Europe Frozen Food Market Size 2026-2030

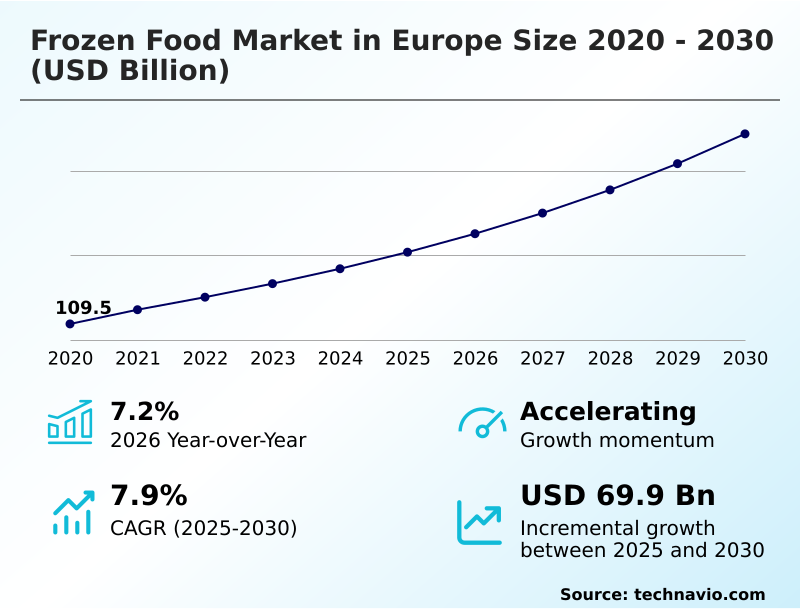

The europe frozen food market size is valued to increase by USD 69.9 billion, at a CAGR of 7.9% from 2025 to 2030. Institutionalization of anti-food waste mandates and sustainability goals will drive the europe frozen food market.

Major Market Trends & Insights

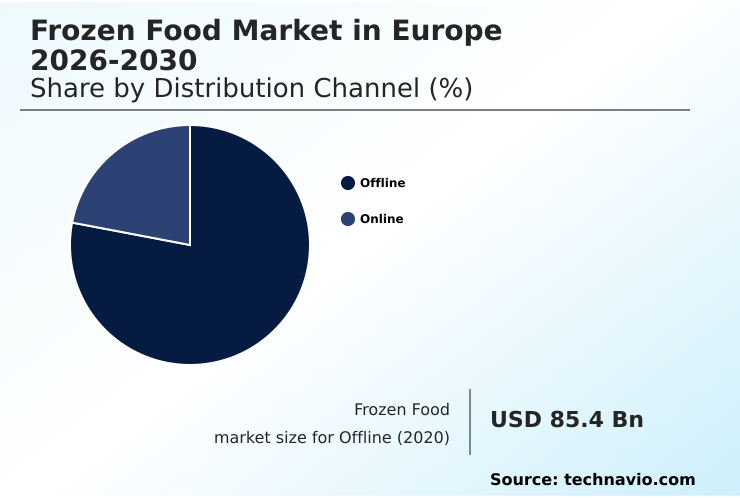

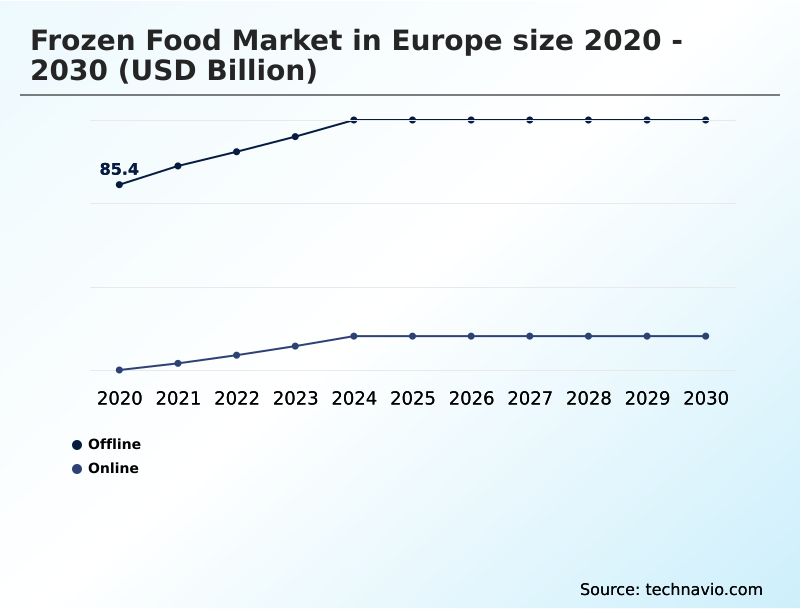

- By Distribution Channel - Offline segment was valued at USD 106.8 billion in 2024

- By Product - Frozen ready meals segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 112.3 billion

- Market Future Opportunities: USD 69.9 billion

- CAGR from 2025 to 2030 : 7.9%

Market Summary

- The frozen food market in Europe is undergoing a significant transformation, moving beyond convenience to embrace health, sustainability, and technological innovation. This evolution is driven by the institutionalization of food waste reduction strategies and the strategic proliferation of health-oriented, plant-forward ready meals.

- Advanced preservation techniques like individual quick freezing are central to this shift, as they lock in the nutritional value and texture of ingredients without synthetic preservatives, meeting consumer demand for clean-label products. A key business scenario involves optimizing cold chain logistics, where companies leverage AI-driven analytics to predict demand, manage inventory in zero-warehousing facilities, and ensure temperature-controlled distribution.

- This not only minimizes waste but also enhances operational efficiency in the face of volatile energy costs. Concurrently, the rise of ultrafast grocery delivery services is reshaping retail dynamics, creating new avenues for high-margin frozen products. However, the market faces challenges from stringent regulatory mandates on sustainable packaging and persistent consumer skepticism about ultra-processed formulations.

- Success in this landscape requires a balance of culinary innovation, technological adoption, and a demonstrable commitment to environmental stewardship and nutritional transparency, ensuring frozen food remains a vital part of the modern European diet.

What will be the Size of the Europe Frozen Food Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Europe Frozen Food Market Segmented?

The europe frozen food industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Distribution channel

- Offline

- Online

- Product

- Frozen ready meals

- Frozen fish and seafood

- Frozen meat and poultry

- Frozen fruits and vegetables

- Others

- End-user

- Retail consumers

- Foodservice

- Institutional buyers

- Geography

- Europe

- Italy

- Germany

- France

- Europe

By Distribution Channel Insights

The offline segment is estimated to witness significant growth during the forecast period.

The offline segment remains the structural backbone of the frozen food market in Europe, where physical retail environments are critical for maintaining cold chain logistics.

Supermarkets and hypermarkets are heavily investing in energy-efficient refrigeration to enhance the visibility of private-label offerings and innovative plant-based proteins. These retailers leverage the tactile shopping experience, allowing consumers to scrutinize clean-label ingredients and sustainable packaging.

This channel is the primary forum for introducing new nutrient-dense entrees and is crucial for foodservice procurement. Advanced inventory management systems are now used to ensure optimal product quality, reducing energy consumption in refrigeration units by up to 15%.

The strategic placement of products and in-store promotions are vital for driving sales and encouraging the discovery of new frozen food categories.

The Offline segment was valued at USD 106.8 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The intricate dynamics of the frozen food market in Europe are increasingly defined by the interplay between operational costs and technological innovation. The impact of energy prices on frozen food logistics is a primary concern, as maintaining the integrity of refrigerated transport and zero warehousing is non-negotiable.

- This challenge is driving investment in advanced technologies, where the role of AI in optimizing frozen food quality has become paramount. For instance, AI-driven individual quick freezing systems not only enhance nutritional density but also reduce energy consumption by up to 15% compared to legacy batch-freezing methods, directly impacting the bottom line.

- Concurrently, consumer trends in plant-based frozen meals continue to surge, forcing manufacturers to innovate with high-moisture meat analogues and sophisticated plant-based proteins. However, this innovation is met with significant challenges in sustainable packaging for frozen products, as new mono-material films must provide adequate moisture barriers at sub-zero temperatures while complying with the EU's circular economy model.

- The evolution of the market is further accelerated by how quick-commerce is changing frozen food retail, turning frozen goods into a high-margin, impulse-buy category in major urban centers. This requires a complete rethinking of supply chain challenges in cold chain logistics, from automated fulfillment centers to last-mile temperature management.

What are the key market drivers leading to the rise in the adoption of Europe Frozen Food Industry?

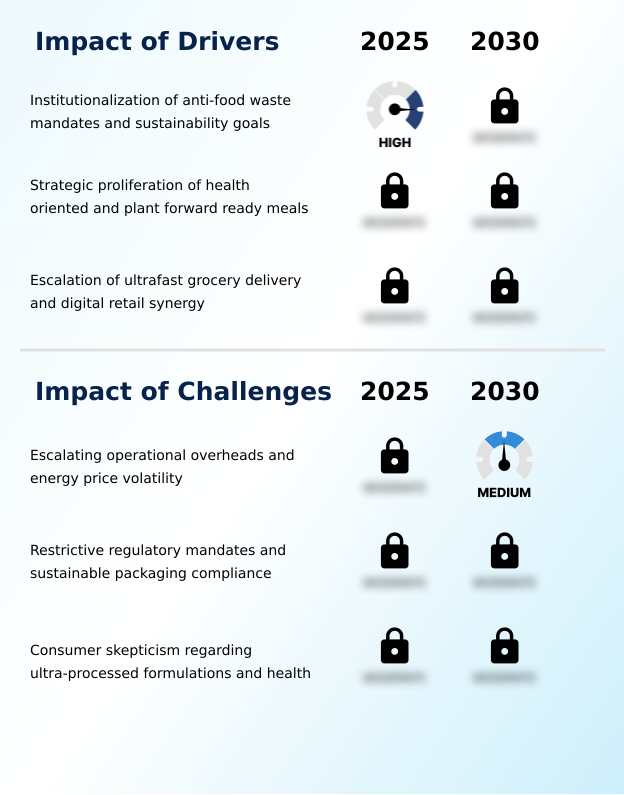

- The institutionalization of anti-food waste mandates and sustainability goals is a primary driver for the market.

- The growth of the frozen food market in Europe is propelled by powerful, interconnected drivers.

- A primary driver is the institutionalization of anti-food waste mandates, as frozen products with superior portion control can reduce household food waste by up to 45%.

- This aligns with the strategic proliferation of health-oriented and plant-forward ready meals, which use flash-freezing technology to preserve the nutritional value of clean-label ingredients without additives. This trend caters to rising consumer demand for nutrient-dense entrees.

- A third major driver is the escalation of ultrafast grocery delivery and digital retail synergy.

- Quick-commerce platforms in urban centers have seen a 40% year-over-year increase in frozen food sales, turning frozen goods into a high-margin, convenience-driven category and necessitating innovations in last-mile transport and automated fulfillment centers.

What are the market trends shaping the Europe Frozen Food Industry?

- The industrialization of plant-based ready meal engineering represents a key market trend, driven by consumer demand for sophisticated and sustainable frozen entrees.

- Key trends shaping the frozen food market in Europe center on technological and product evolution. The industrialization of plant-based ready meal engineering is advancing rapidly, with high-moisture meat analogues and sophisticated plant-based proteins becoming standard.

- In parallel, advancements in circular and regulatory-compliant packaging are critical, with new mono-material films offering a 20% weight reduction over traditional multi-layer plastics while ensuring product integrity. The most transformative trend is the evolution of AI-driven individual quick freezing, where optical sorters now achieve 99.5% accuracy in defect removal.

- This technology not only enhances the nutritional density of organic vegetables but also optimizes energy use, a crucial factor given the high costs of refrigerated transport and cold chain logistics. These innovations collectively push the market toward premium, sustainable, and technologically advanced solutions.

What challenges does the Europe Frozen Food Industry face during its growth?

- Escalating operational overheads and energy price volatility present a significant challenge to industry growth.

- The frozen food market in Europe confronts significant operational and regulatory headwinds. A primary challenge is the escalating operational overhead from energy price volatility, with electricity for zero warehousing and refrigerated transport accounting for up to 30% of logistics costs. This financial pressure is compounded by restrictive regulatory mandates for sustainable packaging.

- Complying with new EU rules to eliminate non-recyclable plastics can increase packaging expenses by 10–15% for manufacturers transitioning to mono-material films. Furthermore, persistent consumer skepticism regarding ultra-processed formulations and health impacts remains a hurdle. Overcoming this requires substantial investment in reformulating products with clean-label ingredients, which adds to R&D costs and puts pressure on profit margins across the industry.

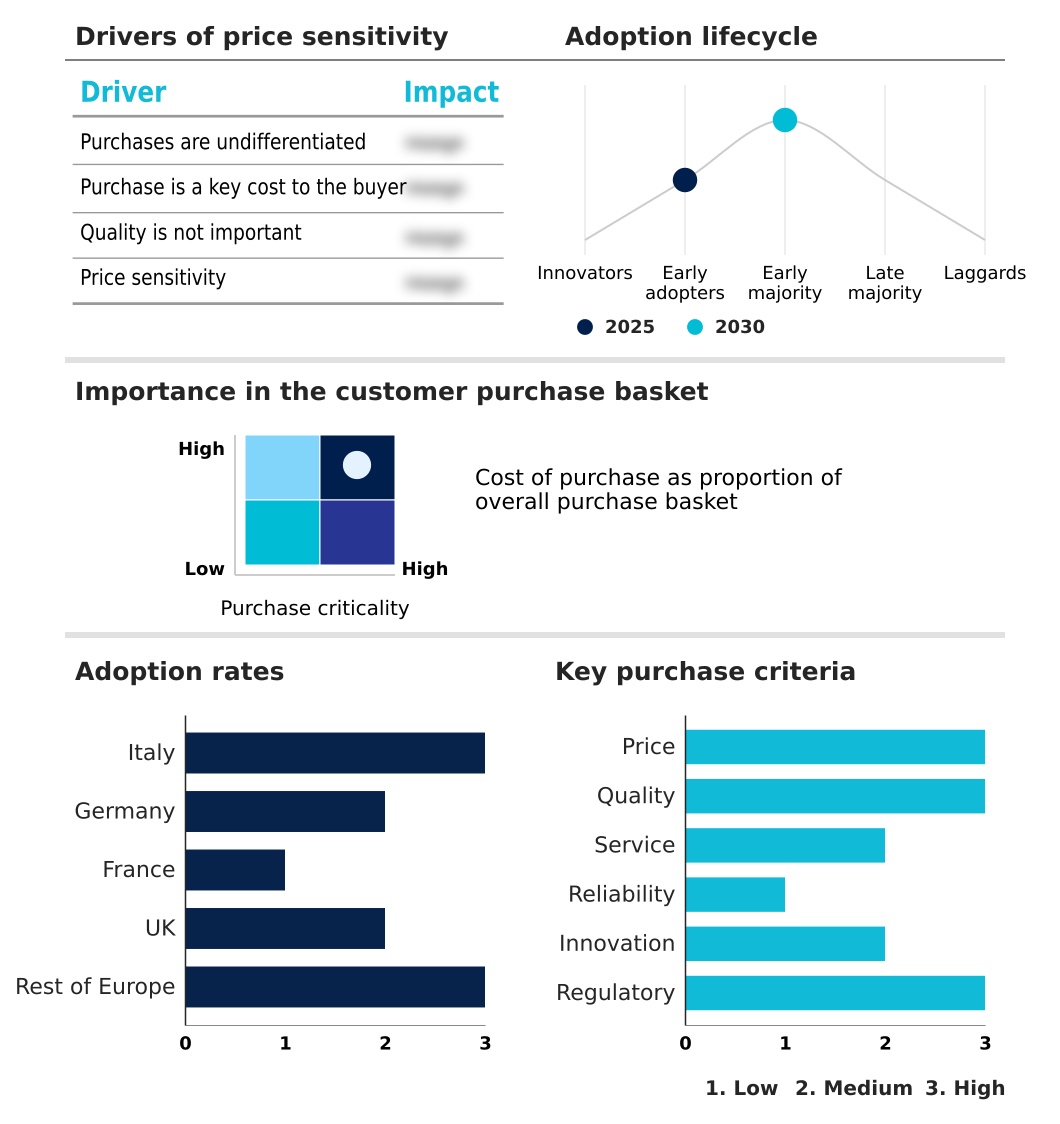

Exclusive Technavio Analysis on Customer Landscape

The europe frozen food market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the europe frozen food market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Europe Frozen Food Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, europe frozen food market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ajinomoto Co. Inc. - The company provides a wide range of frozen foods, including frozen dumplings, gyoza, and ready-to-eat meal products.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ajinomoto Co. Inc.

- ARYZTA AG

- BRF SA

- Cargill Inc.

- Dr. August Oetker KG

- Farmersland GmbH

- Freiberger Lebensmittel GmbH

- Frostkrone Food Group

- General Mills Inc.

- Iceland Foods Ltd.

- JBS SA

- Lantmannen Unibake

- McCain Foods Ltd.

- Nestle SA

- Nomad Foods Ltd.

- Orkla ASA

- The Kraft Heinz Co.

- Tyson Foods Inc.

- ULTRACONGELADOS VIRTO SAU

- Zumdieck GmbH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Europe frozen food market

- In April 2025, Nomad Foods Ltd. finalized a major regional leadership restructuring, appointing dedicated presidents for southern and central Europe to enhance commercial execution and operational efficiency across key markets.

- In February 2025, the Packaging and Packaging Waste Regulation (EU) 2025/40 officially entered into force, introducing legally binding sustainability and recyclability mandates for all packaging materials in the market by August 2026.

- In January 2025, Iceland Foods Ltd. reached a resolution in its long-standing trademark dispute with the nation of Iceland, following a ruling by the European Union General Court that clarified the limitations on geographic brand exclusivity.

- In October 2024, McCain Foods Ltd. launched its third 'Farm of the Future' in North Yorkshire, UK, a facility designed to pilot regenerative agriculture practices and develop circular nutrient systems at a commercial scale.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Europe Frozen Food Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 218 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.9% |

| Market growth 2026-2030 | USD 69.9 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.2% |

| Key countries | Italy, Germany, France, UK and Rest of Europe |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The frozen food market in Europe is navigating a structural recalibration driven by the convergence of consumer demands for nutritional density and stringent sustainability mandates. Key industry participants are leveraging advanced flash-freezing technology and cryogenic freezing to deliver premium frozen desserts and nutrient-dense entrees, moving away from ultra-processed formulations.

- The adoption of energy-efficient cold chain technologies, which can reduce the total carbon footprint by up to 20%, is now a critical boardroom-level decision tied to both compliance and brand reputation. Innovations in sustainable packaging, such as mono-material films and resealable pouches, are essential for meeting the EU's circular economy model.

- Concurrently, the proliferation of plant-based proteins and high-moisture meat analogues reflects a fundamental shift in dietary preferences. This transition is supported by automated fulfillment centers and quick-commerce services, which are revolutionizing temperature-controlled distribution and last-mile transport.

- For manufacturers, balancing clean-label ingredients with the operational realities of zero warehousing, food safety regulations, and supply chain sustainability is the defining challenge of the current landscape.

What are the Key Data Covered in this Europe Frozen Food Market Research and Growth Report?

-

What is the expected growth of the Europe Frozen Food Market between 2026 and 2030?

-

USD 69.9 billion, at a CAGR of 7.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Offline, and Online), Product (Frozen ready meals, Frozen fish and seafood, Frozen meat and poultry, Frozen fruits and vegetables, and Others), End-user (Retail consumers, Foodservice, and Institutional buyers) and Geography (Europe)

-

-

Which regions are analyzed in the report?

-

Europe

-

-

What are the key growth drivers and market challenges?

-

Institutionalization of anti-food waste mandates and sustainability goals, Escalating operational overheads and energy price volatility

-

-

Who are the major players in the Europe Frozen Food Market?

-

Ajinomoto Co. Inc., ARYZTA AG, BRF SA, Cargill Inc., Dr. August Oetker KG, Farmersland GmbH, Freiberger Lebensmittel GmbH, Frostkrone Food Group, General Mills Inc., Iceland Foods Ltd., JBS SA, Lantmannen Unibake, McCain Foods Ltd., Nestle SA, Nomad Foods Ltd., Orkla ASA, The Kraft Heinz Co., Tyson Foods Inc., ULTRACONGELADOS VIRTO SAU and Zumdieck GmbH

-

Market Research Insights

- The frozen food market in Europe is shaped by a confluence of technological advancements and evolving consumer behaviors. The adoption of AI-driven individual quick freezing techniques has led to significant quality improvements, with automated optical sorters increasing defect detection accuracy by over 20% compared to conventional methods.

- This focus on premiumization aligns with the growth of health-oriented frozen food, where clean-label and high-protein frozen meals are increasingly sought after. Simultaneously, the integration of quick-commerce services has revolutionized retail, with sales of frozen food via digital channels experiencing a 40% year-over-year increase in key urban centers.

- This growth is supported by investments in robotic fulfillment centers and specialized last-mile transport solutions. However, this digital synergy is tempered by the high operational costs of maintaining the cold chain, where energy expenses and temperature maintenance during transit remain critical concerns for profitability.

We can help! Our analysts can customize this europe frozen food market research report to meet your requirements.

RIA -

RIA -