Frozen Food Market Size 2026-2030

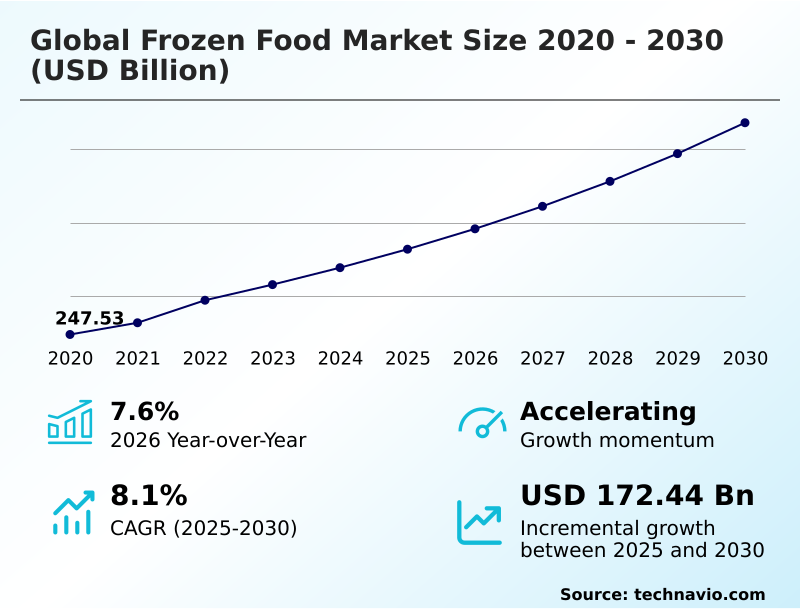

The frozen food market size is valued to increase by USD 172.44 billion, at a CAGR of 8.1% from 2025 to 2030. Integration of high-protein functional formulations and industrialization of nutrient-dense frozen entrees will drive the frozen food market.

Major Market Trends & Insights

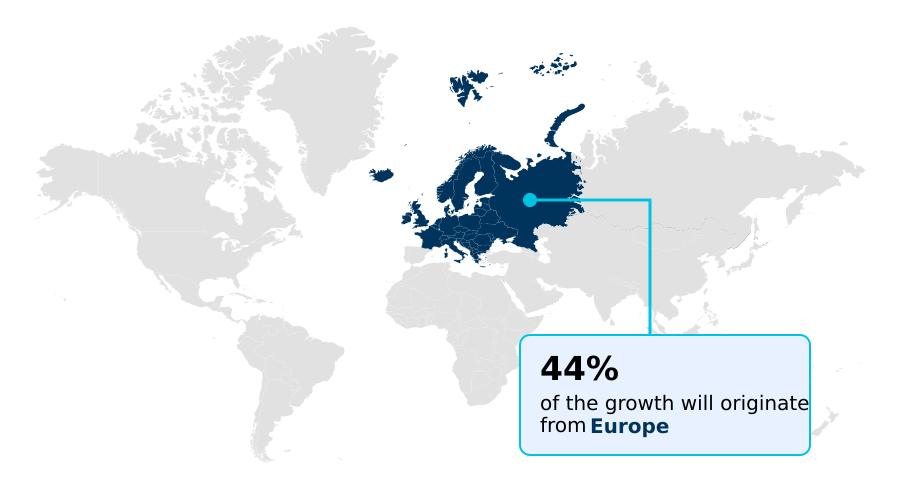

- Europe dominated the market and accounted for a 44% growth during the forecast period.

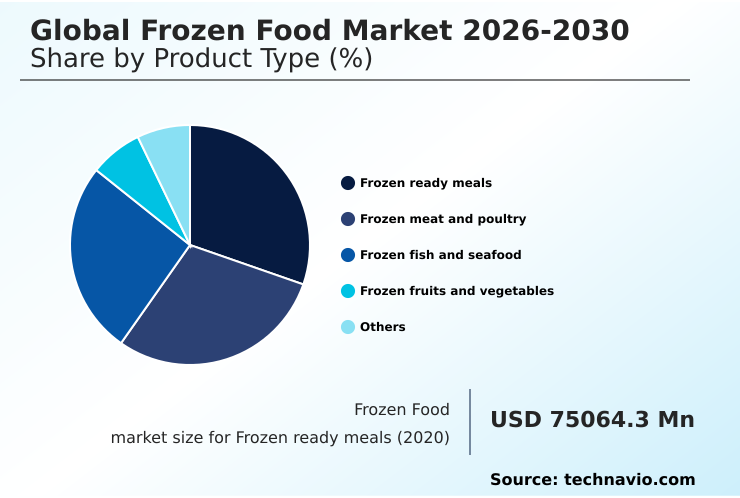

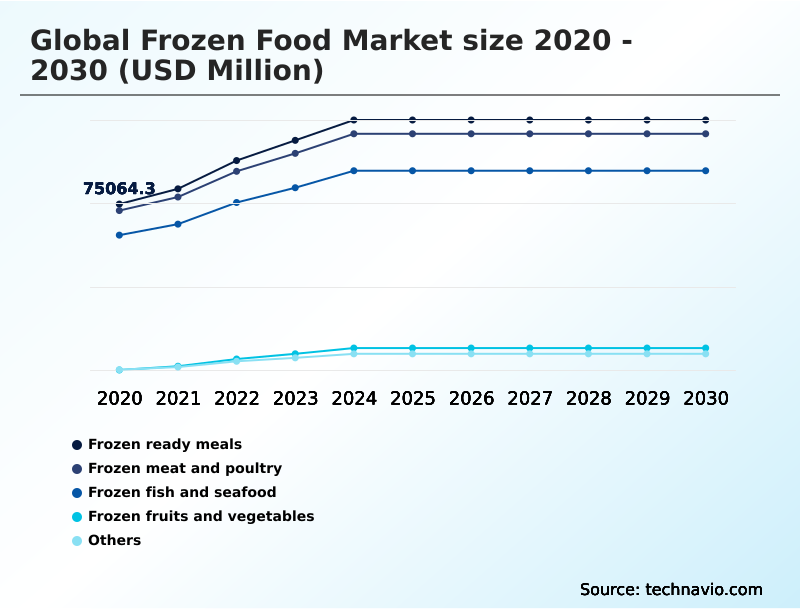

- By Product Type - Frozen ready meals segment was valued at USD 104.18 billion in 2024

- By Distribution Channel - Offline segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 288.74 billion

- Market Future Opportunities: USD 172.44 billion

- CAGR from 2025 to 2030 : 8.1%

Market Summary

- The frozen food market is undergoing a significant evolution, transitioning from a category of convenience staples to a sophisticated ecosystem of advanced nutritional solutions. This progression is driven by the convergence of consumer demand for health-oriented products and technological advancements in food preservation.

- Key drivers include the industrialization of high-protein functional formulations and nutrient-dense frozen entrees that cater to specific dietary and lifestyle needs. Trends such as clean-label functionalism and the adoption of global street-food authenticity are reshaping product development, moving offerings toward premium, experience-driven formats.

- These innovations are made possible by technologies like individual quick freezing (iqf), cryogenic freezing, and flash-freezing, which preserve texture and nutritional integrity. However, the industry grapples with challenges, including rising energy costs necessitating a shift to a low-carbon cold chain, and stringent requirements for digital traceability.

- For instance, a foodservice operator implementing a speed-scratch cooking model relies on pre-portioned high-quality components and par-baked frozen products to ensure menu consistency and manage labor shortages, all underpinned by robust cold-chain automation and inventory management.

What will be the Size of the Frozen Food Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Frozen Food Market Segmented?

The frozen food industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product type

- Frozen ready meals

- Frozen meat and poultry

- Frozen fish and seafood

- Frozen fruits and vegetables

- Others

- Distribution channel

- Offline

- Online

- Consumption pattern

- Retail

- Food service

- Geography

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- Europe

By Product Type Insights

The frozen ready meals segment is estimated to witness significant growth during the forecast period.

The frozen ready meals segment is a principal component of the market, driven by consumer demand for convenient, high-quality meal solutions that align with modern health trends.

This category has expanded to include texture-safe global cuisines and specialized frozen grain bowls, moving far beyond basic offerings.

Innovations in cryogenic freezing and thermodynamic innovation ensure product integrity, while the use of clean-label binders and natural antioxidants addresses wellness demands.

In response to consumer priorities, where nearly 40% now favor minimally processed options, the industry is adopting value-added packaging and active packaging to enhance shelf appeal and freshness, supported by robotic fulfillment centers to ensure frictionless replenishment.

The Frozen ready meals segment was valued at USD 104.18 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 44% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Frozen Food Market Demand is Rising in Europe Get Free Sample

The geographic landscape is defined by varied regional dynamics, with Europe accounting for 44% of the market’s incremental growth by focusing on sustainable sourcing practices and a low-carbon cold chain.

This addresses industrial energy pricing and helps decarbonize refrigeration networks to meet carbon-reduction targets. The adoption of advanced cold chain infrastructure utilizing individual quick freezing (iqf) and blast freezing for microbial growth arrest and enzymatic activity arrest has improved efficiency.

In contrast, APAC is expanding at 8.5%, fueled by urbanization and investment in modern logistics featuring rapid heat extraction methods and secure temperature-controlled storage to promote clean-label functionalism.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The technological evolution of the frozen food market is reshaping both product quality and operational efficiency. Central to this is the goal of achieving superior texture preservation in frozen bakery items and ensuring nutrient retention in flash-frozen produce. Advanced methods like cryogenic freezing for seafood quality and individual quick freezing for vegetables are becoming standard for premium lines.

- In the B2B sector, cold chain automation in foodservice is critical for enabling speed-scratch cooking with frozen components, a key strategy for firms seeking labor shortage solutions in food processing. This automation, coupled with ai-driven logistics for cold storage and robotic fulfillment for frozen e-commerce, enhances supply chain resilience.

- For instance, firms implementing ai-driven logistics have reported inventory accuracy improvements twice that of those using legacy systems. On the consumer front, demand is shifting toward high-protein formulations in frozen meals and specialized glp-1 friendly frozen meal options, reflecting broader wellness trends.

- This is complemented by the rising popularity of global street food frozen meal trends and plant-based protein frozen innovations. Addressing safety and sustainability involves implementing digital traceability for food safety, automating temperature monitoring in freezers, and using sustainable packaging for frozen goods.

- These measures also help in reducing food waste with frozen products, a key benefit as the industry confronts the impact of energy costs on cold chain operations and aims for shelf life extension via blast freezing.

What are the key market drivers leading to the rise in the adoption of Frozen Food Industry?

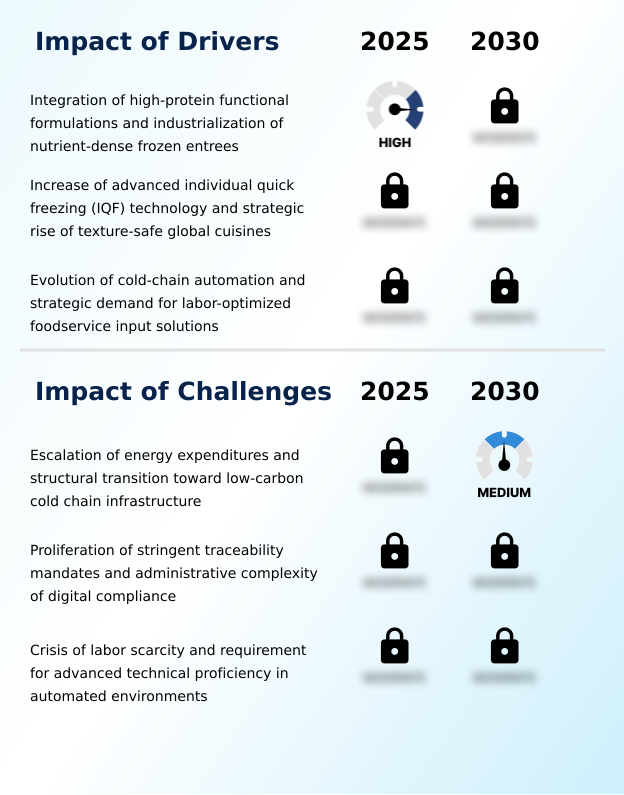

- The integration of high-protein functional formulations and the industrialization of nutrient-dense frozen entrees are key drivers propelling market growth.

- Key market drivers include the demand for high-protein functional formulations and nutrient-dense frozen entrees, including halal-certified packaged food, which require advanced lean protein stabilization. As subscription-based direct-to-consumer models grow, they leverage these offerings.

- In the B2B sector, cold-chain automation and labor-optimized foodservice solutions are paramount. Operators utilizing speed-scratch cooking with pre-portioned high-quality components reduce the need for skilled on-site preparation, achieving up to a 20% operational overhead reduction.

- Furthermore, warehouses employing ai-integrated freezing systems and multi-stage freezing tunnels are reporting inventory accuracy rates exceeding 99.9%, transforming supply chain efficiency.

What are the market trends shaping the Frozen Food Industry?

- The market is experiencing a significant trend toward the standardization of authentic global street-food flavors. This includes a notable increase in products featuring specific and spicy flavor profiles to meet adventurous consumer demand.

- A primary trend is the shift toward gastronomic escapism, driven by demand for global street-food authenticity. This is enabled by flash-freezing technologies that preserve up to 35% more volatile aromatic compounds than older methods. Concurrently, the rise of preservative-free transparency redefines products as frozen-as-fresh.

- Brands offering plant-forward entrees and minimally processed food with superfruit inclusions, including vacuum-sealed frozen meats, report repeat purchase rates 15% higher than their traditional counterparts. Innovations like smart tagging and non-thermal processing technologies, supported by in-store dual-temperature cross-merchandising, are central to this evolution.

What challenges does the Frozen Food Industry face during its growth?

- Escalating energy expenditures and the necessary structural transition toward low-carbon cold chain infrastructure present a key challenge affecting industry growth.

- The industry faces challenges from the proliferation of private-label frozen brands and the need for complex supply chains for items like shelf-stable vegetables and par-baked frozen products. Regulatory pressure mandates digital traceability and tamper-proof digital traceability for foodborne illness prevention, requiring investments in continuous monitoring systems and blockchain-enabled traceability.

- Labor challenges necessitate a shift to automated production lines and human-machine collaboration, where augmented reality training is essential. The wage premium for technicians who can manage predictive maintenance platforms using high-barrier films is now 15% higher, compounding operational costs.

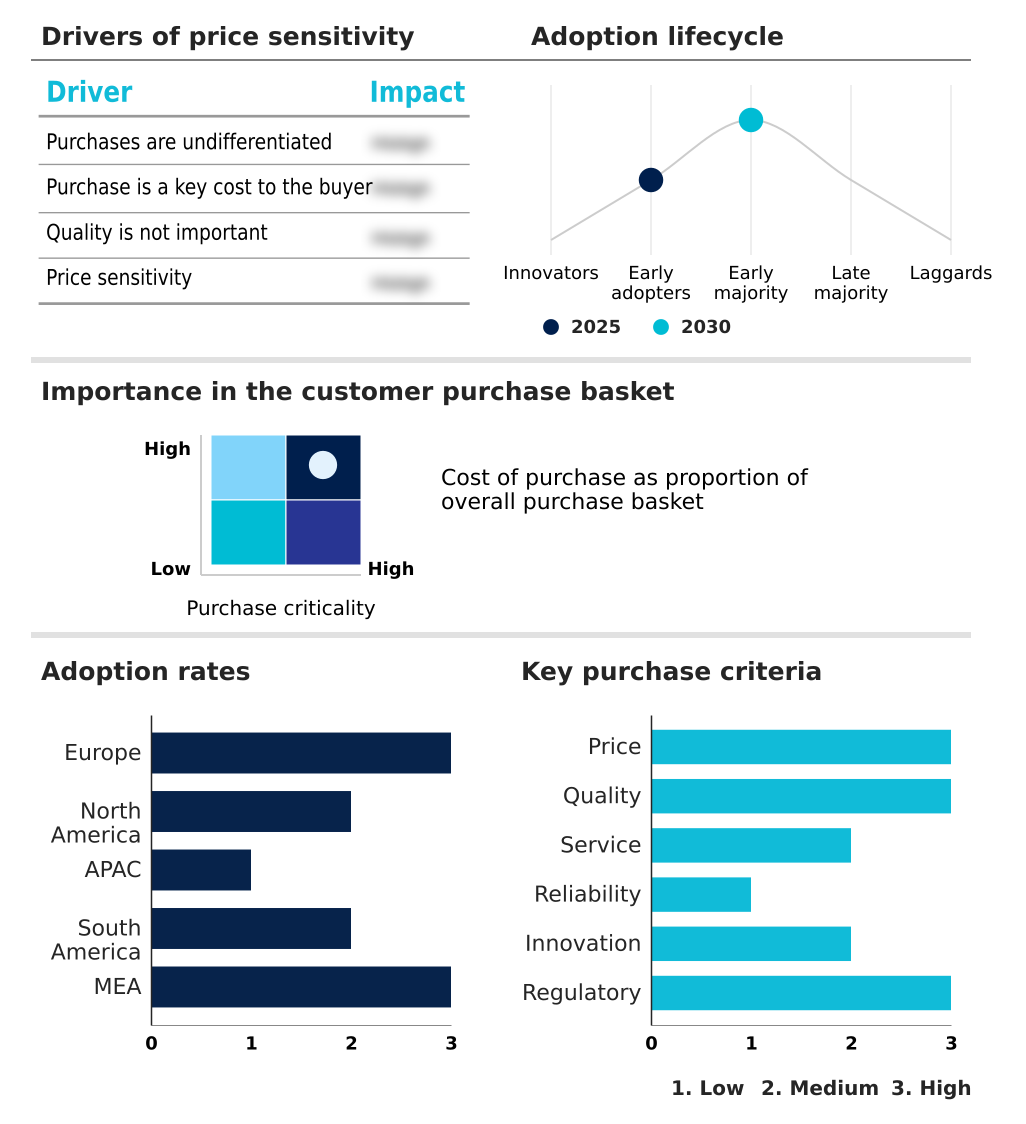

Exclusive Technavio Analysis on Customer Landscape

The frozen food market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the frozen food market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Frozen Food Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, frozen food market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ajinomoto Co. Inc. - The vendor's portfolio focuses on Asian frozen food specialties, including dumplings and complete meals, capitalizing on the demand for convenient, international flavors.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ajinomoto Co. Inc.

- Cargill Inc.

- Conagra Brands Inc.

- Corporativo Bimbo SA de CV

- Dr. August Oetker KG

- General Mills Inc.

- Goya Foods Inc.

- Hanover Foods Corp.

- J. R. Simplot Co.

- Kellanova

- Lantmannen Unibake

- McCain Foods Ltd.

- Nestle SA

- Nomad Foods Ltd.

- NORPAC Foods Inc.

- The Kraft Heinz Co.

- Tyson Foods Inc.

- Unilever PLC

- Vandemoortele NV

- Wawona Frozen Foods Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Frozen food market

- In September 2024, Himalaya Food International launched its line of frozen cinnamon French toast sticks in the United Kingdom, marking a strategic expansion into Western retail markets with its specialty breakfast products.

- In November 2024, Siniora Foods announced a $14 million investment to build a new manufacturing facility in Jeddah, Saudi Arabia, to increase its production capacity for cold cuts and frozen food items.

- In January 2025, Conagra Brands Inc. introduced specialized GLP-1 friendly labeling on its Healthy Choice frozen meal portfolio to cater to consumers using weight-loss medications.

- In April 2025, Ajinomoto Foods North America expanded a recall to include approximately 37 million pounds of frozen food products due to potential foreign material contamination, impacting both retail and foodservice channels.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Frozen Food Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 305 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.1% |

| Market growth 2026-2030 | USD 172444.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.6% |

| Key countries | Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The frozen food market is characterized by a strategic pivot toward technologically advanced production and supply chain management. Core processing methods now include individual quick freezing (iqf), cryogenic freezing, and blast freezing to ensure microbial growth arrest and maintain product quality.

- The industry's focus on high-protein functional formulations and nutrient-dense frozen entrees, often using clean-label binders, has become a key differentiator. This trend toward clean-label functionalism directly influences boardroom decisions regarding R&D investment and marketing strategy.

- Operationally, the entire value chain is being optimized through cold-chain automation and ai-driven logistics optimization, with firms leveraging ai-integrated freezing systems reporting processing time reductions of up to 30%. The move toward a low-carbon cold chain is imperative, driving innovation in temperature-controlled storage and the adoption of non-thermal processing technologies.

- To ensure safety and transparency, digital traceability, tamper-proof digital traceability, and blockchain-enabled traceability are being integrated into automated production lines that feature predictive maintenance platforms and support human-machine collaboration.

- This is complemented by innovations like dual-temperature cross-merchandising, active packaging, and value-added packaging for offerings such as frozen grain bowls, plant-forward entrees, and vacuum-sealed frozen meats, all managed through frictionless replenishment systems and robotic fulfillment centers.

What are the Key Data Covered in this Frozen Food Market Research and Growth Report?

-

What is the expected growth of the Frozen Food Market between 2026 and 2030?

-

USD 172.44 billion, at a CAGR of 8.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product Type (Frozen ready meals, Frozen meat and poultry, Frozen fish and seafood, Frozen fruits and vegetables, and Others), Distribution Channel (Offline, and Online), Consumption Pattern (Retail, and Food service) and Geography (Europe, North America, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

Europe, North America, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Integration of high-protein functional formulations and industrialization of nutrient-dense frozen entrees, Escalation of energy expenditures and structural transition toward low-carbon cold chain infrastructure

-

-

Who are the major players in the Frozen Food Market?

-

Ajinomoto Co. Inc., Cargill Inc., Conagra Brands Inc., Corporativo Bimbo SA de CV, Dr. August Oetker KG, General Mills Inc., Goya Foods Inc., Hanover Foods Corp., J. R. Simplot Co., Kellanova, Lantmannen Unibake, McCain Foods Ltd., Nestle SA, Nomad Foods Ltd., NORPAC Foods Inc., The Kraft Heinz Co., Tyson Foods Inc., Unilever PLC, Vandemoortele NV and Wawona Frozen Foods Inc.

-

Market Research Insights

- The market is undergoing a dynamic shift, leveraging thermodynamic innovation to enhance product quality while adopting new business models like subscription-based direct-to-consumer platforms. A focus on sustainable sourcing practices and pre-portioned high-quality components is becoming standard. Operationally, the adoption of continuous monitoring systems is proving critical, reducing spoilage-related losses by up to 25%.

- Concurrently, to address skilled labor gaps, companies implementing augmented reality training are achieving a 40% reduction in employee onboarding time compared to conventional methods, underscoring the industry's move toward technology-driven efficiency and quality assurance.

We can help! Our analysts can customize this frozen food market research report to meet your requirements.

RIA -

RIA -