Fiberglass Market for Aerospace Industry Size 2024-2028

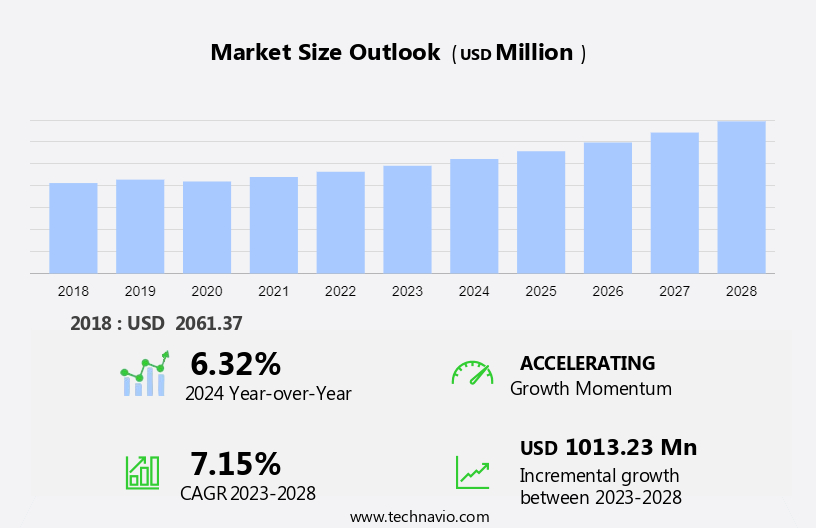

The fiberglass market for aerospace industry size is forecast to increase by USD 1.01 billion at a CAGR of 7.15% between 2023 and 2028.

- The fiberglass market in the aerospace industry exhibits significant growth due to several key factors. One such factor is the increasing demand for cabin retrofitting to enhance passenger comfort in commercial aircraft. Additionally, the construction of new commercial and defense aircraft is on the rise, leading to a rise in the usage of fiberglass in the aerospace sector for commercial aircraft aftermarket parts. However, health hazards associated with fiberglass exposure pose a challenge to market growth. Additionally, fiberglass's use extends beyond the aircraft sector, with applications in wind energy, marine, and transportation industries. Despite this, the benefits of using fiberglass in aerospace applications, such as its lightweight and high-strength properties, make it a preferred material for manufacturers. Overall, the market in the aerospace industry is expected to witness steady growth in the coming years due to these driving factors and the challenges that come with them.

What will be the Size of the Fiberglass Market for Aerospace Industry During the Forecast Period?

To learn more about the market report, Request Free Sample

- In the aerospace industry, the demand for lightweight and eco-friendly materials continues to grow, with fiberglass composites emerging as a popular alternative to traditional metals. Fiberglass, a composite material made of glass fibers and a polymer matrix, offers significant advantages in the aircraft sector. Its lightweight and high strength make it an ideal choice for aircraft construction, contributing to improved fuel efficiency and reduced maintenance costs. Moreover, fiberglass's durability and corrosion resistance ensure the safety and efficiency of operations. The use of fiberglass panels in aircraft manufacturing also enhances insulation and provides durable surfaces. In the aerospace and defense industry, fiberglass's thermoset and thermoplastic variants offer varying benefits, with thermosets providing superior strength and thermoplastics offering easier processing.

- Fiberglass's environmental friendliness is another key factor driving its adoption in the aerospace industry. As concerns over raw material costs and sustainability grow, fiberglass's eco-friendly nature and recyclability make it an attractive option. Overall, fiberglass's unique properties and benefits make it a valuable asset in the aerospace and defense industry, contributing to the development of more efficient, sustainable, and cost-effective aircraft.

How is the Fiberglass Market for Aerospace Industry Segmented?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

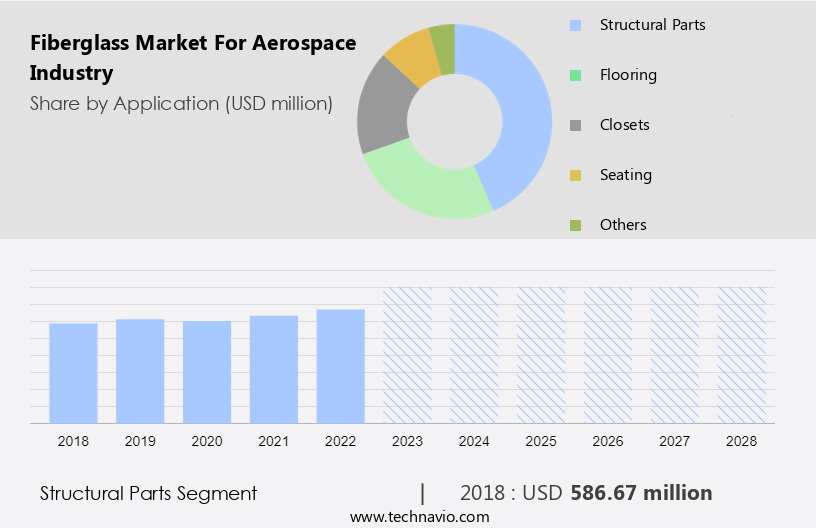

- Application

- Structural parts

- Flooring

- Closets

- Seating

- Others

- Type

- Thermoset resins

- Thermoplastic resins

- Geography

- APAC

- China

- Japan

- North America

- Canada

- US

- Europe

- Germany

- South America

- Middle East and Africa

- APAC

By Application Insights

- The structural parts segment is estimated to witness significant growth during the forecast period.

Fiberglass composites play a significant role in the aerospace industry, accounting for approximately half of the weight in modern aircraft. This material, consisting of glass fibers reinforced in a polymer matrix, is widely used for manufacturing structural components such as fuselage, wings, stabilizers, landing gear, and tail sections. In interior applications, fiberglass is utilized as sheets, panels, and veneers for flooring, closets, air ducts, cargo liners, and insulation. The high strength and durability of fiberglass make it an ideal choice for aerospace manufacturing. Thermoset and thermoplastic matrices are commonly used in fiberglass composites for aerospace applications. Silica, silicate, calcium, magnesium, and boron oxides are often added as reinforcements to enhance the properties of fiberglass composites. While carbon fiber is another popular reinforcement in the aerospace sector, fiberglass remains a cost-effective and widely used option due to its excellent corrosion resistance and lightweight properties.

Get a glance at the market report of share of various segments. Request Free Sample

The structural parts segment was valued at USD 586.67 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

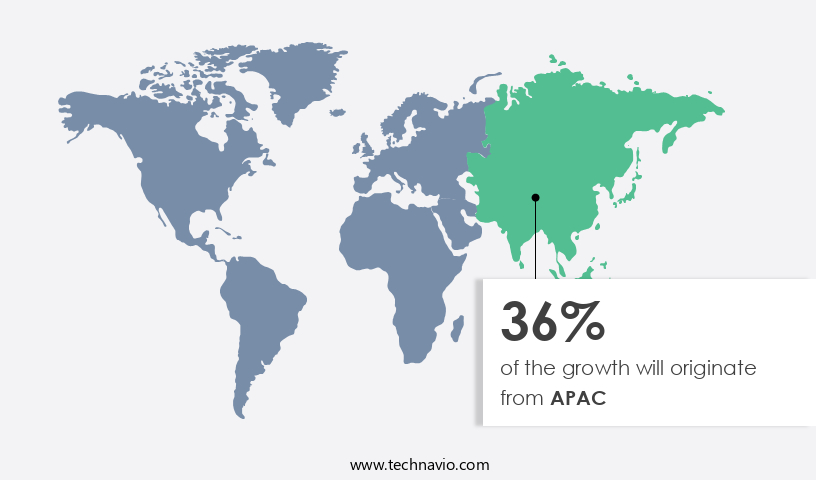

- APAC is estimated to contribute 36% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market is experiencing significant growth in the Asia Pacific (APAC) region due to the increasing construction of lightweight, fuel-efficient aircraft. With a large fleet of aircraft in countries like India, China, Japan, Singapore, and Malaysia, the demand for fiberglass, known for its high strength and durability, is on the rise. China, being a major player in the civil aerospace and aviation services industry, is a key contributor to this trend. Operators in APAC are focusing on expanding their fleets to meet the growing passenger demand in the region, leading to increased adoption of fiberglass in aircraft manufacturing.

Additionally, the emphasis on reducing fuel burn and improving operational efficiency, along with lower maintenance costs and enhanced safety features, further boosts the market's growth. The market in the aerospace industry is expected to continue its expansion in the coming years, with potential applications also extending to wind energy and marine industries.

Fiberglass Market for Aerospace Industry Dynamics

Our market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Key Market Drivers

The need for cabin retrofitting seats to enhance passenger comfort is the key driver of the market.

- In the aerospace industry, fiberglass, a composite material made from glass fibers and a resin matrix, has gained significant attention as a lightweight and eco-friendly alternative to traditional metals. Fiberglass offers superior strength and stiffness, making it an ideal choice for aircraft manufacturing, particularly in the production of wind turbine blades and aircraft components. The use of fiberglass in the aerospace sector contributes to aircraft weight reduction and fuel efficiency, which are crucial factors in the economic and environmental landscapes of the industry. Moreover, fiberglass's durability and resistance to corrosion make it a sustainable solution for aircraft exterior and interior applications.

- The recyclability of fiberglass and its raw materials, such as silica, silicate, calcium, magnesium, boron oxides, and hydroxyapatite particles, aligns with the industry's increasing focus on sustainability and reducing waste. The automotive sector has also embraced fiberglass for lightweighting and enhancing performance, further driving down raw material costs and increasing its availability for the aerospace industry. Innovation and technology continue to advance the use of fiberglass in the aerospace industry, with applications ranging from aircraft interiors and exteriors to panels, insulation, and infrastructure sectors. Quality control is essential in the production of fiberglass components for the aerospace industry. Fiberglass's thermal insulation properties and fire resistance make it an attractive alternative to wood, bone, cellulose fibers, and lignin matrix materials.

Primary Market Trends

Rising construction for new commercial and defense aircraft is the upcoming trend in the market.

- The aerospace industry's reliance on lightweight and eco-friendly materials, such as fiberglass composites, has gained significant traction due to the increasing demand for sustainability and economic efficiency. Fiberglass, a composite material made of glass fibers and a resin matrix, offers high strength, durability, and corrosion resistance, making it an ideal alternative to traditional metals in the aircraft sector. Fiberglass's use extends beyond the aircraft industry, with applications in wind turbine blades, infrastructure sectors, and automotive lightweighting. The raw material costs of fiberglass have remained relatively stable due to the availability of raw materials like silica, silicate, calcium, magnesium, and boron oxides.

- Moreover, the development of recyclable materials and innovative technologies has led to sustainable solutions for fiberglass production and disposal. Quality control is paramount in the aerospace industry, and fiberglass's consistency and uniformity make it an attractive choice. Economic and environmental landscapes have become crucial considerations in the industry, and fiberglass's energy efficiency and performance contribute to both. The strong and stiff fibers in the composite material provide aircraft weight reduction, resulting in fuel economy and fuel burn reduction, which is essential for airline sector sustainability. Innovation and technology continue to drive the fiberglass market, with advancements in autoclave systems, glass wool recycling, and fiberglass fabric production.

Major Market Challenges

Health hazards associated with fiberglass exposure is a key challenge affecting the market growth.

- The aerospace industry's increasing focus on lightweight materials, sustainability, and eco-friendly solutions has led to a significant rise in the usage of fiberglass as a composite material. Fiberglass, a thermoset polymer made of glass fibers and a resin matrix, offers high strength, durability, and excellent corrosion resistance, making it an ideal alternative to metals in aircraft manufacturing. Fiberglass's use extends beyond the aircraft sector, finding applications in various infrastructure sectors such as wind energy, construction, transportation, and insulation. In the automotive industry, fiberglass is used for lightweighting and improving fuel efficiency through automotive lightweighting. Raw material costs, economic landscapes, and environmental landscapes are significant factors influencing the fiberglass market's growth.

- Innovation and technology play a crucial role in enhancing fiberglass's sustainability by developing recyclable materials and improving quality control processes. Fiberglass's use in wind turbine blades and aircraft exterior and interior components contributes to fuel economy and enhanced safety. The sandwich process, which involves the use of fiberglass fabric between two lightweight materials, further reduces aircraft weight and fuel burn. The aerospace and defense industry's new aircraft demand, airline sector growth, and increasing air passenger traffic necessitate the adoption of lightweight and fuel-efficient materials like fiberglass. Additionally, the development of advanced autoclave systems and glass wool recycling technologies is expected to drive market growth.

Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market growth analysis report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market for aerospace industry market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3B the fiberglass Co.

- AGY Holding Corp.

- ATKINS and PEARCE Inc.

- China Jushi Co. Ltd.

- Compagnie de Saint Gobain

- Hexcel Corp.

- Huntsman International LLC

- Johns Manville

- JPS Composite Materials

- Montex Glass Fibre Industries Pvt. Ltd.

- Nan Ya Plastic Corp.

- Nitto Boseki Co. Ltd.

- Park Aerospace Corp.

- Phelps Industrial Products LLC

- Piran Advanced Composites

- Porcher Industries

- SAERTEX GmbH and Co.KG

- Sinoma Science and Technology Co. Ltd.

- Taiwan Glass Ind. Corp.

- Tencom Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Fiberglass, a composite material made of glass fibers and a resin matrix, has gained significant attention in the aerospace industry due to its unique properties. This material offers lightweight, high strength, and durability, making it an ideal choice for various applications in the aerospace sector. The global economic landscape has been witnessing a shift towards eco-friendly and sustainable solutions. This trend is also reflected in the aerospace industry, where fiberglass's role is expanding. Fiberglass is considered an alternative material to traditional metals, offering potential cost savings and environmental benefits.

Moreover, raw material costs are a crucial factor influencing the fiberglass market in the aerospace industry. The prices of raw materials such as silica, silicate, calcium, magnesium, boron oxides, and carbon fiber can significantly impact the production costs of fiberglass. However, the industry's focus on innovation and technology is driving the development of more cost-effective production methods and alternative raw materials. Quality control is another essential aspect of the market in the aerospace industry. The stringent requirements of this sector necessitate high-quality materials and manufacturing processes. Autoclave systems, for instance, are widely used to ensure consistent quality and optimal performance of fiberglass components.

Furthermore, sustainability is a critical concern in today's economic and environmental landscapes. The aerospace industry is exploring various ways to reduce its carbon footprint, and fiberglass plays a role in this endeavor. For example, fiberglass is used in the production of wind turbine blades, contributing to the renewable energy sector's growth. Recyclable materials are another trend gaining traction in the aerospace industry. Glass wool recycling, for instance, is an area of active research, with potential applications in insulation and roofing materials. Fiberglass fabric is also used in aircraft weight reduction, enhancing fuel efficiency and reducing maintenance costs. The infrastructure sectors, including transportation, construction, and energy, are also adopting fiberglass due to its advantages.

|

Fiberglass Market for Aerospace Industry Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

158 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.15% |

|

Market Growth 2024-2028 |

USD 1.01 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.32 |

|

Key countries |

US, Canada, China, Japan, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -