Forklift Trucks Market Size 2026-2030

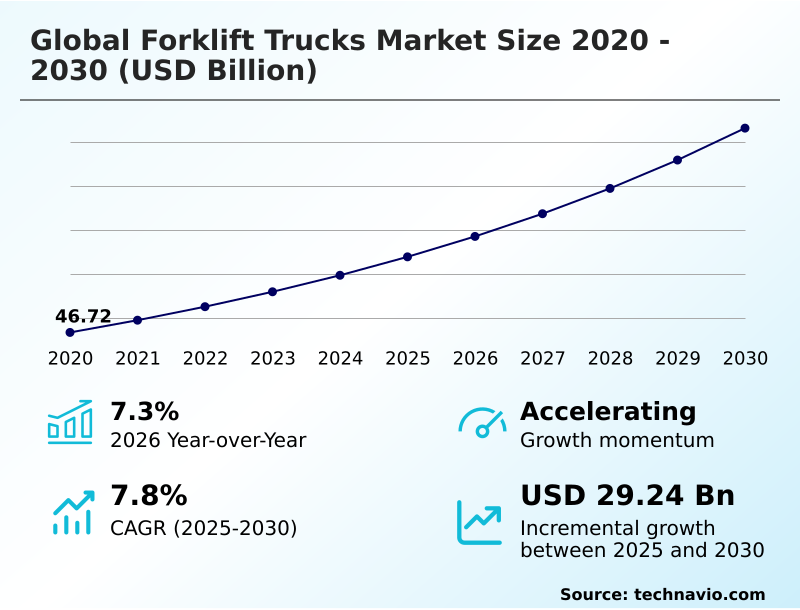

The forklift trucks market size is valued to increase by USD 29.24 billion, at a CAGR of 7.8% from 2025 to 2030. Rapid growth in construction sector will drive the forklift trucks market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 53.8% growth during the forecast period.

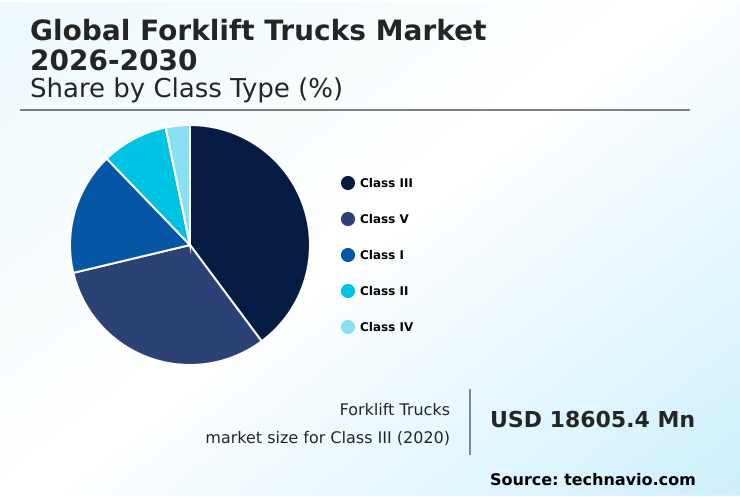

- By Class Type - Class III segment was valued at USD 23.75 billion in 2024

- By Type - Electric segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 46.42 billion

- Market Future Opportunities: USD 29.24 billion

- CAGR from 2025 to 2030 : 7.8%

Market Summary

- The forklift trucks market is characterized by a significant transformation driven by the dual pressures of e-commerce expansion and industrial modernization. The exponential growth in online retail necessitates the development of high-throughput warehouses, escalating demand for electric motor rider trucks and very narrow aisle trucks that maximize spatial efficiency.

- Concurrently, a persistent shortage of skilled operators is accelerating the adoption of warehouse automation, with companies leveraging automated guided vehicles and autonomous mobile robots to maintain productivity and enhance workplace safety.

- For instance, a large third-party logistics provider can deploy a fleet of automated forklifts for repetitive pallet-moving tasks, reallocating its human workforce to complex order-picking assignments, thereby improving overall operational efficiency. However, the high initial investment for advanced lithium-ion batteries and hydrogen fuel cell technology, coupled with stringent emission regulations for internal combustion engines, creates significant financial and compliance challenges.

- Balancing innovation with cost-effectiveness remains a central strategic focus for enterprises navigating this dynamic landscape.

What will be the Size of the Forklift Trucks Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Forklift Trucks Market Segmented?

The forklift trucks industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

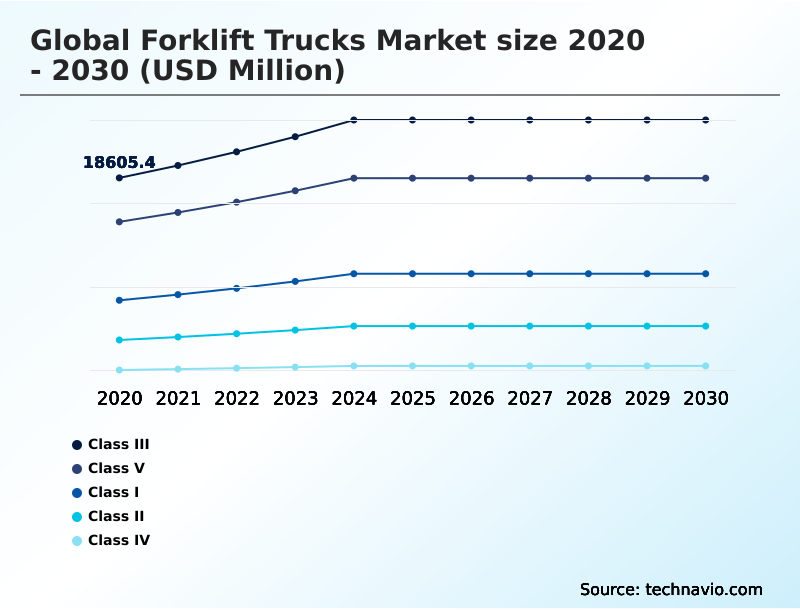

- Class type

- Class III

- Class V

- Class I

- Class II

- Class IV

- Type

- Electric

- Internal combustion engine

- End-user

- Industrial

- Manufacturing

- Construction

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Class Type Insights

The class iii segment is estimated to witness significant growth during the forecast period.

The Class III segment, comprising electric motor hand trucks, serves as a cornerstone for modern material handling equipment.

These zero-emission vehicles like pallet jacks are engineered for horizontal transport in warehouses and retail, excelling in last-mile delivery hubs and supporting lean manufacturing.

Their compact design and ergonomic control handles are crucial for navigating tight spaces common in urban fulfillment centers driven by e-commerce retail. Adoption of advanced batteries enables multi-shift operations through rapid opportunity charging, enhancing operational efficiency.

This is vital in environments like cold storage facilities, where uptime is critical. Integrating these machines with telematics for predictive maintenance has demonstrated the ability to improve picking accuracy by over 15%, reducing errors and boosting throughput.

The Class III segment was valued at USD 23.75 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 53.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Forklift Trucks Market Demand is Rising in APAC Get Free Sample

The geographic landscape is dominated by the APAC region, which accounts for over 53% of the market's incremental growth opportunity.

This is driven by massive industrialization, the Belt and Road Initiative, and the effects of the goods and services tax in key countries, which modernizes supply chains. The region's projected growth rate of 8.5% significantly outpaces Europe's 6.9%.

Demand spans from high-capacity container handlers and straddle carriers at major ports to specialized industrial vehicle types like sideloader forklifts and articulated forklifts in manufacturing. The trend towards nearshoring manufacturing further boosts the need for efficient equipment.

European markets, in contrast, focus more on green procurement strategies and the circular economy, with a high adoption of electric motor rider trucks and walkie straddle stacker models.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in fleet modernization revolve around key technological comparisons, such as hydrogen fuel cell vs lithium-ion forklifts, and understanding the impact of emission standards on forklift design. The ROI of automated forklift implementation is a critical boardroom topic, as the use of automated guided vehicles in warehouse logistics promises significant long-term gains despite high initial costs.

- An electric forklift maintenance cost comparison often reveals lower lifetime expenses, influencing the shift away from internal combustion models. For specific environments, selecting the right equipment is paramount, whether it is a rough terrain forklift for construction sites or a narrow aisle forklift for high-density storage.

- Advanced telematics for forklift fleet management can improve utilization by over 20% compared to fleets without such systems. This data-driven approach allows for forklift fleet optimization using data analytics and enables predictive maintenance for forklift hydraulic systems, further reducing total cost of ownership for forklifts.

- Operator-centric considerations, including ergonomics in forklift operator cabin design and advanced operator safety features in modern forklifts, are also crucial. Technology choices extend to components, with analysis of the benefits of pneumatic vs cushion tires and the latest forklift tyre technology for durability being key to performance in varied applications.

- Furthermore, integrating forklifts with warehouse management systems and understanding lithium-ion battery charging infrastructure requirements are essential for seamless operations, especially in cold storage forklift technology advancements and e-commerce fulfillment centers.

What are the key market drivers leading to the rise in the adoption of Forklift Trucks Industry?

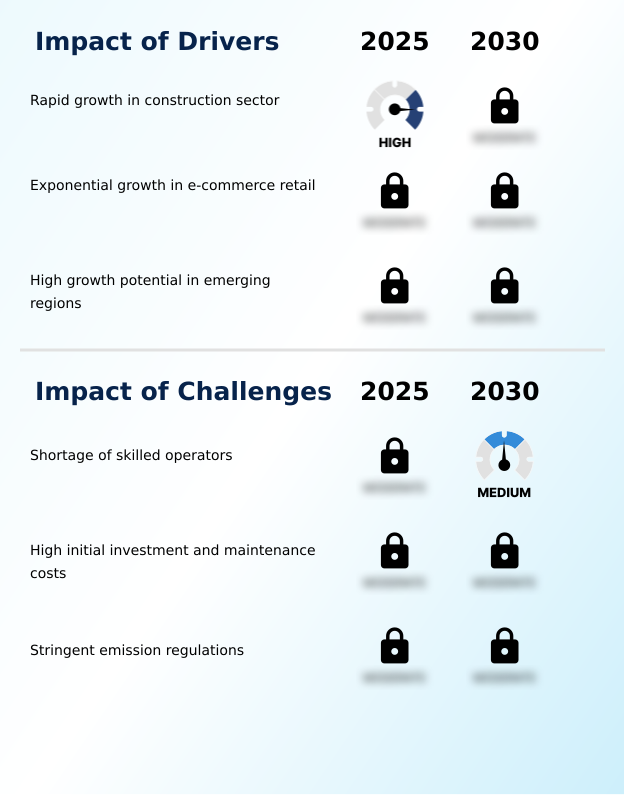

- Rapid growth in the global construction sector is a primary driver for the forklift trucks market, escalating the need for efficient material handling on job sites.

- The expansion of e-commerce retail is a primary market driver, fueling demand for modern logistics and warehousing infrastructure.

- This has led to a 15% year-over-year increase in demand for equipment suited for high-density storage systems, such as order pickers and pallet jacks. Third-party logistics providers are investing heavily to support rapid just-in-time delivery models.

- In parallel, the construction sector drives demand for heavy-duty applications, where rough terrain forklifts and telehandlers equipped with durable pneumatic tires are essential.

- Advanced fleet management systems are being deployed in these environments to monitor assets, improving energy efficiency and reducing fuel consumption by as much as 10%, a critical factor for profitability on large-scale projects.

What are the market trends shaping the Forklift Trucks Industry?

- The advent of hydrogen fuel cell-powered forklift trucks is an emerging market trend, presenting cleaner and more efficient power solutions compared to traditional alternatives.

- The market is advancing toward the fourth industrial revolution, driven by trends in warehouse automation and carbon neutral operations. Hydrogen fuel cell technology is a key innovation, allowing zero-emission vehicles to refuel in under three minutes, a vast improvement over the 6-8 hours for some battery types. This supports intense, multi-shift intralogistics.

- Simultaneously, the adoption of automated guided vehicles and autonomous mobile robots, integrated with warehouse management software, is redefining supply chain management. These systems, including very narrow aisle trucks with advanced operator presence detection, improve order fulfilment speed and can increase overall operational efficiency by up to 25% in high-volume distribution centers.

What challenges does the Forklift Trucks Industry face during its growth?

- A persistent shortage of skilled operators represents a key challenge for the forklift trucks market, constraining operational capacity and hindering industry growth.

- High initial investments and stringent emission regulations pose significant market challenges. The upfront cost for a forklift with lithium-ion batteries can be up to three times that of traditional internal combustion engines, impacting asset management strategies for many firms.

- Furthermore, compliance with standards like Stage V, which mandates particulate matter emissions below 0.015 g/kWh, requires complex exhaust aftertreatment systems, increasing the total cost of ownership. While AC motor technology improves performance, the industry also faces hurdles related to workplace safety.

- Adopting advanced driver assistance systems, load weight sensors, and operator training simulators is crucial but adds expense, balancing the need for better indoor air quality against budgetary constraints.

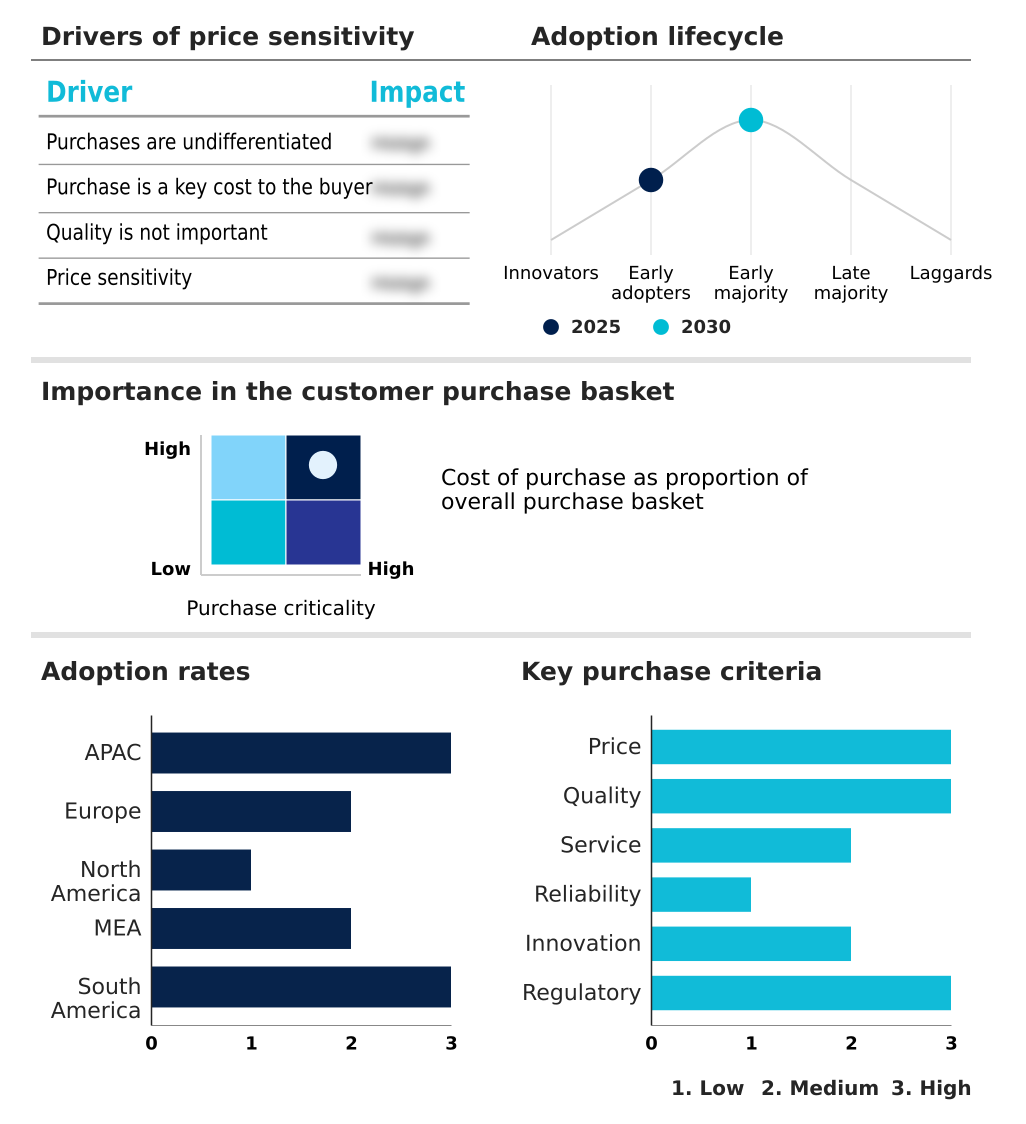

Exclusive Technavio Analysis on Customer Landscape

The forklift trucks market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the forklift trucks market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Forklift Trucks Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, forklift trucks market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Baumann Group SRL - Material handling solutions include electric and internal combustion forklifts engineered for high productivity and operational efficiency in demanding warehouse and industrial applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Baumann Group SRL

- BYD Co. Ltd.

- Clark Material Handling Co.

- Combilift Ltd.

- Crown Equipment Corp.

- Doosan Bobcat Inc.

- Godrej Enterprises Group

- Hangcha Group Co. Ltd.

- Hubtex Maschinenbau GmbH

- Hyster Yale Materials Handling Inc.

- Hyundai Motor Co.

- Jungheinrich Group

- Kalmar Corp.

- KION GROUP AG

- Lonking Holdings Ltd.

- Manitou BF SA

- Merlo Spa

- Mitsubishi Corp.

- Noblelift Equipment Co. Ltd.

- Toyota Industries Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Forklift trucks market

- In May, 2025, The Raymond Corporation debuted three new lithium-ion powered Class III pallet stacker models, the 6310 Walkie Straddle Stacker, the 6410 Walkie Reach Stacker, and the 6510 Walkie Counterbalanced Stacker, designed to boost efficiency and flexibility in warehouse operations.

- In April, 2025, Toyota Material Handling Europe and Plug Power announced a strategic collaboration with STEF to deploy advanced hydrogen-powered forklift trucks and fuel cell solutions at two cold storage distribution centers in France and Spain.

- In March, 2025, PALFINGER premiered its new FLM series middle-seat truck-mounted forklift at the bauma 2025 trade show, a prototype designed to enhance operator visibility, comfort, and ergonomics for transport and logistics applications.

- In January, 2025, Clark expanded its S-Series electric forklift range with new three-wheel and four-wheel models, designed to replace older combustion engine derivatives in the 48-volt segment with load capacities from 1.6 to 2 tonnes.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Forklift Trucks Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 304 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.8% |

| Market growth 2026-2030 | USD 29244.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.3% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Saudi Arabia, UAE, South Africa, Turkey, Qatar, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The forklift trucks market is undergoing a fundamental shift toward intelligent and sustainable operations, driven by technological advancements across its core components. The integration of hydrogen fuel cell technology and advanced lithium-ion batteries into zero-emission vehicles is redefining fleet capabilities, moving beyond traditional internal combustion engines.

- Innovations such as autonomous mobile robots, automated guided vehicles, and warehouse automation systems are becoming standard. These technologies, combined with robust warehouse management software and fleet management systems, enable unprecedented efficiency. For example, the deployment of advanced driver assistance systems and load weight sensors can reduce material damage incidents by over 15%.

- The market offers a diverse range of equipment, from rough terrain forklifts and telehandlers to specialized very narrow aisle trucks, order pickers, and pallet jacks. Key components like pneumatic tires, cushion tires, and non-marking tyres are evolving, while regenerative braking systems and AC motor technology enhance performance in electric motor rider trucks.

- The focus is on creating a connected, safe, and productive ecosystem.

What are the Key Data Covered in this Forklift Trucks Market Research and Growth Report?

-

What is the expected growth of the Forklift Trucks Market between 2026 and 2030?

-

USD 29.24 billion, at a CAGR of 7.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Class Type (Class III, Class V, Class I, Class II, and Class IV), Type (Electric, and Internal combustion engine), End-user (Industrial, Manufacturing, and Construction) and Geography (APAC, Europe, North America, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Rapid growth in construction sector, Shortage of skilled operators

-

-

Who are the major players in the Forklift Trucks Market?

-

Baumann Group SRL, BYD Co. Ltd., Clark Material Handling Co., Combilift Ltd., Crown Equipment Corp., Doosan Bobcat Inc., Godrej Enterprises Group, Hangcha Group Co. Ltd., Hubtex Maschinenbau GmbH, Hyster Yale Materials Handling Inc., Hyundai Motor Co., Jungheinrich Group, Kalmar Corp., KION GROUP AG, Lonking Holdings Ltd., Manitou BF SA, Merlo Spa, Mitsubishi Corp., Noblelift Equipment Co. Ltd. and Toyota Industries Corp.

-

Market Research Insights

- The market's dynamics are shaped by a strong focus on enhancing operational efficiency and achieving sustainability goals. The adoption of electric industrial vehicle fleets has been shown to reduce energy costs by up to 40% compared to legacy internal combustion models, a compelling incentive for green procurement strategies.

- In logistics and warehousing, the integration of advanced material handling equipment with warehouse management software can improve order fulfilment accuracy by over 25%. This push for technological integration is a response to the demands of e-commerce retail and the need for greater precision in supply chain management.

- As firms pursue carbon neutral operations, the shift toward technologies that improve energy efficiency is becoming a standard for maintaining a competitive edge in third-party logistics and manufacturing.

We can help! Our analysts can customize this forklift trucks market research report to meet your requirements.

RIA -

RIA -