Food Contact Paper Market Size 2026-2030

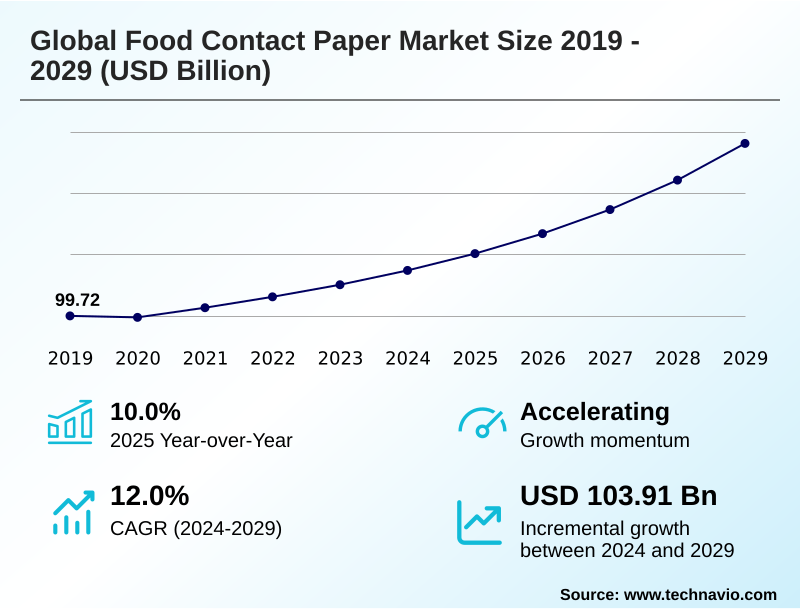

The food contact paper market size is valued to increase by USD 107.80 billion, at a CAGR of 11.4% from 2025 to 2030. Imperative for sustainability and global backlash against plastics will drive the food contact paper market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 35.5% growth during the forecast period.

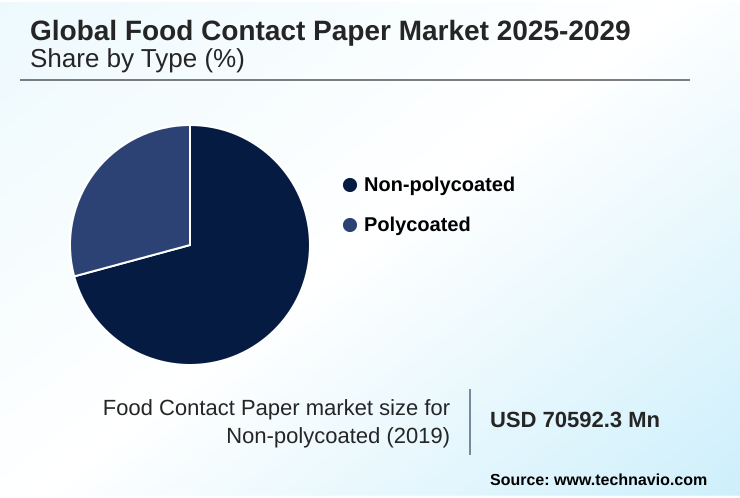

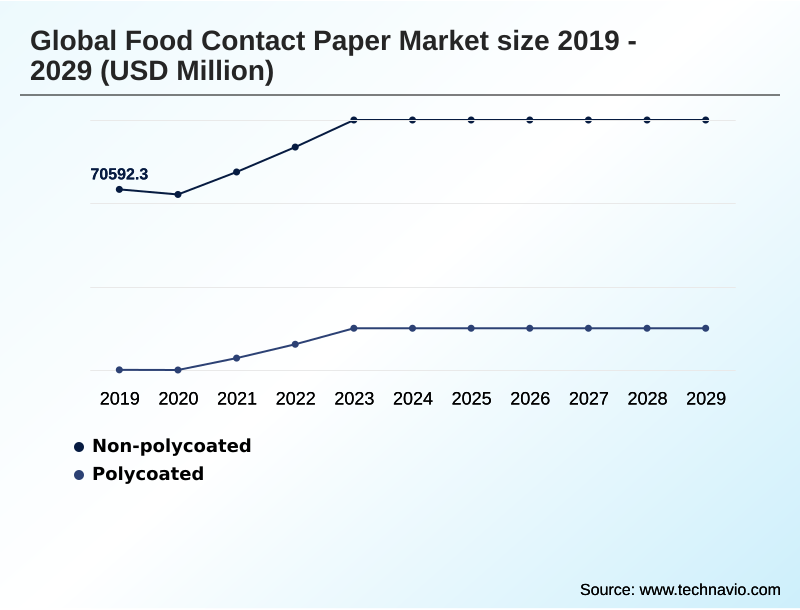

- By Type - Non-polycoated segment was valued at USD 93.72 billion in 2024

- By Material - Kraft paper segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 159.96 billion

- Market Future Opportunities: USD 107.80 billion

- CAGR from 2025 to 2030 : 11.4%

Market Summary

- The food contact paper market is undergoing a significant transformation, driven by a confluence of regulatory pressures, evolving consumer preferences, and technological innovation. The global movement towards environmental responsibility has created substantial opportunities for paper-based packaging solutions.

- This shift necessitates the development of a new generation of food contact paper that is not only biodegradable and recyclable but also meets stringent safety and performance standards. The market is responding with a wave of innovation, focusing on advanced functional barrier coatings that provide necessary protection without compromising environmental credentials.

- A key business scenario involves supply chain optimization, where manufacturers must re-tool production lines to accommodate pfas-free papers and plant-based coatings. This requires significant capital investment in repulpable barrier technology and food-grade paper manufacturing processes to ensure food safety compliance and meet the demand from the food service outlet applications and restaurant applications.

- The rising popularity of online food delivery and the growth of the fast-food sector further fuel demand for high-quality, reliable, and sustainable food packaging, pushing the industry towards a circular economy model where materials like food-grade recycled fiber are utilized more effectively.

What will be the Size of the Food Contact Paper Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Food Contact Paper Market Segmented?

The food contact paper industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Non-polycoated

- Polycoated

- Material

- Kraft paper

- Specialty paper

- Recycled paper

- Others

- End-user

- Food service outlets

- Restaurants

- Households

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Type Insights

The non-polycoated segment is estimated to witness significant growth during the forecast period.

The non-polycoated paper segment is defined by materials achieving functional properties through inherent substrate characteristics rather than polymer films. Demand is driven by sustainability, as these biodegradable paper products align with circular economy packaging principles and stringent paper packaging regulations.

Innovations in food-grade paper manufacturing focus on non-polymeric additives and advanced fiber refining to enhance grease and moisture resistance, ensuring food product integrity without compromising recyclability.

This approach improves end-of-life processing, with new materials increasing compliance with packaging waste reduction targets by over 15%. This focus on a recyclable paper substrate for products like eco-friendly food wraps is crucial for brands targeting environmentally conscious consumers.

Such sustainable food packaging must also pass rigorous organoleptic properties testing to ensure it does not alter the taste or smell of food.

The Non-polycoated segment was valued at USD 93.72 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 35.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Food Contact Paper Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the market is led by APAC, which commands 35.52% of the global incremental growth opportunity, fueled by rapid urbanization and a burgeoning food service industry.

In this region, the demand for specialty packaging papers, particularly for ovenable paper trays and frozen food paperboard, is expanding. North America and Europe are mature markets driven by stringent food safety compliance and consumer demand for plastic-free food containers.

In North America, state-level regulations have accelerated the adoption of heat-sealable paperboard, improving packaging line efficiency by up to 10%. European markets prioritize circular economy packaging, driving innovation in microwavable paperboard and other specialty paper materials.

Key countries such as the United States, China, Germany, and India are pivotal, with their distinct regulatory environments shaping demand for kraft paper material and advanced oxygen barrier paper solutions.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global food contact paper market is navigating a complex transition defined by nuanced material choices and evolving regulations. The debate between non-polycoated vs polycoated food paper is central, with the former gaining favor due to its superior recyclability, although the latter often provides better barrier performance.

- The overall cost of sustainable food packaging remains a significant consideration, influencing adoption rates across different segments. For instance, businesses in regions with strict pfas-free greaseproof paper regulations face supply chain adjustments that can initially increase procurement expenses by up to 12% compared to regions with less stringent rules. This highlights the impact of policy on operational planning.

- A major challenge is the inadequacy of recycling infrastructure for paper cups, which hinders circularity goals. Meanwhile, innovation in bio-based barrier coatings for paper is accelerating, promising to bridge the performance gap. For everyday applications, determining the best paper for wrapping sandwiches involves balancing grease resistance, moisture control, and material cost.

- The safety of food-grade recycled paper is another critical area, governed by strict guidelines to prevent contaminant migration. Ultimately, the utility of kraft paper for food service outlets continues to expand, driven by its strength and favorable environmental profile.

What are the key market drivers leading to the rise in the adoption of Food Contact Paper Industry?

- The imperative for sustainability, underscored by a global backlash against plastics, is a key driver of market growth.

- Market growth is significantly driven by the expansion of the food service industry and the global shift away from plastics.

- The proliferation of quick service restaurant packaging and takeaway food containers, fueled by the rise of food delivery packaging, creates immense demand.

- This has led to a 25% year-over-year increase in the consumption of unbleached kraft paper and other paper-based products in food service outlet applications. The demand extends to household applications, with products like biodegradable baking paper seeing wider adoption.

- To ensure sustainability, there is a strong emphasis on responsible sourcing, with virgin wood pulp often requiring chain-of-custody certification.

- This aligns with extended producer responsibility schemes, making paper a strategically advantageous choice over plastic-free food containers that may lack a robust recycling infrastructure.

What are the market trends shaping the Food Contact Paper Industry?

- The emergence of advanced bio-based and functional barrier technologies represents a significant upcoming market trend. This is driven by the need for sustainable alternatives that do not compromise packaging performance.

- Key trends are reshaping the market, primarily through the emergence of advanced functional barrier coatings and sustainable packaging materials. The industry-wide move to phase out certain chemicals has driven a 30% increase in investment in pfas-free papers and aqueous dispersion coatings. This food packaging innovation is critical for meeting new regulations.

- The development of bio-based polymers and repulpable barrier technology for specialty paper material allows for the creation of high-barrier paper packaging that is also recyclable. Adopting these single-use plastic alternatives helps brands appeal to eco-conscious consumer demand.

- Furthermore, the use of smart packaging solutions offers enhanced traceability, with QR codes on custom printed food paper improving consumer engagement by over 20%.

What challenges does the Food Contact Paper Industry face during its growth?

- A key challenge affecting industry growth is balancing high-performance requirements with cost-competitiveness against traditional packaging materials.

- A primary market challenge is achieving performance and cost parity with plastic while navigating complex end-of-life logistics. Polycoated paper offers excellent barrier properties but complicates recycling, a key issue for compostable takeout packaging.

- The use of food-grade recycled fiber is limited by concerns over chemical migration testing, which requires advanced traceable packaging materials and can increase production costs by up to 15%. Developing mineral oil free paper and effective moisture vapor barriers without traditional additives adds further complexity.

- Furthermore, the inconsistent availability of industrial composting facilities limits the real-world benefits of compostable paper solutions. This gap in recycling infrastructure challenges supply chain transparency and the promise of safe food contact materials for items like confectionery wrapping paper.

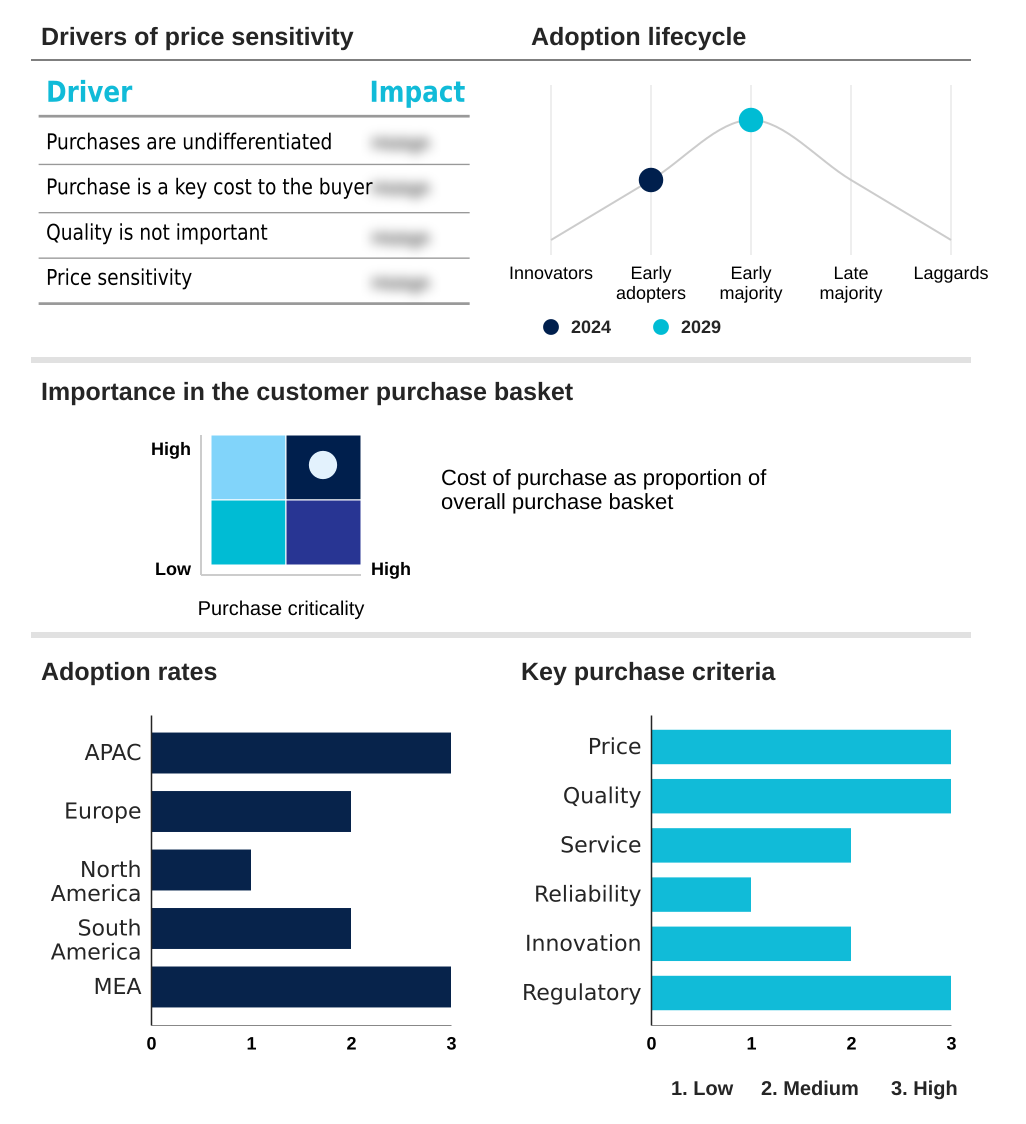

Exclusive Technavio Analysis on Customer Landscape

The food contact paper market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the food contact paper market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Food Contact Paper Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, food contact paper market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ahlstrom Oyj - Offerings include innovative, sustainable fiber-based materials, encompassing advanced filtration media, diagnostic components, and specialized food packaging solutions designed for safety and performance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ahlstrom Oyj

- Billerud AB

- delfortgroup AG

- Domtar Corp.

- Georgia Pacific LLC

- International Paper Co.

- ITC Ltd.

- JK Paper Ltd.

- KRPA Holding CZ AS

- Mondi Plc

- Nordic Paper AS

- Oji Holdings Corp.

- Sappi Ltd.

- Seaman Paper Co.

- Smurfit Westrock plc

- Stora Enso Oyj

- Twin Rivers Paper Co.

- UPM Kymmene Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Food contact paper market

- In September 2024, Mondi Plc announced a strategic partnership with a major European food delivery platform to co-develop a new line of sustainable, temperature-retaining packaging solutions designed to reduce plastic waste.

- In November 2024, Smurfit Kappa Group completed the acquisition of a specialty paper mill in Southeast Asia, aimed at expanding production capacity for high-barrier, PFAS-free food contact papers to meet escalating demand in the APAC market.

- In January 2025, Ahlstrom Oyj introduced a new line of fully compostable and recyclable grease-resistant papers featuring a proprietary plant-based coating as a sustainable alternative to traditional fluorochemical-treated papers.

- In April 2025, International Paper Co. announced a major capital investment in its North American mill system to upgrade pulp processing and paper coating capabilities, increasing the production of PFAS-free and recycled-content papers.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Food Contact Paper Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 303 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 11.4% |

| Market growth 2026-2030 | USD 107803.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 10.4% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Egypt and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The food contact paper market is in a period of fundamental change, moving decisively away from traditional materials toward sustainable alternatives. This evolution is driven by regulatory mandates and a clear consumer preference for environmentally responsible products.

- The core strategic issue for boardroom consideration is the investment required to pivot production towards innovative materials, such as pfas-free papers and those with aqueous dispersion coatings. This involves significant capital for developing repulpable barrier technology and ensuring food safety compliance through rigorous chemical migration testing.

- Companies that successfully integrate sustainable practices, like achieving chain-of-custody certification for virgin wood pulp, have documented a 20% improvement in meeting corporate environmental governance targets. The industry is responding with a focus on functional barrier coatings made from bio-based polymers and plant-based coatings.

- Innovations in non-polymeric additives and the use of unbleached kraft paper are enabling the creation of compostable paper solutions and recyclable paper substrate options that maintain performance without compromising safety, as verified by organoleptic properties testing. This strategic alignment is critical for market leadership.

What are the Key Data Covered in this Food Contact Paper Market Research and Growth Report?

-

What is the expected growth of the Food Contact Paper Market between 2026 and 2030?

-

USD 107.80 billion, at a CAGR of 11.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Non-polycoated, and Polycoated), Material (Kraft paper, Specialty paper, Recycled paper, and Others), End-user (Food service outlets, Restaurants, and Households) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Imperative for sustainability and global backlash against plastics, Balancing high performance requirements with cost competitiveness

-

-

Who are the major players in the Food Contact Paper Market?

-

Ahlstrom Oyj, Billerud AB, delfortgroup AG, Domtar Corp., Georgia Pacific LLC, International Paper Co., ITC Ltd., JK Paper Ltd., KRPA Holding CZ AS, Mondi Plc, Nordic Paper AS, Oji Holdings Corp., Sappi Ltd., Seaman Paper Co., Smurfit Westrock plc, Stora Enso Oyj, Twin Rivers Paper Co. and UPM Kymmene Corp.

-

Market Research Insights

- Market dynamics are shaped by a strong focus on sustainable food packaging and circular economy packaging principles, compelling businesses to adopt innovative materials. The shift toward single-use plastic alternatives has resulted in a 25% increase in R&D spending on high-barrier paper packaging.

- Firms leveraging traceable packaging materials report a 15% improvement in supply chain transparency, meeting heightened eco-conscious consumer demand for safe food contact materials. This strategic pivot is essential as food service paper supplies and quick service restaurant packaging formats evolve.

- Furthermore, the adoption of advanced digital printing for food packaging allows for rapid customization, enhancing brand engagement and supporting the complex needs of the growing food delivery packaging segment.

We can help! Our analysts can customize this food contact paper market research report to meet your requirements.

RIA -

RIA -