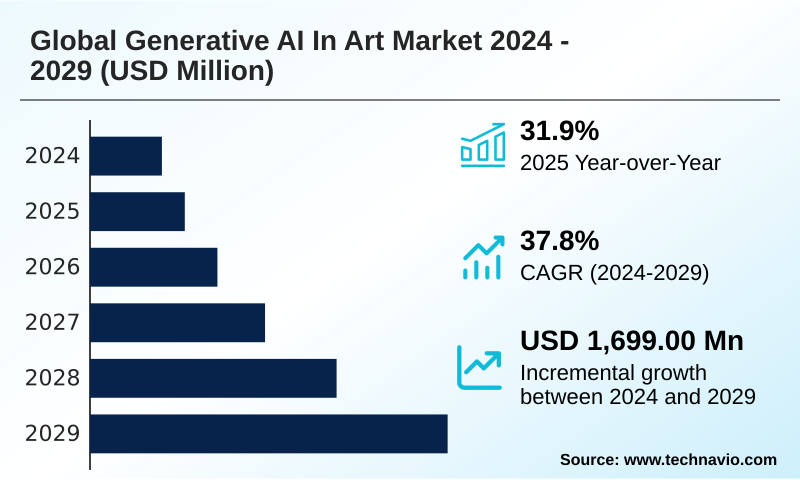

Generative AI In Art Market Size 2025-2029

The generative ai in art market size is valued to increase by USD 1.70 billion, at a CAGR of 37.8% from 2024 to 2029. Democratization of content creation and increased accessibility will drive the generative ai in art market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 33.8% growth during the forecast period.

- CAGR from 2024 to 2029 : 37.8%

Market Summary

- The generative AI in art market is undergoing a period of accelerated growth, transitioning from a niche technological curiosity to a foundational component of modern creative industries. This expansion is driven by continuous advancements in underlying architectures like diffusion models and generative pre-trained transformers, which now yield results with exceptional photorealism and stylistic coherence.

- This technical maturation enables the democratization of creativity, empowering a vast new user base to produce high-quality AI-generated visuals and engage in digital art creation without traditional artistic skills. The technology's utility is seen in its capacity for creative workflow automation, offering unprecedented speed and iterative potential.

- For example, in advertising, agencies leverage AI-assisted creation for concept art generation, reducing initial ideation timelines by up to 40% compared to traditional methods. This efficiency is reshaping professional workflows.

- A critical market trend is the strategic shift toward commercially safe models and enterprise-grade AI solutions, addressing early-stage intellectual property rights concerns and building the trust necessary for generative AI to become an indispensable tool within established creative pipelines, from visual content creation to automated asset production.

What will be the Size of the Generative AI In Art Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Generative AI In Art Market Segmented?

The generative ai in art industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029.

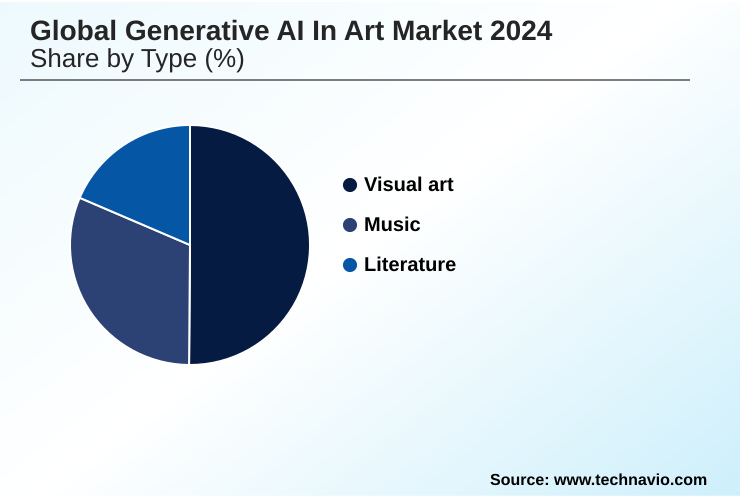

- Type

- Visual art

- Music

- Literature

- Technology

- Cloud-based

- Standalone software

- AI-enabled hardware

- Application

- Advertising and marketing

- Fine art

- Entertainment and gaming

- Design and fashion

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- South Korea

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of World (ROW)

- North America

By Type Insights

The visual art segment is estimated to witness significant growth during the forecast period.

The visual art segment is the most commercially prominent component of the generative AI in art market. It encompasses a wide spectrum of creation, including text-to-video generation and the procedural content generation used in gaming.

The market is fueled by robust demand from end-user industries like advertising, which use AI art generator platforms for rapid creative ideation assistance and the production of automated marketing collateral. These creative AI tools are causing significant creative industry disruption.

For instance, the use of AI-generated visuals as a stock media replacement accelerates campaign development, with some agencies reporting a 25% reduction in asset procurement time.

This evolution from simple image synthesis to sophisticated concept art generation is reshaping professional workflows, though it also intensifies the debate around intellectual property rights and the value of human creation.

Regional Analysis

APAC is estimated to contribute 33.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Generative AI In Art Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the generative AI in art market is defined by distinct regional dynamics. North America leads in foundational research and investment, with an adoption rate in creative agencies approximately 15% higher than in other regions.

This is driven by demand for deep learning art and automated asset production.

APAC is the fastest-growing region, contributing over 30% of the market's incremental growth, fueled by a massive mobile-first user base utilizing creator economy tools for visual content creation.

Europe distinguishes itself with a focus on ethical AI development and a pioneering regulatory stance, which heavily influences data privacy in AI. This region is also a hub for digital content monetization through applications like non-fungible token art.

Across all regions, tools for artistic style replication and design prototyping acceleration are becoming critical for professional adoption.

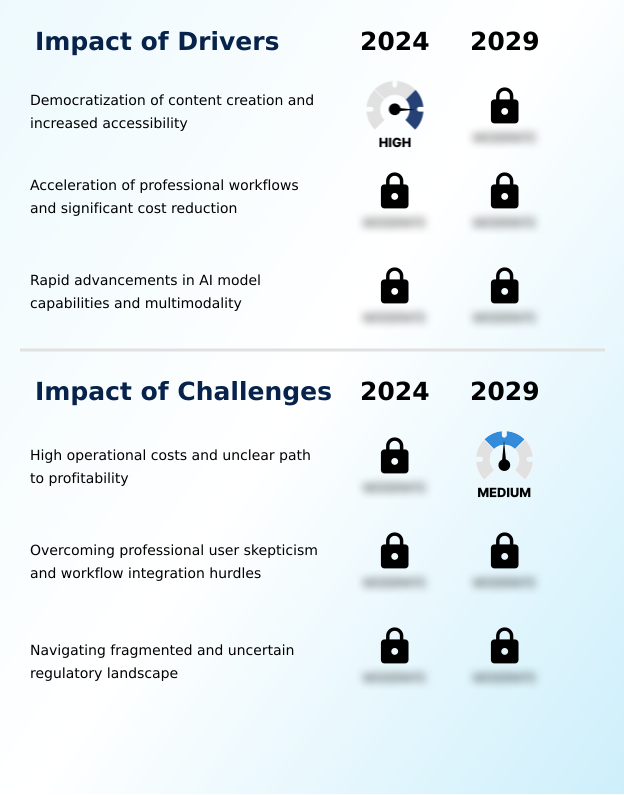

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the generative AI in art market reflects a clear trajectory from novel experimentation to deep operational integration. The initial impact of AI on creative workflows was one of speed, but the focus has now shifted to addressing complex challenges.

- The ethics of using copyrighted art for training remains a central legal battle, directly influencing the development of commercially safe AI-generated assets. Businesses are actively using generative AI for marketing content, yet they struggle with achieving brand consistency with AI, a challenge that specialized models aim to solve.

- The role of generative AI in game development is expanding from simple asset creation to automating 3D asset pipelines with AI. A key technical debate involves comparing on-device vs cloud AI performance, weighing privacy against computational power. This is tied to the legal implications of AI-generated art, which are being shaped by the uncertain regulatory landscape for generative AI.

- For creators, mastering prompt engineering techniques for photorealism has become a critical skill, while the intellectual property of human-AI collaborations remains a gray area. As the future of stock photography with AI looks increasingly disruptive, there are growing concerns over mitigating bias in generative AI outputs.

- For specialized industries, the challenges in generative video consistency are a major hurdle, but new AI tools for independent filmmakers are emerging to address this.

- The generative AI impact on fine art markets and the commercial use of open-source AI models continue to be areas of intense discussion and opportunity, with some platforms seeing user engagement double in a single quarter by offering more refined controls.

What are the key market drivers leading to the rise in the adoption of Generative AI In Art Industry?

- The democratization of content creation, driven by increased accessibility to powerful AI tools, is a primary driver accelerating market expansion and user adoption.

- The profound democratization of creativity is a primary market driver, as diffusion models with intuitive interfaces empower users without technical skills to engage in AI-assisted creation.

- This trend is fueled by the acceleration of professional workflows, where creative workflow automation enables teams to achieve significant efficiency gains. For example, using generative design for rapid brainstorming can reduce initial concepting phases by over 40%.

- The technology is being embedded directly into enterprise software, facilitating professional workflow integration and the use of brand consistency tools. Advances in prompt engineering and model fine-tuning allow for greater control, making user-generated AI content more viable for commercial applications.

- This shift, however, elevates the importance of synthetic media detection and continues to fuel the artistic authorship debate.

What are the market trends shaping the Generative AI In Art Industry?

- The market is witnessing a transformative shift beyond static images. This expansion into multimodality, with a primary focus on video generation, unlocks new commercial applications and creative possibilities.

- A transformative trend is the expansion toward multimodal AI, moving beyond static images to generative video synthesis and 3D model synthesis. This evolution enables significant media production acceleration, with some studios cutting pre-visualization times by up to 50%. The demand for enterprise-grade AI solutions is driving the development of commercially safe models, ensuring legal indemnification for professional use.

- This fosters deeper human-AI collaboration within established pipelines. Concurrently, a push for on-device AI processing is addressing privacy and latency concerns.

- As capabilities like photorealistic rendering and complex inpainting and outpainting become standard, robust content moderation policies are critical for managing outputs and fostering emergent artistic styles in a responsible manner, representing a 30% increase in compliance-related overhead for platform providers.

What challenges does the Generative AI In Art Industry face during its growth?

- Substantial challenges confronting the market include the high operational costs of computation and an often unclear path to sustainable profitability for many service providers.

- The market faces a significant challenge in its intensely resource-heavy economic model, where the computational cost of training generative adversarial networks and performing latent space manipulation creates a precarious path to profitability. Furthermore, professional adoption is hindered by concerns over the homogenization of style from AI-powered design tools.

- Overcoming skepticism requires addressing the copyright infringement concerns tied to the use of art-historical data analysis for training. A fragmented regulatory compliance framework creates operational risks, while the need for algorithmic bias mitigation adds complexity to machine learning for art. These issues of AI ethics in art are paramount.

- For instance, without proper controls, personalized content generation can amplify biases, and anxieties over creative job displacement persist, even as techniques like neural style transfer become more refined.

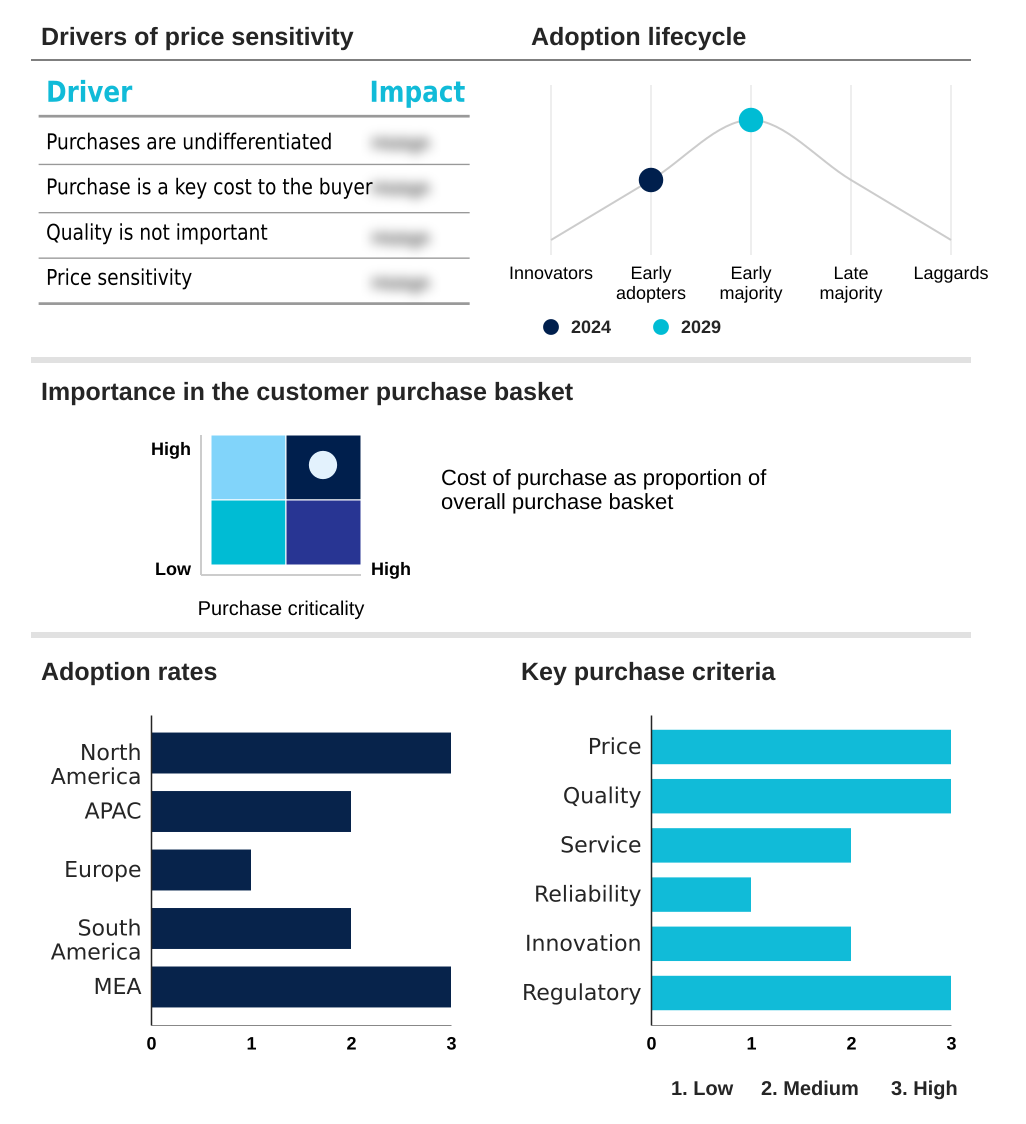

Exclusive Technavio Analysis on Customer Landscape

The generative ai in art market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the generative ai in art market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Generative AI In Art Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, generative ai in art market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adobe Inc. - Offers an integrated suite for text-to-media generation, featuring advanced tools for commercially safe vector, image, and video content creation, enhancing professional creative workflows.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adobe Inc.

- Canva Pty Ltd.

- Craiyon LLC

- DeepAI

- Freepik Co. S.L

- Getty Images Holdings Inc.

- Google LLC

- Jasper AI Inc.

- Kling AI

- Lets Enhance Inc.

- Luma AI

- Midjourney

- Morphogen

- NVIDIA Corp.

- OpenAI

- Pika

- RECRAFT INC.

- REFIK ANADOL STUDIO LLC

- Runway AI Inc.

- Stability AI

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Generative ai in art market

- In September 2024, Adobe Inc. announced a strategic partnership with a leading 3D software company to integrate its Firefly generative AI capabilities directly into 3D modeling and animation workflows.

- In November 2024, Stability AI secured over USD 500 million in a new funding round led by top-tier venture capitalists to accelerate the development of its open-source generative video and audio models.

- In March 2025, the European Union announced the full enforcement of the AI Act's transparency obligations for general-purpose AI models, requiring providers to disclose detailed summaries of their training data.

- In May 2025, Google LLC demonstrated a new generative model capable of creating interactive, real-time 3D environments from text prompts, signaling a major advancement for gaming and simulation applications.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Generative AI In Art Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 284 |

| Base year | 2024 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 37.8% |

| Market growth 2025-2029 | USD 1699.0 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 31.9% |

| Key countries | US, Canada, Mexico, China, Japan, South Korea, India, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, South Africa, Saudi Arabia, UAE, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The generative AI in art market is defined by rapid innovation in text-to-image synthesis, driven by advanced diffusion models and generative adversarial networks. Core technologies enabling this evolution include multimodal AI, which facilitates text-to-video generation and 3D model synthesis, pushing beyond static AI-generated visuals.

- For professionals, creative AI tools that offer sophisticated prompt engineering, style transfer, and latent space manipulation are critical for creative workflow automation. The application of generative design and neural style transfer is becoming central to digital art creation and concept art generation.

- A key boardroom consideration is the adoption of commercially safe models, essential for ethical AI development and mitigating legal risks in automated asset production. Companies integrating these AI-powered design systems report a 20% increase in production speed. The technology, spanning from procedural content generation to photorealistic rendering, relies on model fine-tuning and techniques like inpainting and outpainting.

- This field of computational creativity, powered by machine learning for art and generative pre-trained transformers, is fundamentally reshaping AI-assisted creation, with generative video synthesis being the next major frontier in visual content creation. The proliferation of the AI art generator demonstrates how algorithm-driven art is becoming mainstream.

What are the Key Data Covered in this Generative AI In Art Market Research and Growth Report?

-

What is the expected growth of the Generative AI In Art Market between 2025 and 2029?

-

USD 1.70 billion, at a CAGR of 37.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Visual art, Music, Literature), Technology (Cloud-based, Standalone software, AI-enabled hardware), Application (Advertising and marketing, Fine art, Entertainment and gaming, Design and fashion) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Democratization of content creation and increased accessibility, High operational costs and unclear path to profitability

-

-

Who are the major players in the Generative AI In Art Market?

-

Adobe Inc., Canva Pty Ltd., Craiyon LLC, DeepAI, Freepik Co. S.L, Getty Images Holdings Inc., Google LLC, Jasper AI Inc., Kling AI, Lets Enhance Inc., Luma AI, Midjourney, Morphogen, NVIDIA Corp., OpenAI, Pika, RECRAFT INC., REFIK ANADOL STUDIO LLC, Runway AI Inc. and Stability AI

-

Market Research Insights

- The market is undergoing creative industry disruption, driven by the profound democratization of creativity and the rise of the creator economy tools. This shift facilitates human-AI collaboration and design prototyping acceleration, with early adopters reporting workflow efficiencies improved by over 30%. The integration of enterprise-grade AI solutions allows for professional workflow integration and helps maintain brand consistency tools.

- However, this progress is shadowed by significant copyright infringement concerns and broader questions of AI ethics in art, prompting a robust artistic authorship debate. The technology serves as a potent stock media replacement, enabling personalized content generation and media production acceleration.

- A key challenge is navigating the emerging regulatory compliance framework, data privacy in AI, and the need for effective content moderation policies to manage user-generated AI content. Addressing algorithmic bias mitigation and synthetic media detection is critical, with compliant systems demonstrating a 15% lower risk profile.

- The potential for creative job displacement and the need for digital content monetization solutions like non-fungible token art are also central to the market's evolution, alongside the push for on-device AI processing. This is all supported by creative ideation assistance and new visual communication tools.

We can help! Our analysts can customize this generative ai in art market research report to meet your requirements.

RIA -

RIA -