparkling energy drinks segment was valued at USD 84.08 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 38.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Energy Drinks Market Demand is Rising in APAC Get Free Sample

The geographic landscape is defined by robust expansion in APAC, which is set to contribute nearly 39% of the market's incremental growth.

This region is driven by rising disposable incomes and the adoption of Westernized consumption patterns, creating a fertile ground for both conventional product type and natural product type beverages.

In contrast, North America represents a mature but highly innovative theater, where the focus is on premiumization and functional diversification. Europe remains a complex market shaped by stringent regulations, pushing a rapid transition toward sugar-free variants.

The strategic use of offline distribution and online distribution channels varies significantly, with e-commerce platforms enabling niche brands to bypass traditional retail beverage placement barriers, a strategy that has increased market penetration for new entrants by over 25%.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- A comprehensive analysis of the global energy drinks market 2026-2030 reveals nuanced consumer inquiries shaping product development. Questions around the best energy drink for gamers and energy drinks for corporate professionals are driving the creation of specialized nootropic drinks that prioritize focus over intense physical stimulation.

- The demand for healthy alternatives to energy drinks has led to the growth of plant based energy drinks and products without artificial sweeteners. Consequently, brands are transparent about the caffeine content in energy drinks and are exploring the role of adaptogens in beverages to offer stress-mitigating benefits.

- The impact of sugar tax on beverages has accelerated the push for low sugar pre workout drink options, directly addressing both regulatory challenges in the beverage industry and consumer health concerns. Marketing energy drinks to women has become a key strategy, correcting a historical imbalance.

- On the operational side, companies are optimizing e-commerce strategies for beverage brands, particularly for energy drink consumption in APAC. For example, firms implementing advanced inventory management for their online channels have seen a 10% reduction in stock-outs compared to those relying solely on traditional retail.

- The discussion continues to evolve around new energy drink product launches, comparing sparkling vs still energy drinks, the use of functional ingredients in sports nutrition, and a commitment to sustainable packaging for beverage cans, reflecting a sophisticated and demanding marketplace.

What are the key market drivers leading to the rise in the adoption of Energy Drinks Industry?

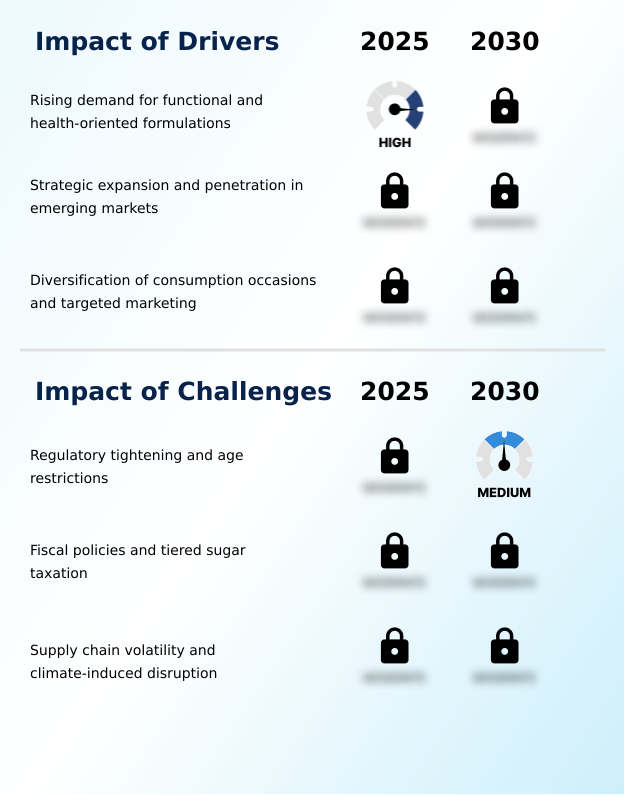

- The primary market driver is the rising consumer demand for functional and health-oriented beverage formulations.

- Market growth is significantly driven by strategic expansion into new consumer segments and consumption occasions. The development of adult-centric productivity drinks and on-the-go energy solutions has broadened the market beyond its traditional youth demographic.

- This has been supported by innovative energy drink distribution strategies, including partnerships that place products in corporate wellness programs, leading to a 15% increase in bulk sales.

- The pre-workout supplements category continues to merge with energy drinks, with hybrid products showing a 30% faster adoption rate than standalone items.

- The increasing popularity of ready-to-drink energy formats, particularly canned energy drinks, available through convenience store beverage sales and quick-commerce platforms, ensures immediate accessibility. Key components driving this demand include vitamin fortification and electrolyte replenishment.

What are the market trends shaping the Energy Drinks Industry?

- The market is experiencing a significant shift toward cognitive enhancement. Nootropic formulations are becoming a key differentiator for brands targeting mental acuity and focus.

- Key market trends are centered on the evolution toward wellness-oriented drinks, where consumer preference is shifting from simple stimulation to holistic benefits. The integration of nootropic formulations for cognitive enhancement is a primary driver, with brands that incorporate such ingredients reporting a 20% higher customer retention rate. This is complemented by a rise in clean-label products that emphasize ingredient transparency.

- The e-sports beverage market continues to expand, with specialized gaming energy drinks designed for sustained focus, a segment that has seen a 25% year-over-year growth in online sales. Furthermore, the diversification of the lifestyle beverage category to include female-focused energy drinks is unlocking new consumer segments, correcting a long-standing market imbalance and expanding the overall addressable audience.

- B-vitamins and taurine remain staple functional ingredients.

What challenges does the Energy Drinks Industry face during its growth?

- Regulatory tightening and the implementation of age restrictions present a key challenge to industry growth.

- The primary market challenge stems from navigating an increasingly complex regulatory environment and shifting consumer perceptions around health. The proliferation of synthetic stimulants in conventional formulations has attracted intense scrutiny, forcing many companies to pivot to natural alternatives. This reformulation process can increase production costs by up to 18%, impacting profit margins.

- Furthermore, the demand for sustainable packaging is pressuring brands to transition away from plastics, a move that requires significant capital investment in new bottling and canning lines. The competitive pressure from the broader sports nutrition drinks market and powdered energy mixers, which offer greater customization, forces constant innovation.

- Finally, managing brand partnerships effectively to maintain an authentic connection with consumers remains a persistent challenge in a crowded marketplace that includes sports drinks.

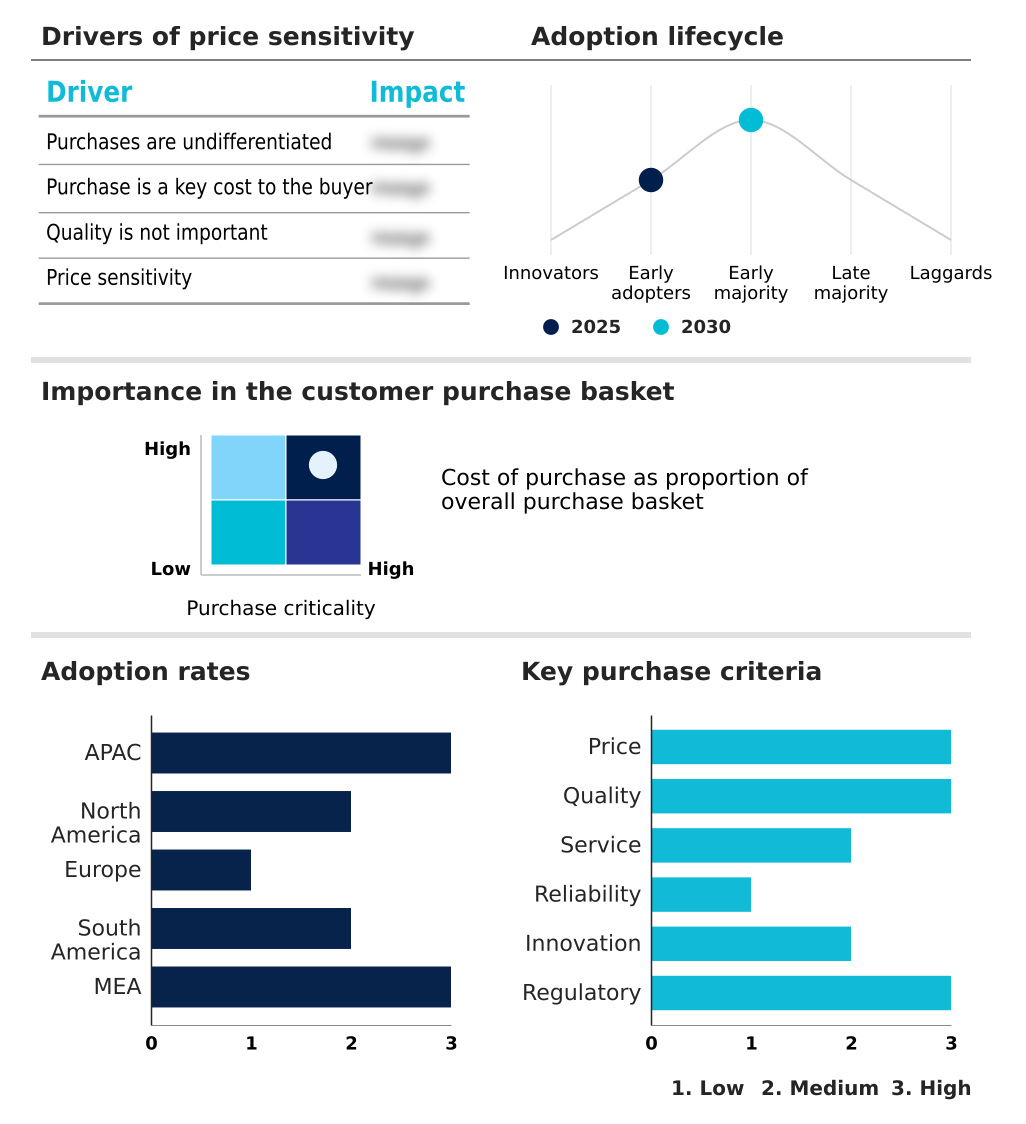

Exclusive Technavio Analysis on Customer Landscape

The energy drinks market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the energy drinks market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Energy Drinks Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, energy drinks market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alani Nutrition LLC - Analysis indicates a focus on formulating low-calorie energy drinks and wellness supplements, targeting a health-conscious consumer base with lifestyle beverage category products.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alani Nutrition LLC

- Amway Corp.

- Celsius Holdings Inc.

- G Fuel

- Ghost LLC

- GOAT Fuel Inc.

- HELL ENERGY Magyarorszag Kft.

- Hype Energy Drinks

- Keurig Dr Pepper Inc.

- Living Essentials Marketing LLC

- Monster Beverage Corp.

- Nutrabolt

- Otsuka Holdings Co. Ltd.

- PepsiCo Inc.

- Red Bull GmbH

- Suntory Beverage and Food Ltd.

- TCP Group

- Uptime Energy Inc.

- Yerbae Brands Co.

- ZOA Energy

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Energy drinks market

- In January 2025, Celsius Holdings Inc. expanded its portfolio with the launch of Sparkling Strawberry Passionfruit, a new flavor released nationwide across major retail and online channels to capture seasonal demand.

- In January 2025, Anheuser-Busch, in collaboration with sports nutrition company 1st Phorm, launched Phorm Energy, a new beverage line distributed through an extensive network of US convenience stores and retailers.

- In April 2025, Celsius Holdings Inc. finalized its acquisition of Alani Nutrition LLC, integrating the Alani Nu brand's ready-to-drink products and supplements into its broader distribution system.

- In July 2025, O'Neill Vintners and Distillers introduced Catalyst, a plant-based energy drink engineered for health-conscious consumers, featuring nootropics and containing zero sugar or artificial additives.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Energy Drinks Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 286 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.9% |

| Market growth 2026-2030 | USD 57264.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.5% |

| Key countries | Japan, China, India, South Korea, Indonesia, Thailand, US, Canada, Mexico, UK, Germany, France, Italy, Spain, Poland, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Egypt and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's innovation is centered on sophisticated beverage formulation, moving away from high-caffeine synthetic stimulants toward a more nuanced use of functional ingredients. We are observing a significant pivot to natural caffeine sources like yerba mate and guarana, often combined with adaptogenic herbs, ginseng, and other herbal extracts to offer holistic benefits.

- The inclusion of nootropic formulations with l-theanine and citicoline for cognitive enhancement is becoming standard. Formulations now frequently include amino acid blends, taurine, and b-vitamins for metabolic support. The market is segmented by product, including sparkling energy drinks and still energy drinks, and by product type, such as natural and conventional.

- Clean-label products, sugar-free variants, and low-calorie options are driving growth, with some brands exploring ketone-based energy and fermented botanicals. This shift has necessitated a 25% increase in R&D spending for firms aiming to validate the efficacy of these new ingredient combinations.

- This complex landscape of functional beverages, which includes sports drinks, ready-to-drink coffee, and carbonated beverages, is increasingly defined by a focus on thermogenesis, electrolyte replenishment, and vitamin fortification, managed through both offline distribution and expanding online distribution channels.

What are the Key Data Covered in this Energy Drinks Market Research and Growth Report?

-

What is the expected growth of the Energy Drinks Market between 2026 and 2030?

-

USD 57.26 billion, at a CAGR of 8.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Sparkling energy drinks, and Still energy drinks), Distribution Channel (Offline, and Online), Product Type (Natural, and Conventional) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising demand for functional and health-oriented formulations, Regulatory tightening and age restrictions

-

-

Who are the major players in the Energy Drinks Market?

-

Alani Nutrition LLC, Amway Corp., Celsius Holdings Inc., G Fuel, Ghost LLC, GOAT Fuel Inc., HELL ENERGY Magyarorszag Kft., Hype Energy Drinks, Keurig Dr Pepper Inc., Living Essentials Marketing LLC, Monster Beverage Corp., Nutrabolt, Otsuka Holdings Co. Ltd., PepsiCo Inc., Red Bull GmbH, Suntory Beverage and Food Ltd., TCP Group, Uptime Energy Inc., Yerbae Brands Co. and ZOA Energy

-

Market Research Insights

- Market dynamics are increasingly shaped by sophisticated energy drink marketing and strategic brand partnerships, which have proven to enhance brand visibility by over 30% in competitive regions. The growth of the direct-to-consumer beverage brands channel has been pivotal, with some companies reporting a 15% reduction in customer acquisition costs compared to traditional retail-focused campaigns.

- This shift is amplified by the rise of quick-commerce beverage delivery, which improves order fulfillment times by an average of 40% in dense urban areas, fundamentally altering on-the-go energy solutions. As consumer demographics evolve, the industry is adapting its beverage formulation to meet new demands for ingredient transparency, creating a more dynamic and responsive market.

We can help! Our analysts can customize this energy drinks market research report to meet your requirements.

RIA -

RIA -