Hockey Equipment Market Size 2024-2028

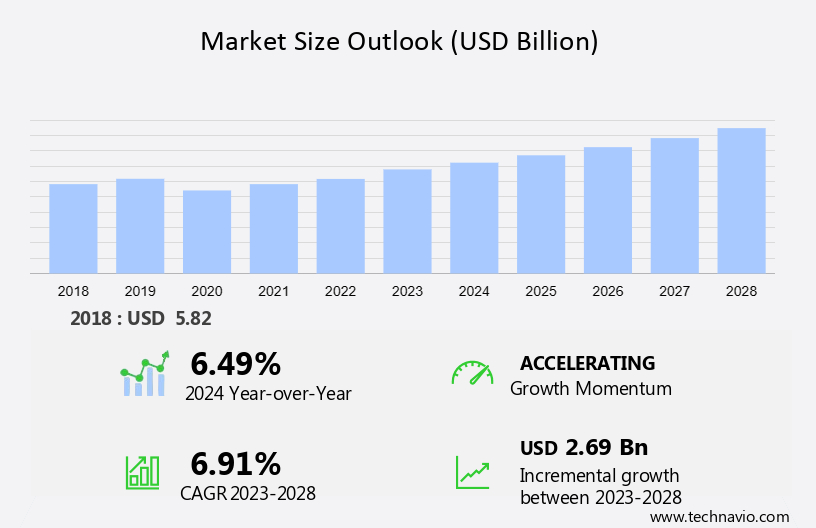

The hockey equipment market size is forecast to increase by USD 2.69 billion at a CAGR of 6.91% between 2023 and 2028.

- The market is witnessing significant growth due to the increasing popularity of ice hockey and advancements in technology. Customizations in hockey equipment cater to the unique needs of players, enhancing their performance and comfort. Technological innovations, such as lightweight and high-performance materials, are revolutionizing the market. Innovative products, such as lightweight sticks made of composite materials and fiberglass, high-performance protective gear, and sensors for performance monitoring, are gaining traction among professional and amateur players. However, the market faces challenges with the rising cost of materials and manufacturing, which may impact the affordability of equipment for players. Despite these challenges, the market is expected to continue its growth trajectory, driven by the passion and dedication of hockey enthusiasts worldwide.

What will be the Size of the Hockey Equipment Market During the Forecast Period?

- The market encompasses a diverse range of products catering to players of all positions, skill levels, and ages. Key market drivers include the growing popularity of hockey, particularly among youth leagues and initiatives, as well as the continuous innovation in gear design and technology. Customization and safety regulations are also significant trends, with an increasing demand for customized products that adhere to stringent safety standards. Manufacturing and distribution channels have evolved, with brands expanding their online presence and implementing 3D scanning technology to offer personalized fits. Sponsorship and advertising play crucial roles in market growth, with professionals endorsing equipment and tournaments providing significant exposure.

- Furthermore, training programs and initiatives, including fan merchandise and player development, further fuel market expansion. Historically, hockey equipment has included essentials such as sticks, protective gear, and skates. However, the market now caters to specialized needs, with gear tailored to specific positions, skill levels, and safety regulations. As the industry continues to evolve, it remains focused on enhancing player performance, safety, and overall enjoyment of the game.

How is this Hockey Equipment Industry segmented and which is the largest segment?

The hockey equipment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Distribution Channel

- Offline

- Online

- Product

- Sticks

- Protective gear

- Footwear

- Others

- Geography

- North America

- Canada

- US

- Europe

- Sweden

- APAC

- South America

- Middle East and Africa

- North America

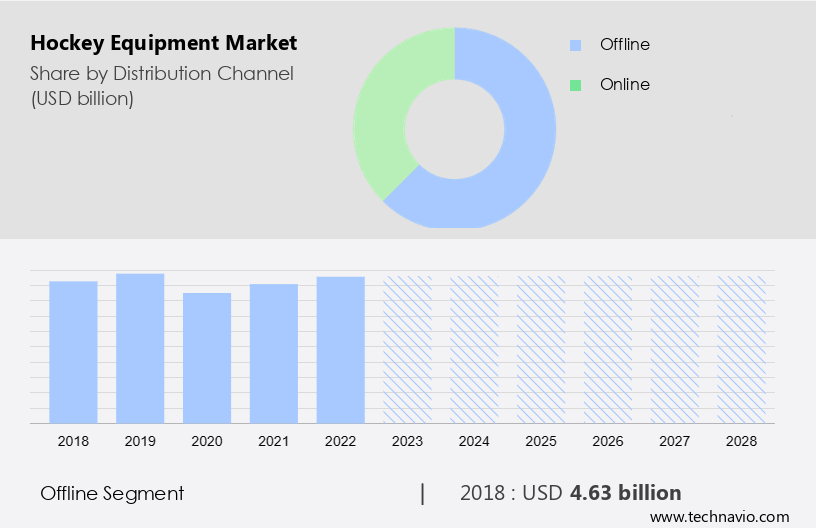

By Distribution Channel Insights

- The offline segment is estimated to witness significant growth during the forecast period.

The offline distribution channel dominates the market, with retailers including hypermarkets, supermarkets, and specialty stores being the primary sellers. Consumers prefer this segment due to the ability to physically assess product quality and specifications. Retailers offer discounts and a wide range of products, making them a popular choice. Market participants are expanding their product reach by partnering with retailers to exhibit innovative equipment. This growth in retail adoption by global market players will enhance consumer awareness of various product types, thereby driving sales during the forecast period.

Get a glance at the Hockey Equipment Industry report of share of various segments Request Free Sample

The offline segment was valued at USD 4.63 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

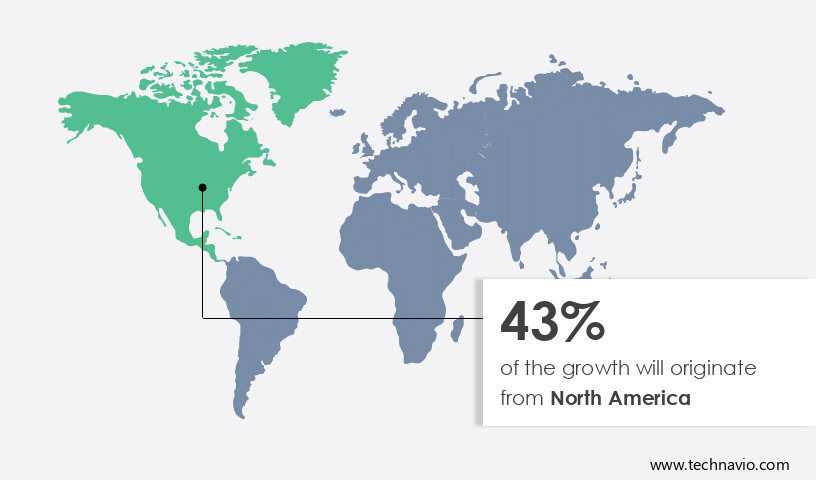

- North America is estimated to contribute 43% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The North American market holds a significant share in the global hockey equipment industry, driven by Canada's strong affinity towards ice hockey as its national winter sport and the US's National Hockey League (NHL) and broadcasting networks promoting the game. The increasing popularity of sports and recreational activities is fueling the demand for hockey equipment in this region. Additionally, e-commerce stores and retail outlets cater to the growing demand for personalized hockey equipment.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Hockey Equipment Industry?

Increasing popularity of ice hockey is the key driver of the market.

- The global ice market is experiencing significant growth due to increasing popularity of the sport in international markets, particularly in countries with winter seasons. The Asia League Ice Hockey is a collaborative effort among Asian nations to establish a credible ice hockey league, which is expanding the distribution networks of manufacturers and reaching new customers. Furthermore, the rise of international and national sports events, increasing consumer awareness towards health and fitness, and growing participation in sports activities are fueling the interest in ice hockey. E-commerce has emerged as a key sales channel for hockey equipment due to its convenience and accessibility.

- In addition, innovative products, such as high-performance sticks made of composite materials like fiberglass and aluminum, protective gear with neck guards and mouthguards, and lightweight skates with molded plastic boots, are driving demand. Celebrity endorsements and performance monitoring sensors are also contributing to market growth. Recreational leagues and emerging markets, including those for women and youth players, are also presenting opportunities for manufacturers to introduce personalized products and manufacturing techniques, such as Lidar scanning and boron fiber blade holders.

What are the market trends shaping the Hockey Equipment Industry?

Customizations and technological advancements in global hockey equipment market is the upcoming market trend.

- The market is experiencing significant growth due to the increasing demand for advanced and personalized equipment among professional clubs, international players, and recreational leagues. Manufacturers are focusing on innovative products, such as lightweight composite sticks made of fiberglass and aluminum, and protective gear with shock-absorbing foams and sensors for performance monitoring. Customization is also a key trend, with players requesting personalized graphics, colors, and sizing.

- Moreover, international federations and leagues, including those for the Winter Olympics and Stanley Cup playoffs, are implementing new rules to prioritize safety, driving the demand for neck guards, mouthguards, and other protective equipment. E-commerce stores and retail outlets are meeting this demand with a wide range of offerings, from high-performance equipment for professional players to entry-level gear for youth and amateur players. The use of emerging materials and manufacturing techniques, such as Lidar scanning and boron fiber blade holders, is also contributing to the growth of the market.

What challenges does the Hockey Equipment Industry face during its growth?

Increasing cost of material and manufacturing of hockey equipment is a key challenge affecting the industry growth.

- The market faces a significant challenge with the escalating expenses of sourcing and manufacturing advanced materials. Protective gear, including helmets, pads, and gloves, necessitates high-performance materials such as Kevlar, carbon fiber, and plastics. These components can be costly to procure and produce, leading to increased prices for consumers. Furthermore, the growing emphasis on player safety, particularly concerning head injuries and concussions, may boost demand for superior protective equipment. This trend could potentially drive up costs and potentially limit accessibility for some consumers seeking the latest and most innovative gear. International federations, professional clubs, and leagues, including the National Hockey League (NHL), host numerous international tournaments and playoffs, such as the Stanley Cup and World Championships.

- In addition, these events feature international players showcasing their skills on synthetic arenas and artificial rinks. To cater to this market, manufacturers employ various manufacturing techniques, including fiberglass, molded plastic, and composite materials, such as boron fiber and aluminum sticks. Additionally, emerging markets, including those catering to women, youth, and amateur players, are increasingly adopting personalized products and performance monitoring sensors. E-commerce stores and retail outlets offer a wide range of hockey equipment, including mouthguards, neck guards, and skates, to cater to the diverse needs of hockey enthusiasts. Celebrity endorsements further fuel demand for high-performance equipment. Despite these challenges, the market continues to grow, driven by innovation and the desire for enhanced player safety.

Exclusive Customer Landscape

The hockey equipment market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the hockey equipment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, hockey equipment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Atlas Hockey

- BAUER HOCKEY LLC

- Canadian Tire Corp. Ltd.

- CanAm Underwater Hockey Gear LLC

- GRAF SKATES AG

- Grays of Cambridge Ltd

- GRYPHON Hockey

- Harrow Sports

- K1 Sportswear

- Pentland Brands Ltd.

- Princess Hockey

- RK Mahajan Exports

- Sport Maska Inc.

- STX LLC

- TK Sports GmbH

- True Temper Sports

- Vaughn Hockey

- Warrior Sports Inc.

- Mazon Hockey

- Adidas AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a wide range of products used by players to participate in this fast-paced and physically demanding sport. Key components of hockey equipment include sticks, skates, protective gear, and goalkeeper equipment. Hockey sticks have undergone significant advancements in recent years, with the primary materials being fiberglass, aluminum, and composite materials. These materials offer various benefits such as increased durability, improved performance, and reduced weight. The use of advanced manufacturing techniques, including LIDAR scanning, has enabled the production of innovative sticks with enhanced blade curvature and surface textures. Skates are another essential piece of equipment for hockey players.

In addition, traditional skates were made of leather boots and metal runners, but modern skates feature molded plastic boots and aluminum or steel runners. These advancements have led to lighter, more comfortable, and higher-performing skates. Protective gear is crucial for ensuring the safety of players during games and practices. Helmets, pads, and gloves are the most common types of protective gear used in hockey. Neck guards, mouthguards, and shin guards are also essential for youth and amateur players. The market is driven by several factors, including the growing popularity of the sport, increasing participation rates, and the continuous pursuit of high-performance equipment.

Furthermore, the market is also influenced by emerging trends, such as personalized products and the integration of technology, including sensors and performance monitoring systems. The market is not limited to professional clubs and international tournaments, such as the World Championships and the Winter Olympics. Recreational leagues and amateur players also contribute significantly to the market's growth. The market is expanding into emerging markets, where the sport's popularity is on the rise. Celebrity endorsements and offline channels, such as retail stores and manufacturing companies, have traditionally been the primary sales channels for hockey equipment. However, the rise of e-commerce stores has disrupted the market, offering convenience and a wider selection of products to consumers.

In addition, despite the advancements in hockey equipment, head injuries remain a significant concern. Rules and regulations governing the use of protective gear, such as helmets and neck guards, are essential to minimize the risk of injuries. Therefore, the market is a dynamic and evolving industry driven by the growing popularity of the sport, technological advancements, and the pursuit of high-performance equipment. The market caters to various segments, including professional clubs, recreational leagues, and amateur players, and offers a wide range of products, from sticks and skates to protective gear and goalkeeper equipment. The market is also influenced by various factors, including manufacturing techniques, emerging trends, and sales channels.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

147 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.91% |

|

Market growth 2024-2028 |

USD 2.69 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.49 |

|

Key countries |

US, Canada, Russia, Sweden, and Finland |

|

Competitive landscape |

Leading Companies, market growth and forecasting, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Hockey Equipment Market Research and Growth Report?

- CAGR of the Hockey Equipment industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the hockey equipment market growth of industry companies

We can help! Our analysts can customize this hockey equipment market research report to meet your requirements.

RIA -

RIA -