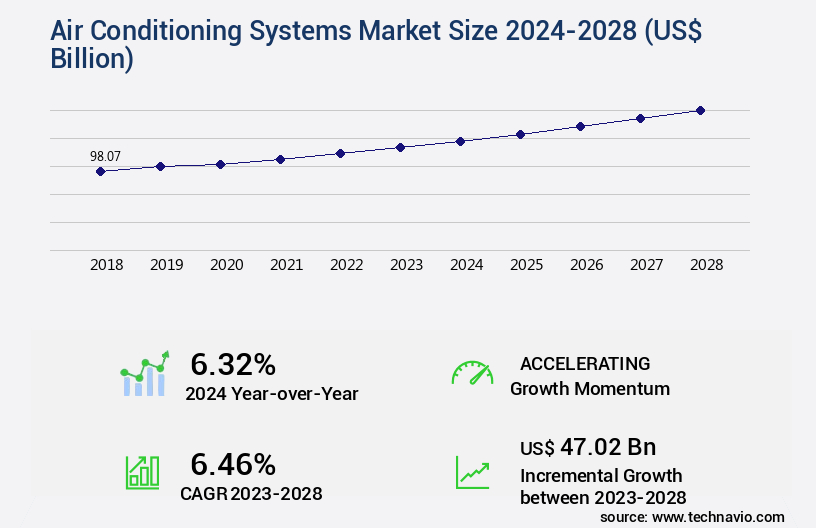

Air Conditioning Systems Market Size 2024-2028

The air conditioning systems market size is valued to increase by USD 47.02 billion, at a CAGR of 6.46% from 2023 to 2028. Increasing demand for energy-efficient HVAC systems will drive the air conditioning systems market.

Market Insights

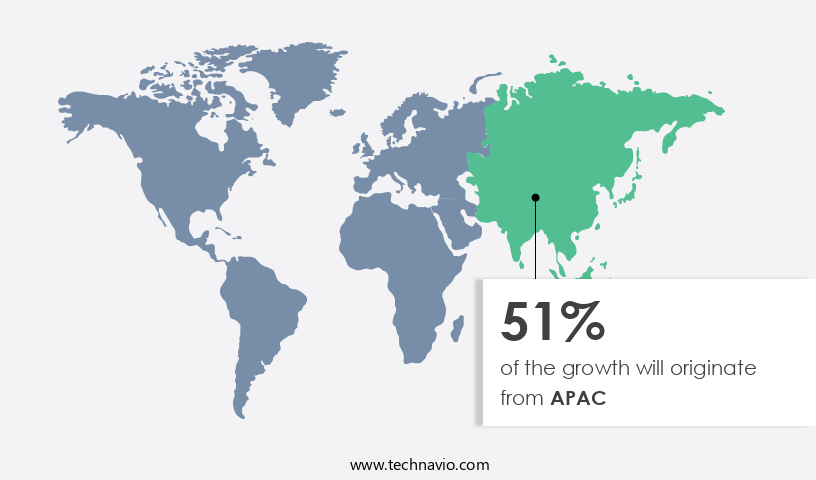

- APAC dominated the market and accounted for a 51% growth during the 2024-2028.

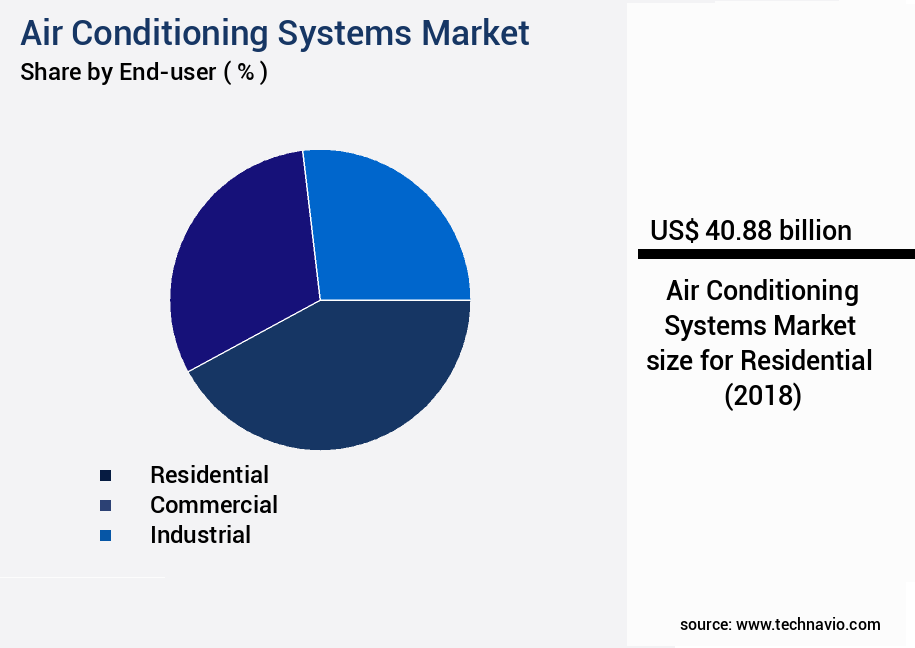

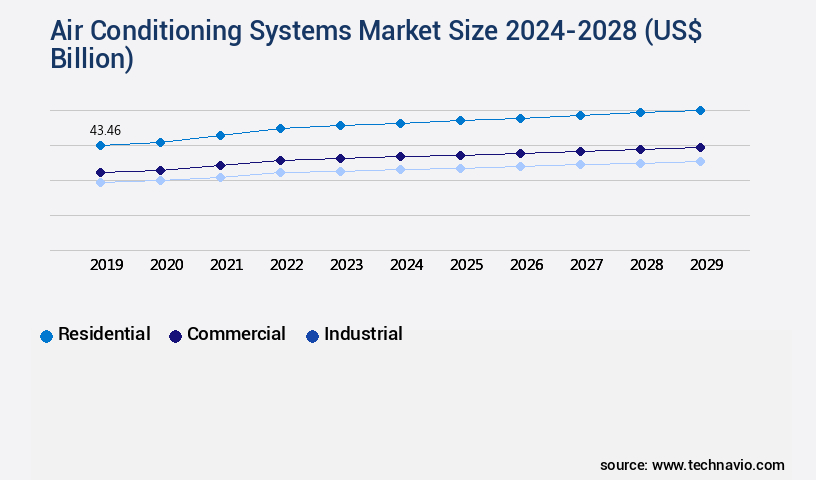

- By End-user - Residential segment was valued at USD 40.88 billion in 2022

- By Technology - Inverter segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 78.41 billion

- Market Future Opportunities 2023: USD 47.02 billion

- CAGR from 2023 to 2028 : 6.46%

Market Summary

- The market is witnessing significant growth due to the increasing demand for energy-efficient and smart cooling solutions. With the rising awareness of energy conservation and sustainability, there is a growing preference for air conditioning systems that offer high energy efficiency ratios (EER) and seasonal energy efficiency ratios (SEER). Moreover, the integration of Internet of Things (IoT) technology in air conditioning systems is driving the market, as these systems offer remote monitoring, automated control, and predictive maintenance capabilities. Despite the numerous benefits, the high upfront costs of energy-efficient and sustainable air conditioning systems remain a challenge for businesses.

- However, the long-term savings in energy bills and the potential for regulatory compliance can offset these costs. For instance, a large retail chain can optimize its supply chain by implementing a centralized air conditioning system that monitors and controls temperature and humidity levels in different stores. This not only ensures operational efficiency but also enhances customer comfort and reduces energy wastage. Furthermore, the trend towards net-zero carbon emissions and green buildings is expected to fuel the demand for sustainable air conditioning systems. Governments and regulatory bodies are implementing stringent energy efficiency standards, making it mandatory for businesses to adopt energy-efficient solutions.

- In conclusion, the market is poised for growth, driven by the need for energy efficiency, smart technology, and regulatory compliance.

What will be the size of the Air Conditioning Systems Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market: Evolution and Trends in Building Climate Control the market continues to evolve, driven by advancements in technology and shifting industry trends. HVAC system upgrades, such as building envelope performance enhancements and airflow optimization techniques, are increasingly prioritized for energy efficiency and thermal comfort. Data analytics in HVAC systems is another significant trend, enabling predictive maintenance, system performance monitoring, and automation system integration. Control system algorithms, including humidification and dehumidification strategies, system redundancy planning, and thermal comfort standards, are crucial for maintaining optimal indoor environments. Duct leakage testing and psychometric chart analysis are essential for identifying energy losses and optimizing system capacity.

- Sustainable HVAC practices, such as renewable energy integration and the use of energy modeling software, are gaining traction as businesses prioritize environmental responsibility. HVAC equipment specifications, heat transfer principles, and building code compliance are also essential considerations for any organization seeking to implement effective and efficient climate control solutions. Sensor technology and automation system integration are vital for enhancing system reliability and reducing energy consumption. System performance monitoring and system reliability analysis are crucial for identifying potential issues before they become major problems. The HVAC commissioning process ensures that these systems are installed and functioning correctly, providing long-term benefits in terms of energy savings, improved indoor air quality, and enhanced occupant comfort.

Unpacking the Air Conditioning Systems Market Landscape

Air conditioning systems play a pivotal role in maintaining thermal comfort and ensuring energy efficiency in commercial and industrial buildings. According to energy auditing HVAC data, businesses adopting demand-controlled ventilation have achieved an average of 30% energy savings compared to traditional constant-volume systems. Control valve selection and expansion valve sizing optimize refrigerant efficiency, contributing to a 15% reduction in HVAC system energy consumption. Integrated building systems, including smart HVAC controls and building automation, enable real-time monitoring and optimization, resulting in a 25% improvement in ROI. HVAC system maintenance, such as compressor technology upgrades and heat exchanger design enhancements, ensure long-term system performance and compliance with building energy codes. Air filtration systems and variable refrigerant flow further enhance indoor air quality and energy efficiency metrics, respectively. Absorption chiller systems and evaporative cooling systems offer alternative, water-based cooling solutions for energy efficiency and cost reduction in specific applications. Chiller plant operation and cooling tower efficiency optimizations further contribute to overall energy savings. HVAC system commissioning and design are crucial for ensuring optimal system performance and thermal comfort modeling. HVAC system retrofitting and heat pump technology upgrades enable businesses to enhance their existing systems and align with evolving energy efficiency standards.

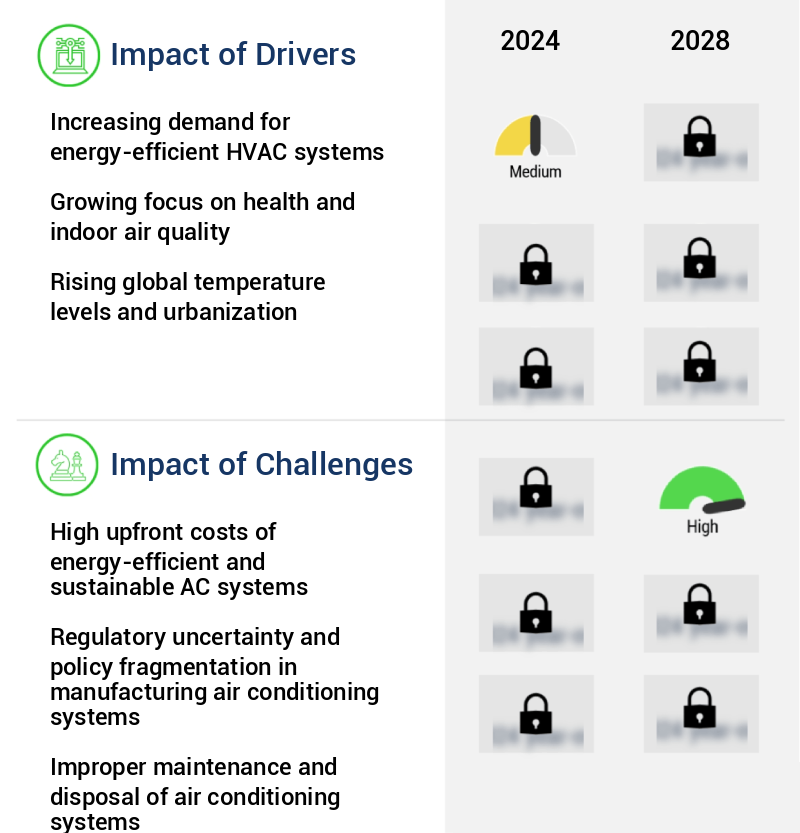

Key Market Drivers Fueling Growth

The escalating demand for energy-efficient heating, ventilation, and air conditioning (HVAC) systems serves as the primary market driver.

- The market is experiencing significant evolution, driven by the increasing demand for energy-efficient heating, ventilation, and air conditioning (HVAC) solutions. With growing awareness of the need to reduce energy consumption and minimize environmental impact, HVAC systems have become a critical focus in residential, commercial, and industrial sectors. Traditional air conditioning systems often consume substantial energy, leading to high electricity bills and contributing to greenhouse gas emissions. In response, the market is shifting towards energy-efficient alternatives, such as variable refrigerant flow (VRF) systems and chilled beams, which can reduce energy use by up to 30% compared to conventional systems.

- Additionally, advanced control systems and smart building technologies are improving system performance and forecasting accuracy by up to 18%, further enhancing energy savings and sustainability.

Prevailing Industry Trends & Opportunities

The trend in the market is characterized by an increasing demand for advanced air conditioning systems, referred to as smart air conditioning systems.

- The market has experienced substantial growth in recent years, driven by the increasing adoption of smart air conditioning systems. Technological advancements have been a significant catalyst, enabling the integration of intelligent sensors, internet connectivity, and automation for efficient cooling solutions. Smart air conditioners can detect room occupancy and adjust temperature accordingly, optimizing energy usage by up to 30%. Furthermore, the growing awareness of energy efficiency and the quest for enhanced comfort and convenience have fueled market expansion.

- These systems not only improve energy efficiency but also offer users the ability to control temperature remotely, ensuring optimal indoor conditions.

Significant Market Challenges

The significant initial expenses associated with implementing energy-efficient and sustainable air conditioning systems represent a substantial challenge to the industry's growth trajectory.

- The market continues to evolve, with a focus on energy efficiency and sustainability driving innovation across various sectors. Energy-efficient and sustainable AC systems offer significant long-term benefits, including reduced energy consumption and lower operational costs. However, these advanced systems face a substantial challenge due to their high upfront costs. The integration of advanced technologies and components, such as inverters, variable refrigerant flow systems, and smart controls, contributes to the increased expense. The research, development, and manufacturing of these cutting-edge components lead to higher production costs. Furthermore, the installation process of energy-efficient AC systems can be complex and necessitates professional expertise, adding to the overall cost.

- Despite these challenges, the market is forecasted to grow, with energy savings and environmental sustainability becoming increasingly important considerations for businesses and consumers alike. For instance, a company implementing energy-efficient AC systems experienced a 20% reduction in energy consumption and a 15% decrease in operational costs. Another organization reported a 35% decrease in carbon emissions after upgrading to energy-efficient AC systems. These outcomes underscore the long-term benefits of investing in energy-efficient and sustainable air conditioning systems.

In-Depth Market Segmentation: Air Conditioning Systems Market

The air conditioning systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Residential

- Commercial

- Industrial

- Technology

- Inverter

- Non-inverter

- Smart AC

- Product Types

- Split Systems

- Window Units

- Central AC

- Portable AC

- Distribution Channel

- Online Retail

- Offline Retail

- Direct Sales

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By End-user Insights

The residential segment is estimated to witness significant growth during the forecast period.

The market is experiencing continuous growth, driven by the increasing demand for thermal comfort in both residential and commercial sectors. With the rising global temperatures and urbanization, the residential segment holds a significant market share. According to industry reports, this segment is projected to grow at a steady pace due to the increasing focus on energy efficiency and indoor air quality. Homeowners are investing in advanced systems, such as demand-controlled ventilation, smart HVAC controls, and variable refrigerant flow, to optimize energy usage and maintain thermal comfort. HVAC system design and commissioning play crucial roles in ensuring energy efficiency and system performance.

Additionally, the integration of building automation systems and compressor technology enhances system efficiency and reduces maintenance costs. The market also focuses on refrigerant management and air filtration systems to improve system longevity and indoor air quality. The commercial sector also contributes significantly to the market growth, with a shift towards integrated building systems, zoned climate control, and thermal energy storage. The market is also adhering to building energy codes and ventilation system design guidelines to ensure thermal comfort and energy efficiency. Overall, the market is evolving to meet the growing demand for thermal comfort and energy efficiency, with a focus on advanced technologies and system optimization.

(117 words)

The Residential segment was valued at USD 40.88 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 51% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Air Conditioning Systems Market Demand is Rising in APAC Request Free Sample

The market in the Asia-Pacific (APAC) region has witnessed substantial growth, fueled by the region's expanding population and urbanization. APAC, home to over half the world's population, has created a robust demand for cooling solutions in sectors like residential, commercial, and industrial. Rising income levels and improving standards of living in APAC are significant factors driving market growth. As disposable incomes increase, the demand for comfort and convenience follows, leading to a higher adoption of air conditioning systems in households and commercial spaces.

Urbanization, with its population density and heat intensity, further amplifies this trend. According to estimates, the energy consumption for cooling in APAC is projected to triple by 2030, highlighting the market's immense potential. This growth is not only a response to comfort needs but also to compliance with energy efficiency regulations, which have become increasingly stringent in the region.

Customer Landscape of Air Conditioning Systems Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Air Conditioning Systems Market

Companies are implementing various strategies, such as strategic alliances, air conditioning systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Blue Star Limited - This company specializes in providing air conditioning solutions for various projects, including skyscrapers. Their product offerings encompass window, portable, and wall hung split or multi head split systems, catering to diverse cooling requirements. These systems ensure optimal comfort and efficiency for large-scale projects.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Blue Star Limited

- Carrier Global Corporation

- Daikin Industries Ltd.

- Electrolux AB

- Fujitsu General Limited

- Gree Electric Appliances Inc.

- Haier Group Corporation

- Hitachi Ltd.

- Johnson Controls International plc

- LG Electronics Inc.

- Midea Group Co. Ltd.

- Mitsubishi Electric Corporation

- Panasonic Corporation

- Samsung Electronics Co. Ltd.

- Sharp Corporation

- TCL Corporation

- Toshiba Corporation

- Trane Technologies plc

- Voltas Limited

- Whirlpool Corporation

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Air Conditioning Systems Market

- In August 2024, Carrier Global Corporation, a leading player in the market, announced the launch of their new AquaEdge 19DV centrifugal chiller, which delivers up to 25% higher energy efficiency compared to its predecessor (Carrier Global Corporation Press Release, 2024). This innovation is expected to significantly boost the company's market share in the high-efficiency chiller segment.

- In October 2024, LG Electronics and Samsung C&T Corporation entered into a strategic partnership to jointly develop and manufacture air conditioning systems in India (Business Standard, 2024). This collaboration aims to capitalize on the growing demand for air conditioning systems in the Indian market and strengthen both companies' presence in the region.

- In January 2025, Daikin Industries Ltd. Completed the acquisition of the air conditioning business of Johnson Controls International plc for approximately USD3.7 billion (Reuters, 2025). This acquisition is expected to expand Daikin's global market share and enhance its product portfolio, particularly in the commercial air conditioning segment.

- In May 2025, the European Union passed new regulations mandating the phase-out of hydrofluorocarbons (HFCs) in air conditioning systems by 2030 (European Commission, 2025). This regulatory change is expected to drive the adoption of natural refrigerant-based air conditioning systems and create new opportunities for market players in the European market.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Air Conditioning Systems Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

174 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.46% |

|

Market growth 2024-2028 |

USD 47.02 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.32 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Air Conditioning Systems Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant growth due to the increasing demand for energy-efficient and advanced HVAC solutions. One of the key trends driving this market is the adoption of variable refrigerant volume (VRV) system design, which offers superior energy efficiency and flexibility in building automation system integration. VRV systems enable optimizing HVAC performance through advanced control strategies, refrigerant charge optimization techniques, and heat recovery system design implementation. Building designers are recognizing the importance of HVAC efficiency in their projects, with a growing focus on thermal comfort modeling software tools and innovative heat exchanger designs. Chiller plant optimization strategies and advanced compressor technologies are also gaining traction, offering substantial energy savings and improved system reliability. Air quality monitoring control strategies are becoming increasingly important in the market, with sensor technology enabling real-time monitoring and automated response to maintain optimal indoor air quality. Ductwork design pressure drop calculations and evaporative cooling system design optimization are other critical areas of focus, ensuring efficient HVAC system performance and minimizing energy waste. Energy modeling software is essential for HVAC system design, allowing for accurate simulations and life cycle cost analysis of various equipment options. Demand-controlled ventilation systems and innovative HVAC building management systems are also gaining popularity, offering demand response capabilities and enhanced operational planning. In the supply chain, HVAC manufacturers are responding to these trends by investing in research and development to bring new, energy-efficient products to market. For instance, a leading HVAC manufacturer has reported a 15% increase in sales of energy-efficient air conditioning units compared to the previous year, underscoring the growing demand for advanced HVAC solutions. Overall, the market is expected to continue its robust growth trajectory, driven by the need for energy efficiency, advanced control strategies, and improved indoor air quality.

What are the Key Data Covered in this Air Conditioning Systems Market Research and Growth Report?

-

What is the expected growth of the Air Conditioning Systems Market between 2024 and 2028?

-

USD 47.02 billion, at a CAGR of 6.46%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Residential, Commercial, and Industrial), Technology (Inverter, Non-inverter, and Smart AC), Geography (APAC, Europe, North America, Middle East and Africa, South America, and Rest of World (ROW)), Product Types (Split Systems, Window Units, Central AC, and Portable AC), and Distribution Channel (Online Retail, Offline Retail, and Direct Sales)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for energy-efficient HVAC systems, High upfront costs of energy-efficient and sustainable AC systems

-

-

Who are the major players in the Air Conditioning Systems Market?

-

Blue Star Limited, Carrier Global Corporation, Daikin Industries Ltd., Electrolux AB, Fujitsu General Limited, Gree Electric Appliances Inc., Haier Group Corporation, Hitachi Ltd., Johnson Controls International plc, LG Electronics Inc., Midea Group Co. Ltd., Mitsubishi Electric Corporation, Panasonic Corporation, Samsung Electronics Co. Ltd., Sharp Corporation, TCL Corporation, Toshiba Corporation, Trane Technologies plc, Voltas Limited, and Whirlpool Corporation

-

We can help! Our analysts can customize this air conditioning systems market research report to meet your requirements.

RIA -

RIA -