Headlight Control Module Market Size 2024-2028

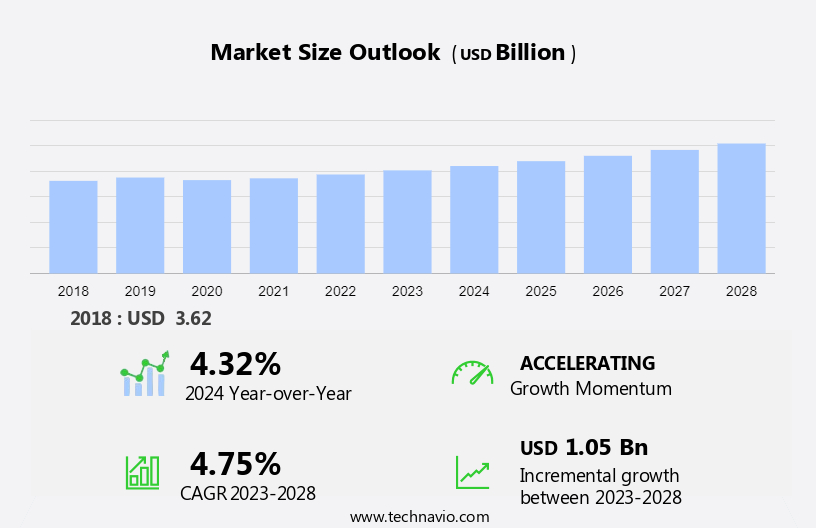

The headlight control module market size is forecast to increase by USD 1.05 billion at a CAGR of 4.75% between 2023 and 2028. The market is witnessing significant growth due to the incorporation of energy-efficient solutions in automobiles. With the increasing focus on reducing carbon emissions and improving fuel efficiency, automakers are investing heavily in advanced headlight technologies. This trend is driving the market for headlight control modules, which enable the efficient management of headlight systems. Additionally, the rise in Research and Development (R&D) spending on headlight technology is fueling innovation, leading to the development of advanced features such as adaptive headlights and matrix lighting. However, the market faces challenges, including the shortage of semiconductors used in manufacturing headlight control modules. This scarcity is causing supply chain disruptions and increasing costs for manufacturers. Despite these challenges, the market is expected to continue its growth trajectory, driven by the demand for energy-efficient and advanced headlight systems in automobiles.

Market Analysis

The headlight control module market is witnessing significant growth due to the increasing demand for advanced lighting systems in premium vehicles. LED headlights are becoming increasingly popular due to their aesthetically appealing looks and energy efficiency. Headlight control modules are essential electronic devices that manage the intensity, direction, and beam patterns of headlights to ensure compliance with lighting standards and enhance road safety. These modules are crucial for adaptive headlights, which adjust the beam pattern based on vehicle speed, steering angle, and surrounding environment. The passenger vehicle segment, including SUVs and luxury vehicles, is the major contributor to the Headlight Control Modules market.

Moreover, the market is driven by the growing preference for energy-efficient lighting technology and the increasing demand for advanced safety features in vehicles. The market is segmented based on lighting type, vehicle type, and region. Halogen and LED are the two primary lighting types, with LED gaining popularity due to its energy efficiency and longer lifespan. The market is expected to grow at a steady pace in the coming years, driven by the increasing demand for adaptive headlights and the growing popularity of premium vehicles. The market is expected to be a significant contributor to the automotive industry, providing advanced lighting solutions that enhance safety and improve the driving experience. The market is expected to grow at a CAGR of over 7% during the forecast period, driven by the increasing demand for energy-efficient lighting technology and the growing popularity of premium vehicles.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Technology

- LED

- Halogen

- Xenon

- Vehicle Type

- Passenger car

- Light commercial vehicle

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Europe

- Germany

- South America

- Middle East and Africa

- APAC

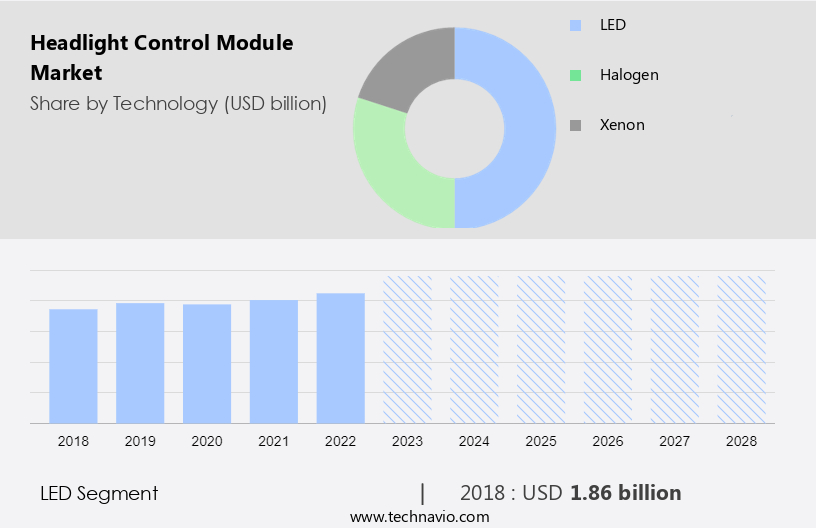

By Technology Insights

The LED segment is estimated to witness significant growth during the forecast period.LED headlights have gained significant popularity in the premium vehicle segment due to their energy-efficient and aesthetically appealing features. Compared to traditional halogen headlights, LEDs offer several advantages, including lower power consumption, reduced environmental impact, and a brighter, more focused light beam. LED headlights enable automotive manufacturers to design innovative lighting configurations, enhancing the looks of both the vehicles and consumer appeal. Headlight control modules, an essential component of LED headlights, offer precise control of individual LED elements, facilitating advanced lighting features such as adaptive headlights, automatic high beams, and dynamic lighting patterns. With predictive lighting accuracy and advanced lighting systems like automatic emergency braking, adaptive cruise control, and lane keep assist, LEDs contribute significantly to road safety.

Moreover, the LED segment in the automotive lighting market is experiencing high production and sales, driven by the increasing sales of automobiles, passenger vehicles, SUVs, and premium car sales. The durability and long lifespan of LEDs translate to lower maintenance costs and a more sustainable lighting solution for consumers.

Get a glance at the market share of various segments Request Free Sample

The LED segment was valued at USD 1.86 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

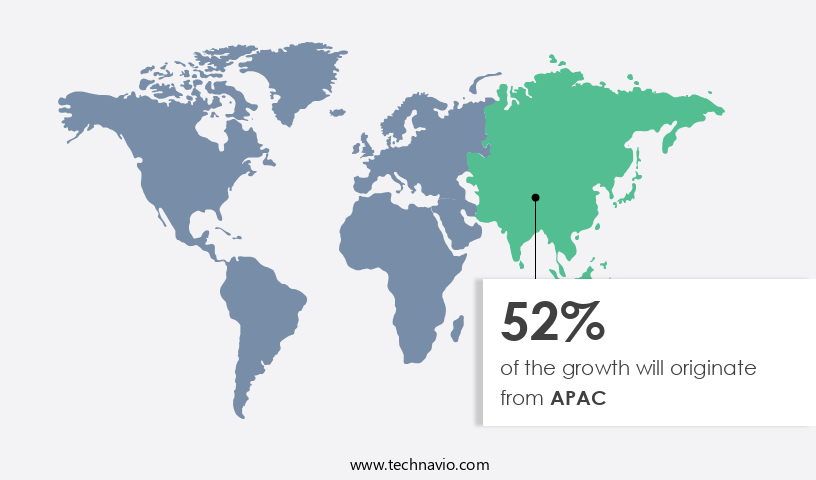

APAC is estimated to contribute 52% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The market in APAC is experiencing significant growth due to the region's high economic expansion, driven primarily by China's consumption-driven economy. The increasing population and strong economic growth in China will continue to fuel market expansion. China is also a manufacturing hub for international OEMs and headlight suppliers, making it a significant contributor to The market. APAC is home to several high-volume vehicle markets, including India and China, as well as developed countries such as Japan and South Korea. The adoption of advanced lighting technologies, such as Human-centric lighting technologies, Matrix LED headlights, and High Beam Assist, is increasing in passenger cars, SUVs, luxury vehicles, commercial vehicles, and heavy commercial vehicles.

Moreover, vehicle connectivity and V2X systems are also driving the demand for software-defined lighting solutions. Key players in the market include Halogen, LED, and Xenon lighting technology providers. The market is witnessing a shift towards advanced lighting technologies, such as LED and Matrix LED headlights, due to their superior road visibility and energy efficiency. The adoption of these technologies is also increasing in semi-autonomous and autonomous vehicles to enhance safety and improve the driving experience. Overall, the market in APAC is expected to continue its dominance in the global market due to the high volume of vehicle production and adoption of advanced lighting technologies.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

The incorporation of energy-efficient solutions in automobiles is the key driver of the market. Governments worldwide are encouraging the production and adoption of energy-efficient vehicles to minimize emissions and fuel consumption. Automotive Original Equipment Manufacturers (OEMs) are integrating energy-saving technologies into their vehicles in response. Headlight control modules, specifically those using LED technology, contribute significantly to this trend. LED headlights offer substantial energy savings compared to conventional halogen or xenon lighting systems. They consume less power, leading to lower fuel consumption and reduced CO2 emissions throughout a vehicle's lifecycle. In the premium passenger vehicle segment, LED headlights are increasingly popular due to their adaptive features, aesthetically appealing looks, and advanced lighting systems such as automatic high beams.

Moreover, these features enhance road safety by providing better illumination and adaptability to various traffic conditions. The adoption of LED headlights is not limited to passenger vehicles; the sales of SUVs and premium cars are also experiencing due to their advanced lighting technology. Advanced lighting systems, including predictive lighting accuracy, automatic emergency braking, adaptive cruise control, lane keep assist, and matrix LEDs, are becoming standard features in modern vehicles. These systems utilize adaptive driving beams to optimize lighting intensity and direction based on traffic, oncoming traffic in opposite directions, and lighting standards. As a result, the LED segment of the automotive lighting market is expected to grow at a high rate in the coming years.

Market Trends

An increase in R and D spending on headlight technology is the upcoming trend in the market. The automotive lighting market has seen significant advancements since the introduction of incandescent lights, with LED headlights becoming increasingly popular in both passenger vehicles and SUVs. Premium vehicle manufacturers, such as Audi and BMW, have utilized headlight control modules to incorporate adaptive features, including automatic high beams and adaptive driving beams, into their models. These advanced lighting systems not only provide aesthetically appealing looks but also enhance safety on highways by adjusting beam patterns based on traffic conditions, oncoming traffic from opposite directions, and lighting standards. R&D investments have been crucial in advancing automotive headlight technology, leading to innovations like matrix LEDs and predictive lighting accuracy.

However, these advanced lighting systems work in conjunction with other automotive electronic devices, such as automatic emergency braking, adaptive cruise control, and lane keep assist, to improve overall vehicle safety. The high production and sales of vehicles, particularly in the premium car segment, have driven the demand for these advanced lighting systems, making them an essential component of modern automobiles.

Market Challenge

Shortage of semiconductors used in the manufacturing of headlight control modules is a key challenge affecting the market growth. The market is experiencing a substantial challenge due to the ongoing semiconductor shortage. This scarcity of essential chips utilized in various headlight control module functions is affecting the market in several ways. Automakers globally are compelled to reduce production as a result of the chip deficiency, leading to fewer vehicles being sold. This translates to lost revenue and potential customers for headlight control module manufacturers. In 2021, approximately 10-11 million vehicles were cut from production worldwide due to the semiconductor shortage. The semiconductor crisis, which emerged in Europe in December 2020, caused production disruptions across various industries, including automotive.

However, advanced lighting systems, such as LED headlights with adaptive features, are increasingly popular in premium vehicles, passenger vehicles, and even SUVs. These lighting solutions offer aesthetically appealing looks, energy efficiency, and adaptive capabilities, including automatic high beam, adaptive driving beams, and predictive lighting accuracy. The LED segment of the automotive lighting market is expected to grow significantly due to consumer adoption and the high sales of automobiles. Additionally, advanced safety features, such as automatic emergency braking, adaptive cruise control, and lane keep assist, rely on electronic devices and lighting standards. Ensuring road safety is a top priority, and lighting type and vehicle type are crucial factors in the development and implementation of automotive headlight technology.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

BEEKAY AUTOMOTIVES - The company offers headlight control modules, including gas spring cars, headlight assemblies, LED cabin lights, tail lamps, side indicator assemblies, side indicator assemblies tata 407, fog lamps, and 142mm lamps.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ams OSRAM AG

- Continental AG

- DENSO Corp.

- HELLA GmbH and Co. KGaA

- Hyundai Motor Co.

- Lear Corp.

- Marelli Holdings Co. Ltd.

- Motorlamp Auto Electricals Private Limited

- NXP Semiconductors NV

- Renesas Electronics Corp.

- UNIQUE AUTO SPARES

- Valeo SA

- ZKW Group GmbH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Headlight control modules have become an essential component in modern automotive lighting systems, enhancing both functionality and aesthetics in premium vehicles. These modules enable adaptive features like automatic high beams and adaptive headlights, catering to various driving conditions and traffic scenarios. LED headlights, a significant part of headlight control modules, offer numerous advantages, including energy efficiency and long-lasting performance. The premium vehicle segment is witnessing high production and sales due to the growing consumer adoption of these advanced lighting systems. Adaptive headlights adjust their beam patterns and intensity based on driving conditions, such as highways and traffic.

Moreover, they also respond to oncoming traffic and vehicles in the opposite direction, ensuring road safety. Advanced lighting systems, including automatic emergency braking, adaptive cruise control, lane keep assist, and Matrix LEDs, are increasingly being integrated into headlight control modules. The sales of automobiles, particularly passenger vehicles and SUVs, are surging due to the integration of these advanced lighting technologies. The automotive headlight technology market is expected to grow significantly, driven by the increasing demand for energy-efficient, adaptive, and aesthetically appealing headlights. The market growth is also influenced by the evolving lighting standards and the integration of electronic devices into headlight control modules.

Furthermore, in conclusion, headlight control modules are revolutionizing automotive lighting, offering advanced features and enhancing road safety in premium vehicles. The integration of LED technology, adaptive driving beams, and advanced systems like automatic emergency braking, adaptive cruise control, and lane keep assist is driving the growth of the automotive headlight technology market.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

159 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.75% |

|

Market Growth 2024-2028 |

USD 1.05 billion |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

4.32 |

|

Regional analysis |

APAC, North America, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 52% |

|

Key countries |

US, China, Japan, India, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

ams OSRAM AG, BEEKAY AUTOMOTIVES, Continental AG, DENSO Corp., HELLA GmbH and Co. KGaA, Hyundai Motor Co., Lear Corp., Marelli Holdings Co. Ltd., Motorlamp Auto Electricals Private Limited, NXP Semiconductors NV, Renesas Electronics Corp., UNIQUE AUTO SPARES, Valeo SA, and ZKW Group GmbH |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -