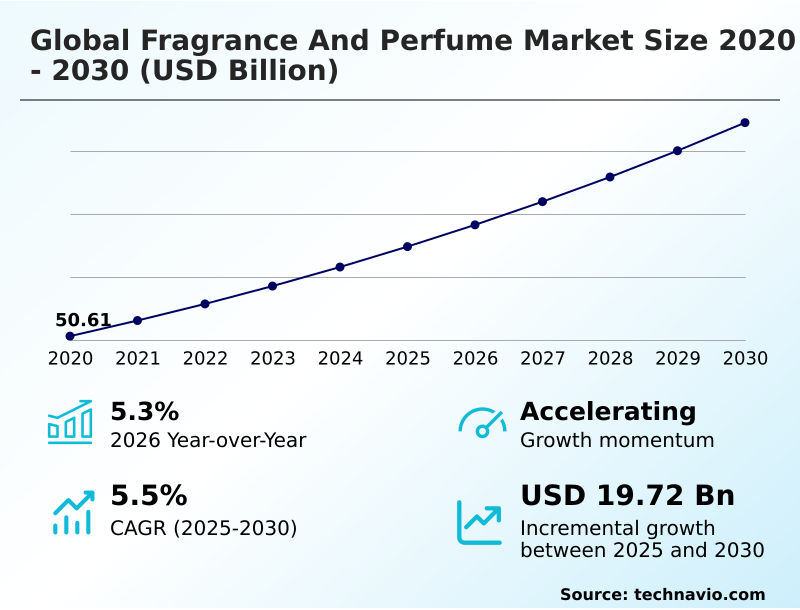

Fragrance And Perfume Market Size 2026-2030

The fragrance and perfume market size is valued to increase by USD 19.72 billion, at a CAGR of 5.5% from 2025 to 2030. Rising influence of social media will drive the fragrance and perfume market.

Major Market Trends & Insights

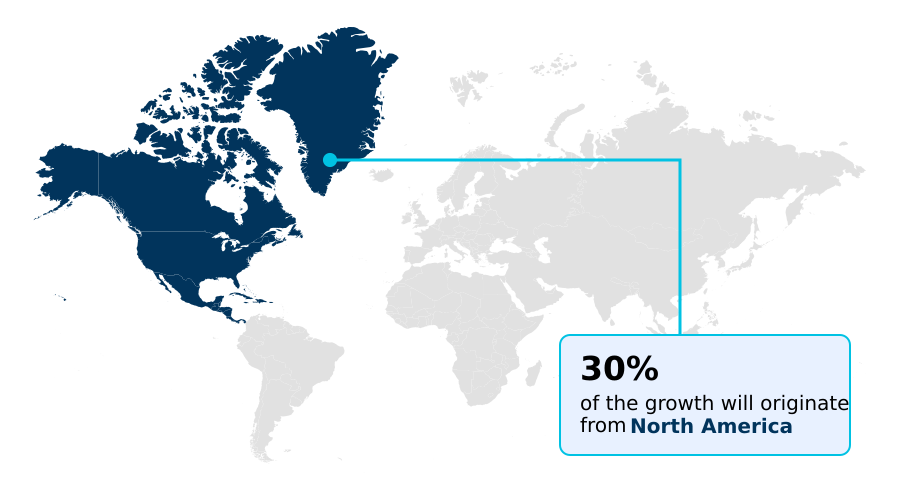

- North America dominated the market and accounted for a 30.4% growth during the forecast period.

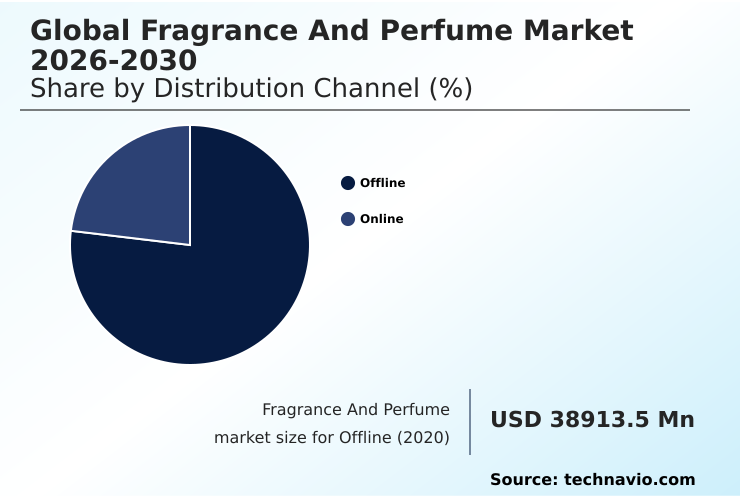

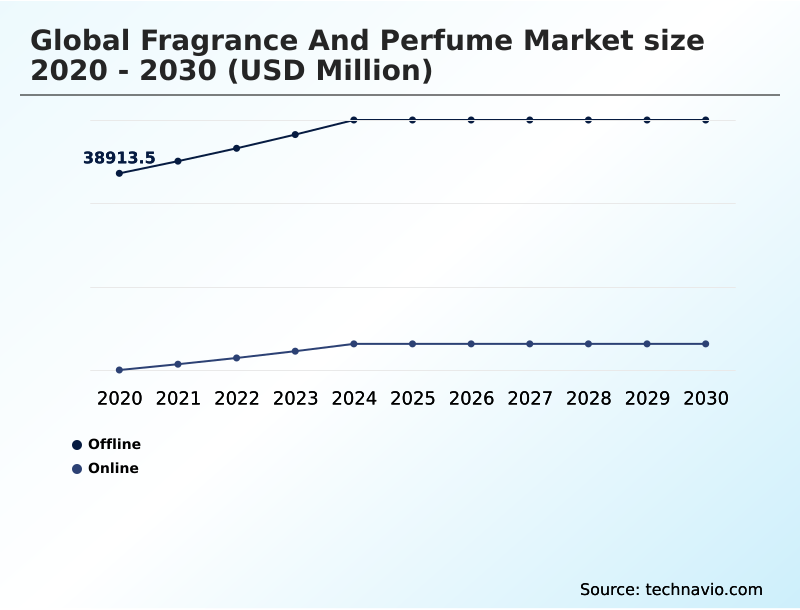

- By Distribution Channel - Offline segment was valued at USD 46.29 billion in 2024

- By Type - Fragrance segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 33.97 billion

- Market Future Opportunities: USD 19.72 billion

- CAGR from 2025 to 2030 : 5.5%

Market Summary

- The fragrance and perfume market is undergoing a significant transformation, moving beyond traditional luxury to embrace personalization, sustainability, and technological innovation. At its core, the industry develops products with complex blends of natural essential oils and synthetic aroma chemicals, designed to interact with olfactory receptors.

- However, consumer preferences are evolving, driving a pronounced shift towards plant-based ingredients and transparent, ethical sourcing practices. This trend is compelling brands to invest in green chemistry and biotechnology to create novel aroma molecules that are both high-performing and environmentally responsible.

- For instance, a mid-sized brand navigating this shift must balance the high cost of securing fair trade partnerships for its raw material sourcing against the marketing imperative of a 'clean' label. This challenge is compounded by the need to maintain consistent olfactive profiles while reformulating products to exclude certain synthetic fixatives, a process that demands significant R&D investment.

- The industry's future lies in its ability to merge the art of perfumery with scientific advancements, delivering sophisticated sensory experiences that align with modern values around health and wellness and environmental stewardship.

What will be the Size of the Fragrance And Perfume Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Fragrance And Perfume Market Segmented?

The fragrance and perfume industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Distribution channel

- Offline

- Online

- Type

- Fragrance

- Perfume

- End-user

- Women

- Men

- Unisex

- Geography

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- Europe

By Distribution Channel Insights

The offline segment is estimated to witness significant growth during the forecast period.

The offline segment remains the cornerstone of the fragrance and perfume market, with physical retail environments providing an essential platform for sensory storytelling and brand immersion.

Brick-and-mortar channels, including department stores and specialty boutiques, facilitate a tactile and olfactory experience that digital platforms cannot fully replicate, allowing consumers to engage with olfactive profiles and understand the complex transition of volatile molecules.

This direct interaction is critical for high-value purchases, where the perception of luxury is tied to the in-store experience.

Despite the growth of e-commerce, offline sales continue to dominate, accounting for approximately 75% of total market revenue, underscoring the enduring importance of physical touchpoints for consumer validation and discovery in the personal care products sector.

The Offline segment was valued at USD 46.29 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 30.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Fragrance And Perfume Market Demand is Rising in North America Get Free Sample

While Europe continues to be a benchmark for luxury perfumery, North America is poised to drive a significant portion of the market's future expansion, contributing over 30% of the incremental opportunity.

This growth is fueled by a strong consumer appetite for niche and artisan perfumery.

In APAC, which accounts for nearly 28% of the global opportunity, markets like China and South Korea are leading the adoption of digital retail channels for personal care products.

This digital-first approach has enabled brands to improve inventory turnover by as much as 15% by leveraging real-time sales data and targeted social media fragrance marketing.

The Middle East and Africa region also presents a strong market, rooted in a deep cultural appreciation for potent fragrance compounds and complex olfactive profiles.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

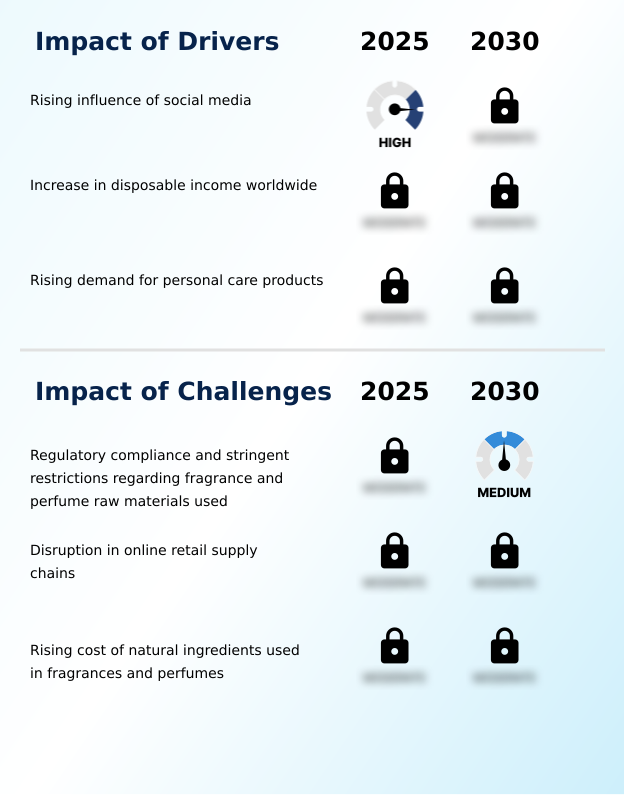

- The contemporary fragrance landscape is defined by the profound impact of social media on fragrance sales, which has elevated the consumer preference for natural perfume ingredients to a primary market driver. This shift creates significant operational hurdles, as companies must navigate complex regulations affecting perfume raw material sourcing.

- In response, the role of biotechnology in fragrance creation is expanding, offering sustainable alternatives. Simultaneously, trends in sustainable and eco-friendly packaging are becoming standard practice, driven by consumer demand and the impact of the clean beauty movement on perfumes.

- This environment has spurred the growth of niche and independent perfume houses, though they often grapple with challenges in fragrance supply chain management. Industry-wide, there are notable advancements in perfume delivery systems and innovation in long-lasting perfume technology.

- Marketing strategies for luxury fragrance brands now deeply integrate the psychology of scent and consumer behavior, with a clear trajectory toward the future of personalized perfume experiences. The use of AI for perfume recommendation is central to this evolution. The ongoing comparison of natural vs synthetic fragrances continues, while ethical considerations in animal-derived ingredients have nearly eliminated their use.

- This has amplified the demand for gender-neutral fragrance products. An analysis of the fragrance market in emerging economies reveals unique opportunities, particularly for the direct-to-consumer fragrance market, where brands can leverage how influencers shape fragrance buying habits to build loyalty faster than through traditional retail, showing a notably higher engagement rate.

What are the key market drivers leading to the rise in the adoption of Fragrance And Perfume Industry?

- The rising influence of social media platforms is a key driver for the market, shaping consumer preferences and purchasing behaviors through digital storytelling and influencer marketing.

- The primary driver is the pervasive influence of social media fragrance marketing, which has democratized scent discovery. Platforms enable powerful sensory branding and olfactory marketing, allowing DTC fragrance brands to compete with established houses.

- Influencer-led campaigns have demonstrated a 3x higher ROI than traditional advertising, illustrating a fundamental shift in marketing spend. Moreover, online perfume retail and fragrance subscription boxes are flourishing, as they lower the barrier to trial.

- This digital ecosystem fosters a community around men's fragrance trends and women's perfume preferences, with brands leveraging fragrance and emotion research to create more targeted and impactful campaigns.

- The resulting data on consumer fragrance behavior improves inventory management by up to 20% by better predicting demand.

What are the market trends shaping the Fragrance And Perfume Industry?

- The market is witnessing a significant trend driven by the growing consumer demand for fragrances formulated with natural and sustainable ingredients. This shift reflects a broader emphasis on transparency and environmental responsibility in personal care.

- A defining trend is the pivot toward natural perfume ingredients and sustainable fragrance packaging. The rise of niche perfume brands is challenging established players, as they often lead in artisan perfumery and cater to consumer demand for authenticity and unique olfactive profiles.

- These brands, which emphasize clean beauty fragrances and eco-friendly perfumes, are experiencing growth rates 25% higher than their mass-market counterparts. Furthermore, the adoption of refillable packaging, a key aspect of perfume packaging design, has enabled some companies to reduce their packaging waste by over 40%.

- This movement is also influencing celebrity fragrance endorsements, with partnerships now frequently highlighting ethical sourcing practices and a commitment to sustainability, reflecting a significant shift in consumer values.

What challenges does the Fragrance And Perfume Industry face during its growth?

- A key challenge affecting industry growth is the need for regulatory compliance amid stringent restrictions on the use of specific raw materials in fragrances and perfumes.

- A significant challenge lies in navigating stringent fragrance regulations and ensuring compliance with restrictions on raw material sourcing and perfume raw materials. The cost of reformulating a legacy product to meet new allergen safety standards can increase R&D expenditure by over 30%.

- This complexity is heightened by the rising cost of plant-based ingredients, which can compress margins by an average of 5-7% industry-wide. Furthermore, the technical details of perfume chemistry and the perfume manufacturing process require substantial investment in green chemistry and biotechnology to develop compliant yet effective stabilizing fixatives and fragrance compounds.

- Ensuring a stable supply chain for ethically sourced natural essential oils and synthetic aroma chemicals while maintaining consistent olfactive profiles remains a critical operational hurdle for all market participants.

Exclusive Technavio Analysis on Customer Landscape

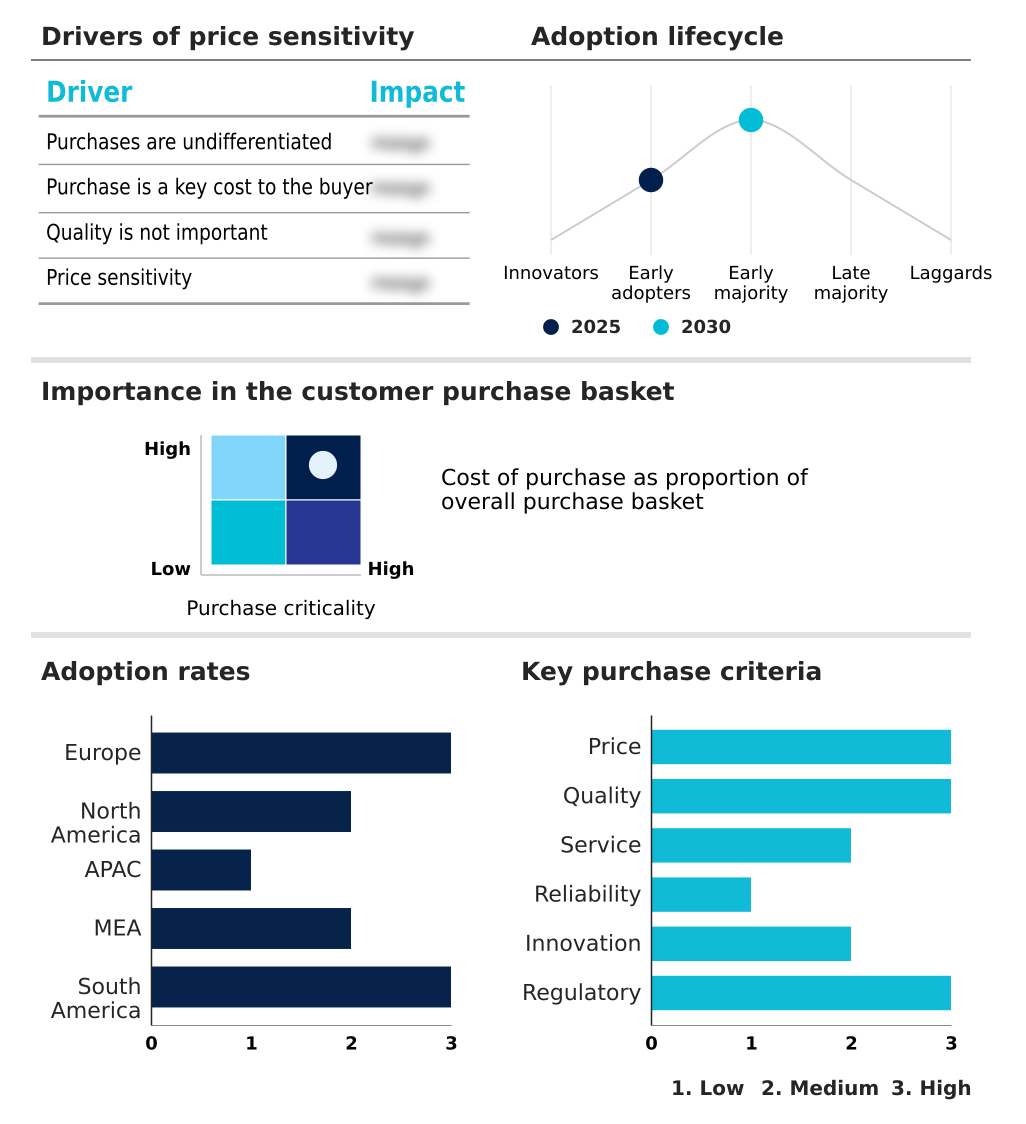

The fragrance and perfume market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the fragrance and perfume market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Fragrance And Perfume Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, fragrance and perfume market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Chanel Ltd. - Specializes in iconic fragrance and perfume creations, including globally recognized luxury scents that define olfactory branding and market prestige.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Chanel Ltd.

- Coty Inc.

- Dolce and Gabbana Srl

- DSM Firmenich AG

- Giorgio Armani SpA

- Givaudan SA

- Hermes International SA

- International Flavors Inc.

- Interparfums Inc.

- Kering SA

- Loreal SA

- LVMH Moet Hennessy

- PUIG S.L.

- Revlon Inc.

- Robertet SA

- Shiseido Co. Ltd.

- Symrise Group

- Takasago International Corp.

- The Estee Lauder Co. Inc.

- V Mane Fils

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Fragrance and perfume market

- In March, 2025, The European Union implemented the Clean Scent Initiative, a regulatory framework mandating full disclosure of all chemical constituents in fragrances to enhance consumer safety and environmental protection.

- In June, 2025, Lavie Luxe expanded its fragrance portfolio with the launch of Love and Pearl, two premium long-lasting perfumes, alongside the Shadow and Marine scents under its Lavie Sport line.

- In July, 2025, DHL partnered with multiple French perfume houses to launch a drone delivery pilot program for high-value fragrance orders in Paris and Berlin, aiming to reduce the carbon footprint of last-mile deliveries.

- In July, 2025, LVMH inaugurated a pioneering research facility in Grasse, France, dedicated to advancing the stabilization of volatile natural oils from rare flowers, aiming to enhance perfume longevity without using synthetic fixatives.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Fragrance And Perfume Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 285 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.5% |

| Market growth 2026-2030 | USD 19717.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.3% |

| Key countries | Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The fragrance and perfume market is defined by a complex interplay of art and science, where the creation of unique olfactive profiles depends on a sophisticated supply chain for perfume raw materials and fragrance raw materials.

- Firms are increasingly focused on raw material sourcing, prioritizing ethical sourcing practices and renewable harvesting methods to meet consumer demand for sustainable personal care products. The industry leverages advancements in biotechnology and green chemistry to develop novel fragrance compounds and cosmetic active ingredients, moving away from traditional synthetic fixatives.

- This shift is critical for ensuring allergen safety and complying with evolving regulations on chemical constituents. For instance, brands that have integrated carbon neutral substitutes and upcycled ingredients into their perfume formulation have reported a 20% increase in positive consumer sentiment online.

- This transition involves more than just ingredients; it extends to marketing through sensory storytelling and synesthesia marketing to connect with consumers on an emotional level. The integration of scent technology for advanced scent profiling is creating hyper-personalized products for both household care and health and wellness applications, showcasing the industry's dynamic evolution beyond traditional perfumery.

What are the Key Data Covered in this Fragrance And Perfume Market Research and Growth Report?

-

What is the expected growth of the Fragrance And Perfume Market between 2026 and 2030?

-

USD 19.72 billion, at a CAGR of 5.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Offline, and Online), Type (Fragrance, and Perfume), End-user (Women, Men, and Unisex) and Geography (Europe, North America, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

Europe, North America, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Rising influence of social media, Regulatory compliance and stringent restrictions regarding fragrance and perfume raw materials used

-

-

Who are the major players in the Fragrance And Perfume Market?

-

Chanel Ltd., Coty Inc., Dolce and Gabbana Srl, DSM Firmenich AG, Giorgio Armani SpA, Givaudan SA, Hermes International SA, International Flavors Inc., Interparfums Inc., Kering SA, Loreal SA, LVMH Moet Hennessy, PUIG S.L., Revlon Inc., Robertet SA, Shiseido Co. Ltd., Symrise Group, Takasago International Corp., The Estee Lauder Co. Inc. and V Mane Fils

-

Market Research Insights

- The dynamics of the fragrance and perfume market are increasingly shaped by digital transformation and a focus on personalized experiences. The rise of DTC fragrance brands and online perfume retail has fundamentally altered consumer engagement, with AI in perfume creation now enabling hyper-customization.

- These platforms leverage data on women's perfume preferences and men's fragrance trends to offer tailored recommendations, improving conversion rates by over 15% compared to traditional retail. Furthermore, brands that provide transparency around fragrance ingredient sourcing and the perfume manufacturing process report a 10% higher customer retention rate.

- This shift underscores a broader trend where sensory branding and social media fragrance marketing are becoming more critical than ever for capturing consumer attention in a competitive landscape.

We can help! Our analysts can customize this fragrance and perfume market research report to meet your requirements.

RIA -

RIA -