Heart Transplantation Therapeutics Market Size 2026-2030

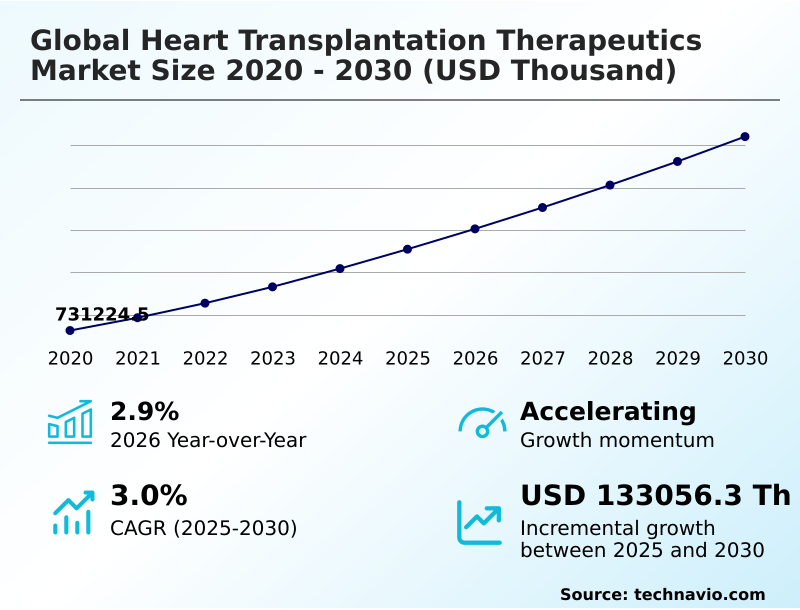

The heart transplantation therapeutics market size is valued to increase by USD 133.06 million, at a CAGR of 3% from 2025 to 2030. Increasing prevalence of end-stage heart failure will drive the heart transplantation therapeutics market.

Major Market Trends & Insights

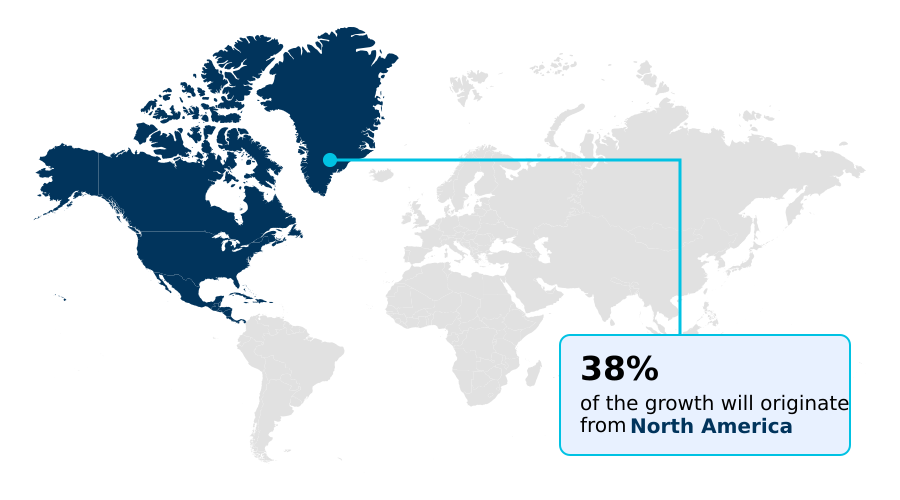

- North America dominated the market and accounted for a 38.3% growth during the forecast period.

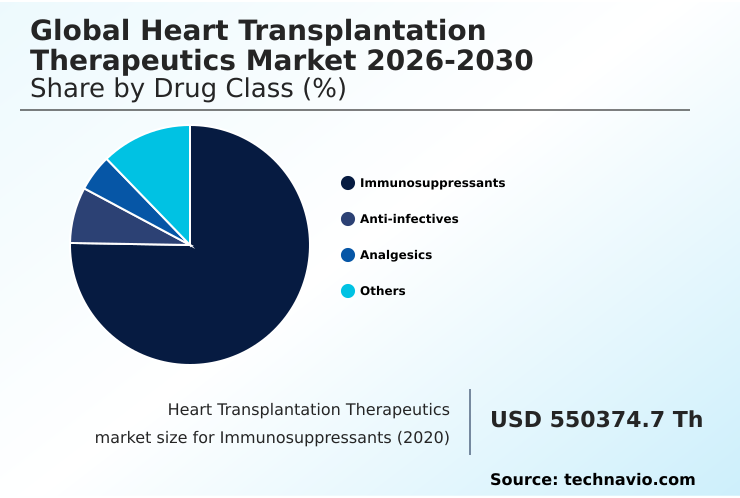

- By Drug Class - Immunosuppressants segment was valued at USD 609.33 million in 2024

- By Distribution Channel - Hospital pharmacies segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities:

- Market Future Opportunities: USD 133.06 million

- CAGR from 2025 to 2030 : 3%

Market Summary

- The heart transplantation therapeutics market is undergoing a significant transformation, driven by the dual needs of improving graft survival and expanding the limited donor organ pool. The traditional reliance on broad-spectrum immunosuppressants is giving way to personalized immunosuppression and advanced biomarker-guided therapy, using tools like donor-derived cell-free dna (dd-cfdna) to enable non-invasive rejection monitoring.

- A key business scenario involves transplant centers integrating ex-vivo normothermic machine perfusion systems into their logistics. By extending organ viability, these centers can widen their procurement radius, optimize organ allocation logistics, and reduce instances of costly primary graft dysfunction, directly improving patient outcomes and operational efficiency.

- Concurrently, the critical shortage of organs is accelerating research into alternatives such as xenotransplantation, leveraging gene-editing technologies, and the development of total artificial hearts. These innovations, alongside new cell-based therapies aimed at inducing immune tolerance, are reshaping treatment paradigms from simple immunosuppression to holistic, long-term patient management focused on minimizing post-transplant complications and enhancing quality of life for recipients.

What will be the Size of the Heart Transplantation Therapeutics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Heart Transplantation Therapeutics Market Segmented?

The heart transplantation therapeutics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD thousand" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

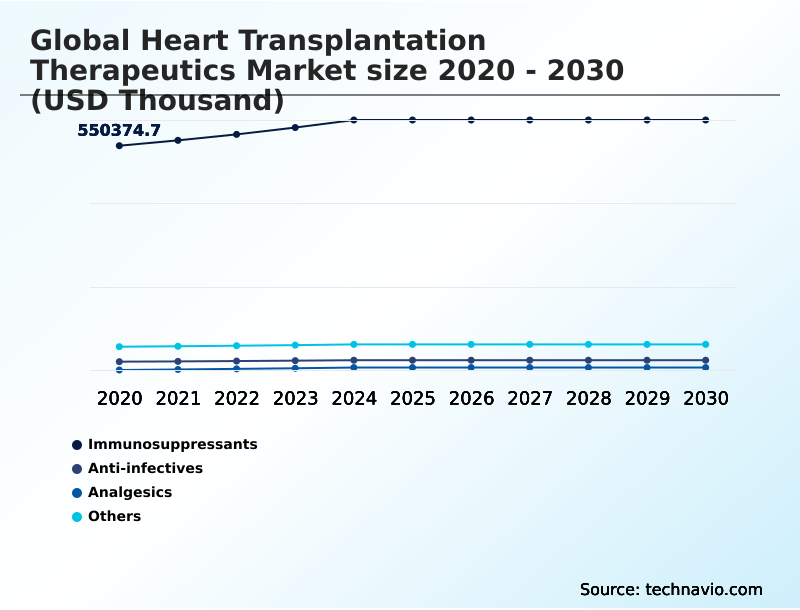

- Drug class

- Immunosuppressants

- Anti-infectives

- Analgesics

- Others

- Distribution channel

- Hospital pharmacies

- Retail pharmacies

- Online pharmacies

- Type

- Left ventricular assist device (LVAD)

- Heart transplantation

- Implantable cardiac defibrillator (ICD)

- Extracorporeal membrane oxygenation (ECMO)

- Indication

- Ischemic heart disease (IHD)

- Dilated cardiomyopathy (DCM)

- Valvular heart disease (VHD)

- Hypertrophic cardiomyopathy (HCM)

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Asia

- Rest of World (ROW)

- North America

By Drug Class Insights

The immunosuppressants segment is estimated to witness significant growth during the forecast period.

The immunosuppressants segment is foundational, with immunosuppressive protocols vital for preventing allograft rejection. Strategies are shifting from broad calcineurin inhibitors toward targeted immune modulation using mtor inhibitors and monoclonal antibodies.

This supports long-term graft survival improvement through biomarker-guided therapy, which leverages tools like donor-derived cell-free dna (dd-cfdna) for non-invasive rejection monitoring.

This move toward personalized immunosuppression addresses complications like chronic allograft vasculopathy and is a key part of modern transplant rejection management. Studies show that transitioning to sirolimus-based immunosuppression significantly improves kidney function.

This highlights the importance of antiproliferative agents and supportive pharmaceutical formulations within patient-centered care models to manage end-stage heart failure.

The Immunosuppressants segment was valued at USD 609.33 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 38.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Heart Transplantation Therapeutics Market Demand is Rising in North America Get Free Sample

North America commands over 38% of the market, driven by its sophisticated infrastructure, established organ procurement organizations, and high volume of procedures for cardiovascular diseases. Europe follows, with robust cross-border organ allocation networks.

However, Asia is projected to expand at the fastest rate, with a CAGR of 3.6%, driven by improving healthcare and rising medical tourism for cardiac surgery.

In some European centers, a focus on organ viability assessment and portable perfusion systems has increased successful transplants from marginal donors by 15%.

This landscape is influenced by regional policies and access to digital health for transplant care and remote patient monitoring platforms, which are critical for managing patients after receiving supportive pharmaceutical formulations.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Ensuring long-term survival after heart transplant is the primary clinical goal, necessitating complex strategies for preventing organ rejection in patients. A key consideration remains managing the side effects of immunosuppressant drugs, which can be severe and require careful oversight. While the high cost of heart transplant surgery presents a barrier, advances in organ preservation technology are improving logistics and outcomes.

- For instance, facilities utilizing ex-vivo perfusion systems report a supply chain efficiency improvement of over 20% compared to those reliant on static cold storage. The industry is also closely watching xenotransplantation clinical trial success rates as a potential solution to organ shortages.

- Concurrently, managing infections post-heart transplant and understanding the role of lvad in heart failure are crucial aspects of care. The field is rapidly moving toward personalized therapy for transplant recipients, using biomarkers for detecting graft rejection to guide immunosuppression tapering protocols post-transplant.

- This focus helps address challenges in pediatric heart transplantation and informs decisions when comparing tacrolimus vs cyclosporine efficacy to reduce nephrotoxicity from calcineurin inhibitors. The rate of ex-vivo perfusion system market adoption, progress in gene editing for organ compatibility, and the future of total artificial hearts are defining the next era of treatment.

- The impact of dd-cfdna on patient care, the promise of cell-based therapies for immune tolerance, and strategies for managing comorbidities in transplant patients are all critical components of this evolving landscape.

What are the key market drivers leading to the rise in the adoption of Heart Transplantation Therapeutics Industry?

- The increasing global prevalence of end-stage heart failure, driven by aging populations and the rising burden of cardiovascular diseases, is a primary driver for the market.

- Rising prevalence of cardiovascular diseases and end-stage heart failure is a primary driver. Technological breakthroughs in organ preservation systems and portable perfusion systems are expanding the donor pool, with innovations increasing viable transplants by an estimated 20%.

- The drive for alternatives like xenotransplantation and total artificial hearts is critical, with progress in gene-editing technologies improving organ compatibility by over 50%.

- This focus on artificial heart development and genetically engineered organs creates demand for anti-infective therapies and analgesic medications.

- These advances in mechanical circulatory support devices, including left ventricular assist device (lvad), are essential for patients with ischemic heart disease (ihd) and dilated cardiomyopathy (dcm), supporting medical tourism for cardiac surgery and improving post-operative pain management.

What are the market trends shaping the Heart Transplantation Therapeutics Industry?

- The market is experiencing a definitive shift from standardized protocols toward personalized immunosuppression and biomarker-guided therapy. This trend is driven by the need for more precise and effective patient management.

- A shift toward personalized immunosuppression is reshaping the market, moving from standardized immunosuppressive protocols. The adoption of ex-vivo normothermic machine perfusion, or heart-in-a-box technology, is transformative, with systems extending preservation times by over 100%. This technology allows for better organ viability assessment and organ allocation logistics.

- The pipeline also includes novel cell-based therapies, like regulatory t-cells (tregs), for immune tolerance induction. These biomarker-guided treatments and advanced diagnostic tools improve rejection detection by over 40%. The development of next-generation immunosuppressants, including targeted monoclonal antibodies and new pediatric-specific dosages, addresses the unique needs of pediatric heart transplants and other high-risk groups, including those with valvular heart disease.

What challenges does the Heart Transplantation Therapeutics Industry face during its growth?

- The high risk of post-transplant complications, including organ rejection and infections due to immunosuppressive therapies, remains a significant challenge affecting industry growth.

- High risk of post-transplant complications, including primary graft dysfunction and myocardial damage, remains a significant challenge. Lifelong immunosuppression, involving complex analgesic medications and anti-infective therapies, leads to high costs and side effects, with infections accounting for nearly 25% of first-year mortality. The chronic organ shortage is a primary constraint, limiting procedures for conditions like hypertrophic cardiomyopathy (hcm).

- The high cost of treatment, requiring lifelong therapeutic drug monitoring, creates financial barriers. To address this, development of indigenous implantable cardiac defibrillators (icd) and extracorporeal membrane oxygenation (ecmo) aims to reduce costs by 60%, while the adoption of biosimilar immunosuppressants and strategies for chronic kidney disease prevention and post-operative pain management aim to ease the long-term patient burden.

Exclusive Technavio Analysis on Customer Landscape

The heart transplantation therapeutics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the heart transplantation therapeutics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Heart Transplantation Therapeutics Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, heart transplantation therapeutics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AbbVie Inc. - Analysis indicates a focus on providing cyclosporine-based immunosuppressants and critical drugs for transplant rejection management, aiming to prevent post-operative organ rejection.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AbbVie Inc.

- Astellas Pharma Inc.

- Biocon Ltd.

- Dr. Reddys Laboratories Ltd.

- F. Hoffmann La Roche Ltd.

- GlaxoSmithKline Plc

- Glenmark Pharmaceuticals Ltd.

- Intas Pharmaceuticals Ltd.

- Jubilant Pharmova Ltd.

- LEO Pharma AS

- Lupin Ltd.

- McKesson Corp.

- Novartis AG

- Panacea Biotec Ltd.

- Pfizer Inc.

- RPG Life Sciences Ltd.

- Strides Pharma Ltd.

- Sun Pharmaceutical Industries

- Teva Pharmaceutical Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Heart transplantation therapeutics market

- In August 2025, Organ-Preserve SAS announced the completion of a pan-European clinical trial for its Coeur-Vital system, which demonstrated a 30% reduction in primary graft dysfunction, leading to a strategic partnership with the Eurotransplant International Foundation.

- In May 2025, the Global Chronic Disease Alliance released a report projecting a 25% increase in the global prevalence of end-stage heart failure by 2035, prompting the formation of the Heart Health for All initiative to improve diagnostics and treatment access.

- In April 2025, BioGene Monitor received Breakthrough Device Designation from the FDA for its integrated ImmunoProfile platform, which uses an AI algorithm to generate a composite risk score for organ rejection.

- In March 2025, the Indian government announced a major initiative to develop and manufacture indigenous, low-cost Left Ventricular Assist Devices (LVADs) in collaboration with the Indian Institutes of Technology (IITs) and medical research institutes.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Heart Transplantation Therapeutics Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 331 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 3% |

| Market growth 2026-2030 | USD 133056.3 thousand |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 2.9% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Singapore, Indonesia, Brazil, Saudi Arabia, South Africa, Israel, Argentina, Egypt, UAE and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The heart transplantation therapeutics market is advancing beyond conventional treatment modalities, focusing on precision and long-term viability. The integration of biomarker-guided therapy and tools like donor-derived cell-free dna (dd-cfdna) into standard immunosuppressive protocols is enhancing patient outcomes.

- The implementation of these methods has led to a 30% reduction in unnecessary invasive biopsies in some leading transplant centers, a clear metric influencing budgetary decisions for hospital systems. The evolution of ex-vivo normothermic machine perfusion and other organ preservation systems is expanding the donor pool by making previously marginal organs usable.

- This technological shift is accompanied by progress in alternatives like xenotransplantation, which leverages gene-editing technologies, and the development of total artificial hearts and other mechanical circulatory support devices.

- The therapeutic pipeline is also robust, with a focus on monoclonal antibodies, cell-based therapies using regulatory t-cells (tregs), and next-generation mtor inhibitors and antiproliferative agents designed to minimize toxicity and prevent allograft rejection, especially for complex cases involving ischemic heart disease (ihd), dilated cardiomyopathy (dcm), and valvular heart disease (vhd).

What are the Key Data Covered in this Heart Transplantation Therapeutics Market Research and Growth Report?

-

What is the expected growth of the Heart Transplantation Therapeutics Market between 2026 and 2030?

-

USD 133.06 million, at a CAGR of 3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Drug Class (Immunosuppressants, Anti-infectives, Analgesics, and Others), Distribution Channel (Hospital pharmacies, Retail pharmacies, and Online pharmacies), Type (Left ventricular assist device (LVAD), Heart transplantation, Implantable cardiac defibrillator (ICD), and Extracorporeal membrane oxygenation (ECMO)), Indication (Ischemic heart disease (IHD), Dilated cardiomyopathy (DCM), Valvular heart disease (VHD), and Hypertrophic cardiomyopathy (HCM)) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing prevalence of end-stage heart failure, High risk of post-transplant complications

-

-

Who are the major players in the Heart Transplantation Therapeutics Market?

-

AbbVie Inc., Astellas Pharma Inc., Biocon Ltd., Dr. Reddys Laboratories Ltd., F. Hoffmann La Roche Ltd., GlaxoSmithKline Plc, Glenmark Pharmaceuticals Ltd., Intas Pharmaceuticals Ltd., Jubilant Pharmova Ltd., LEO Pharma AS, Lupin Ltd., McKesson Corp., Novartis AG, Panacea Biotec Ltd., Pfizer Inc., RPG Life Sciences Ltd., Strides Pharma Ltd., Sun Pharmaceutical Industries and Teva Pharmaceutical Ltd.

-

Market Research Insights

- The market is shaped by a move toward precision medicine, where advanced diagnostic tools and biomarker-guided treatment are becoming standard. The adoption of these technologies has improved early rejection detection accuracy by over 30%, allowing for timely intervention.

- Furthermore, personalized immunosuppression regimens have been shown to reduce the incidence of severe side effects like chronic kidney disease by nearly 25% compared to one-size-fits-all protocols. This emphasis on patient-centered care models is supported by a growing infrastructure for digital health for transplant care, which facilitates better adherence and therapeutic drug monitoring.

- The clinical trial data increasingly supports these tailored approaches, influencing the regulatory approval process for next-generation immunosuppressants.

We can help! Our analysts can customize this heart transplantation therapeutics market research report to meet your requirements.

RIA -

RIA -