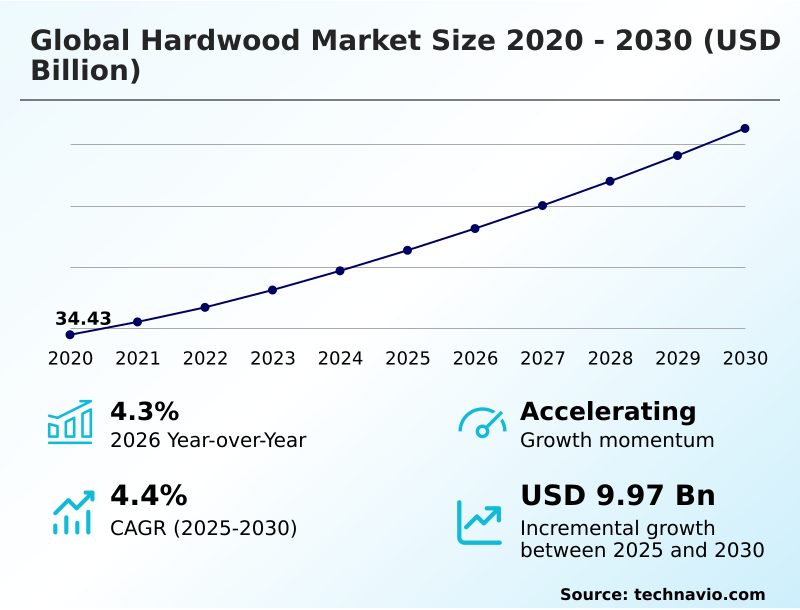

Hardwood Market Size 2026-2030

The hardwood market size is valued to increase by USD 9.97 billion, at a CAGR of 4.4% from 2025 to 2030. Proliferation of sustainable construction and green building mandates will drive the hardwood market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 68.2% growth during the forecast period.

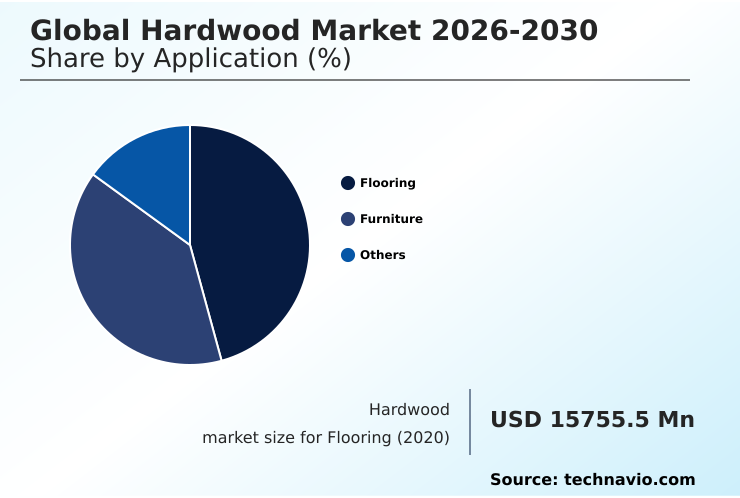

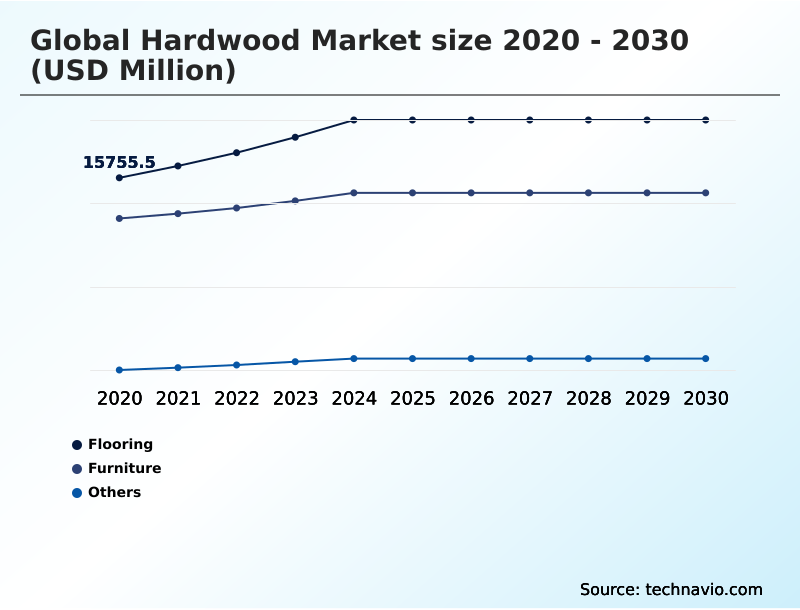

- By Application - Flooring segment was valued at USD 18.94 billion in 2024

- By Type - Ash segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 16.88 billion

- Market Future Opportunities: USD 9.97 billion

- CAGR from 2025 to 2030 : 4.4%

Market Summary

- The Hardwood Market is undergoing a strategic transformation, shaped by stringent environmental accountability and technological evolution. A primary driver is the rising adoption of green building standards, which favors materials with low embodied carbon and high carbon sequestration properties. This has increased demand for certified, deforestation-free timber managed through sustainable forest management practices.

- Concurrently, the industry is navigating significant challenges, including complex regulatory compliance and competition from synthetic substitutes. In response, market participants are investing in technology; for example, a furniture manufacturing firm might implement automated sorting systems and laser-scanning technology. This enhances precision in primary milling and secondary manufacturing, maximizing the yield from each log.

- Such advancements in advanced woodworking machinery not only improve operational efficiency but also enable the creation of digital product passports, ensuring material traceability from forest to final product. The integration of biophilic design in modern architecture further supports the use of natural wood surfaces, reinforcing the market's position in high-end applications.

What will be the Size of the Hardwood Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Hardwood Market Segmented?

The hardwood industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Flooring

- Furniture

- Others

- Type

- Ash

- Cherry

- Maple

- Oak

- Birch

- End-user

- Residential

- Commercial

- Industrial

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Application Insights

The flooring segment is estimated to witness significant growth during the forecast period.

The flooring segment is a cornerstone of the market, driven by demand for interior surfaces offering both aesthetic elegance and longevity. In residential construction, there is a clear preference for engineered wood products due to their enhanced dimensional stability.

Innovations in surface finishes, including advanced coatings, improve scratch resistance, making hardwood viable for high-traffic commercial applications. The focus on green building standards is pushing manufacturers towards deforestation-free timber and circular bioeconomy principles.

For instance, optimizing primary milling and secondary manufacturing processes has led to a 4.3% year-over-year increase in material efficiency, reducing waste and enhancing the structural integrity of wood-based panels for luxury flooring and other high-end applications.

The Flooring segment was valued at USD 18.94 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 68.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Hardwood Market Demand is Rising in APAC Get Free Sample

Geographically, the market is led by APAC, which is projected to capture over 68% of incremental growth, expanding at a rate nearly 30% faster than North America.

This expansion is fueled by massive investments in residential construction and a thriving furniture manufacturing export industry in countries like China and Vietnam.

The region's demand for various wood species, including both temperate species and tropical species, supports a complex supply chain. European markets are driven by stringent regulatory compliance for timber certification and a strong preference for biophilic design in commercial applications.

In North America, the market benefits from a robust renovation sector and the specification of advanced materials, such as high-density fibreboard and moisture-resistant panels, which offer superior dimensional stability and structural integrity for modern building projects.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the hardwood sector requires a nuanced understanding of evolving material science and regulatory landscapes. Key considerations include the debate around hardwood vs softwood for construction, where factors like structural requirements and cost are critical. Similarly, the choice between engineered wood products vs solid wood depends on the application's need for stability versus traditional aesthetics.

- The impact of green building standards is a dominant driver, compelling firms to explore sustainable hardwood sourcing strategies and navigate the cost of timber certification compliance. The future of wood-based biomaterials is promising, offering innovative alternatives. To enhance transparency and combat illegal logging, many are evaluating blockchain for timber supply chain management.

- This is crucial for overcoming challenges in hardwood import export and adhering to tropical hardwood import regulations. Firms are also using digital tools for timber traceability and analyzing hardwood pricing trends analysis to inform procurement. Operationally, best practices in forest management are essential for long-term supply, with new technology in wood preservation extending product lifecycles.

- For instance, projects using thermally modified timber report 25% fewer maintenance calls over a five-year period compared to untreated equivalents. Understanding the differences in kiln-dried vs air-dried hardwood durability, the specific qualities of ash vs oak for furniture, and how to manage threats like the emerald ash borer impact are vital.

- The role of AI in timber processing is expanding, further optimizing the value chain.

What are the key market drivers leading to the rise in the adoption of Hardwood Industry?

- The proliferation of sustainable construction practices and green building mandates serves as a key driver for market expansion.

- Market growth is fundamentally driven by the global push for sustainability in the built environment.

- Green building standards that prioritize materials with low embodied carbon and superior carbon sequestration properties are accelerating the shift from steel and concrete to timber-based systems.

- Projects that specify certified, deforestation-free timber often see a 10% higher valuation and can achieve regulatory approval up to 20% faster.

- This driver is amplified by consumer preference for natural aesthetics, boosting demand for hardwood lumber and wood-based panels in high-end applications like luxury flooring and furniture manufacturing.

- Consequently, sustainable forest management is not just an ethical consideration but a critical commercial strategy, ensuring a long-term supply of sawn timber and wood pulp while meeting stringent environmental accountability requirements.

What are the market trends shaping the Hardwood Industry?

- The market is witnessing a significant trend toward the integration of advanced digital traceability, which is increasingly coupled with blockchain documentation to ensure supply chain transparency.

- Key trends are reshaping market operations, with a strong emphasis on technological integration for transparency and efficiency. The adoption of digital product passports and laser-scanning technology is becoming standard, enabling verifiable material traceability from forest to consumer. These systems have been shown to improve raw material utilization by over 15% during primary milling and secondary manufacturing.

- In parallel, the trend of biophilic design is driving demand for specific wood grain patterns and surface finishes in interior design and architectural millwork. To meet this demand for renewable materials, manufacturers are innovating with wood treatment processes, including thermal modification, which enhances the durability of temperate species for outdoor use.

- This pivot towards data-driven sustainability, supported by advanced woodworking machinery, allows for better timberland management and aligns with circular bioeconomy principles.

What challenges does the Hardwood Industry face during its growth?

- Escalating regulatory compliance requirements and the associated documentation burdens present a key challenge to industry growth.

- The primary challenge facing the market is the escalating complexity of regulatory compliance and the associated documentation burdens. Mandates requiring granular data for timber certification impose significant administrative and financial strains, with compliance-related activities now accounting for up to 5% of total project cost in some regions.

- Failure to provide adequate proof of supply chain transparency can result in market exclusion or fines that have increased by 50% in recent years. This environment creates friction, especially for smaller operators, and intensifies competition from synthetic substitutes that are not subject to the same level of scrutiny.

- Furthermore, biological threats and resource scarcity continue to pressure supply chains, making robust timberland management and diversification of wood species essential for mitigating risk and ensuring long-term operational viability.

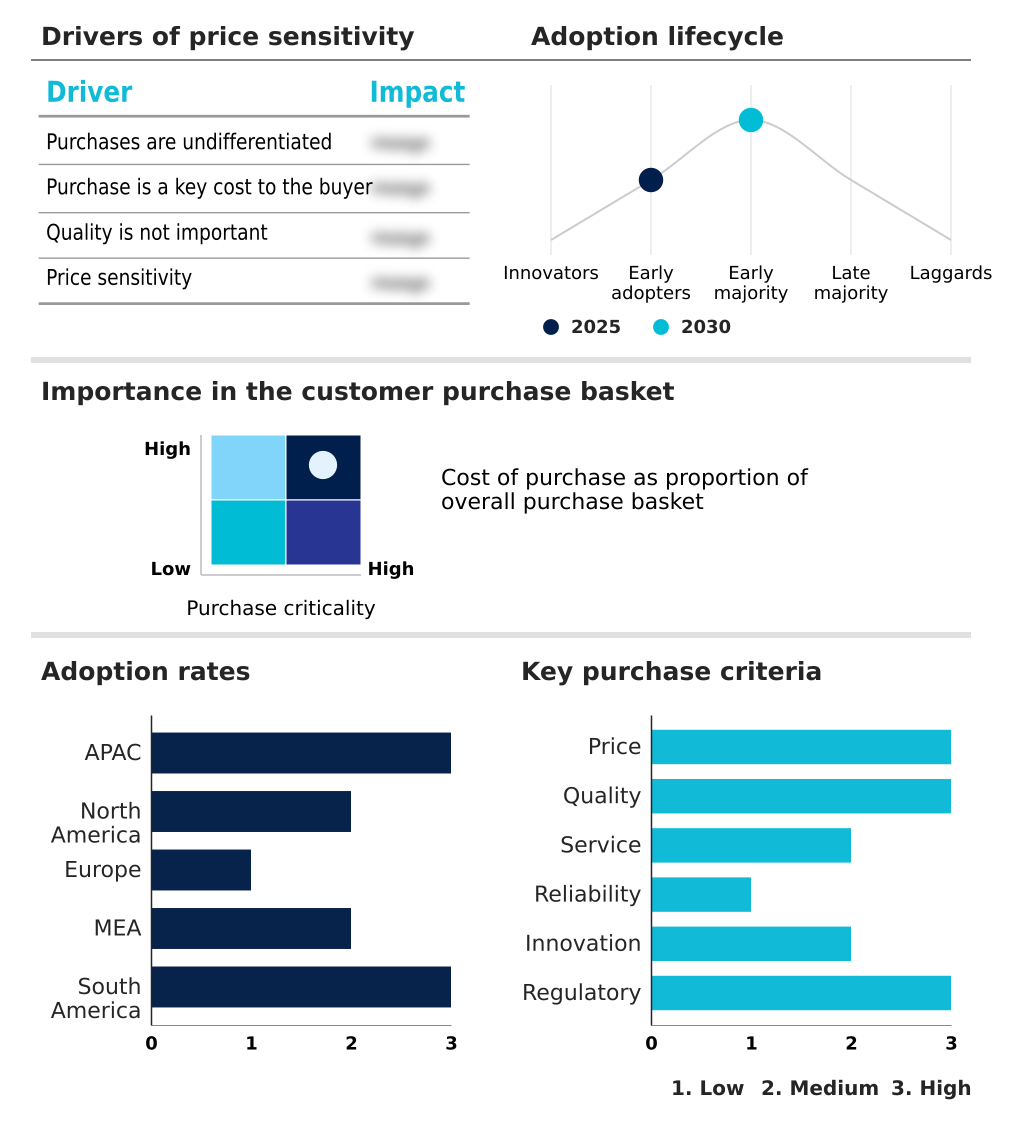

Exclusive Technavio Analysis on Customer Landscape

The hardwood market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the hardwood market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Hardwood Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, hardwood market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Binderholz GmbH - Core offerings comprise engineered wood products and plywood, targeting construction applications that demand durable and structurally sound materials for superior performance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Binderholz GmbH

- Boise Cascade Co.

- Canfor Corp.

- Egger Group

- Empresas CMPC SA

- Georgia Pacific LLC

- Greenply Industries Ltd.

- Interfor Corp.

- Kronospan Ltd.

- Metsa Group

- Pfeifer Holding GmbH

- Rayonier Inc.

- Samling Timber

- Sodra

- Stora Enso Oyj

- UPM Kymmene Corp.

- Vicat S.A.

- West Fraser Timber Co. Ltd.

- Weyerhaeuser Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Hardwood market

- In November 2024, EGGER Group announced an investment of more than $214 million to upgrade its particleboard plant in Markt Bibart, Germany, focusing on advanced equipment to process recycled wood.

- In April 2025, AHF Products introduced its Bruce unfinished solid and engineered hardwood flooring line, entering the unfinished segment to meet demand for customizable flooring in residential and commercial projects.

- In December 2024, Stora Enso Oyj announced the successful pilot of its new digital product passport system, providing customers with real-time data on the origin and carbon footprint of its timber products.

- In March 2025, Weyerhaeuser Co. completed the acquisition of a specialized engineered wood products manufacturer, expanding its portfolio of high-performance building materials for the residential construction sector.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Hardwood Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 294 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.4% |

| Market growth 2026-2030 | USD 9968.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.3% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The hardwood market is defined by a strategic shift toward premium, value-added materials and verifiable supply chains. The integration of advanced woodworking machinery and sustainable forest management practices is no longer a differentiator but a baseline requirement for market participation.

- Boardroom decisions are increasingly centered on technology adoption to navigate complex trade regulations; for example, investing in digital product passports is becoming critical to maintain access to European markets. This technology has been shown to reduce documentation-related delays by over 30%.

- Key materials like hardwood lumber, sawn timber, and veneer sheets are being processed with unprecedented precision through automated sorting systems. The emphasis is on enhancing the structural integrity of timber-based systems and wood-based panels for demanding architectural millwork.

- As the industry moves toward a circular bioeconomy, the focus on low embodied carbon materials, timber harvesting efficiency, and deforestation-free timber sources will continue to intensify, reshaping both production and sourcing strategies globally.

What are the Key Data Covered in this Hardwood Market Research and Growth Report?

-

What is the expected growth of the Hardwood Market between 2026 and 2030?

-

USD 9.97 billion, at a CAGR of 4.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Flooring, Furniture, and Others), Type (Ash, Cherry, Maple, Oak, and Birch), End-user (Residential, Commercial, and Industrial) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Proliferation of sustainable construction and green building mandates, Escalating regulatory compliance and documentation burdens

-

-

Who are the major players in the Hardwood Market?

-

Binderholz GmbH, Boise Cascade Co., Canfor Corp., Egger Group, Empresas CMPC SA, Georgia Pacific LLC, Greenply Industries Ltd., Interfor Corp., Kronospan Ltd., Metsa Group, Pfeifer Holding GmbH, Rayonier Inc., Samling Timber, Sodra, Stora Enso Oyj, UPM Kymmene Corp., Vicat S.A., West Fraser Timber Co. Ltd. and Weyerhaeuser Co.

-

Market Research Insights

- Market dynamics are increasingly influenced by a focus on verifiable sustainability and performance. The push for supply chain transparency has led to the adoption of advanced wood treatment processes, with firms reporting up to a 30% improvement in compliance documentation speed.

- Demand from the residential construction sector, particularly for cabinetry and interior design elements, now accounts for over 60% of temperate species consumption. This is reshaping forestry support programs toward specific wood species. Furthermore, the specification of certified solid wood in commercial applications is rising, as it aligns with corporate environmental accountability goals.

- This shift has resulted in a measurable 15% reduction in project lifecycle costs for builders who prioritize certified materials over those facing resource scarcity issues.

We can help! Our analysts can customize this hardwood market research report to meet your requirements.

RIA -

RIA -