Europe Body Bags Market Size 2026-2030

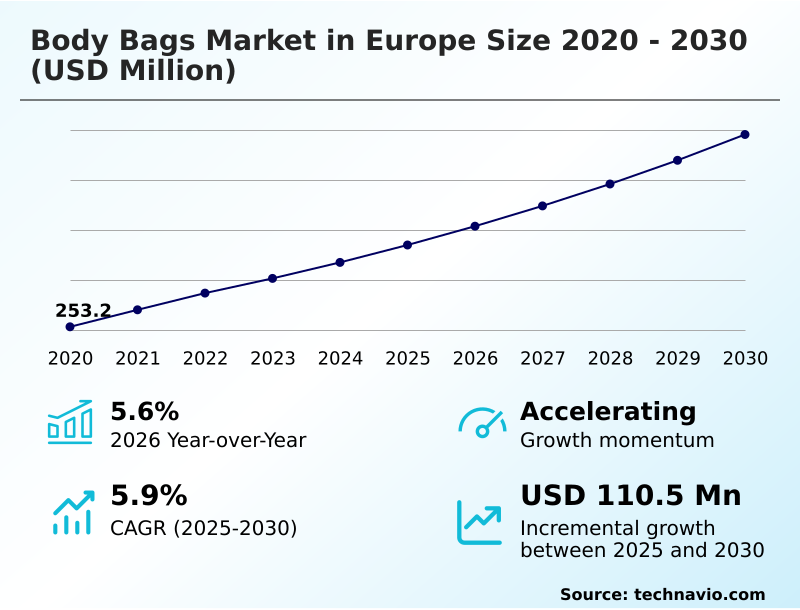

The europe body bags market size is valued to increase by USD 110.5 million, at a CAGR of 5.9% from 2025 to 2030. Increasing prevalence of chronic diseases will drive the europe body bags market.

Major Market Trends & Insights

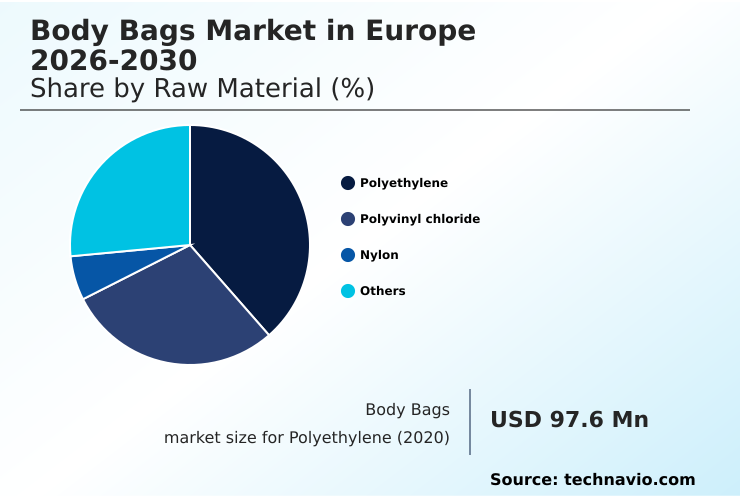

- By Raw Material - Polyethylene segment was valued at USD 123.4 million in 2024

- By End-user - Morgue segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 192.3 million

- Market Future Opportunities: USD 110.5 million

- CAGR from 2025 to 2030 : 5.9%

Market Summary

- The body bags market in Europe is evolving beyond a reactive supply model, driven by an aging population and the corresponding increase in mortality from chronic diseases. This creates a stable baseline demand from hospitals and morgues, which is now augmented by a proactive focus on public health preparedness and disaster resilience.

- A key trend is the industry's pivot toward sustainability, with a growing preference for eco-friendly and biodegradable material to replace traditional plastics, aligning with stricter environmental regulations. Innovations are centered on enhancing product functionality, including the development of a bariatric body bag with superior tensile strength and a specialized human remains pouch that guarantees forensic evidence preservation.

- For instance, a large hospital network might implement a new procurement strategy to balance costs with compliance, sourcing chlorine-free polymer bags for general use while maintaining a strategic stockpile of heavy-duty disaster response pouch models.

- This approach optimizes inventory for both routine mortuary supplies and mass casualty incident scenarios, ensuring both regulatory adherence and operational readiness without compromising on the dignified handling of remains or infection control.

What will be the Size of the Europe Body Bags Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Europe Body Bags Market Segmented?

The europe body bags industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

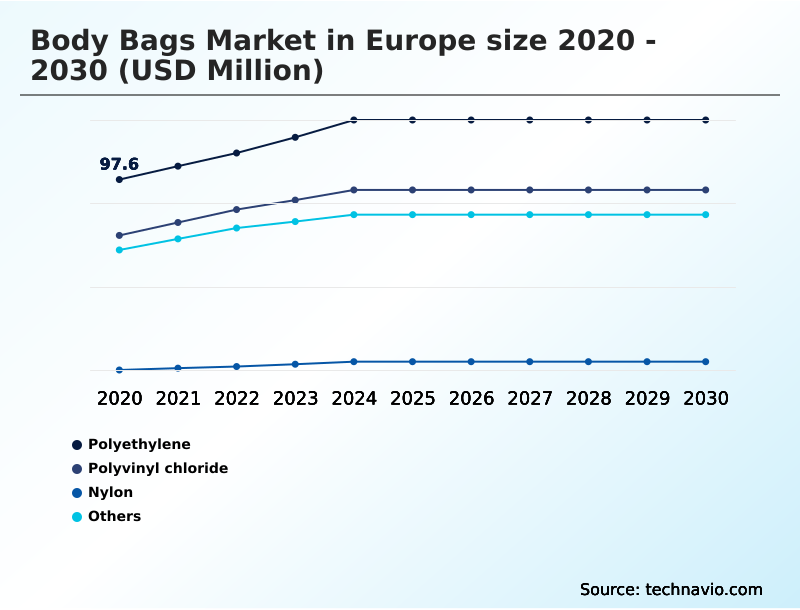

- Raw material

- Polyethylene

- Polyvinyl chloride

- Nylon

- Others

- End-user

- Morgue

- Hospital

- Others

- Type

- Adult bags

- Heavy duty and bariatric bags

- Child or infant bags

- Geography

- Europe

- Germany

- Italy

- Europe

By Raw Material Insights

The polyethylene segment is estimated to witness significant growth during the forecast period.

The polyethylene segment's market dominance is rooted in its economic viability and functional adaptability, making it a primary choice for high-volume centralized procurement of mortuary supplies.

As a chlorine-free polymer, polyethylene aligns with stringent European regulatory compliance for waste incineration, avoiding harmful emissions and supporting regional waste reduction goals. This material provides a reliable balance of fluid resistance and tensile strength for routine applications.

Innovations in recycled polyethylene are enhancing its role within circular economy principles, with some advanced formulations showing a 15% improvement in durability.

This ensures better mortuary equipment integration and logistical efficiency without compromising core performance, reinforcing its position as the standard for non-porous materials and securing its product certification across numerous health systems.

The Polyethylene segment was valued at USD 123.4 million in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Procurement strategies in the European market are becoming increasingly specialized, moving beyond one-size-fits-all solutions to address specific end-user requirements. The demand for heavy duty bariatric body bags, for instance, has grown at nearly double the rate of standard products, driven by public health trends and the need for safer manual handling protocols in mortuaries.

- This reflects a broader shift towards fit-for-purpose equipment. Similarly, the call for eco-friendly biodegradable body bags is reshaping supply chains, as healthcare systems and funeral services align with circular economy principles and green burial practices.

- In forensic applications, the forensic use human remains pouch is now a critical tool, with features like tamper-evident seals and material inertness being non-negotiable for maintaining the chain of custody. For routine hospital use and disaster preparedness, chlorine-free polymer body bags are becoming the standard to ensure compatibility with modern incineration facilities and reduce harmful emissions.

- This specialization extends to crisis management, where dedicated body bags for disaster response are pre-positioned in strategic stockpiles, featuring ruggedized construction and rapid-deployment packaging to ensure operational readiness during large-scale emergencies. This fragmentation of demand requires manufacturers to maintain a diverse and technically advanced product portfolio.

What are the key market drivers leading to the rise in the adoption of Europe Body Bags Industry?

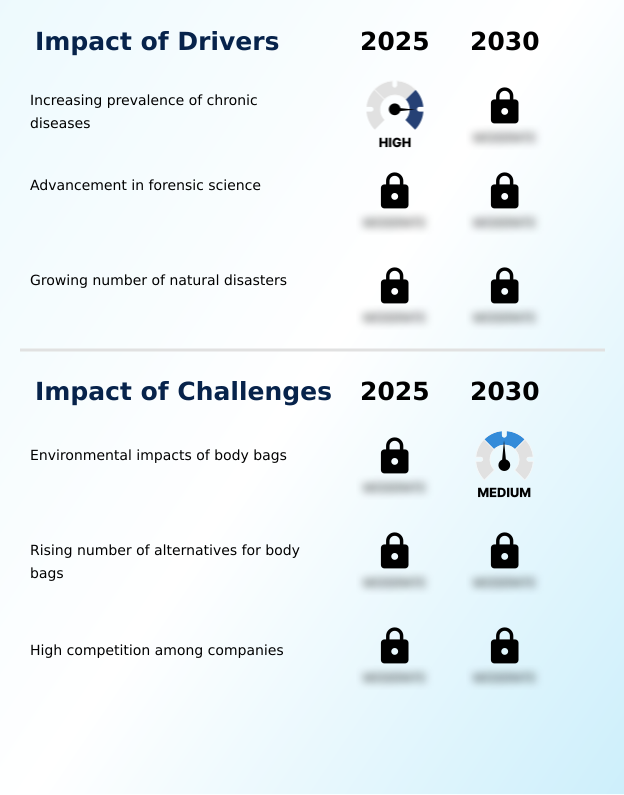

- The rising prevalence of chronic diseases, a leading cause of mortality in Europe, is a significant driver for sustained demand in the body bags market.

- Key market drivers are increasingly tied to public health preparedness and forensic accuracy.

- A heightened focus on disaster resilience has spurred a 35% rise in the strategic stockpiling of essential supplies like the disaster response pouch, crucial for mass casualty incident response. This is guided by comprehensive emergency response planning.

- Simultaneously, advancements in forensic investigation support have created demand for products that ensure evidence integrity, with specifications now requiring a higher weight capacity rating. This drives a need for improved post-mortem handling techniques and robust supply chain resilience.

- As a result, public health preparedness and the need for reliable disaster victim identification are fundamentally shaping procurement strategies and product specifications.

What are the market trends shaping the Europe Body Bags Industry?

- An increase in traffic-related fatalities across Europe is heightening the demand for reliable and hygienic body containment solutions. This trend is driving the need for durable materials and standardized handling protocols within emergency response and healthcare systems.

- A pronounced shift toward enhanced hygiene and sustainability is reshaping product development. The demand for advanced infection control features has driven a 40% increase in the adoption of bags with microbial-barrier film and superior thermal bonding capability. This emphasis on hygienic handling protocols is prompting a move away from traditional polyvinyl chloride toward alternatives like ethylene vinyl acetate (EVA).

- Concurrently, the focus on sustainable disposal solutions has spurred interest in biodegradable material, with group purchasing organizations (GPOs) now specifying materials with proven environmental stress cracking resistance. Innovations in material traceability and the integration of heavy-duty zippers with a tamper-evident seal are becoming standard, enhancing security and accountability in post-mortem transfers.

What challenges does the Europe Body Bags Industry face during its growth?

- Growing environmental concerns regarding the disposal of traditional plastic-based body bags present a significant challenge, compelling the industry to innovate with sustainable materials and disposal methods.

- The industry faces significant challenges in balancing performance with environmental responsibility and cost. Adherence to a green procurement policy is driving a shift away from materials with high environmental impact, but alternatives that offer comparable puncture resistance, like nylon, come at a premium, increasing costs by up to 18%.

- This complexity is amplified for the bariatric body bag segment, where strength is non-negotiable. Furthermore, stringent biohazard waste management regulations and occupational health and safety standards dictate cadaver bag specification, requiring materials with proven chemical inertness for long-term preservation. This creates a complex operational landscape, forcing a re-evaluation of material use to achieve environmental impact reduction without compromising safety.

Exclusive Technavio Analysis on Customer Landscape

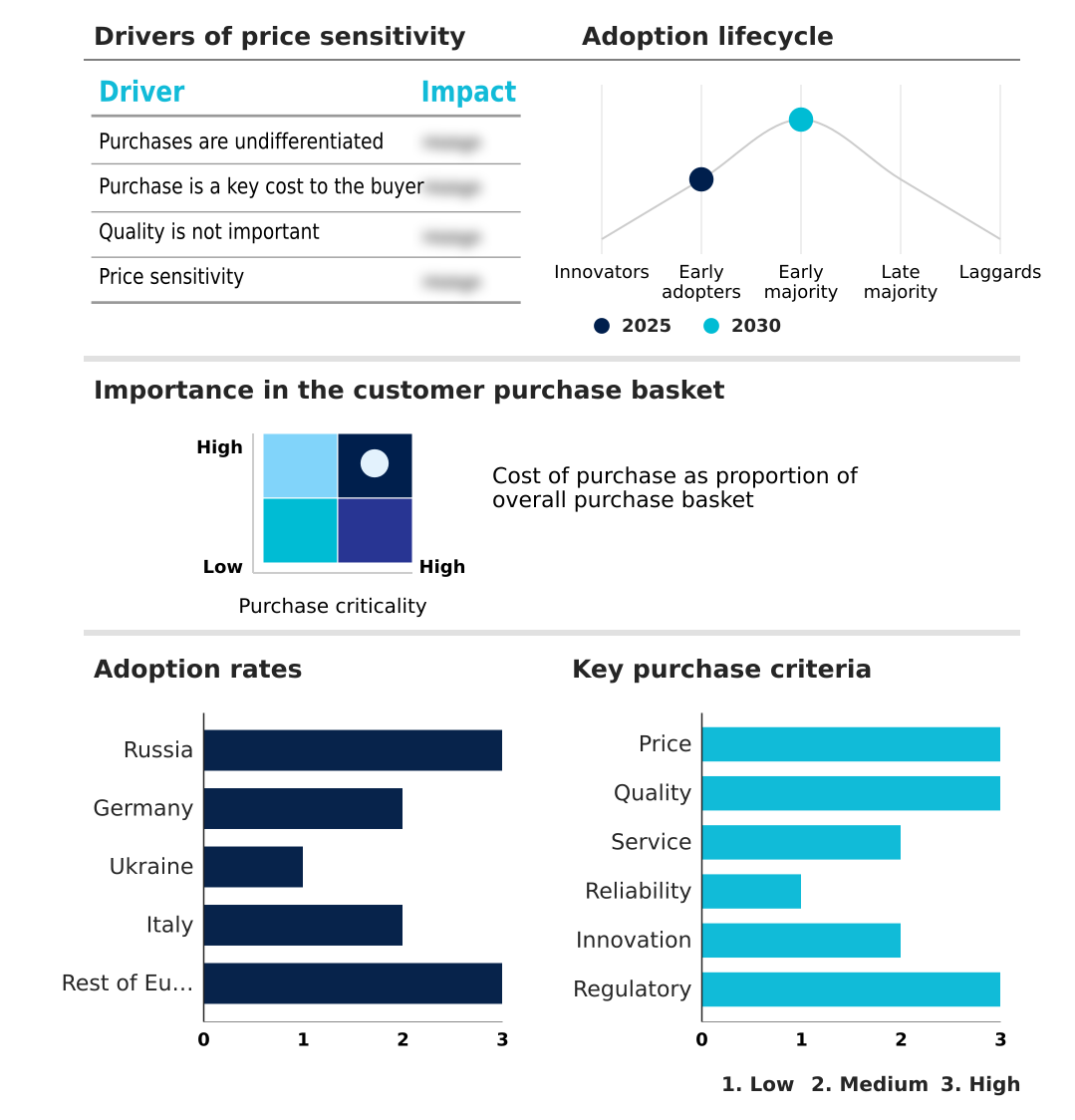

The europe body bags market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the europe body bags market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Europe Body Bags Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, europe body bags market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3D Barrier Bags Inc. - Specialized containment solutions include standard cadaver bags, bariatric disaster pouches, and forensic-grade human remains pouches, meeting diverse post-mortem handling and evidentiary requirements.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3D Barrier Bags Inc.

- Auden Funeral Supplies Ltd.

- Body Bag

- Boen Healthcare Co. Ltd.

- CEABIS

- EIHF ISOFROID

- HYGECO International SA

- Jiangsu Rooe Medical

- Mortech Manufacturing

- MP Acquisition LLC

- MuHeSa Verpackungsmittel

- Polcreative Group

- Slik Pak Ltd.

- Synrein Medical

- Wye Valley manufacturing Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Europe body bags market

- In September 2024, Polcreative Group launched its new line of Bio-Compostable body bags, certified to EN 13432 standards, addressing growing demand for sustainable disposal solutions in the European healthcare sector.

- In November 2024, Synrein Medical announced a three-year exclusive agreement with a major European disaster response agency to supply 50,000 heavy-duty disaster pouches, strengthening its position in the emergency preparedness market.

- In January 2025, MP Acquisition LLC completed the acquisition of MuHeSa Verpackungsmittel, a German specialist in hygiene and containment products, to expand its portfolio and distribution network in the DACH region.

- In April 2025, CEABIS partnered with a leading forensic science institute to develop a new human remains pouch with integrated RFID tracking and enhanced tamper-evident seals, setting a new standard for chain of custody documentation.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Europe Body Bags Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 205 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.9% |

| Market growth 2026-2030 | USD 110.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.6% |

| Key countries | Russia, Germany, Ukraine, Italy and Rest of Europe |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The European market is evolving from commodity-based procurement to a specification-driven landscape. A key boardroom decision involves balancing the cost of traditional polyvinyl chloride with investments in sustainable alternatives like a chlorine-free polymer or biodegradable material. Product differentiation is achieved through features like a leak-proof design, high tensile strength, and puncture resistance, particularly for a specialized bariatric body bag.

- Advanced infection control features and a tamper-evident seal on a human remains pouch for forensic evidence preservation can command a price premium of over 15%. The market also demands niche products like an infant containment bag and bags meeting military specification (MIL-SPEC).

- Success now depends on ensuring cold storage compatibility, providing clear chain of custody documentation, and managing a resilient supply chain for all mortuary supplies, from non-porous materials like woven nylon fabric to finished disaster response pouch models. This technical depth is essential for maintaining a competitive edge.

What are the Key Data Covered in this Europe Body Bags Market Research and Growth Report?

-

What is the expected growth of the Europe Body Bags Market between 2026 and 2030?

-

USD 110.5 million, at a CAGR of 5.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Raw Material (Polyethylene, Polyvinyl chloride, Nylon, and Others), End-user (Morgue, Hospital, and Others), Type (Adult bags, Heavy duty and bariatric bags, and Child or infant bags) and Geography (Europe)

-

-

Which regions are analyzed in the report?

-

Europe

-

-

What are the key growth drivers and market challenges?

-

Increasing prevalence of chronic diseases, Environmental impacts of body bags

-

-

Who are the major players in the Europe Body Bags Market?

-

3D Barrier Bags Inc., Auden Funeral Supplies Ltd., Body Bag, Boen Healthcare Co. Ltd., CEABIS, EIHF ISOFROID, HYGECO International SA, Jiangsu Rooe Medical, Mortech Manufacturing, MP Acquisition LLC, MuHeSa Verpackungsmittel, Polcreative Group, Slik Pak Ltd., Synrein Medical and Wye Valley manufacturing Ltd.

-

Market Research Insights

- Market dynamics are increasingly shaped by a focus on operational safety and efficiency. The implementation of stringent hygienic handling protocols has demonstrably reduced cross-contamination risks in mortuary settings by over 20%. Concurrently, centralized procurement through group purchasing organizations (GPOs) has streamlined purchasing, improving logistical efficiency and achieving cost reductions of up to 15% on bulk orders.

- Disaster resilience planning has become a critical factor, with emergency response planning now mandating higher levels of public health preparedness. This has led to a significant uptick in demand for products with a higher weight capacity rating and enhanced material traceability, ensuring both occupational health and safety and accountability during post-mortem transfers and in mass casualty incidents.

We can help! Our analysts can customize this europe body bags market research report to meet your requirements.

RIA -

RIA -