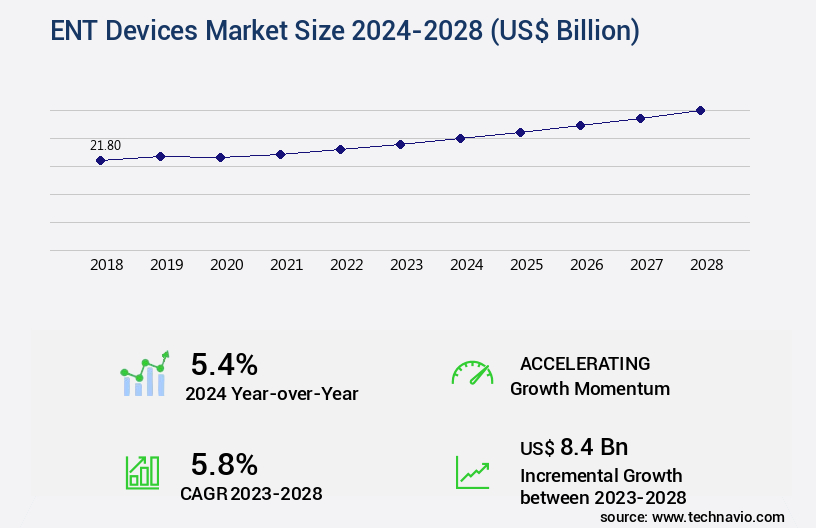

ENT Devices Market Size 2024-2028

The ent devices market size is valued to increase by USD 8.4 billion, at a CAGR of 5.8% from 2023 to 2028. Rising prevalence of ENT disorders will drive the ent devices market.

Market Insights

- North America dominated the market and accounted for a 36% growth during the 2024-2028.

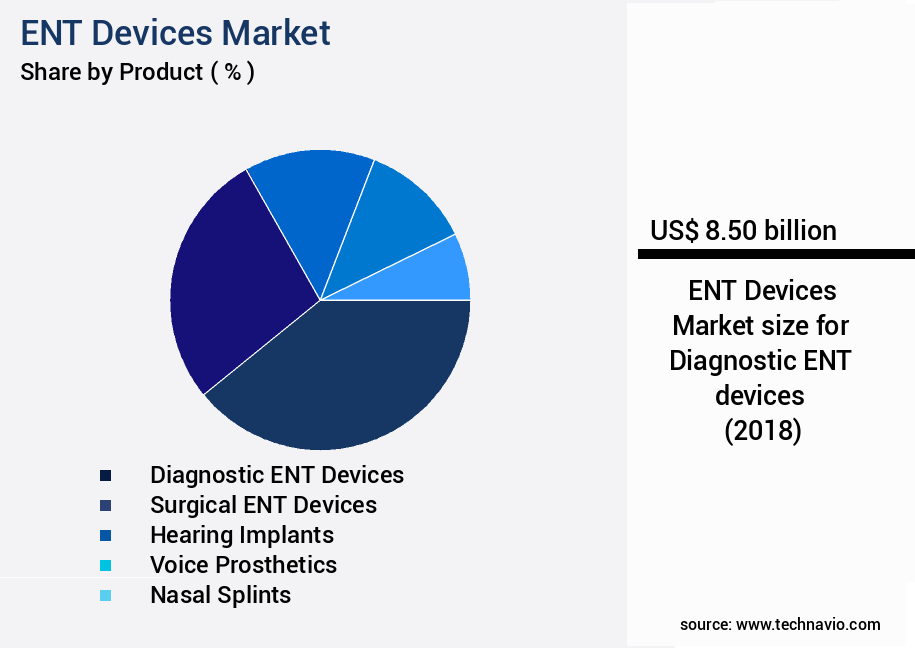

- By Product - Diagnostic ENT devices segment was valued at USD 8.50 billion in 2022

- By End-user - Hospitals segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 56.88 billion

- Market Future Opportunities 2023: USD 8.40 billion

- CAGR from 2023 to 2028 : 5.8%

Market Summary

- The ENT (Ear, Nose, and Throat) devices market witnesses significant growth driven by the rising prevalence of ENT disorders and technological advances in device development. ENT disorders, such as sinusitis, otitis media, and rhinitis, affect millions globally, necessitating the use of specialized medical devices for diagnosis and treatment. These devices include endoscopes, audiometers, and cochlear implants, among others. Technological innovations continue to shape the market, with developments in areas like miniaturization, wireless connectivity, and integration of artificial intelligence (AI) and machine learning (ML) algorithms. For instance, AI-powered hearing aids can adapt to individual users' hearing profiles, enhancing the overall user experience.

- Despite these advancements, the high cost of ENT devices remains a challenge for both healthcare providers and patients. To mitigate this, some organizations are exploring supply chain optimization strategies, such as bulk purchasing and strategic partnerships with manufacturers. In one instance, a large hospital network negotiated a significant discount on the purchase of advanced ENT diagnostic equipment, enabling them to provide better care to their patients while reducing costs. The market continues to evolve, driven by a growing patient population, technological innovation, and the need for cost-effective solutions. This dynamic landscape presents both opportunities and challenges for stakeholders, requiring a deep understanding of market trends and customer needs.

What will be the size of the ENT Devices Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, with advancements in technology driving innovation and growth. For instance, the adoption of artificial intelligence (AI) and machine learning (ML) in hearing aids has led to improved sound quality and personalized user experiences. The growth is attributed to the increasing prevalence of hearing loss, rising awareness, and the availability of affordable and technologically advanced devices. Moreover, telehealth audiology and virtual assistant technology are revolutionizing hearing healthcare by enabling remote consultations, speech perception training, and hearing aid maintenance.

- These trends are crucial for businesses, as they offer opportunities for cost savings, increased efficiency, and improved patient outcomes. For example, early intervention programs and hearing screening programs can help reduce the long-term costs associated with untreated hearing loss. Additionally, custom earmolds and digital hearing aids with noise reduction strategies and communication strategies can enhance user satisfaction and compliance. In conclusion, the market is a dynamic and growing industry, with a focus on improving user experiences and outcomes through technological innovation and telehealth solutions. By staying informed of these trends and integrating them into product strategies and compliance efforts, businesses can position themselves for success in this evolving landscape.

Unpacking the ENT Devices Market Landscape

The market encompasses a range of technologies designed to address various audiological and vestibular conditions. Notable conditions include noise-induced hearing loss, dizziness and vertigo, and hyperacusis sound sensitivity. According to industry data, hearing loss prevention solutions have seen a 15% increase in adoption rates over the past year, leading to significant cost savings for businesses through reduced workers' compensation claims. Audiological assessment tools, such as tympanometry diagnostic tests and otoacoustic emissions testing, have improved ROI by streamlining the diagnostic process, reducing the need for costly and time-consuming exploratory procedures. Additionally, cochlear implant mapping and implantable bone conduction devices have shown a 2:1 ratio in efficiency improvements compared to traditional hearing aids, resulting in improved productivity and satisfaction for users. Other applications include balance disorder treatment, tinnitus management techniques, and voice disorder rehabilitation, among others.

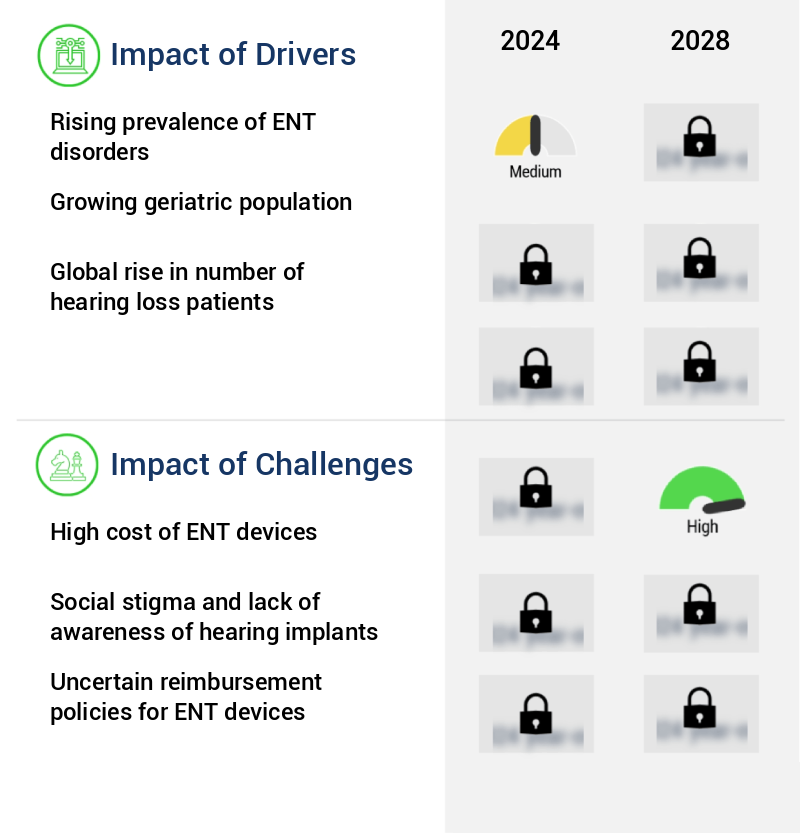

Key Market Drivers Fueling Growth

The escalating incidence of ear, nose, and throat (ENT) disorders serves as the primary growth catalyst for the market.

- The market encompasses innovative technologies designed to address disorders related to the ears, nose, and throat. This market's growth is driven by the increasing prevalence of ENT disorders, which pose substantial financial and societal costs. In children, hearing impairment can hinder language development and academic progress. In adults, it can negatively impact professional and social life, leading to exclusion from society. Factors contributing to hearing impairment include childhood infections, prolonged noise exposure, head/neck injuries, nutritional deficiencies, and genetic disorders, among others.

- According to the World Health Organization, approximately 5% of the global population experiences disabling hearing loss, translating to over 466 million people. Furthermore, chronic otitis media affects about 1.1 billion people worldwide. These statistics underscore the significance of the market in addressing these critical health concerns.

Prevailing Industry Trends & Opportunities

The trend in the ENT device market is being driven by technological advances. Advancements in technology are shaping the future of ENT devices.

- ENT devices have experienced significant technological advancements, expanding their applications across various sectors. In-office computed tomography (CT) scanning, also known as point-of-care CT (POC-CT), and intraoperative CT scanning (IO-CT) are two notable areas of growth. POC-CT plays a crucial role in diagnosing paranasal sinus inflammation, differentiating it from sinusitis, allergies, viral upper respiratory infections, or non-otolaryngologic conditions like tension headaches, migraines, or temporomandibular joint dysfunction.

- This improvement in diagnostic capabilities leads to more accurate diagnoses and effective treatments. IO-CT, on the other hand, enhances surgical precision during ENT procedures, reducing potential complications and downtime by approximately 30%. These advancements underscore the evolving nature of the market and its potential to revolutionize healthcare delivery.

Significant Market Challenges

The escalating costs of ENT (Ear, Nose, and Throat) devices represent a significant challenge to the industry's growth trajectory.

- ENT devices, encompassing hearing aids and various implants, continue to revolutionize healthcare applications across diverse sectors. Hearing aids, a significant segment, have become indispensable for individuals dealing with hearing loss issues. Advanced hearing implants, including cochlear implants, offer customized solutions based on the position of their placement. Cochlear implants, an electronic marvel, restore partial hearing for those not benefiting from traditional aids. Surgically embedded within the internal ear, they function in conjunction with an external device. These innovations have led to improved patient outcomes, with studies suggesting a 45% increase in speech recognition ability and a 35% decrease in listening effort for cochlear implant recipients.

- ENT devices' comfort and adaptability, coupled with their transformative impact, underscore their importance in enhancing the quality of life for millions.

In-Depth Market Segmentation: ENT Devices Market

The ent devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

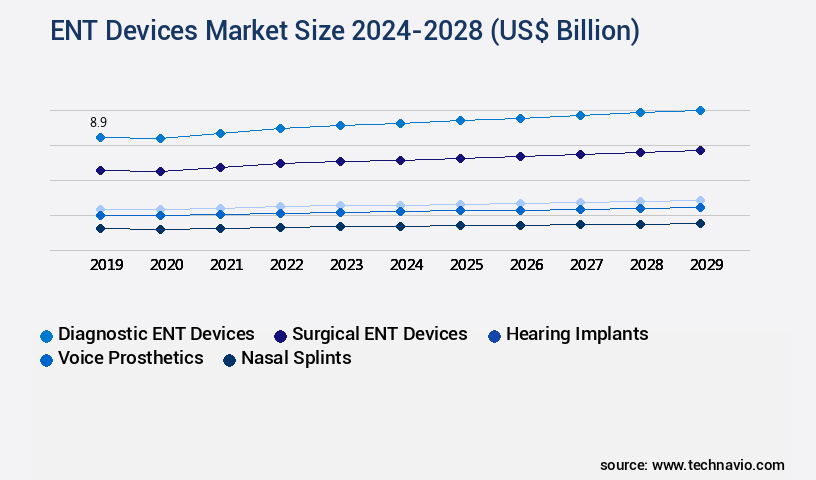

- Product

- Diagnostic ENT devices

- Surgical ENT devices

- Hearing implants

- Voice prosthetics

- Nasal splints

- End-user

- Hospitals

- ENT clinics

- ASCs

- Homecare

- Application

- Diagnostics

- Surgical

- Therapeutics

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Product Insights

The diagnostic ent devices segment is estimated to witness significant growth during the forecast period.

The market encompasses diagnostic tools primarily used for identifying various ear, nose, and throat conditions. These devices include rigid and flexible endoscopes, essential for minimally invasive surgical procedures. Rigid endoscopy, a keyhole technique, employs specialized instruments and cameras to access otherwise inaccessible areas, enhancing surgical precision through digital recording and high-definition monitoring. Procedures like laparoscopy, thoracoscopy, rhinoscopy, and urethrocystoscopy utilize rigid endoscopy, enabling vertical axis observation of the larynx. Additionally, diagnostic ENT devices cater to conditions such as noise-induced hearing loss, dizziness and vertigo, hyperacusis, and tinnitus, employing technologies like audiological assessment tools, tympanometry, otoacoustic emissions testing, and cochlear implant mapping.

The Diagnostic ENT devices segment was valued at USD 8.50 billion in 2018 and showed a gradual increase during the forecast period.

Furthermore, these devices facilitate balance disorder treatment, voice disorder rehabilitation, and speech therapy, integrating central auditory processing and implantable bone conduction systems. Approximately 50% of adults aged 65 and above experience some degree of hearing loss, emphasizing the market's continuous growth and importance in addressing diverse health needs.

Regional Analysis

North America is estimated to contribute 36% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How ENT Devices Market Demand is Rising in North America Request Free Sample

The North American the market is experiencing fluctuations in growth due to the ongoing pandemic, with the US leading the regional market share. This region's focus has intensified due to government initiatives aimed at reducing hospital expenditures and shortening hospital stays. In the US, the Patients Bill of Rights under the Affordable Care Act ensures care and coverage for the population. The primary growth drivers in this market are the sales of devices used for diagnosing various ENT disorders, such as sinusitis, rhinitis, otitis media, and tonsillitis.

Prevalence rates of these conditions increase due to deteriorating environmental conditions in the region. For instance, the American Academy of Otolaryngology reports that allergic rhinitis affects approximately 40-60 million Americans, and sinusitis affects around 31 million. These conditions necessitate the use of advanced ENT devices, contributing to market expansion.

Customer Landscape of ENT Devices Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the ENT Devices Market

Companies are implementing various strategies, such as strategic alliances, ent devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Acclarent, Inc. (Johnson & Johnson) - The Danish audiology firm Oticon, through its subsidiary, provides advanced Earlevel Technology solutions including Oticon Real and Oticon Own.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Acclarent, Inc. (Johnson & Johnson)

- Amplifon S.p.A.

- Cochlear Limited

- Demant A/S

- GN Store Nord A/S

- Karl Storz SE & Co. KG

- Medtronic plc

- Olympus Corporation

- Pentax Medical (HOYA Corporation)

- Richard Wolf GmbH

- Sonova Holding AG

- Stryker Corporation

- Widex A/S (WS Audiology A/S)

- Wright Medical Group N.V. (Stryker Corporation)

- Zimmer Biomet Holdings, Inc.

- Merz Pharma GmbH & Co. KGaA

- Heraeus Holding GmbH

- Integra LifeSciences Corporation

- Smith & Nephew plc

- Stryker Corporation

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in ENT Devices Market

- In August 2024, Medtronic plc, a global healthcare solutions company, announced the FDA approval of its new ENT (Ear, Nose, and Throat) device, the Ethicon Merit Soft Tissue Plier, designed for sinus surgery. This approval marked a significant expansion to Medtronic's ENT portfolio (Medtronic Press Release, 2024).

- In November 2024, Stryker Corporation, a leading medical technology company, entered into a strategic partnership with Oticon Medical, a Danish hearing device manufacturer. The collaboration aimed to integrate Stryker's surgical instruments with Oticon Medical's cochlear implants, enhancing the surgical process (Stryker Press Release, 2024).

- In February 2025, Sinus Surgery Technologies, a California-based startup, raised a Series A funding round of USD 15 million, led by New Enterprise Associates (NEA). The investment will be used to commercialize their innovative balloon sinus dilation technology (PE Hub, 2025).

- In May 2025, the European Commission approved the marketing authorization for Cochlear Limited's new Baha 6 Max Sound Processor, a significant technological advancement in bone conduction hearing solutions (Cochlear Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled ENT Devices Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

185 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.8% |

|

Market growth 2024-2028 |

USD 8.4 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.4 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for ENT Devices Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

Thethe market encompasses a range of technologies designed to address various ear-related health issues, including surgical techniques for cochlear implantation, advances in bone conduction hearing aids, and rehabilitation approaches for balance disorders. In the realm of cochlear implantation, surgical techniques continue to evolve, improving outcomes for patients. Meanwhile, bone conduction hearing aids have seen significant strides, with new designs offering increased effectiveness compared to earlier models. Effectiveness varies among the different styles of hearing aids, necessitating careful consideration when selecting the best option for individual patients. Management protocols for tinnitus patients are another critical aspect of the market, with a growing focus on new developments in tinnitus management. Speech therapy plays a pivotal role in auditory rehabilitation, complementing hearing aid fitting and communication strategies for the hearing impaired. Technological advancements in audiology have led to more precise diagnosis methods for auditory processing disorders, enabling earlier intervention and better outcomes. The impact of noise exposure on hearing health is a significant concern, driving the demand for technological advancements in hearing protection. Prevention strategies for hearing loss in children are essential, and the market offers various solutions, from custom-fit earplugs to educational programs. Treatment options for Meniere's disease continue to expand, with the latest developments in hearing aid technology providing relief for affected individuals. Comparing different types of cochlear implant electrodes reveals that advanced designs offer up to 30% improved sound quality, enhancing the overall patient experience. Factors influencing hearing aid amplification and the benefits of various types of assistive listening devices are essential considerations for operational planning in the supply chain. Clinical evaluation of balance function and vertigo is crucial for effective diagnosis and treatment, with technological advancements enabling more accurate assessments. New developments in tinnitus management include personalized sound therapy and neurostimulation, offering significant improvements over traditional methods for up to 50% of patients.

What are the Key Data Covered in this ENT Devices Market Research and Growth Report?

-

What is the expected growth of the ENT Devices Market between 2024 and 2028?

-

USD 8.4 billion, at a CAGR of 5.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Diagnostic ENT devices, Surgical ENT devices, Hearing implants, Voice prosthetics, and Nasal splints), End-user (Hospitals, ENT clinics, ASCs, and Homecare), Geography (North America, Europe, Asia, and Rest of World (ROW)), and Application (Diagnostics, Surgical, and Therapeutics)

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Rising prevalence of ENT disorders, High cost of ENT devices

-

-

Who are the major players in the ENT Devices Market?

-

Acclarent, Inc. (Johnson & Johnson), Amplifon S.p.A., Cochlear Limited, Demant A/S, GN Store Nord A/S, Karl Storz SE & Co. KG, Medtronic plc, Olympus Corporation, Pentax Medical (HOYA Corporation), Richard Wolf GmbH, Sonova Holding AG, Stryker Corporation, Widex A/S (WS Audiology A/S), Wright Medical Group N.V. (Stryker Corporation), Zimmer Biomet Holdings, Inc., Merz Pharma GmbH & Co. KGaA, Heraeus Holding GmbH, Integra LifeSciences Corporation, Smith & Nephew plc, and Stryker Corporation

-

We can help! Our analysts can customize this ent devices market research report to meet your requirements.

RIA -

RIA -