High Performance Biomaterials Market Size 2024-2028

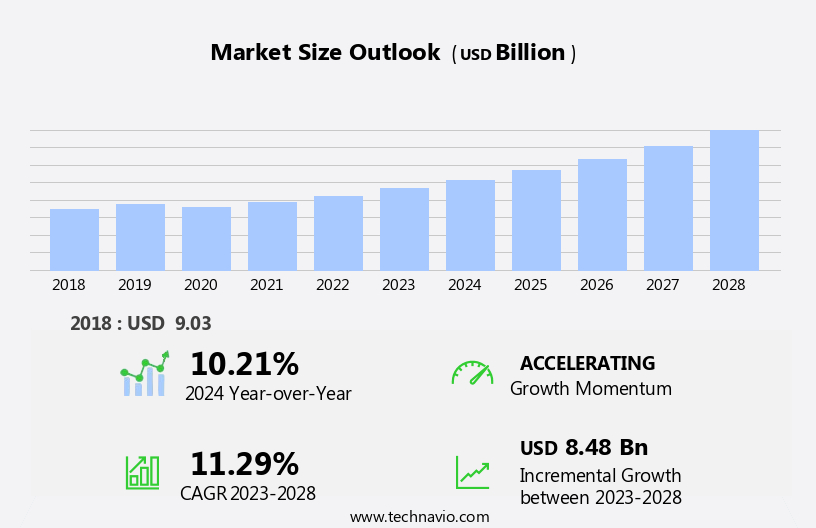

The high performance biomaterials market size is forecast to increase by USD 8.48 billion at a CAGR of 11.29% between 2023 and 2028.

- The market is witnessing significant growth due to the increasing prevalence of musculoskeletal diseases and disorders. According to the World Health Organization, musculoskeletal conditions account for approximately 14% of the global burden of disease, making it a major health concern worldwide. This trend is driving the demand for advanced biomaterials in tissue engineering applications. Moreover, the development of high-performance biomaterials is gaining momentum in the field of tissue engineering. These materials offer superior properties such as biocompatibility, mechanical strength, and bioactivity, making them ideal for the fabrication of tissue scaffolds and implants. However, the market faces challenges due to the presence of stringent clinical and regulatory standards.

- The regulatory approval process for biomaterials is lengthy and expensive, which can hinder market growth. Additionally, the need for long-term clinical trials to ensure safety and efficacy further adds to the challenges. Companies seeking to capitalize on market opportunities must navigate these regulatory hurdles effectively to bring innovative biomaterial solutions to market.

What will be the Size of the High Performance Biomaterials Market during the forecast period?

- The high performance biomaterials market continues to evolve, driven by advancements in biomaterial analysis and modeling. Intellectual property plays a crucial role in shaping market dynamics, with ongoing research and development leading to an influx of patents in the field. Regenerative medicine applications are a significant focus, with clinical trials underway to assess the efficacy of biomaterials in tissue engineering and drug delivery systems. Ethical considerations are a constant concern, with rigorous regulatory guidelines ensuring biocompatibility testing and adherence to biomaterial standards. Implantable devices, such as dental and orthopedic implants, are major applications for high performance biomaterials.

- Surface modification and biomimetic materials enable improved mechanical strength and bioactivity, enhancing the performance of these devices. Biomaterial properties are a key consideration, with researchers exploring the use of bioreabsorbable materials and polymer composites for medical applications. Biomaterials design and 3D printing are revolutionizing the industry, enabling the creation of complex structures and customized implants. Additive manufacturing and biomaterial processing are also gaining traction, offering increased efficiency and precision. The biomaterial industry is continually pushing the boundaries of innovation, with ongoing research in areas such as biomaterial simulation, biomaterial characterization, and biomaterial applications in pharmaceuticals and dental fields.

- The market for high performance biomaterials is diverse and dynamic, with ongoing activities in various sectors. Biomaterials research and development are a continuous process, with in vitro and in vivo studies providing valuable insights into the potential applications and properties of these materials. The future of the market is bright, with a wealth of opportunities for innovation and growth.

How is this High Performance Biomaterials Industry segmented?

The high performance biomaterials industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Metallic

- Polymers

- Ceramic

- Application

- Orthopedics

- Dental

- Cardiovascular

- Plastic surgery

- Tissue engineering and others

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

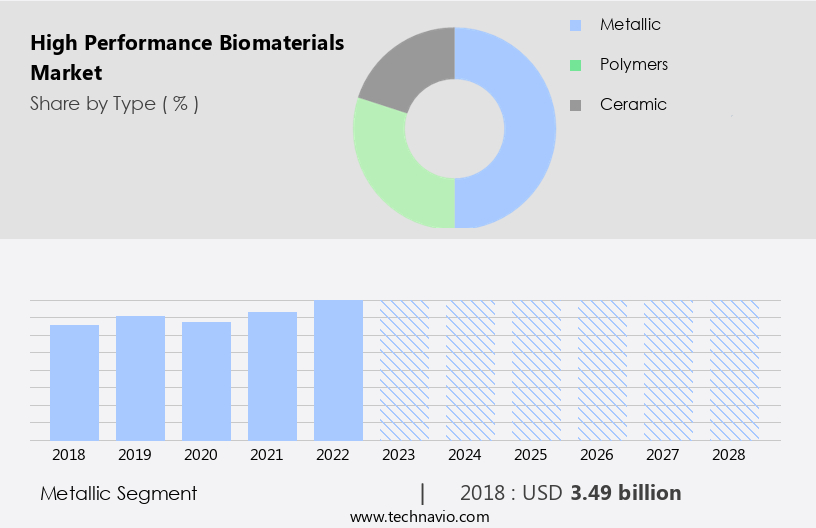

By Type Insights

The metallic segment is estimated to witness significant growth during the forecast period.

Metallic biomaterials, known for their superior thermal conductivity and mechanical properties, are a significant segment in the high-performance biomaterials market. These materials have found extensive use in medical devices and components, such as dental implants, orthopedic implants, cardiovascular stents, and more, due to their suitable mechanical properties and biocompatibility. The market for metallic high-performance biomaterials is poised for growth, driven by their extensive application in various medical sectors, including cardiovascular, dental, and orthopedic applications. Titanium-based alloys are popular choices in this segment due to their excellent strength and biocompatibility. Furthermore, advancements in biomaterial modeling, characterization, and simulation are enabling the development of more sophisticated biomimetic materials, enhancing their performance and applicability in medical applications.

Intellectual property protection through patents plays a crucial role in the biomaterial industry, ensuring innovation and investment in research and development. Regulatory guidelines and ethical considerations are essential factors influencing the market, with stringent regulations governing biocompatibility testing, clinical trials, and in vitro and in vivo studies. Additionally, emerging trends such as 3D printing, additive manufacturing, and polymer composites are expanding the application scope of high-performance biomaterials in areas like tissue engineering, drug delivery systems, and medical devices. Ceramic materials are another class of high-performance biomaterials, offering unique properties such as high mechanical strength and biocompatibility, making them suitable for various medical applications, including dental implants and orthopedic implants.

The biomaterial market is a dynamic and evolving landscape, with ongoing research and innovation shaping its future.

The Metallic segment was valued at USD 3.49 billion in 2018 and showed a gradual increase during the forecast period.

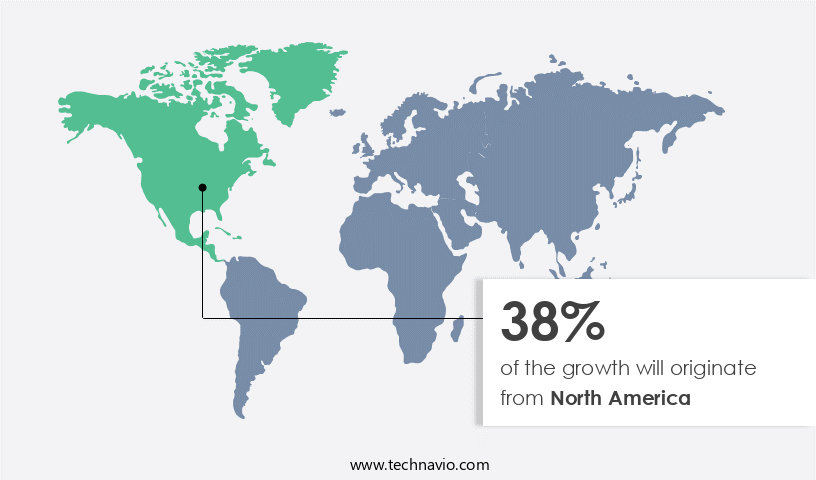

Regional Analysis

North America is estimated to contribute 38% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is experiencing significant growth due to the high prevalence of orthopedic and dental disorders, the increasing adoption of advanced medical devices, and a growing awareness of these conditions among the population. In October 2023, RevBio secured a grant of up to USD3.4 million from the National Institute on Aging (NIA), a division of the National Institutes of Health (NIH), through its Commercialization Readiness Programme. This funding will support the development of the company's bioresorbable materials for orthopedic applications. The market is characterized by the use of biomaterials with unique properties, such as biocompatibility, mechanical strength, and surface modification, for various medical applications, including dental implants, regenerative medicine, and pharmaceutical applications.

Regulatory guidelines play a crucial role in ensuring the safety and efficacy of these materials. Biomaterial modeling and simulation, as well as biomimetic materials and tissue engineering, are key areas of research in the industry. The market includes various types of materials, such as metal alloys, ceramics, polymers, and composites, used in medical devices, implantable devices, and drug delivery systems. The market is also witnessing the increasing use of additive manufacturing and 3D printing for the production of customized implants and scaffolds. Intellectual property protection through patents is essential for companies in this competitive landscape. The market's growth is driven by the increasing demand for biocompatible materials and the development of new applications, such as in vivo studies and clinical trials, for these materials.

Ethical considerations and biocompatibility testing are critical factors in the market's evolution.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of High Performance Biomaterials Industry?

- The rising incidence of musculoskeletal diseases and disorders serves as the primary market driver, underpinning significant growth in this sector.

- High-performance biomaterials play a crucial role in addressing musculoskeletal disorders, which are a significant health concern worldwide. These disorders, caused by orthopedic trauma or injuries, impact the ligaments, tendons, muscles, nerves, and bones, leading to decreased quality of life and daily functioning. Arthritis, the most common musculoskeletal disorder, affects over 54 million Americans, with this number projected to reach 78 million by 2040, according to the Centers for Disease Control and Prevention (CDC). In response to this growing demand, the high-performance biomaterials market has seen significant advancements in biomaterial analysis and modeling to create materials with optimal biocompatibility and mechanical properties for regenerative medicine applications.

- Intellectual property protection is essential to encourage innovation in this field, ensuring ethical considerations are met during clinical trials. Medical applications of high-performance biomaterials extend to implantable devices, where surface modification techniques enhance their integration with the body. By focusing on optimizing biomaterial properties, researchers and manufacturers aim to improve patient outcomes and expand the scope of medical applications.

What are the market trends shaping the High Performance Biomaterials Industry?

- Tissue engineering is experiencing a notable trend towards the development of advanced biomaterials. High-performance biomaterials are increasingly in demand due to their potential to enhance tissue regeneration and improve therapeutic outcomes.

- Tissue engineering is a field that employs biological cells, material methods, bioengineering, and suitable biochemical and physiochemical factors to enhance or replace the functions of vital organs or tissues within the human body. This process aims to restore damaged or impaired living structures, such as skin, muscles, cartilage, and blood vessels. High-performance biomaterials play a significant role in tissue engineering due to their non-toxic profiles, hypoallergenic properties, biocompatibility, biodegradability, and bioactive characteristics. These materials offer various mechanical and structural properties necessary for the proper functioning of repaired tissues. Regulatory guidelines mandate biocompatibility testing for biomaterials to ensure their safety and efficacy in medical applications.

- Biomaterial simulation and in vivo studies are crucial for evaluating the behavior of high-performance biomaterials in real-life conditions. Bioresorbable materials and biomimetic materials are gaining popularity due to their ability to mimic the natural properties of tissues and gradually degrade over time. Biomaterial characterization is essential to understand their physical, chemical, and biological properties and their interaction with the biological environment. High-performance biomaterials have extensive applications in various medical fields, including dental implants. The biomaterial market continues to grow as researchers and scientists strive to develop advanced materials for tissue engineering applications. The focus is on creating materials that offer superior biocompatibility, mechanical strength, and biodegradability to improve the quality of life for patients.

What challenges does the High Performance Biomaterials Industry face during its growth?

- The stringent clinical and regulatory standards pose a significant challenge to the growth of the industry, requiring companies to adhere to rigorous guidelines and undergo extensive testing and approval processes.

- High-performance biomaterials play a significant role in various medical applications, such as orthopedic implants, cell culture, pharmaceutical applications, and medical devices. These materials undergo stringent testing and clinical trials to ensure their safety and efficacy before approval by regulatory bodies. The biomaterials design process involves the use of advanced technologies like 3D printing and additive manufacturing to create materials with specific properties. Metal alloys and bioactive materials are commonly used in medical applications due to their unique properties. The safety profile of these materials is a crucial factor in the US Food and Drug Administration's (FDA) assessment process for medical devices.

- Biomaterial patents are essential in protecting the intellectual property of these innovative materials, ensuring their exclusive use by the patent holders. The biomaterial industry continues to evolve, with ongoing research and development in this field.

Exclusive Customer Landscape

The high performance biomaterials market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the high performance biomaterials market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, high performance biomaterials market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Medical Solutions Group Plc - This company specializes in the production and supply of advanced biomaterials for various surgical applications, including orthopaedics, spinal, dental, and sports surgery.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Medical Solutions Group Plc

- Arctic Biomaterials Oy Ltd

- BASF SE

- Berkeley Advanced Biomaterials

- CAM Bioceramics BV

- CoorsTek Inc.

- Corbion nv

- Covestro AG

- Dentsply Sirona Inc.

- Evonik Industries AG

- Himed LLC

- Honeywell International Inc.

- Koninklijke DSM NV

- Regenity Biosciences

- RevBio Inc.

- Solesis

- Stryker Corp.

- Victrex Plc

- Zimmer Biomet Holdings Inc.

- ZimVie Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in High Performance Biomaterials Market

- In February 2024, BASF Corporation announced the launch of its new high-performance biomaterial, known as Ecovio Cycled, which is made from at least 50% recycled content. This innovative material is designed to reduce plastic waste and support the circular economy in the packaging industry (BASF Corporation, 2024).

- In October 2024, DuPont and Corbion, two leading biomaterial companies, entered into a strategic collaboration to develop and commercialize renewable polymers and bioplastics. The partnership aims to accelerate the production of sustainable materials and reduce the reliance on fossil fuels in the industry (DuPont, 2024).

- In January 2025, Solvay, a global chemical company, completed the acquisition of DSM's Specialty Polymers business. This acquisition significantly expanded Solvay's high-performance materials portfolio, strengthening its position in the biomaterials market (Solvay, 2025).

- In March 2025, the European Union approved the Horizon Europe research and innovation program, which includes a â¬1 billion investment in biobased and circular bioeconomy research. This initiative will support the development and commercialization of high-performance biomaterials, contributing to the EU's goal of becoming climate-neutral by 2050 (European Commission, 2025).

Research Analyst Overview

The market encompasses a diverse range of materials engineered for various applications in healthcare and biotechnology. Key areas of focus include biomaterial mechanical testing for assessing material strength and durability, biomaterial wound healing through advanced composites, and biomaterial cancer therapy utilizing bioinspired materials. Additionally, biomaterial sensors, microstructural analysis, vascular repair, and biocompatibility testing are crucial for ensuring safety and efficacy. Functionalized biomaterials, genotoxicity testing, fibers, gene delivery, imaging, immune modulation, drug delivery, therapeutics, membranes, diagnostics, nanoparticles, actuators, robotics, cytotoxicity testing, bone repair, cartilage repair, microparticles, coatings, degradation studies, gels, nerve repair, computational modeling, smart materials, surface analysis, and electronics are all integral components of this dynamic market.

Continuous advancements in biomaterial technology drive innovation in areas such as tissue regeneration and personalized medicine. Biomaterials are also increasingly being integrated with electronics and robotics to create advanced medical devices and systems. Overall, the market is characterized by constant research and development, regulatory compliance, and a focus on improving patient outcomes.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled High Performance Biomaterials Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

183 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 11.29% |

|

Market growth 2024-2028 |

USD 8.48 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

10.21 |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this High Performance Biomaterials Market Research and Growth Report?

- CAGR of the High Performance Biomaterials industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the high performance biomaterials market growth of industry companies

We can help! Our analysts can customize this high performance biomaterials market research report to meet your requirements.

RIA -

RIA -