Generative AI Cybersecurity Market Size 2025-2029

The generative AI cybersecurity market size is forecast to increase by USD 11.61 billion, at a CAGR of 35.4% between 2024 and 2029.

- The market is witnessing significant growth, driven by the escalating sophistication and proliferation of AI-generated threats. Malicious actors are increasingly leveraging AI to create complex and evasive cyber threats, making it challenging for traditional security solutions to keep up. In response, there is a growing trend towards the adoption of AI-augmented cybersecurity tools and platforms. These solutions utilize AI to analyze vast amounts of data and identify patterns and anomalies that may indicate cyber threats. Another key driver in the market is the proliferation of AI-specific governance, risk, and compliance platforms. Anomaly detection algorithms, powered by machine learning models and deep learning techniques, are increasingly being used to identify and respond to cyber threats in real-time.

- However, challenges remain. One significant challenge is the lack of standardization and interoperability between different AI cybersecurity solutions. This makes it difficult for organizations to implement a cohesive and effective AI security strategy. Additionally, the rapidly evolving nature of AI technology and cyber threats presents ongoing challenges for cybersecurity professionals. They must stay up-to-date with the latest developments to effectively protect their organizations. Cloud security solutions are essential as businesses increasingly migrate their operations to the cloud.

What will be the Size of the Generative AI Cybersecurity Market during the forecast period?

Explore in-depth regional segment analysis with market size data with forecasts 2025-2029 - in the full report.

Request Free Sample

- The market for generative AI in cybersecurity continues to evolve, with applications expanding across various sectors. Model integrity verification, a critical aspect of AI security, ensures the accuracy and trustworthiness of AI models. AI adversarial attacks, a growing concern, attempt to manipulate AI systems through deceptive inputs. AI system authentication verifies the identity of AI entities, while vulnerability scanning and penetration testing identify weaknesses and potential threats. Threat intelligence, an essential component of AI security, analyzes data to anticipate and respond to cyber threats. AI security frameworks and architectures provide a structured approach to implementing AI security solutions. AI security certification validates the compliance and effectiveness of these solutions.

- According to recent industry reports, the global AI cybersecurity market is expected to grow by over 20% annually, driven by the increasing adoption of AI in business operations and the continuous unfolding of market activities and evolving patterns. For instance, a leading financial services company reported a 35% reduction in security incidents after implementing an AI-powered threat detection system. Companies looking to capitalize on this opportunity must focus on developing interoperable solutions and staying abreast of the latest technological advancements and cybersecurity trends. This dynamic market encompasses solutions for network security, cloud security, endpoint protection, identity and access management, and threat intelligence.

How is this Generative AI Cybersecurity Market segmented?

The generative AI cybersecurity market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029,for the following segments.

- Component

- Software

- Services

- Type

- Network security

- Threat detection and analysis

- Adversarial defense

- Insider threat detection

- Others

- Technology

- GANs

- DNNs

- VAEs

- Reinforcement learning

- Others

- End-user

- BFSI

- Retail and e-commerce

- Government and defense

- Healthcare and life sciences

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South America

- Brazil

- Rest of World (ROW)

- North America

By Component Insights

The Software segment is estimated to witness significant growth during the forecast period. The market is witnessing significant growth, with the software segment serving as its cornerstone. This segment comprises platforms, applications, and tools that either employ generative AI for security enhancements or secure AI models themselves. Innovation is at the forefront, with market players concentrating on two primary value propositions: utilizing AI for security and ensuring security for AI. The first proposition harnesses the power of generative models, such as large language models (LLMs), to bolster security functions. Advanced threat detection systems use LLMs to identify new malware signatures, while AI-driven phishing simulators generate hyper-realistic lures for training purposes.

Security copilots, acting as conversational assistants for security analysts, are another application. The second proposition focuses on securing generative AI models. Homomorphic encryption and differential privacy techniques are employed to protect sensitive data, while model explainability methods ensure transparency and accountability. Neural network security, AI data anonymization, and synthetic data security are crucial components, as well. Responsible AI development, machine learning security, and AI system compliance are essential aspects, with market participants emphasizing the importance of ethical AI and regulatory adherence. Data poisoning defense mechanisms, generative AI watermarking, and adversarial example detection are also integral to maintaining model integrity.

Get Key Insights on Market Forecast (PDF)- Request Free Sample

Regional Analysis

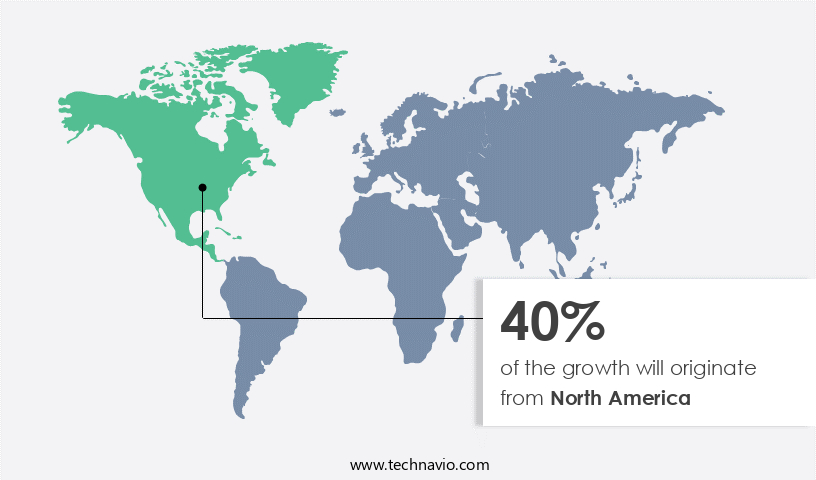

North America is estimated to contribute 40% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How generative AI cybersecurity market Demand is Rising in North America Request Free Sample

The North American market for generative AI cybersecurity is leading the global landscape, driven by the presence of foundational model developers, a competitive enterprise technology sector, a mature venture capital ecosystem, and a proactive regulatory environment. Enterprises in this region, including those in the United States and Canada, have been early adopters of large language models for productivity, customer service, and software development. This trend, while offering significant opportunities, also exposes them to novel threats such as prompt injection attacks, data poisoning, and the generation of malicious content. To mitigate these risks, the market is witnessing the adoption of advanced security solutions. Log management and analysis help detect and respond to anomalous behavior, and artificial intelligence (AI) and machine learning (ML) technologies enhance threat intelligence and improve overall security posture.

Homomorphic encryption is being employed to secure AI models during computation, ensuring data privacy and confidentiality. Model explainability methods are being used to increase transparency and trust in AI systems, enabling responsible AI development. Neural network security is being strengthened to protect against adversarial examples and data poisoning attacks. AI data anonymization and differential privacy are being utilized to safeguard sensitive information. Generative model robustness is being highlighted to prevent the creation and spread of malicious content. Synthetic data security is gaining traction to address data scarcity while maintaining data privacy. The market is also focusing on AI system compliance and implementing data poisoning defense mechanisms.

Generative AI watermarking and adversarial example detection are emerging as crucial techniques to ensure the integrity and authenticity of AI-generated content. The market is expected to grow at a significant rate, reaching over 25% of the total cybersecurity spending by 2025. However, there is a cyber talent shortage, making it essential for organizations to invest in cloud-based cybersecurity solutions and advanced technologies like AI and ML for network security, cloud application security, and endpoint security.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage. The market is experiencing significant growth as organizations seek to mitigate the unique risks posed by adversarial attacks on AI systems. These attacks, which can include prompt injection and the use of adversarial examples in AI, require new approaches to enhancing generative model robustness. To address these challenges, companies are investing in solutions that improve AI model explainability, allowing for better understanding of how AI makes decisions and improving the ability to detect and respond to attacks. Implementing AI data anonymization techniques and access control mechanisms are also crucial for securing AI systems.

Creating AI incident response plans and using AI security monitoring tools help organizations respond effectively to threats in real-time. Conducting regular AI security audits and managing risks effectively are also critical components of an effective AI security strategy. Ensuring AI system compliance with regulations and building a secure AI development lifecycle are also key considerations. The implementation of AI security governance frameworks and risk assessment methodologies can help organizations establish best practices and measure the effectiveness of their AI security efforts. Establishing AI security awareness training programs and adopting AI security best practices are also important for ensuring the long-term success of AI cybersecurity initiatives.

Measuring AI security effectiveness metrics and maintaining AI data protection and privacy compliance are essential for maintaining the trust and confidence of customers and stakeholders. The market is a dynamic and evolving landscape, requiring organizations to stay informed about the latest threats and trends and invest in solutions that can help them effectively manage the unique risks associated with AI systems. Developing AI security testing frameworks and applying AI threat modeling methods are essential for identifying vulnerabilities and potential attacks. Email security and access control systems protect sensitive data, while vulnerability prioritization and digital forensics aid in effective remediation.

What are the key market drivers leading to the rise in the adoption of Generative AI Cybersecurity Industry?

- The proliferation of AI-augmented cyber threats serves as the primary catalyst for market growth in this domain. The market is experiencing exponential growth due to the increasing use of sophisticated cyber threats fueled by generative artificial intelligence. Malicious actors are rapidly adopting these advanced tools, transforming the threat landscape and rendering traditional cybersecurity defenses obsolete. This offensive arms race necessitates organizations to implement commensurate AI-powered defensive mechanisms to safeguard their digital assets. Generative AI significantly reduces the entry barrier for less skilled threat actors, democratizing advanced attack capabilities. Previously, creating convincing phishing emails, developing new malware strains, or executing complex social engineering schemes required considerable expertise, time, and resources.

- According to recent reports, the market is expected to grow by over 30% in the next five years, underscoring the urgency for businesses to invest in robust defensive solutions. For instance, a leading financial institution reported a 15% increase in successful phishing attacks after a generative AI model was used to craft convincing emails. This trend underscores the need for organizations to prioritize AI-powered cybersecurity solutions to stay ahead of evolving threats. However, widely available or specialized malicious large language models (LLMs) can now automate these tasks with alarming efficiency.

What are the market trends shaping the Generative AI Cybersecurity Industry?

- The trend in the market involves the increasing prevalence of specialized governance, risk, and compliance platforms for artificial intelligence. The market is experiencing significant growth as organizations recognize the need for specialized AI Governance, Risk, and Compliance (GRC) platforms. This shift marks a pivotal moment in the market, progressing from reactive threat detection to a comprehensive, AI-centric approach. Regulatory pressures, potential for substantial reputational damage, and the inherent complexity of large language models are primary catalysts for this evolution.

- As a result, a burgeoning category of solutions is emerging to offer a unified system of record for an organization's AI usage. A recent study indicates a 12% increase in AI security investments among businesses, underscoring the industry's anticipated growth. Traditional security and GRC solutions are found wanting when confronted with the unique risks associated with generative AI, including algorithmic bias, model transparency, data privacy infringements, and intellectual property leakage.

What challenges does the Generative AI Cybersecurity Industry face during its growth?

- The escalating sophistication and proliferation of AI-generated threats pose a significant challenge to the industry's growth, requiring continuous advancements in cybersecurity measures to mitigate potential risks. The market is characterized by the dual-use potential of its core technology, posing significant challenges for businesses worldwide. Large language models (LLMs) and diffusion models, utilized by cybersecurity firms to develop defensive systems, are also employed by malicious actors to create sophisticated threats. This dynamic results in a continuous and resource-intensive arms race, with defensive innovations constantly countered by equally advanced offensive measures.

- They can now generate polymorphic malware, craft hyper-realistic phishing emails, and execute complex social engineering campaigns using deepfake audio and video. According to recent estimates, the market is expected to grow by over 25% annually, underscoring the urgency for businesses to invest in advanced defensive solutions. For instance, a financial services company reported a 50% reduction in phishing attacks after implementing a generative AI-powered email security system. The ease of access to sophisticated cyberattack tools has lowered the barrier to entry for novice threat actors.

Exclusive Customer Landscape

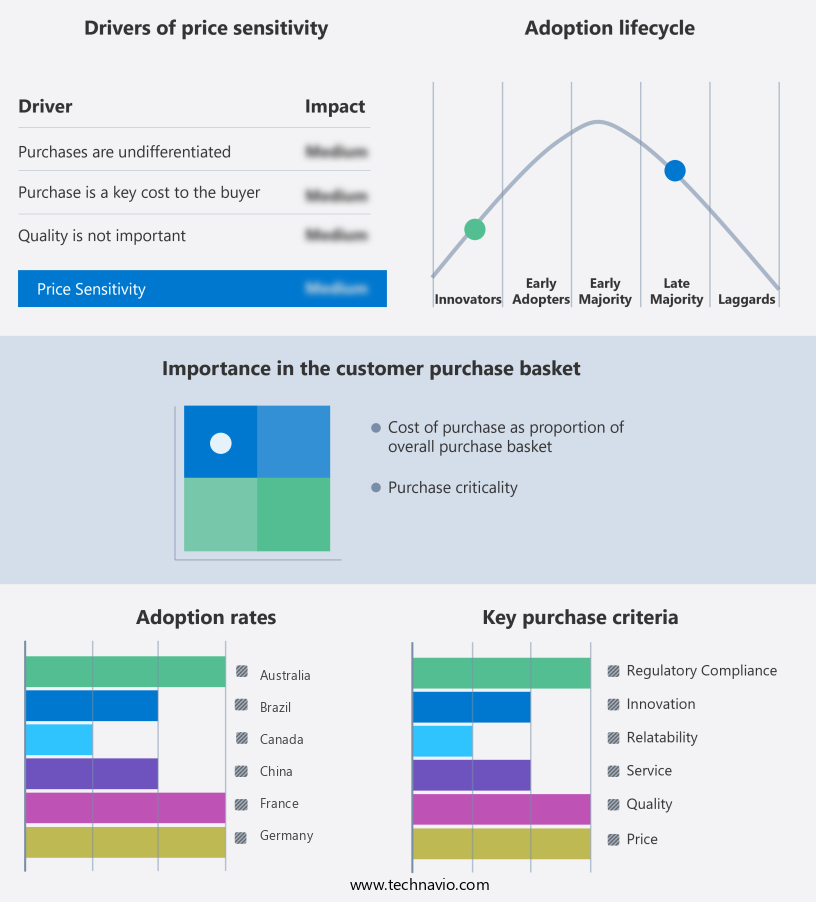

The generative AI cybersecurity market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the generative AI cybersecurity market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, generative AI cybersecurity market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture PLC - The company's mySecurity suite leverages advanced generative AI technology for robust cybersecurity solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture PLC

- Amazon Web Services Inc.

- Check Point Software Technologies Ltd.

- Cisco Systems Inc.

- Cloudflare Inc.

- CrowdStrike Inc.

- Cyera Ltd.

- Darktrace Holdings Ltd.

- Fortinet Inc.

- Google LLC

- INKY Technology Corp.

- International Business Machines Corp.

- Microsoft Corp.

- Netskope Inc.

- NVIDIA Corp.

- Palo Alto Networks Inc.

- SENTINELONE Inc.

- Splunk Inc.

- Vectra AI Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Generative AI Cybersecurity Market

- In January 2024, CyberSecurity Ventures, a leading cybersecurity research firm, announced the launch of their new Generative AI Cybersecurity product, "AIGuard," designed to predict and prevent advanced cyber threats using machine learning algorithms. (Source: CyberSecurity Ventures press release)

- In March 2024, IBM Security and Microsoft announced a strategic partnership to integrate IBM's AI-powered security platform, QRadar, with Microsoft's Azure Sentinel. This collaboration aimed to enhance threat detection and response capabilities for joint customers. (Source: IBM and Microsoft press releases)

- In May 2024, Darktrace, a leading cybersecurity AI company, raised USD100 million in a Series F funding round, bringing their total funding to USD 400 million. The investment was led by KKR and will be used to expand their global presence and accelerate product development. (Source: Darktrace press release)

- In December 2024, the European Union Agency for Cybersecurity (ENISA) published guidelines on the use of Generative AI in cybersecurity. The document provided recommendations for implementing AI in threat detection, incident response, and risk assessment, emphasizing the importance of transparency, explainability, and accountability. (Source: ENISA press release)

Research Analyst Overview

- The Generative AI Cybersecurity Market is witnessing rapid growth as organizations adopt advanced measures to protect AI-driven systems from emerging threats. Core challenges include AI model security, large language model security, and deep learning security risks, as well as evolving cybersecurity vulnerabilities in AI. Strategies such as AI bias mitigation techniques, AI system integrity checks, and AI ethics and security are critical to ensuring trust and fairness. With rising threats like prompt injection attacks, experts highlight mitigating prompt injection attacks and detecting adversarial examples in AI. Data protection remains paramount, driven by data privacy regulations in AI, differential privacy in AI, and homomorphic encryption in AI to safeguard sensitive information. Organizations are deploying AI system access control mechanisms, AI infrastructure security, and AI model monitoring tools to ensure operational resilience.

- Proactive defense includes AI incident response plans, AI security audit procedures, AI vulnerability scanning, AI penetration testing, and AI red teaming exercises to simulate attacks. Additionally, AI threat intelligence, AI risk assessment methods, and AI risk assessment methodology implementation strengthen defense frameworks. Governance is reinforced through AI data governance frameworks and AI security governance framework implementation. Operational best practices involve AI model version control, AI model retraining strategies, AI model retraining frequency, and improving AI model explainability via explainable AI (XAI). Compliance is ensured through AI security policy compliance and conducting AI security audits, alongside robust AI security metrics and AI security maturity assessments.

- The market also sees growth in AI security consulting services, AI security technology roadmaps, AI security incident management, AI security incident reporting, AI security awareness programs, and AI security talent acquisition. With building a secure AI development lifecycle and managing AI security risks effectively, stakeholders are increasingly deploying AI security solutions for future-proof protection.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Generative AI Cybersecurity Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

261 |

|

Base year |

2024 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 35.4% |

|

Market growth 2025-2029 |

USD 11.61 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

30.1 |

|

Key countries |

US, Canada, UK, Germany, France, China, India, Japan, Australia, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Generative AI Cybersecurity Market Research and Growth Report?

- CAGR of the Generative AI Cybersecurity industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the generative AI cybersecurity market growth of industry companies

We can help! Our analysts can customize this generative AI cybersecurity market research report to meet your requirements.

RIA -

RIA -