Enteral Feeding Devices Market Size 2024-2028

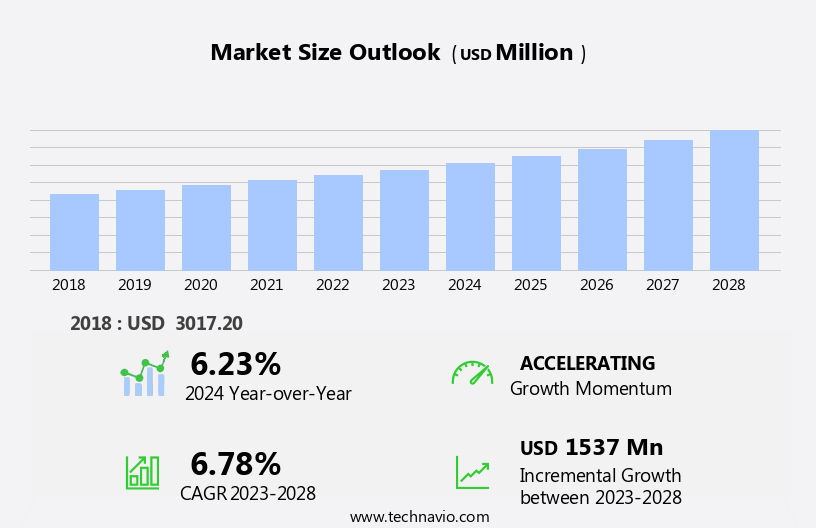

The enteral feeding devices market size is forecast to increase by USD 1.54 billion at a CAGR of 6.78% between 2023 and 2028.

- The enteral feeding devices market is witnessing significant growth, driven by the rising prevalence of chronic conditions and preterm births, which necessitate nutritional support solutions. Additionally, the growing demand for wireless enteral feeding devices is enhancing patient convenience and mobility, allowing for more flexible care.However, frequent product recalls remain a challenge, pushing manufacturers to emphasize safety, quality, and compliance in product development. As the market evolves, addressing these challenges while leveraging technological advancements will be key to sustained growth.

- ALCOR Scientific is a leading provider of enteral feeding devices, offering the SENTINELplus Enteral Feeding Pump. This advanced system features dual display screens and intuitive alarm systems, ensuring accurate and efficient enteral nutrition delivery for patients with gastrointestinal disorders or those unable to consume food orally. By prioritizing precision and patient comfort, the company enhances clinical outcomes and overall healthcare efficiency.

What will be the Size of the Enteral Feeding Devices Market During the Forecast Period?

- The market encompasses a range of products used to deliver nutrients directly into the digestive system, bypassing the mouth and stomach. This market caters to various patient populations, including those with gastrointestinal diseases, geriatric populations, chronic illnesses such as diabetes, Parkinson's, Alzheimer's disease, osteoporosis, and osteoarthritis, as well as pediatric and neonatal patients.

- Factors driving market growth include the increasing prevalence of chronic diseases, complications from surgical trauma in Intensive Care Units (ICUs), and the need for alternative nutrition methods for patients with swallowing difficulties or breathing issues. Enteral feeding devices include tri-funnel replacement g-tubes, j-tubes, enteral feeding pumps, and enteral feeding tubes.

- Technological advancements in bolus delivery systems, human milk fortifiers, and parenteral nutrition therapies continue to shape the market landscape. Complications from enteral feeding, such as tube misplacement, leakage, and infection, remain challenges to market growth. The market is expected to witness significant expansion due to the increasing focus on improving patient outcomes and reducing healthcare costs associated with parenteral nutrition.

How is this Enteral Feeding Devices Industry segmented and which is the largest segment?

The enteral feeding devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Hospitals

- Homecare

- Product

- Accessories

- Enteral pumps

- Age Group

- Adults

- Pediatrics

- Indication

- Alzheimer's

- Nutrition Deficiency

- Cancer Care

- Diabetes

- Chronic Kidney Diseases

- Orphan Diseases

- Dysphagia

- Pain Management

- Malabsorption/GI Disorder/Diarrhea

- Others

- Geography

- North America

- Canada

- US

- Europe

- UK

- Asia

- China

- Japan

- Rest of World (ROW)

- North America

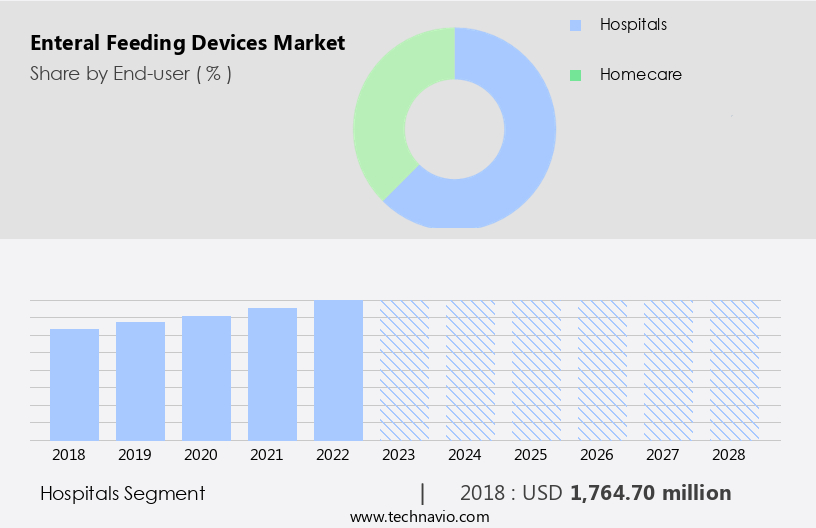

By End-user Insights

- The hospitals segment is estimated to witness significant growth during the forecast period.

Enteral feeding devices are essential medical tools used in hospitals to provide nutritional support to patients who cannot consume food orally due to medical conditions or surgical interventions. These devices are commonly used in intensive care units (ICUs), surgical wards, and specialized units to deliver essential nutrients and medications to patients. The rising prevalence of chronic illnesses, including cancer, neurological disorders such as Parkinson's disease, Alzheimer's disease, and motor neuron disease, and gastrointestinal diseases, has increased the demand for enteral feeding devices in hospital settings. Patients with severe pancreatitis, diabetes, cystic fibrosis, inflammatory bowel disease, sepsis, anorexia, and other chronic diseases often require long-term enteral support.

Enteral feeding devices include tri-funnel replacement G-tubes, J-tubes, enteral feeding pumps, and enteral feeding tubes. Complications such as tube feeding complications, human milk use, swallowing difficulties, suckling problems, and breathing issues are common concerns in enteral feeding. Enteral nutrition and parenteral nutrition are two common feeding therapies used in clinical settings. Enteral feeding tubes are placed In the stomach, duodenum, jejunum, or endoscopically, depending on the patient's condition and the location of the gastrointestinal tract damage. Home healthcare services, enterostomy feeding tubes, and federal funding are essential considerations for long-term enteral support. Reverse balloon designs are an innovative solution for adult patients with complex clinical problems, including swallowing difficulties and nutritional problems. Enteral feeding devices are crucial in maintaining balanced nutritional intake and improving healthcare costs for patients with chronic diseases.

Get a glance at the Enteral Feeding Devices Industry report of share of various segments Request Free Sample

The Hospitals segment was valued at USD 1.76 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

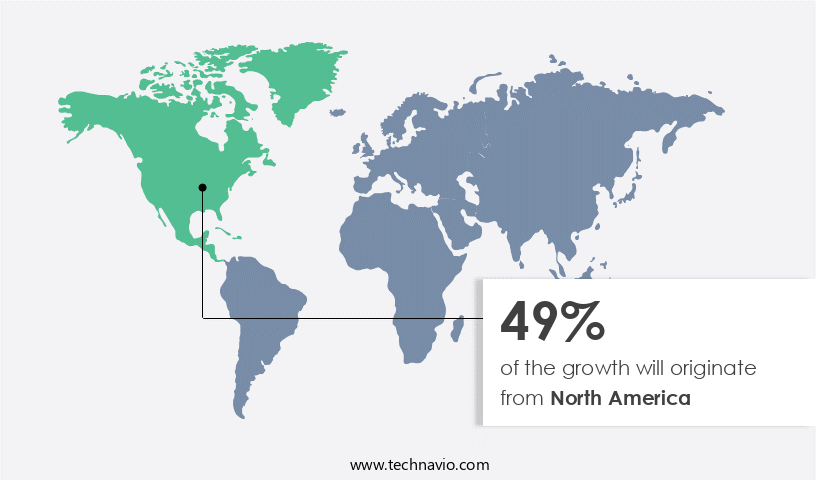

- North America is estimated to contribute 49% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The North American market for enteral feeding devices is poised for steady expansion due to several key drivers. These include the escalating prevalence of chronic conditions, such as neurological disorders and cancer, which necessitate enteral feeding. For instance, in 2023, over 11,500 new laryngeal cancer cases and nearly 55,000 new oral cavity, pharynx, and other cancer cases were diagnosed In the US. Moreover, the increasing number of product launches featuring advanced technologies and the growing presence of regional and global companies are further fueling market growth. Additionally, initiatives by government and non-profit organizations to raise awareness about enteral feeding are also contributing to market expansion.

Enteral feeding is a critical component of healthcare provision in both acute hospitals and community settings for managing clinical problems and nutritional issues. Healthcare costs associated with chronic diseases and the adoption of enteral feeding devices are significant, making reimbursement policies and third-party payer coverage essential considerations for market growth. Enteral feeding devices are used in various parts of the gastrointestinal tract, including the abdominal wall, stomach, duodenum, jejunum, and endoscopy, laparoscopy, and open surgery sites. Federal funding and home healthcare services also play a crucial role In the market's growth.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Enteral Feeding Devices Industry?

Increasing prevalence of chronic conditions and preterm birth is the key driver of the market.

- The global market for enteral feeding devices is experiencing significant growth due to the increasing prevalence of chronic conditions, such as cancers and neurological disorders, as well as preterm births. Oral cancer, which develops on the tongue, oral mucosa, mouth, and oropharynx, is a major contributor to this trend. The primary causes of oral cancer are smoking and excessive alcohol consumption. In the US, throat cancer accounts for approximately 3% of all new cancer cases each year, and the global market for throat cancer therapeutics has seen a notable expansion in recent years. Enteral feeding devices are essential for individuals with gastrointestinal diseases, severe pancreatitis, diabetes, and other chronic illnesses, including Parkinson's disease, nervous system disorders, Alzheimer's disease, osteoporosis, and osteoarthritis.

- These devices are also used in surgical trauma ICUs, pediatric and neonatal patients, and those with congenital genetic disorders and rare genetic diseases such as Prader-Willi Syndrome. Enteral feeding pumps, tubes, and replacement G-tubes (tri-funnel and J-tubes) are commonly used for tube feeding, while parenteral nutrition and enteral nutrition provide balanced nutritional intake for patients with swallowing, suckling, breathing, and bolus delivery complications. Complications from enteral feeding can include tube misplacement, tube blockages, and infection, among others. Enteral feeding devices are used in both acute hospitals and community settings, and their adoption is influenced by reimbursement policies, third-party payers, and federal funding.

- Home healthcare services and enterostomy feeding tubes are also gaining popularity for long-term enteral support. Reverse balloon designs and adult patients are segments of the market that are experiencing growth, with the children segment also showing significant potential. Diseases such as multiple sclerosis, liver disease, motor neuron disease, sepsis, anorexia, cystic fibrosis, dementia, and inflammatory bowel disease are among those that can benefit from enteral feeding therapies. The healthcare provision landscape is continuously evolving, and enteral feeding devices play a crucial role in addressing the nutritional needs of patients with various clinical problems.

What are the market trends shaping the Enteral Feeding Devices Industry?

Increasing demand for wireless enteral feeding devices is the upcoming market trend.

- The market is witnessing significant growth due to the increasing prevalence of chronic diseases, particularly among the geriatric population. Diabetes, severe pancreatitis, gastrointestinal diseases, and nervous system disorders such as Parkinson's and Alzheimer's disease are driving the demand for enteral feeding devices. In surgical trauma ICUs, tri-funnel replacement G-tubes and J-tubes are commonly used for enteral feeding. According to NCBI studies, enteral nutrition is preferred over parenteral nutrition for chronic illnesses due to its ability to maintain a balanced nutritional intake and reduce complications. Enteral feeding pumps and tubes are essential for pediatric and neonatal patients, especially those with congenital genetic disorders, rare genetic diseases, and swallowing disorders.

- Complications such as morbidity and neonatal mortality can be minimized through tube feeding, especially in pre-term infants. Enteral feeding devices are used in various healthcare settings, including acute hospitals and community settings, for patients with clinical problems related to swallowing, suckling, breathing, bolus delivery, and human milk feeding. The adoption of enteral feeding devices is influenced by reimbursement policies and third-party payers. Federal funding for home healthcare services and the availability of enterostomy feeding tubes have also contributed to the growth of the market. The market is segmented into adult patients and children, with chronic diseases such as multiple sclerosis, liver disease, motor neuron disease, sepsis, anorexia, cystic fibrosis, dementia, inflammatory bowel disease, and cancer being the major indications.

- Technological advancements, such as reverse balloon designs, long-term enteral support, and wireless connectivity, are expected to further drive the growth of the market.

What challenges does the Enteral Feeding Devices Industry face during its growth?

Frequent product recalls is a key challenge affecting the industry growth.

- The market In the healthcare industry is driven by the increasing prevalence of chronic illnesses such as diabetes, severe pancreatitis, gastrointestinal diseases, neurological disorders including Parkinson's and Alzheimer's disease, osteoporosis, and osteoarthritis, among others. According to NCBI studies, enteral feeding is an essential nutritional support option for patients with swallowing difficulties due to clinical problems like stroke, brain injury, or nervous system disorders. Enteral feeding devices, including tri-funnel replacement G-tubes, J-tubes, enteral feeding pumps, and enteral feeding tubes, are used in various clinical settings such as surgical trauma ICUs, home healthcare services, and long-term care facilities. These devices are crucial for providing balanced nutritional intake to patients with chronic diseases, pre-term infants, neonatal patients, and pediatric patients with congenital genetic disorders or rare genetic diseases like Prader-Willi Syndrome.

- Complications from enteral feeding, such as tube misplacement, tube blockage, and feeding intolerance, can lead to morbidity and increased healthcare costs. To mitigate these risks, enteral feeding pumps and tubes are continually being improved with advanced technologies like reverse balloon designs and bolus delivery systems. Parenteral nutrition and enteral nutrition are alternative feeding methods used when enteral feeding is not feasible. Parenteral feeding therapies involve delivering nutrients directly into a patient's bloodstream, while enteral feeding tubes are used to deliver nutrients into the stomach, duodenum, jejunum, or other parts of the gastrointestinal tract through endoscopy, laparoscopy, or open surgery.

- The adult patients segment and the age group segment, including children, account for a significant portion of the market. Chronic diseases such as multiple sclerosis, liver disease, motor neuron disease, Parkinson's disease, sepsis, anorexia, cystic fibrosis, dementia, and inflammatory bowel disease are common indications for enteral feeding devices. The adoption of enteral feeding devices is influenced by reimbursement policies, third-party payers, and federal funding. Enterostomy feeding tubes are used for abdominal wall access, while human milk is often used for neonatal patients. Clinical problems and nutritional problems are the primary drivers for the use of enteral feeding devices in acute hospitals and community settings.Balanced nutritional intake is essential for maintaining patient health and reducing healthcare costs.

Exclusive Customer Landscape

The enteral feeding devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the enteral feeding devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, enteral feeding devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ALCOR Scientific

- Amsino International Inc.

- Applied Medical Technology Inc.

- Avanos Medical Inc.

- B.Braun SE

- Becton Dickinson and Co.

- Boston Scientific Corp.

- Canafusion Technologies Inc.

- Cardinal Health Inc.

- Conmed Corp.

- Cook Group Inc.

- Danone SA

- Fresenius SE and Co. KGaA

- HMC Premedical Spa

- Medela AG

- Medline Industries LP

- Moog Inc.

- Shenzhen Bestman Instrument Co. Ltd.

- Trendlines Group Ltd.

- Vygon SAS

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Enteral feeding devices refer to medical devices used to deliver nutrients directly into the gastrointestinal tract (GI tract) through a tube. These devices are essential for individuals who are unable to consume food orally due to various clinical conditions, such as gastrointestinal diseases, severe pancreatitis, surgical trauma in Intensive Care Units (ICUs), neurological disorders, genetic disorders, and chronic illnesses. The market is driven by the increasing geriatric population, which is more susceptible to chronic diseases and nutritional deficiencies. Diabetes, osteoporosis, osteoarthritis, and Alzheimer's disease are some of the common chronic conditions that require long-term enteral support. Furthermore, the rise In the prevalence of severe gastrointestinal diseases, such as inflammatory bowel disease, cystic fibrosis, and cancer, also contributes to the market growth.

Enteral feeding devices are available in various forms, including enteral feeding pumps, enteral feeding tubes, and enterostomy feeding tubes. The choice of device depends on the patient's clinical condition, age, and the duration of nutritional support required. For instance, tube feeds are suitable for short-term support, while long-term enteral support may require the use of reverse balloon designs or enterostomy feeding tubes. The market for enteral feeding devices is segmented based on patient segments and types of devices. The adult patients segment accounts for the largest share of the market due to the high prevalence of chronic diseases and the increasing aging population.

The children segment, which includes neonatal and pediatric patients, is expected to grow at a significant rate due to the increasing incidence of pre-term births and congenital genetic disorders. The market is characterized by the presence of several players, including large multinational corporations and small and medium-sized enterprises. The market is highly competitive, with companies constantly innovating to improve the design and functionality of their products. For instance, some companies are developing tri-funnel replacement G-tubes and J-tubes with advanced features, such as improved bolus delivery and compatibility with human milk. The market for enteral feeding devices is also influenced by various factors, including clinical problems, nutritional problems, healthcare costs, reimbursement policies, and third-party payers.

For instance, the adoption of enteral feeding devices in home healthcare services and acute hospitals is influenced by the availability of federal funding and the cost-effectiveness of these devices compared to parenteral nutrition. The use of enteral feeding devices is not without complications, such as tube misplacement, tube blockage, and tube leakage. Therefore, there is a growing focus on developing devices with advanced features, such as endoscopic and laparoscopic placement, and open surgery, to minimize these complications. In conclusion, the market is expected to grow significantly due to the increasing prevalence of chronic diseases and the need for long-term nutritional support.

The market is highly competitive, with companies constantly innovating to improve the design and functionality of their products. The market is also influenced by various factors, including clinical problems, nutritional problems, healthcare costs, reimbursement policies, and third-party payers.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

163 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.78% |

|

Market growth 2024-2028 |

USD 1537 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.23 |

|

Key countries |

US, UK, Canada, China, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Enteral Feeding Devices Market Research and Growth Report?

- CAGR of the Enteral Feeding Devices industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the enteral feeding devices market growth of industry companies

We can help! Our analysts can customize this enteral feeding devices market research report to meet your requirements.

RIA -

RIA -