Field Force Automation Market Size 2024-2028

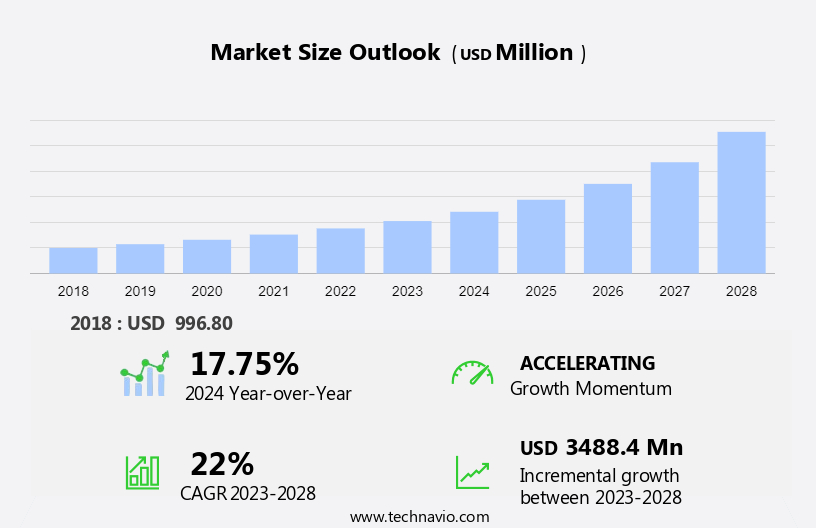

The field force automation market size is forecast to increase by USD 3.49 billion at a CAGR of 22% between 2023 and 2028.

- The market is experiencing significant growth due to several key trends. The increasing demand for field force automation in Customer Relationship Management (CRM) is a major driving factor, as businesses seek to streamline operations and improve customer engagement. The IT and telecom sector, transportation and logistics, construction, real estate, and other sectors are leveraging field force automation solutions to enhance productivity and efficiency. Additionally, the strong growth of the IT industry is fueling the adoption of advanced technologies, such as mobile devices and cloud computing, which are essential for field force automation solutions. However, data privacy and security concerns associated with field force automation are challenges that must be addressed to ensure the successful implementation of these systems. Overall, the market is expected to continue its growth trajectory as businesses recognize the benefits of automating their field operations.

What will be the Size of the Field Force Automation Market During the Forecast Period?

- The market is experiencing significant growth due to the increasing adoption of mobile internet penetration, cloud computing, IoT, AI, and communication technologies in various industries. Field forces, comprising technicians and head office staff, are increasingly using handheld wireless devices for automated scheduling, worker dispatching, daily reporting, mobile workforce monitoring, tracking, and real-time communication. Real-time data exchange and error reduction are key benefits of field force automation, enabling businesses to streamline operations and improve customer service.

- Moreover, connected devices and IoT are driving the adoption of field force automation, providing real-time data access and enabling proactive problem-solving. AI is being integrated into field force automation solutions to enhance predictive maintenance and improve decision-making capabilities. Overall, the market is poised for strong growth, offering significant opportunities for businesses to optimize operations and enhance customer satisfaction.

How is this Field Force Automation Industry segmented and which is the largest segment?

The field force automation industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- IT and telecom

- Healthcare and life sciences

- Manufacturing

- Transportation and logistics

- Others

- Deployment

- On-premises

- Cloud-based

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Middle East and Africa

- South America

- North America

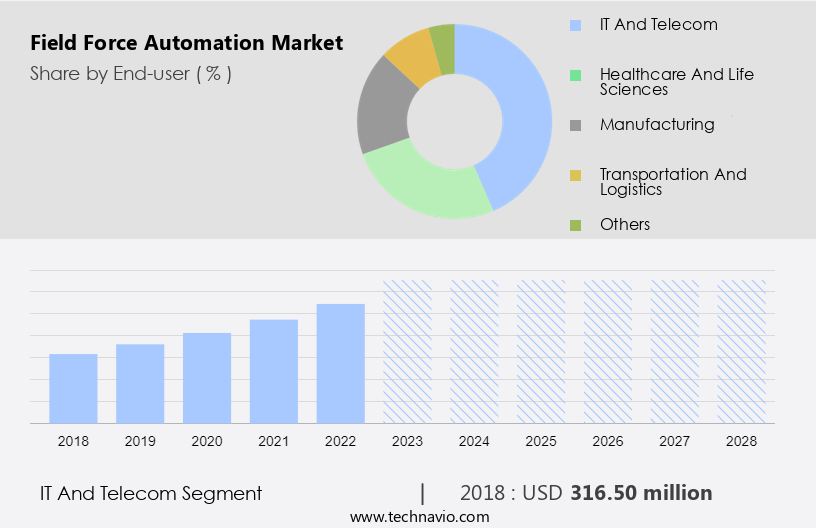

By End-user Insights

- The IT and telecom segment is estimated to witness significant growth during the forecast period.

Field Force Automation (FFA) refers to the implementation of technology solutions to automate and optimize the activities of field-based workers in various industries. With the increasing penetration of mobile internet and the adoption of cloud computing, FFA has gained significant traction in sectors such as transportation and logistics, construction, real estate, and IT and telecom. FFA platforms enable businesses to manage their dispersed workforce effectively, enabling real-time communication and access to critical information. In the IT and telecom industry, FFA plays a pivotal role in enhancing operational efficiency, customer service, and workforce productivity. Field technicians and engineers can access work orders, customer information, and task details on their handheld wireless devices, eliminating the need for manual paperwork and reducing administrative overhead.

Get a glance at the Field Force Automation Industry report of share of various segments Request Free Sample

The IT and telecom segment was valued at USD 316.50 million in 2018 and showed a gradual increase during the forecast period.

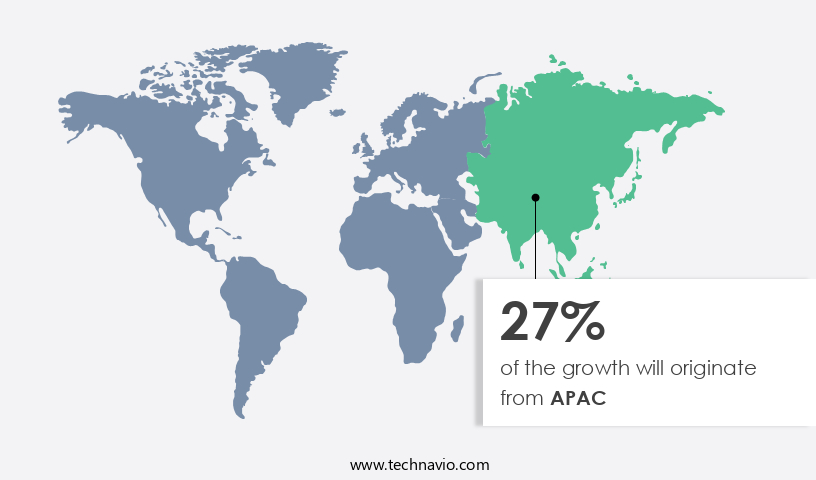

Regional Analysis

- APAC is estimated to contribute 27% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market is witnessing significant growth due to the digitalization of processes in various industries, particularly in fast-moving consumer goods (FMCG), manufacturing, energy and utilities, and large enterprises. This automation enables efficient stock tracking, sales order management, and real-time communication between field forces and organizations. Mobile devices, such as smartphones and tablets, are being increasingly used to automate scheduling, dispatching, and daily reporting for field crews. Cloud-based and on-premises solutions offer organizations of all sizes the flexibility to access computing resources and manage their mobile workforces more effectively. Large manufacturing companies are leveraging IoT sensors, actuators, and alerts to monitor physical assets and minimize downtime on manufacturing floors.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Field Force Automation Industry?

Rising demand for field force automation in CRM is the key driver of the market.

- Field Force Automation (FFA) is a vital solution In the IT and Telecom sector, particularly in industries such as transportation and logistics, construction, real estate, and multinationals, to boost workforce productivity and enhance business operations. FFA leverages mobile internet penetration, cloud computing, Internet of Things (IoT), Artificial Intelligence (AI), and connected devices to streamline workflows and improve communication between head office staff and field executives. Cloud-based solutions, including Field Service Management, Enterprise Resource Planning, and Customer Relationship Management systems, offer advanced capabilities such as real-time data analysis, automatic schedules, attendance management, workforce monitoring, and sales automation. Solutions like Oracle Field Service Cloud integrate with CRM systems, providing technicians with access to customer data in real-time, enabling more informed and personalized interactions.

- In addition, FFA also incorporates ML, robotics, computer vision, and cyberattack protection to ensure accurate data analysis and secure information transmission. Handheld wireless devices enable real-time data entry, reducing errors and improving field executive performance. Overall, FFA empowers businesses to optimize their workflows, improve customer engagement, and enhance operational efficiency.

What are the market trends shaping the Field Force Automation Industry?

strong growth of IT industry is the upcoming market trend.

- The market is witnessing significant growth due to the advancements in technology, particularly In the IT sector. With the increasing mobile internet penetration and the adoption of cloud computing, connected devices, and IoT, field force automation solutions have become more sophisticated. AI, ML, robotics, computer vision, and advanced analytics are being integrated into these solutions to enhance workforce productivity and efficiency. The transportation and logistics, construction, real estate, and other industries are leveraging these technologies to streamline business operations, improve communication between head office staff and technicians, and optimize workflows. Cloud-based solutions offer real-time data analysis, predictive maintenance, and automatic schedules, while attendance management and workforce monitoring provide greater control and accuracy.

- In addition, the use of handheld wireless devices enables on-the-go access to data and automates workflows, reducing errors and improving field executive performance. The integration of cybersecurity measures ensures data security, making these solutions a valuable investment for multinationals and businesses of all sizes.

What challenges does the Field Force Automation Industry face during its growth?

Data privacy and security concerns associated with field force automation is a key challenge affecting the industry growth.

- The Field Force Automation (FFA) market is witnessing significant growth due to the increasing adoption of mobile internet penetration, cloud computing, Internet of Things (IoT), Artificial Intelligence (AI), and connected devices in various industries such as IT and Telecom, transportation and logistics, construction, and real estate. FFA solutions offer advanced capabilities like sales automation, field service management, enterprise resource planning, and customer relationship management through cloud-based solutions. These solutions enable real-time communication and data analysis, improving workforce productivity and performance. FFA solutions also incorporate technologies like ML, robotics, computer vision, and cyberattack protection. Handheld wireless devices enable technicians and head office staff to access automatic schedules, attendance management, workforce monitoring, and advanced analytics in real-time.

- However, data privacy and security concerns are crucial considerations when implementing FFA solutions. Sensitive customer data, including personal information, financial details, and contact information, must be protected from unauthorized access. Encryption protocols are essential to secure data transmission and prevent interception and misuse. Organizations must adhere to applicable data protection and privacy regulations, such as GDPR and CCPA, to ensure compliance.

Exclusive Customer Landscape

The field force automation market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the field force automation market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, field force automation market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abuyo Inc.

- Accruent

- Acumatica Inc.

- BT Group Plc

- Channelplay Ltd.

- FieldEZ

- Folio3 Software Inc.

- IFS World Operations AB

- Kloudq Technologies Ltd.

- MACmobile Pty Ltd.

- MarketXpander Services Pvt. Ltd.

- Microsoft Corp.

- Nimap Infotech

- Oracle Corp.

- PTC Inc.

- Salesforce Inc.

- SAP SE

- SPEC India

- Trimble Inc.

- Vasista Enterprise Solutions Pvt. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Field Force Automation (FFA) is a critical business solution that has gained significant traction in various industries due to the increasing adoption of mobile internet penetration, cloud computing, Internet of Things (IoT), and advanced technologies like AI, ML, robotics, computer vision, and cyberattacks. FFA is transforming IT and telecom, transportation and logistics, construction, real estate, and multinationals by automating sales, workforce productivity, and business operations. FFA solutions enable real-time communication between head office staff and technicians through cloud-based sales automation solutions, field service management, enterprise resource planning, and customer relationship management. These solutions are essential for managing connected devices and ensuring error-free execution of tasks.

In addition, handheld wireless devices are the primary tool for field executives, enabling automatic schedules, attendance management, workforce monitoring, and advanced analytics. AI solutions offer data analysis and workflow automation, enhancing business efficiency and productivity. ML algorithms help in predictive maintenance, while robotics and computer vision provide automated inspections and error detection. Cyberattacks pose a significant challenge to FFA adoption, necessitating strong security measures. Cloud solutions offer scalability, flexibility, and cost savings, making them a preferred choice for businesses. Overall, FFA is revolutionizing business operations by automating workflows, enhancing workforce performance, and improving customer satisfaction.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

166 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 22% |

|

Market growth 2024-2028 |

USD 3.49 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

17.75 |

|

Key countries |

US, China, UK, Germany, and Japan |

|

Competitive landscape |

Leading Companies, market growth and forecasting , Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Field Force Automation Market Research and Growth Report?

- CAGR of the Field Force Automation industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the field force automation market growth of industry companies

We can help! Our analysts can customize this field force automation market research report to meet your requirements.

RIA -

RIA -