North America Flexible Intermediate Bulk Container Market Size 2026-2030

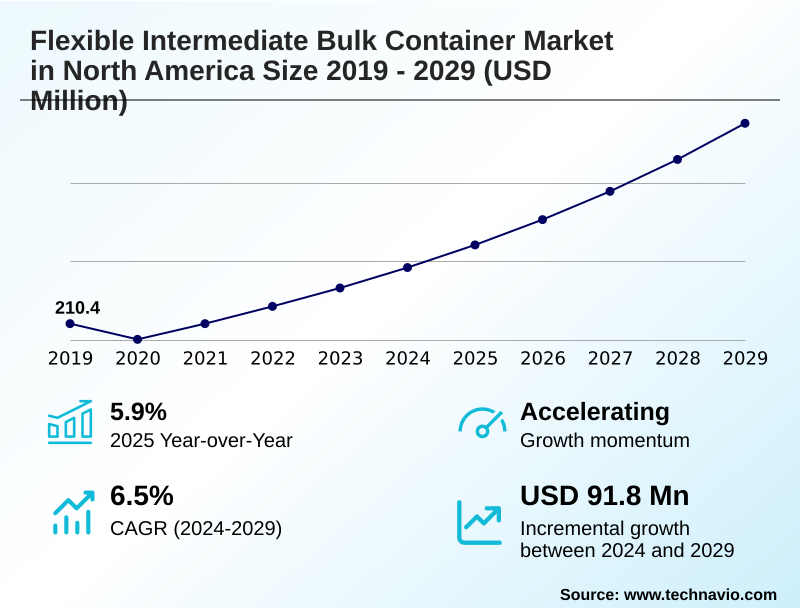

The north america flexible intermediate bulk container market size is valued to increase by USD 99.2 million, at a CAGR of 6.7% from 2025 to 2030. Growing demand for bulk packaging will drive the north america flexible intermediate bulk container market.

Major Market Trends & Insights

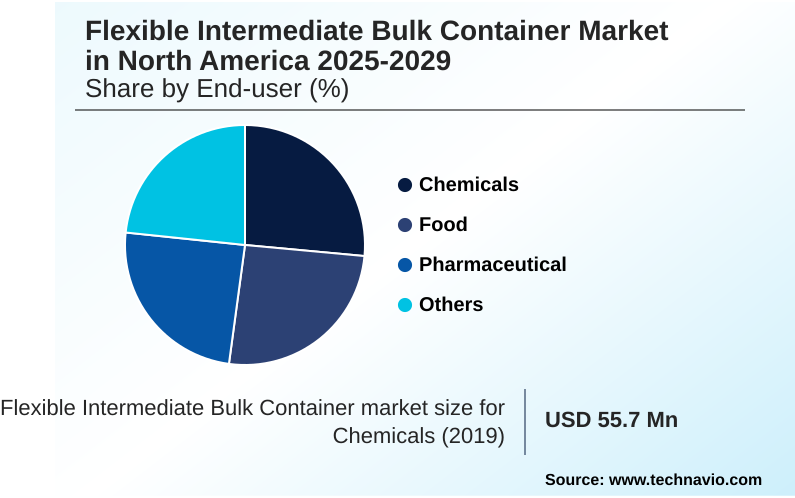

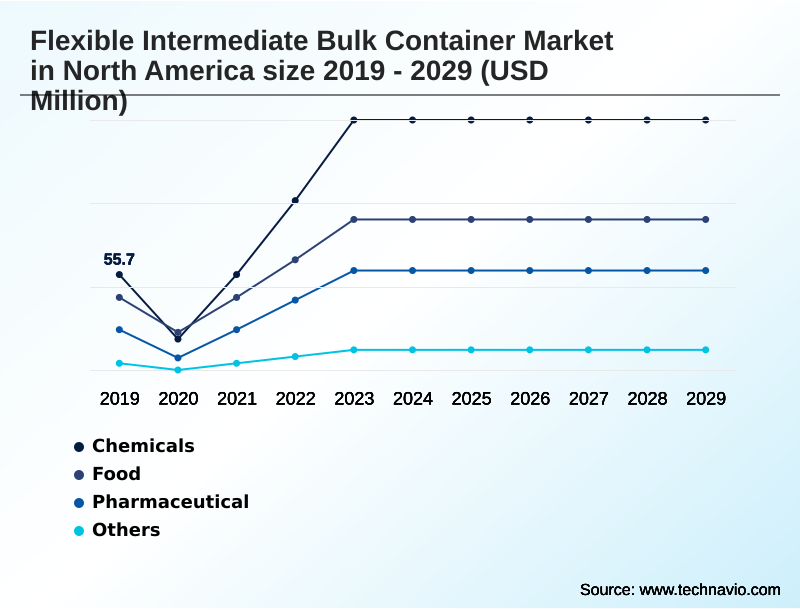

- By End-user - Chemicals segment was valued at USD 74 million in 2024

- By Material - Woven polypropylene segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 159.3 million

- Market Future Opportunities: USD 99.2 million

- CAGR from 2025 to 2030 : 6.7%

Market Summary

- The flexible intermediate bulk container market in North America is evolving beyond simple storage, driven by demands for greater supply chain efficiency and sustainability. These containers, made from materials like woven polypropylene fabric, are integral for the powder transport logistics of fine chemicals and the granular material handling required in agriculture and construction.

- A key trend is the adoption of high-performance variants, such as type d antistatic bags and food-grade certified bags, to meet stringent safety and hygiene standards. For instance, a pharmaceutical firm can leverage clean-room certified bags with high barrier liners to ensure zero contamination during the global transit of active ingredients, optimizing for both safety and operational excellence.

- However, challenges such as inadequate recycling infrastructure and price volatility from fluctuating raw material costs persist. The market is also seeing increased use of automated filling systems, which require containers with precise dimensions and reinforced structures, pushing manufacturers toward greater innovation in baffle bag design and overall durability.

- This intersection of technology, regulation, and efficiency defines the industry's current trajectory, demanding advanced and specialized packaging solutions.

What will be the Size of the North America Flexible Intermediate Bulk Container Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the North America Flexible Intermediate Bulk Container Market Segmented?

The north america flexible intermediate bulk container industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Chemicals

- Food

- Pharmaceutical

- Others

- Material

- Woven polypropylene

- Polyethylene

- Conductive fabrics

- Application

- Powder transport

- Granular material handling

- Hazardous material packaging

- Geography

- North America

- US

- Canada

- Mexico

- North America

By End-user Insights

The chemicals segment is estimated to witness significant growth during the forecast period.

The chemicals segment is a primary consumer in the flexible intermediate bulk container market in North America, driven by the need for secure transport of volatile and non-volatile substances.

Enhanced safety protocols and stringent regulations necessitate the use of specialized containers for hazardous material packaging, including type c conductive fibcs and those with robust sift-proof seams.

The expansion of chemical manufacturing output directly fuels demand for efficient bulk packaging solutions that ensure material integrity assurance.

A significant industry-wide movement toward circularity is evidenced by a comprehensive transition to using 80% recycled polypropylene in all flexible intermediate bulk container for domestic logistics, reflecting a commitment to sustainable packaging initiatives without compromising the structural integrity required for high-purity chemical transport and regulatory compliance management.

The Chemicals segment was valued at USD 74 million in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

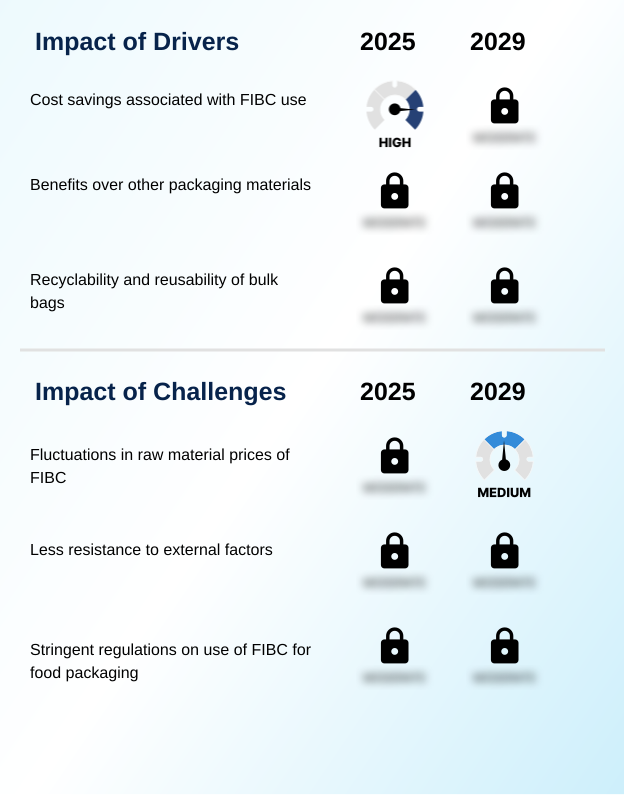

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in the flexible intermediate bulk container market are increasingly influenced by granular operational factors. For instance, evaluating type d vs type c fibc safety is critical for industries handling combustible dusts, where selecting the appropriate electrostatic protection can prevent catastrophic accidents.

- Similarly, understanding the total cost of food grade fibc certification is essential for budget planning in food and pharmaceutical sectors, as compliance dictates market access. The push for efficiency is driving interest in automating fibc filling and discharging, a move that requires significant capital but promises long-term labor savings.

- The impact of pp resin price on fibcs remains a primary concern for procurement managers, forcing diversification of suppliers to mitigate volatility. Key long-tail considerations now include fibc solutions for hazardous waste, the benefits of baffle bags in shipping for load stability, and sourcing fibc liners for moisture sensitive products.

- Businesses are also focused on reducing product loss with sift proof fibcs and meeting UN certification requirements for bulk bags to ensure global compliance. Specialized applications like fibc for pharmaceutical powder transport and sustainable fibc material innovations are defining niche market growth.

- Further analysis extends to fibc design for mineral concentrates and fibc use in specialty chemical logistics, which demand custom solutions. In agriculture, enhancing fibc UV resistance for agriculture and adopting fibcs for organic food ingredient handling are becoming standard. Elsewhere, the demand for lightweight fibc for air freight savings is growing.

- Finally, implementing closed-loop fibc recovery systems analysis is a core part of corporate sustainability strategy, alongside establishing multi-trip fibc durability testing standards and optimizing fibc performance in automated warehouses, which has shown to reduce handling errors by a significant margin compared to manual processes.

What are the key market drivers leading to the rise in the adoption of North America Flexible Intermediate Bulk Container Industry?

- The increasing transition toward bulk packaging solutions to enhance logistics efficiency and reduce operational costs is a key factor driving market demand.

- Market growth is fueled by the relentless pursuit of operational efficiency and cost control. The expansion of chemical manufacturing output and increased agricultural commodity transport are creating sustained demand for reliable bulk packaging solutions.

- Integrating automated filling systems with dust control mechanisms has proven to boost packaging throughput by up to 30%, a critical factor for high-volume operations. This drive for efficiency enables significant operational cost reduction and enhances supply chain efficiency.

- Furthermore, advanced packaging designs are improving warehouse space optimization and leading to tangible freight expense reduction, making these containers an indispensable component of modern industrial packaging logistics and supporting wider food processing applications and construction material handling.

What are the market trends shaping the North America Flexible Intermediate Bulk Container Industry?

- A significant transformation is underway as industries increasingly prioritize sustainability and circular material use, prompting a growing shift toward recyclable and eco-efficient bulk packaging solutions.

- Key trends are reshaping the market, centered on sustainability and enhanced product safety. The adoption of recyclable pp materials is accelerating, with closed-loop recovery programs gaining traction as companies aim to reduce their environmental footprint. This shift has resulted in a 15% increase in the use of recycled content in new containers without compromising structural integrity.

- Simultaneously, the demand for food-grade certified bags is rising to meet stringent hygienic packaging standards. These containers, often manufactured with advanced polyethylene liners and UV stabilized fabrics, have been shown to reduce cross-contamination incidents by over 25% in food processing applications.

- The focus on high barrier liners and tamper-evident design further underscores the industry's commitment to material integrity assurance and supply chain security.

What challenges does the North America Flexible Intermediate Bulk Container Industry face during its growth?

- The region's limited and inconsistent recycling infrastructure for polypropylene-based bulk bags presents a defining challenge for the market.

- The market confronts several structural challenges that impact stability and growth. The lack of widespread recycling infrastructure development remains a primary barrier, hindering the circularity of multi-wall paper bags and other containers. This gap complicates sustainability goals and increases reliance on virgin materials.

- Concurrently, high-tenacity polymers and other advanced materials are subject to price volatility due to import duty impacts, creating budget uncertainty for end-users. Logistics delays mitigation is another critical issue, as disruptions in global shipping can extend lead times by several weeks, affecting inventory management for sectors reliant on timely deliveries for pharmaceutical ingredient storage and mineral transport systems.

- These challenges necessitate greater investment in domestic supply chains and innovative materials to ensure resilience.

Exclusive Technavio Analysis on Customer Landscape

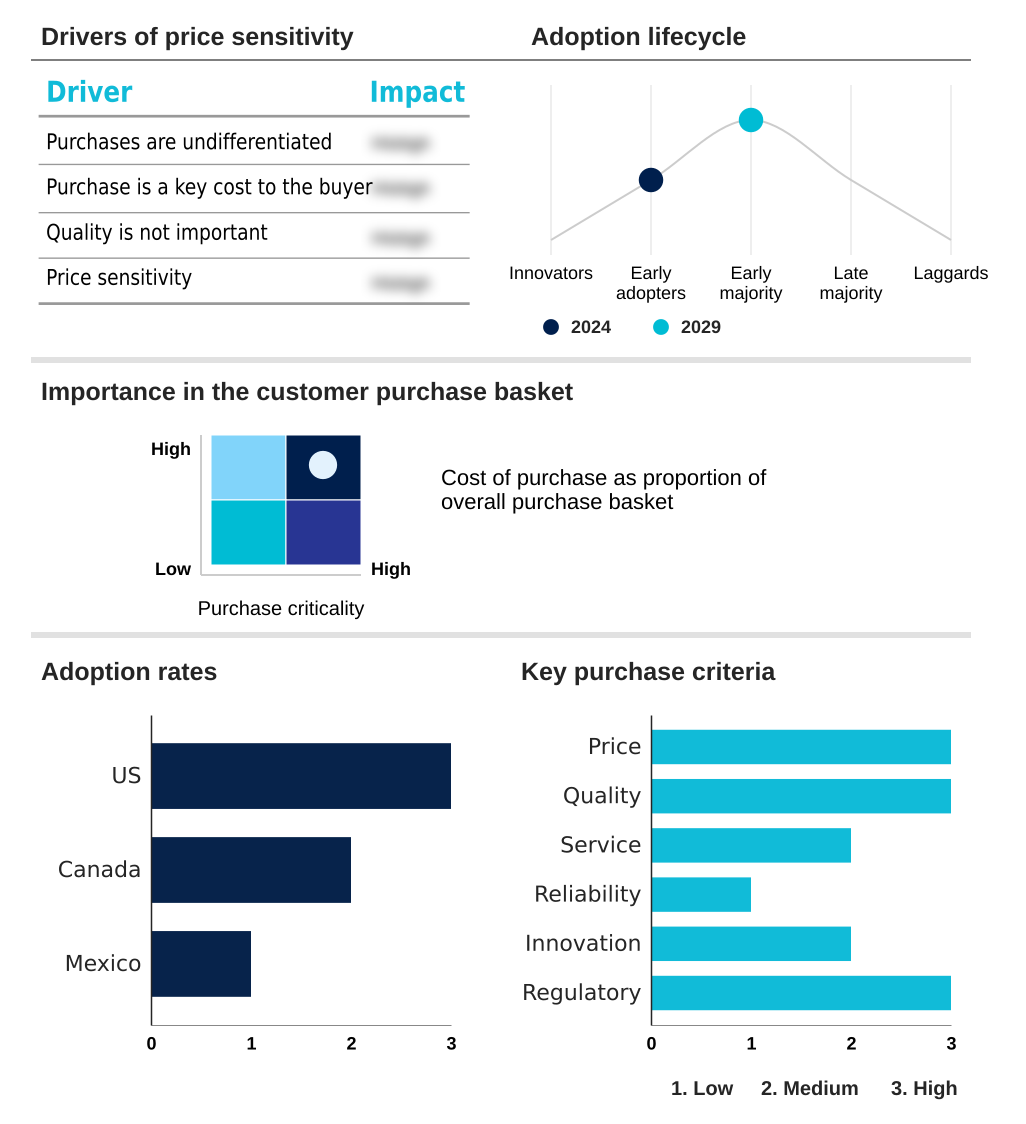

The north america flexible intermediate bulk container market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the north america flexible intermediate bulk container market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of North America Flexible Intermediate Bulk Container Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, north america flexible intermediate bulk container market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AmeriGlobe LLC - Offerings include patented bulk bag designs and comprehensive material handling systems engineered to optimize warehouse space and elevate shipping efficiency across industrial applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AmeriGlobe LLC

- BAG Corp.

- Bulk Lift International LLC

- Bulkcorp International Ltd.

- Foison Packaging Inc.

- Global Pak Inc.

- Greif Inc.

- Halsted Corp.

- Intertape Polymer Group Inc.

- Jumbo Bag Ltd.

- Langston Companies Inc.

- Minibulk Inc.

- NNZ Inc.

- Safpack Packaging Solutions

- Southern Packaging LP

- Sunbelt Packaging LLC

- The Griff Network

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in North america flexible intermediate bulk container market

- In August 2025, Intertape Polymer Group Inc. introduced advanced barrier resins for its product portfolio to improve the protection of sensitive food ingredients against oxidation.

- In November 2025, Bulkcorp International Ltd. operationalized a new manufacturing wing dedicated to the production of high-strength woven polypropylene fabrics for heavy-duty applications.

- In May 2025, Greif Inc. launched a significant sustainability initiative that facilitates the collection and refurbishment of used containers to promote a circular economy.

- In March 2025, WM Inc. introduced a comprehensive recovery program for large-scale industrial textiles, ensuring used bulk containers are converted into secondary raw materials instead of ending up in landfills.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled North America Flexible Intermediate Bulk Container Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 200 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.7% |

| Market growth 2026-2030 | USD 99.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.1% |

| Key countries | US, Canada and Mexico |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The flexible intermediate bulk container market in North America is defined by a transition toward high-specification, value-added solutions. Core materials like woven polypropylene fabric are being enhanced with high-tenacity polymers and UV stabilized fabrics to meet demanding industrial requirements.

- The adoption of specialized containers, including type c conductive fibcs and type d antistatic bags, is driven by stringent safety regulations for hazardous material packaging. In parallel, the food and pharmaceutical sectors are mandating food-grade certified bags and clean-room certified bags featuring advanced moisture barrier layers and tamper-evident design to ensure product purity.

- Innovations in baffle bag design and sift-proof seams are improving storage density and minimizing product loss during granular material handling and powder transport logistics. This shift toward specialization is a key boardroom consideration, as investment in UN certified bulk bags or polyethylene liners directly impacts regulatory compliance and risk management.

- For instance, facilities implementing automated filling systems equipped with dust control mechanisms report a 30% increase in throughput. The market's evolution is further shaped by the push for sustainability through recyclable pp materials and closed-loop recovery programs, demanding a holistic approach to packaging strategy across all heavy-duty industrial applications.

What are the Key Data Covered in this North America Flexible Intermediate Bulk Container Market Research and Growth Report?

-

What is the expected growth of the North America Flexible Intermediate Bulk Container Market between 2026 and 2030?

-

USD 99.2 million, at a CAGR of 6.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Chemicals, Food, Pharmaceutical, and Others), Material (Woven polypropylene, Polyethylene, and Conductive fabrics), Application (Powder transport, Granular material handling, and Hazardous material packaging) and Geography (North America)

-

-

Which regions are analyzed in the report?

-

North America

-

-

What are the key growth drivers and market challenges?

-

Growing demand for bulk packaging, Limited recycling infrastructure for FIBCs

-

-

Who are the major players in the North America Flexible Intermediate Bulk Container Market?

-

AmeriGlobe LLC, BAG Corp., Bulk Lift International LLC, Bulkcorp International Ltd., Foison Packaging Inc., Global Pak Inc., Greif Inc., Halsted Corp., Intertape Polymer Group Inc., Jumbo Bag Ltd., Langston Companies Inc., Minibulk Inc., NNZ Inc., Safpack Packaging Solutions, Southern Packaging LP, Sunbelt Packaging LLC and The Griff Network

-

Market Research Insights

- Market dynamics are shaped by a strategic focus on operational cost reduction and enhanced logistics flexibility. The adoption of advanced bulk packaging solutions has been shown to improve warehouse space optimization by over 25%, directly impacting freight expense reduction.

- Concurrently, heightened standards for cross-contamination prevention are driving innovation in hygienic packaging standards, with specialized containers reducing product spillage minimization rates by up to 40%. As industries from food processing to chemicals expand, the need for reliable agricultural commodity transport and material integrity assurance is paramount.

- These factors compel a shift toward sophisticated packaging that supports both efficiency and stringent quality control, defining the competitive landscape.

We can help! Our analysts can customize this north america flexible intermediate bulk container market research report to meet your requirements.

RIA -

RIA -