Industrial Valves And Actuators Market Size 2024-2028

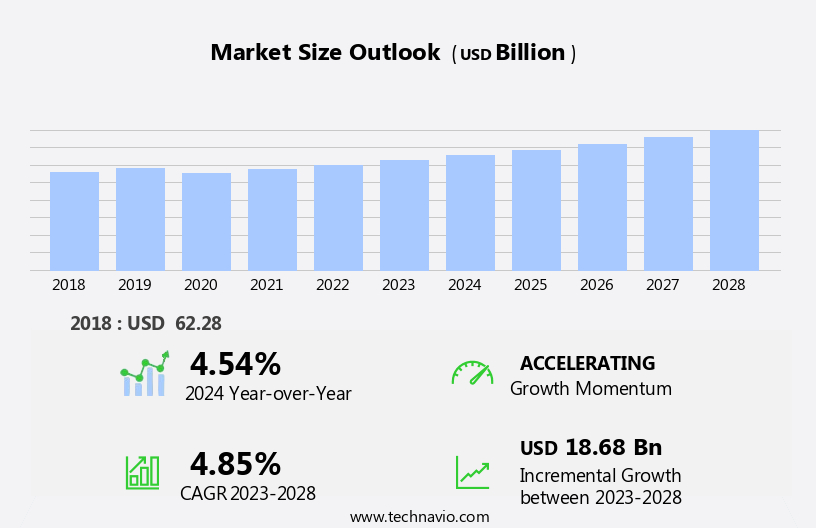

The industrial valves and actuators market size is forecast to increase by USD 18.68 billion at a CAGR of 4.85% between 2023 and 2028.

- The market is experiencing significant growth, driven by increasing investments in modernizing industrial facilities across the globe. This modernization trend is particularly prominent in sectors such as oil and gas, power generation, and chemical processing, where the need for efficient and reliable valve systems is paramount. Another key trend shaping the market is the evolution of valve diagnostics, which enables predictive maintenance and reduces downtime. This is particularly important in industries where even brief interruptions can result in substantial losses. However, the market is not without challenges. Competitive pricing strategies from low-cost Asian manufacturers pose a significant threat to market players in more established regions.

- These manufacturers are able to offer lower prices due to lower labor costs and economies of scale. To counter this, market participants are focusing on innovation and value-added services to differentiate themselves and maintain their market share. Companies that can effectively navigate these challenges and capitalize on the opportunities presented by the evolving market landscape are well positioned for success.

What will be the Size of the Industrial Valves And Actuators Market during the forecast period?

- The market in the United States is a dynamic and significant sector, encompassing a wide range of products including plug valves, diaphragm valves, cryogenic valves, solenoid valves, quarter-turn valves, smart valves, cast iron valves, check valves, electric actuators, control valves, manual actuators, rising stem valves, butterfly valves, ball valves, multi-turn valves, globe valves, gate valves, linear actuators, brass valves, plastic valves, rotary actuators, and more. Market growth is driven by various factors, such as increasing industrial automation, the need for process efficiency, and stringent safety regulations.

- The market's size is substantial, with continued expansion expected due to the growing demand for reliable and advanced valve and actuator solutions in various industries, including oil and gas, power generation, water and wastewater treatment, and chemical processing. Innovations in materials science, automation technology, and design are also contributing to the market's growth and direction.

How is this Industrial Valves And Actuators Industry segmented?

The industrial valves and actuators industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Industrial quarter-turn valves

- Multi-turn valves

- Industrial control valves

- Industrial actuators

- End-user

- Chemical and petroleum industry

- Water and wastewater industry

- Power industry

- Mining and minerals industry

- Others

- Geography

- APAC

- China

- Japan

- Europe

- France

- UK

- North America

- US

- Middle East and Africa

- South America

- APAC

By Product Insights

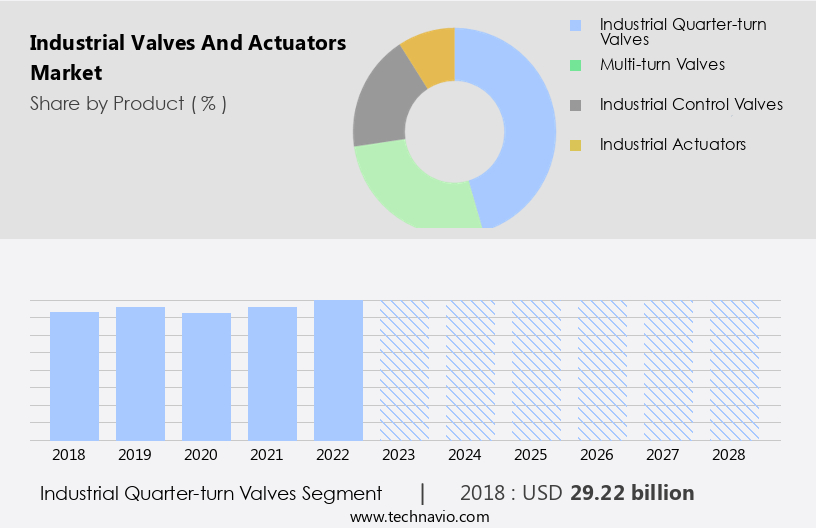

The industrial quarter-turn valves segment is estimated to witness significant growth during the forecast period.

Quarter-turn valves, consisting of ball, butterfly, and plug valves, are widely used in various industries due to their simplicity of design, ease of operation, and affordability. These valves are manually operated by turning the handle at right angles or 0 deg-90 deg to regulate flow parameters. Their advantages include easy maintenance, suitability for chemical and corrosive media, compact and lightweight design, and low-pressure drop with high-pressure recovery. However, they have limitations such as difficulty in cleaning, restrictions in throttling due to differential pressure buildup, and flow turbulence affecting unguided disc movement, which can result in cavitation and choke formation at times.

The growth of quarter-turn valves is driven by the increasing number of greenfield projects in the water and wastewater industry and the maintenance of existing installations. Valve regulations, retrofitting, positioners, standards (ISO, ANSI, API), and certifications play a significant role in the market. Valve inspection services, repair, and testing are essential for maintaining optimal performance. Actuators, including pneumatic, hydraulic, electric, and linear, are used for automating valve functions. Other valve types, such as diaphragm, metal seated, globe, and check valves, also have their unique applications. Overall, the market for quarter-turn valves and related accessories is expected to grow due to the increasing demand for fluid control and process automation in various industries.

Get a glance at the market report of share of various segments Request Free Sample

The Industrial quarter-turn valves segment was valued at USD 29.22 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

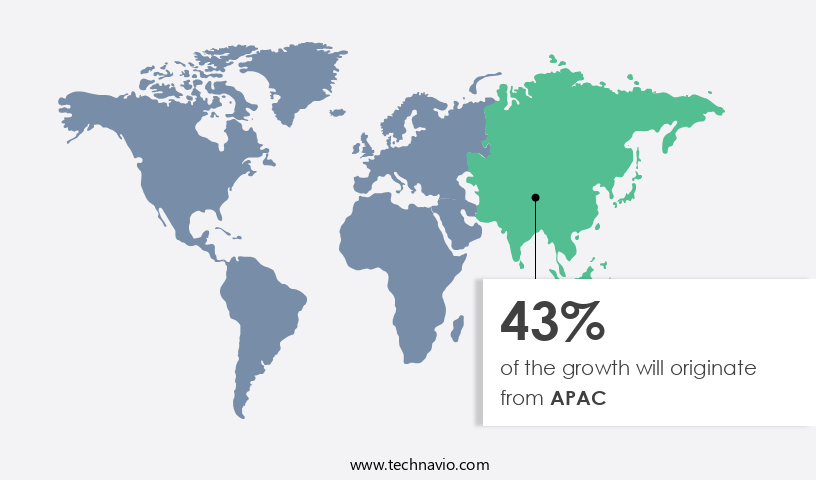

APAC is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The market in APAC is experiencing significant growth due to the increasing demand for refining in the oil and gas industry. China is a major contributor to this growth, investing heavily in new projects to meet domestic demand. Western Australia, with its abundant resources of gas and oil, is attracting substantial investments. According to the Department of State Development, Western Australia accounts for 70% of Australia's and nearly 8% of global LPG exports. With over 130 trillion cubic feet of gas resources and 1,700 million barrels of oil and natural liquids available, the region is expected to see continued investment.

Valves play a crucial role in the oil and gas industry, with various types including Diaphragm Valves, Butterfly Valves, Solenoid Valves, Linear Actuators, and more, each with unique applications. Actuators, such as Pneumatic Actuators, Electric Actuators, and Hydraulic Actuators, are essential for automating valve functions. Valve Regulations and Valve Standards, including ISO Valves, API Valves, and ANSI Valves, ensure safety and quality. Valve Inspection Services, Valve Repair Services, and Valve Testing Services are essential for maintaining optimal valve performance. Market dynamics include the increasing demand for Valve Controllers, Valve Positioners, and Valve Certifications. Smart Valves, Multi-turn Valves, Check Valves, and other advanced valve technologies are also gaining popularity.

The market for Valve Accessories, including Valve Positioners, Valve Positioners, and Valve Positioners, is also growing, as is the demand for Plastic Valves, Metal Seated Valves, and Low Pressure Valves. High Pressure Valves, Cryogenic Valves, and Soft Seated Valves are other important segments. Quarter-turn Valves, such as Ball Valves and Gate Valves, and Manual Actuators, Rotary Actuators, and Rising Stem Valves are also in demand. DIN Valves, Actuated Globe Valves, Actuated Ball Valves, Cast Iron Valves, and other types of valves are essential for various industrial applications. In summary, the market in APAC is experiencing significant growth due to the increasing demand for refining in the oil and gas industry.

Various types of valves and actuators, along with related services, are in high demand to meet the needs of this sector. Regulations and standards ensure safety and quality, while advanced technologies continue to drive innovation.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Industrial Valves And Actuators Industry?

- Increasing investments in modernizing industrial facilities is the key driver of the market.

- The global industrial sector is undergoing a significant transformation as manufacturers invest in modernizing their facilities to enhance efficiency and productivity. This trend is particularly evident in the Asia Pacific region, where governments are initiating developments to bolster the domestic manufacturing sector. With the increasing adoption of automation and advanced control technologies, manufacturing processes are becoming more streamlined and efficient. This shift is essential for manufacturers to remain competitive in today's market, as they strive to yield faster and better returns on their investments.

- The emerging trends in automation, such as the integration of artificial intelligence and machine learning, are expected to shape the competitive landscape of the industrial sector in the coming years. Manufacturers are allocating a considerable portion of their annual budgets towards the adoption of these technologies, recognizing the long-term benefits they bring to the manufacturing process.

What are the market trends shaping the Industrial Valves And Actuators Industry?

- Evolution of valve diagnostics is the upcoming market trend.

- Industrial control valves play a crucial role in modern manufacturing facilities, enhancing operational efficiency, profitability, and safety. These valves, acting as the final control element, significantly impact a plant's performance. Valve diagnostics have emerged as a vital tool, easing the burden on maintenance teams and process control personnel by monitoring valve performance and providing actionable insights. This technology enables the identification of planned maintenance requirements and accurate diagnosis of valves, leading to improved process output with minimal disruptions. The integration of microprocessor-based valve positioning systems and the assimilation of valve-related data into supervisory systems facilitate real-time tracking and monitoring of industrial valves.

- By leveraging advanced technologies, manufacturers can optimize their valve performance, ensuring uninterrupted operations and maintaining the highest quality standards. The adoption of these solutions not only enhances plant efficiency but also contributes to a safer working environment.

What challenges does the Industrial Valves And Actuators Industry face during its growth?

- Competitive pricing strategy of low-cost Asian manufacturers is a key challenge affecting the industry growth.

- The market is witnessing significant growth due to the increasing demand for cost-effective solutions in the manufacturing sector, particularly in Asian countries. With affordably priced land, labor, and raw materials, these regions have attracted substantial investments. End-users in Asia are prioritizing economical machinery and solutions, leading valves and actuator Original Equipment Manufacturers (OEMs) to form strategic partnerships with subcomponent suppliers. In the past, low-cost imports from Asian manufacturers, including China, have penetrated American and European markets, offering competitive pricing due to their abundant resources and labor force.

- This trend continues to influence the market dynamics, making it essential for OEMs to remain price-competitive to maintain market share.

Exclusive Customer Landscape

The industrial valves and actuators market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the industrial valves and actuators market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, industrial valves and actuators market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - The company specializes in innovative sports products, delivering top-tier solutions to enhance athletic performance and leisure activities. Our offerings cater to various sports and fitness enthusiasts, incorporating advanced technology and ergonomic design for optimal results. By prioritizing quality and customer satisfaction, we aim to elevate the sports experience for individuals worldwide.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- ACTUATECH Spa

- AUMA Riester GmbH and Co. KG

- Automation Technology Inc.

- AVK Holding AS

- BOMAFA Armaturen GmbH

- Danfoss AS

- EBRO ARMATUREN Gebr. Broer GmbH

- Emerson Electric Co.

- Flowserve Corp.

- General Electric Co.

- Georg Fischer Ltd.

- Honeywell International Inc.

- MRC Global Inc.

- Rotork Plc

- SAMSON AG

- Schlumberger Ltd.

- The Weir Group Plc

- Velan Inc.

- WAMGROUP Spa

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Industrial valves and actuators play a crucial role in various industries, ensuring the efficient and safe transfer of fluids and gases. These components are essential in regulating pressure, controlling flow rates, and maintaining process conditions in numerous applications. In this context, the market for industrial valves and actuators continues to evolve, driven by several key factors. One significant trend is the increasing demand for automation and digitalization in industrial processes. This has led to the growth of smart valves and actuators, which offer advanced features such as remote monitoring, diagnostics, and predictive maintenance. These technologies enable improved operational efficiency, enhanced safety, and reduced downtime.

Another trend is the focus on regulatory compliance and safety standards. Valve manufacturers and end-users are increasingly prioritizing the use of valves and actuators that meet stringent industry regulations and certifications. This includes ISO, API, ANSI, DIN, and other recognized standards, which ensure the reliability and safety of these components. Moreover, the market for industrial valves and actuators is witnessing a shift towards sustainable and eco-friendly solutions. This includes the use of materials such as brass, cast iron, and plastic, which offer excellent durability and resistance to corrosion, while being recyclable and environmentally friendly. Additionally, there is a growing demand for cryogenic valves and actuators, which are designed to operate in extremely low temperatures, making them ideal for applications in the oil and gas, food and beverage, and pharmaceutical industries.

Furthermore, the market for industrial valves and actuators is witnessing a rise in demand for repair and maintenance services. As these components are critical to the smooth functioning of industrial processes, regular inspections and maintenance are essential to ensure their longevity and optimal performance. Valve inspection services, repair services, and retrofitting are becoming increasingly popular, as they help extend the life of existing valves and actuators, reduce downtime, and lower replacement costs. The market for industrial valves and actuators is diverse and complex, with a wide range of products catering to various applications and industries. These include diaphragm valves, butterfly valves, solenoid valves, linear actuators, and pneumatic, hydraulic, and electric actuators.

Each type of valve and actuator offers unique advantages, such as high pressure capabilities, tight shut-off, quick response times, and ease of installation and maintenance. In , the market for industrial valves and actuators is driven by several key trends, including automation, regulatory compliance, sustainability, and repair and maintenance services. The diverse range of products available caters to various applications and industries, ensuring the efficient and safe transfer of fluids and gases. As the demand for these components continues to grow, manufacturers and end-users must stay abreast of the latest trends and technologies to remain competitive and meet the evolving needs of their customers.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

194 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.85% |

|

Market growth 2024-2028 |

USD 18.68 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.54 |

|

Key countries |

China, US, UK, France, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Industrial Valves And Actuators Market Research and Growth Report?

- CAGR of the Industrial Valves And Actuators industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the industrial valves and actuators market growth of industry companies

We can help! Our analysts can customize this industrial valves and actuators market research report to meet your requirements.

RIA -

RIA -