Industrial Floor Coatings Market Size 2024-2028

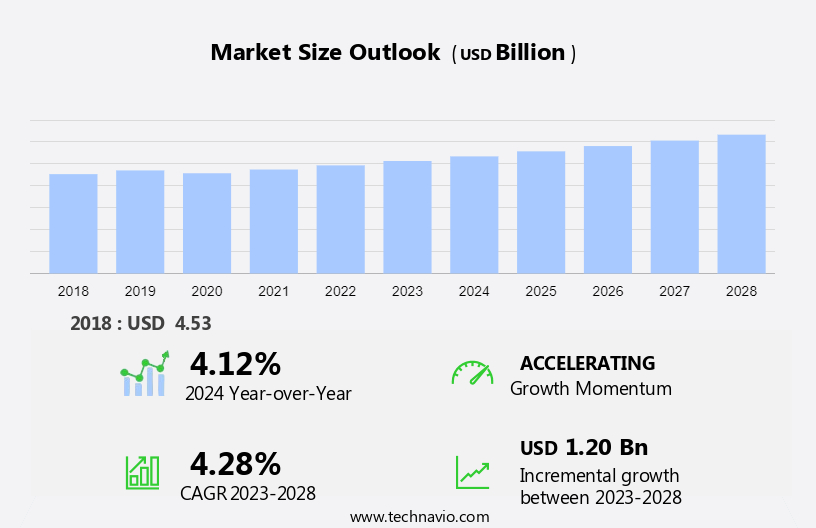

The industrial floor coatings market size is forecast to increase by USD 1.20 billion at a CAGR of 4.28% between 2023 and 2028.

- The market is experiencing significant growth, driven by several key trends and challenges. One notable trend is the increasing demand for environment-friendly coatings, as companies prioritize sustainability and reduce their carbon footprint. Another growth factor is the rising number of mergers and acquisitions among companies, leading to consolidation and innovation within the industry. However, the market also faces challenges, such as the difficulty in preparing substrate surfaces for floor coatings, which can impact the overall quality and durability of the final product. Paints and optical products are also used in some applications. Industrial floor coating systems are used to protect against VOCs (volatile organic compounds) and provide a smooth, even surface for material handling equipment. Proper surface preparation is crucial to ensure the adhesion and longevity of the coating, making it an essential consideration for manufacturers and suppliers in the market.

What will be the Size of the Market During the Forecast Period?

- Industrial floor coatings refer to specialized coatings applied on industrial floors to provide protection against mechanical wear, corrosive liquids, and other harsh conditions. Industrial flooring includes concrete base and smooth flooring surfaces used in various industries such as food-processing, transportation, and consumer products. The market for industrial floor coatings is driven by the increasing demand for floor protection in various sectors. Epoxy coatings and polyaspartic coatings are popular types of industrial floor coatings due to their high-performance properties. These coatings offer excellent chemical resistance, durability, and easy application. Two-component coatings are also gaining popularity due to their fast curing properties.

- In addition, flooring materials used in industrial applications include resins, epoxies, and specialty materials. Coating failures can occur due to various reasons such as improper surface preparation, inadequate curing, and exposure to harsh chemicals. To address these issues, manufacturers are developing advanced coatings with improved chemical resistance and durability. Companies such as DSM and Concrete base are investing in research and development to innovate and offer sustainable solutions.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Epoxy

- Acrylics

- Polyurethane

- Others

- Product

- Concrete

- Mortar

- Terrazzo

- Others

- Geography

- APAC

- China

- Japan

- Europe

- Germany

- UK

- North America

- US

- Middle East and Africa

- South America

- APAC

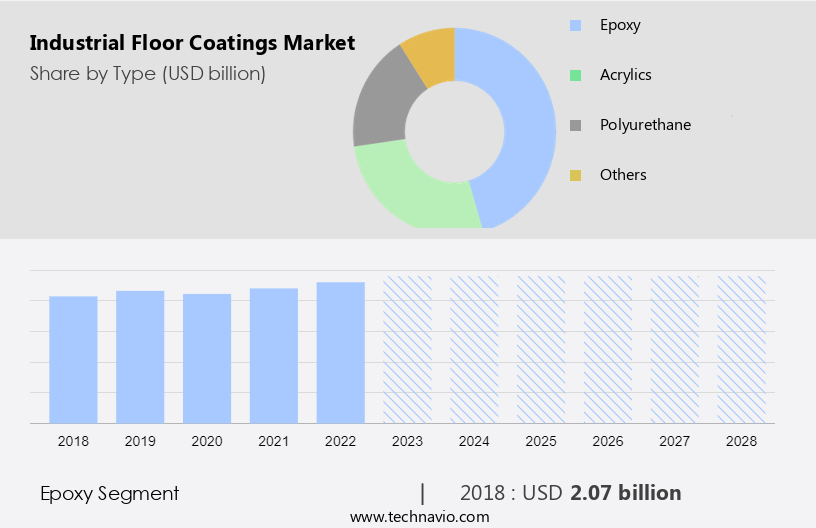

By Type Insights

- The epoxy segment is estimated to witness significant growth during the forecast period.

Epoxy resin is a primary component in industrial floor coatings, forming a protective layer when combined with a curing agent. These coatings are primarily used on concrete floors in various industries, including transportation and consumer products, to ensure performance and longevity. Epoxy floor coatings offer superior chemical resistance, preventing damage from corrosive liquids and acids. They are also resilient against mechanical wear and cracking, making them ideal for high-traffic areas and material handling equipment. Specialty materials, such as optical products and paints, can be incorporated into epoxy floor coatings to enhance their properties. For instance, bio-based floor coating systems derived from bio-renewable resources are gaining popularity due to their fast curing properties and eco-friendly nature.

Get a glance at the market report of share of various segments Request Free Sample

The epoxy segment was valued at USD 2.07 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

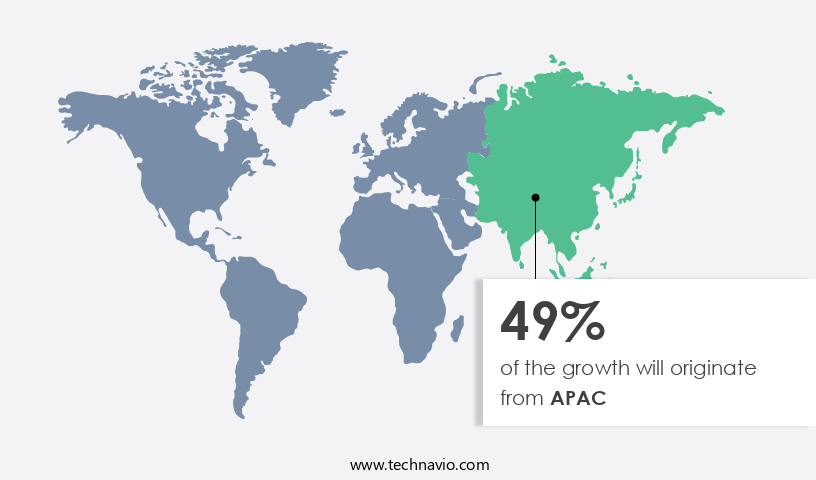

- APAC is estimated to contribute 49% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

In the Asia Pacific (APAC) region, the industrial sector is witnessing significant growth due to the expansion of the automotive and electronics industries. Concrete floor coatings, a crucial component of industrial flooring solutions, play a vital role in these sectors, ensuring mechanical and chemical resistance for material handling areas. The chemical composition of these coatings varies, with polymers such as epoxy, polyaspartic, and two-component coatings being commonly used. APAC's rapid industrialization and infrastructure development have led to an increase in construction projects, including manufacturing facilities, warehouses, logistics centers, and industrial parks. These projects require high-performance coatings that offer durability and protection against abrasion, impact, and chemical spills.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Industrial Floor Coatings Market?

Rising number of mergers and acquisitions among vendors is the key driver of the market.

- The market is witnessing growth and consolidation as leading companies strategically expand their market presence and product portfolios. Mergers and acquisitions enable these entities to integrate resources, optimize operations, and achieve economies of scale, thereby strengthening their competitive position. By acquiring complementary businesses or capabilities, industrial floor coatings companies can broaden their value proposition, lessen reliance on external suppliers, and capture a larger share of the value chain. Resin-based coatings, such as epoxy, dominate the industrial flooring landscape due to their exceptional chemical resistance and durability. Epoxy segment's growth can be attributed to its ability to provide superior performance in various industries, including transportation, consumer products, and food processing.

- In addition, epoxy materials offer excellent resistance to mechanical wear, corrosive liquids, and cracking, making them ideal for floor coating systems in demanding environments. Bio-based floor coatings derived from bio-renewable resources are gaining traction due to their eco-friendly nature and fast curing properties. These coatings cater to the needs of industries like food processing, where smooth flooring surfaces are essential for efficient material handling and equipment operation. Moreover, bio-renewable coatings offer excellent resistance to chemical leakage and bio-based materials, making them a viable alternative to traditional petroleum-based coatings. Industrial floor coatings play a crucial role in protecting floors from wear and tear, chemical exposure, and bio-based materials.

What are the market trends shaping the Industrial Floor Coatings Market?

Increasing demand for environment-friendly industrial floor coatings is the upcoming trend in the market.

- The market is witnessing significant growth due to the increasing demand for durable and high-performance coatings in various industries. Epoxy resins remain a popular choice for industrial flooring due to their excellent chemical resistance and ability to withstand mechanical wear and corrosive liquids. However, there is a growing trend towards the use of specialty materials, such as bio-based coatings, derived from renewable resources. These eco-friendly coatings offer faster curing times, reduced VOC emissions, and improved sustainability. The food-processing industries, in particular, are adopting bio-renewable coatings to meet stringent regulatory requirements and ensure food safety. In addition, the transportation sector is also embracing performance coatings for their ability to protect against chemical leakage and provide long-lasting corrosion protection.

- In addition, industrial floor coating systems are essential for protecting floors from wear and damage, and they are used extensively in applications involving material handling equipment, wheels, and heavy machinery. Polyurethane and epoxy materials continue to dominate the market, but there is a growing interest in petroleum-free alternatives made from bio-renewable resources. The shift towards sustainable coatings is expected to gain momentum as more businesses and governments prioritize environmental responsibility in their construction projects. For instance, The Sherwin Williams Company offers a range of high-performance, eco-friendly coatings that meet the demands of various industries while reducing the environmental impact of flooring materials.

What challenges does Industrial Floor Coatings Market face during the growth?

Difficulty in preparation of substrate surface for floor coatings is a key challenge affecting the market growth.

- Industrial floor coatings play a crucial role in protecting and enhancing the durability of concrete surfaces in various industries. These coatings, which include resins such as epoxy and specialty materials, serve as essential flooring solutions for consumer products, transportation, and performance applications. In industrial settings, epoxy coatings are particularly popular due to their chemical resistance and ability to provide durable, crack-resistant flooring systems. However, the success of industrial floor coatings relies heavily on proper surface preparation. Substrates, often concrete, can present challenges for coating application. Contaminants like oil, grease, dirt, and existing coatings must be removed prior to application.

- In addition, imperfections, such as cracks, spalls, or unevenness, require repair or leveling. Moisture in the substrate can hinder adhesion and curing, leading to coating failure. Consumers may prefer flooring solutions with fast curing properties if they encounter difficulties with substrate preparation. Bio-based floor coatings, derived from bio-renewable resources, have gained popularity due to their eco-friendly nature. These coatings offer the benefits of chemical resistance, mechanical wear protection, and corrosion protection, making them suitable for industries like food processing and material handling. In the transportation sector, coatings with high chemical resistance are essential for protecting against chemical leakage and ensuring the safety of wheels and other moving parts.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Akzo Nobel NV

- Ardex Endura

- ArmorGarage

- BASF SE

- Carolina Painting Co.

- Coatings For Industry Inc.

- Epoxy Central

- Green Surface

- Jemkon Pvt. Ltd.

- Majestic Chemicals

- National Polymers Inc.

- PennCoat Inc.

- Penntek Industrial Coatings

- PPG Industries Inc.

- Resinwerks

- RPM International Inc.

- Sika AG

- The Sherwin Williams Co.

- UCI NA LLC

- Watco Industrial Floors

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Industrial floor coatings refer to specialized coatings applied on concrete and other flooring materials to enhance their durability and performance. These coatings are essential in various industries, including consumer products, transportation, and food-processing industries, to protect floors from mechanical wear, chemical resistance, and corrosive liquids. Epoxy is a prominent segment in the industrial floor coating market due to its durability and chemical resistance. Other specialty materials, such as polyurethane, are also used for their fast curing properties and ability to provide smooth flooring surfaces. Floor coating systems are crucial for protecting floors from cracking and chemical leakage. Performance coatings, such as those used for corrosion protection, are also essential in industries that use material handling equipment with wheels.

Bio-based floor coatings are gaining popularity due to their eco-friendliness. These coatings are made from bio-renewable resources and offer excellent chemical resistance. The use of bio-renewable coatings in industrial flooring is expected to increase as more companies adopt sustainable practices. Industries such as food processing require smooth flooring surfaces for easy cleaning and hygiene. Industrial floor coatings play a crucial role in maintaining these surfaces and ensuring optimal floor usage. Chemical resistance is a significant factor in the selection of industrial floor coatings. Epoxy materials are widely used for their ability to withstand acids and other harsh chemicals. However, petroleum compounds and other chemicals can also impact the performance of floor coatings, making it essential to choose the right coating for specific applications.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

174 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.28% |

|

Market growth 2024-2028 |

USD 1.20 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.12 |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -