Insurance Business Process Outsourcing (BPO) Market Size 2026-2030

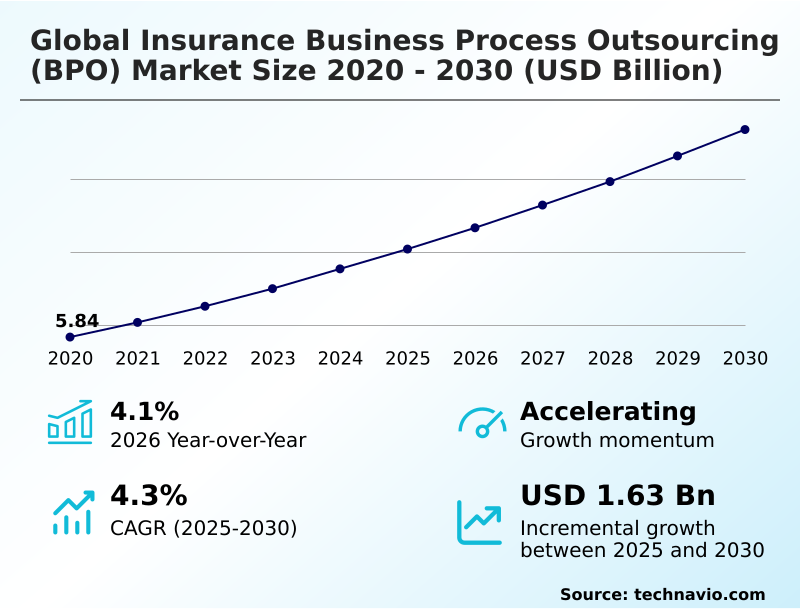

The insurance business process outsourcing (bpo) market size is valued to increase by USD 1.63 billion, at a CAGR of 4.3% from 2025 to 2030. Rising imperative for scalable pension and retirement risk transfer solutions will drive the insurance business process outsourcing (bpo) market.

Major Market Trends & Insights

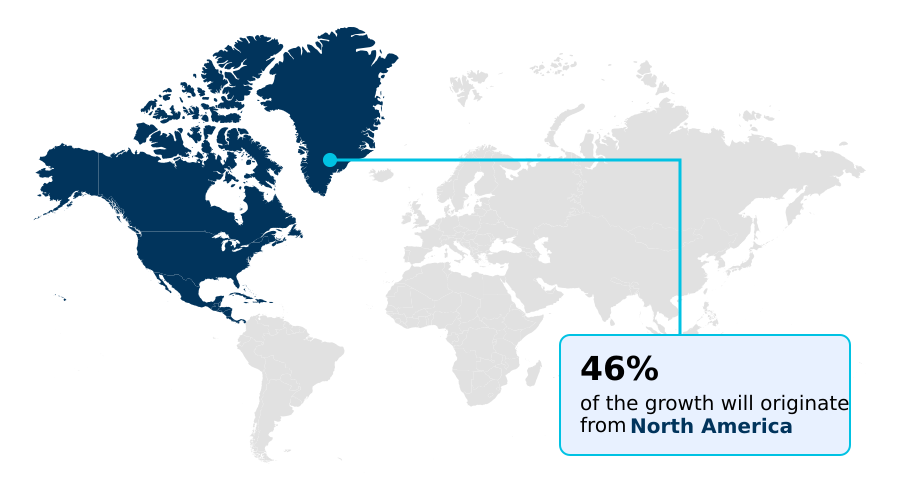

- North America dominated the market and accounted for a 46.5% growth during the forecast period.

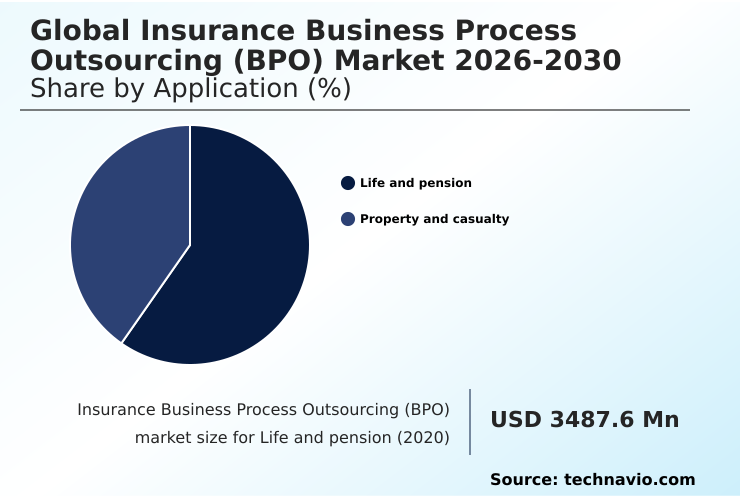

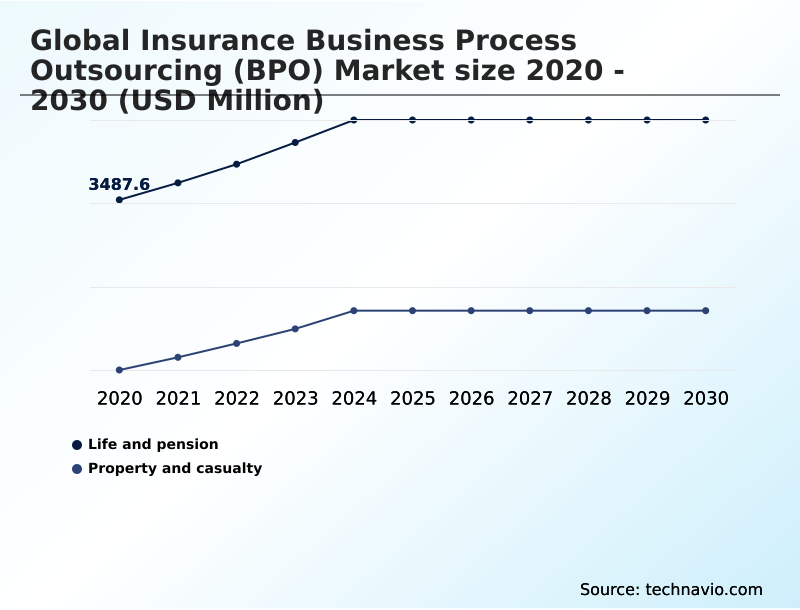

- By Application - Life and pension segment was valued at USD 4.02 billion in 2024

- By End-user - Insurance companies segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 2.83 billion

- Market Future Opportunities: USD 1.63 billion

- CAGR from 2025 to 2030 : 4.3%

Market Summary

- The Insurance Business Process Outsourcing (BPO) market is evolving from a cost-reduction tool into a strategic enabler of digital transformation. Insurers increasingly rely on external partners to navigate complex regulatory landscapes, enhance operational efficiency, and modernize legacy systems.

- A primary driver is the need for specialized expertise in areas like pension risk transfer and cyber liability administration, which many carriers lack in-house. Key trends include the adoption of robotic process automation (RPA) and AI-driven insurance operations to automate routine tasks and improve data analytics capabilities.

- For instance, a property and casualty insurer might outsource its claims function to a BPO provider that uses AI-powered tools for first notice of loss automation and virtual damage assessment, reducing claim cycle times and improving policyholder satisfaction. However, challenges persist, particularly around data security and the integration of sophisticated cloud-native insurance platforms with existing core infrastructure.

- This strategic shift positions BPO providers as critical partners in achieving agility and resilience in a competitive environment.

What will be the Size of the Insurance Business Process Outsourcing (BPO) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Insurance Business Process Outsourcing (BPO) Market Segmented?

The insurance business process outsourcing (bpo) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Life and pension

- Property and casualty

- End-user

- Insurance companies

- Brokers and agents

- Type

- Claims management

- Customer service

- Policy administration

- IT and technological support

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- India

- China

- Japan

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Application Insights

The life and pension segment is estimated to witness significant growth during the forecast period.

The life and pension segment is undergoing a strategic overhaul focused on long-term operational resilience and core systems modernization. Insurers face mounting pressure to manage complex annuity block management and execute pension risk transfer (PRT) strategies with greater precision.

This has spurred a demand for business process as a service (BPaaS) models and specialized managed services. Outsourcing partners provide essential actuarial data management and multi-jurisdictional regulatory compliance support, utilizing cloud-native insurance platforms for real-time reporting.

The transition from paper-based legacy environments to streamlined digital workflows, incorporating agentic artificial intelligence, allows for the automation of underwriting support services.

This shift enables a documented 20% improvement in reporting accuracy for multi-jurisdictional compliance, a key aspect of insurance operations management.

The Life and pension segment was valued at USD 4.02 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 46.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Insurance Business Process Outsourcing (BPO) Market Demand is Rising in North America Get Free Sample

The geographic landscape of the insurance BPO market is led by North America, where a mature financial services sector drives demand for advanced technological frameworks, including predictive analytics for insurance and AI-powered claims processing.

Insurers in the United States and Canada leverage third-party administration (TPA) for complex claims adjudication and actuarial services outsourcing. In this region, the adoption of automated underwriting has reduced policy issuance times by up to 50%.

In contrast, the APAC region is the fastest-growing market, fueled by rapid digitalization and the expansion of insurance platform management. In Europe, the focus remains on navigating stringent regulatory frameworks and data sovereignty management.

BPO partners in this region help firms achieve over 99% compliance with data sovereignty regulations, demonstrating the critical role of specialized expertise in maintaining operational integrity across diverse legal environments.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic focus within the insurance industry is shifting from generalized cost-cutting to achieving specific, high-impact business outcomes through targeted outsourcing. Insurers are now prioritizing cost reduction in insurance claims processing by deploying solutions that streamline workflows from intake to settlement.

- This involves a concerted effort toward improving underwriting accuracy with BPO partnerships that leverage advanced data analytics and sophisticated risk modeling tools. A key area of growth is the demand for scalable pension administration solutions, driven by the increasing complexity of retirement products and the need for specialized expertise in managing pension risk transfer operational tasks.

- BPO for managing closed blocks of business has become essential for carriers looking to divest non-core liabilities while ensuring seamless service continuity. The implementation of AI in insurance customer service outsourcing is transforming policyholder interactions, creating more responsive and personalized support channels.

- This focus on specialized capabilities is critical for digital transformation for property and casualty insurers, who must adapt to new risk categories and customer expectations. Concurrently, securing policyholder data in outsourced environments has become a top boardroom priority.

- Firms that integrate BPO for end-to-end lifecycle management report operational efficiency gains that are often double those of organizations that only outsource piecemeal back-office tasks, demonstrating the value of a holistic approach.

What are the key market drivers leading to the rise in the adoption of Insurance Business Process Outsourcing (BPO) Industry?

- A key market driver is the rising imperative for scalable solutions to manage pension and retirement risk transfers.

- A critical market driver is the rising need for scalable retirement solutions and the specialized administration of complex pension blocks.

- As insurers divest non-core retirement portfolios, the reliance on third-party providers for closed block administration and managing pension risk transfer (PRT) volumes becomes paramount.

- Outsourcing these functions can reduce administrative costs by up to 25% for large, closed books of business.

- These BPO partners offer the necessary scale and technical infrastructure, including first notice of loss (FNOL) automation and claims lifecycle orchestration, to ensure accurate, timely payments and regulatory adherence.

- The integration of advanced analytics into these services has improved cash flow prediction accuracy by over 20%. This allows carriers to offload significant administrative burdens, optimize capital, and focus internal resources on high-growth segments while leveraging expert insurance back-office outsourcing.

What are the market trends shaping the Insurance Business Process Outsourcing (BPO) Industry?

- A key market trend is the expansion of specialized managed services designed to address niche and emerging risks. This includes areas such as cyber liability, parametric climate coverage, and decentralized finance protection.

- A significant market trend is the expansion of specialized managed services tailored for niche risk categories, moving the industry toward knowledge process outsourcing (KPO). Insurers are partnering with providers for cyber liability administration and parametric insurance support to address complex, data-intensive underwriting and claims scenarios.

- This shift toward outsourcing underwriting solutions enables a 30% faster launch time for new parametric products by leveraging external expertise and pre-built technology stacks. The emphasis on operational resilience is also driving the adoption of multi-sourced sovereign clouds to meet stringent data residency rules.

- Concurrently, firms utilizing specialized BPO services for cyber risk management report a 40% reduction in incident response times, highlighting the value of dedicated expertise in a volatile threat landscape. This evolution signifies a move toward strategic partnerships focused on innovation and risk specialization, enabled by advanced insurance data analytics.

What challenges does the Insurance Business Process Outsourcing (BPO) Industry face during its growth?

- A key challenge affecting industry growth is the presence of obstacles related to digital transformation and legacy system integration.

- A primary market challenge is the technical friction associated with legacy system integration. Many established insurers operate on antiquated core systems, creating significant compatibility issues when attempting to connect with modern, cloud-native platforms used by BPO providers.

- This technical debt hinders the seamless implementation of robotic process automation (RPA) and straight-through processing (STP), with integration projects involving legacy systems often overrunning budgets by an average of 35%. The resulting data silos can delay critical decision-making processes by up to two weeks, diminishing the intended efficiency gains from outsourcing.

- This obstacle complicates digital transformation services and the adoption of advanced solutions like customer lifecycle management, requiring a comprehensive modernization strategy to unlock the full potential of BPO partnerships and avoid further loss adjustment expense reduction.

Exclusive Technavio Analysis on Customer Landscape

The insurance business process outsourcing (bpo) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the insurance business process outsourcing (bpo) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Insurance Business Process Outsourcing (BPO) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, insurance business process outsourcing (bpo) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture Plc - Delivers insurance BPO services, including claims processing and policy administration, driving digital transformation for life, health, and property insurers.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture Plc

- Capgemini SE

- Cogneesol BPO Pvt. Ltd.

- Cognizant Technology Solution

- Concentrix Corp.

- DXC Technology Co.

- ExlService Holdings Inc.

- Genpact Ltd.

- HCL Technologies Ltd.

- Hinduja Global Solutions Ltd.

- Infosys BPM Ltd.

- Invensis Technologies Pvt. Ltd.

- Mphasis Ltd.

- NTT DATA Corp.

- Solartis LLC

- Tata Consultancy Services

- Tech Mahindra Ltd.

- Teleperformance SE

- Wipro Ltd.

- WNS Holdings Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Insurance business process outsourcing (bpo) market

- In March 2025, Accenture acquired Altus Consulting, a UK-based specialist consultancy, to bolster its capabilities in delivering end-to-end digital transformation solutions for financial services and insurance clients.

- In November 2024, Genpact announced a strategic partnership with a leading AI firm to co-develop an autonomous claims processing platform, aiming to reduce manual intervention in low-complexity property claims by up to 80%.

- In September 2024, Infosys announced a definitive agreement to acquire Stratus, a technology solutions provider specializing in the property and casualty insurance sector, to integrate its Guidewire platform expertise with Infosys's AI and cloud offerings.

- In January 2025, WNS (Holdings) Ltd. launched a new AI-powered underwriting support service designed to help life insurers analyze alternative data sources, improving risk assessment accuracy and accelerating policy issuance.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Insurance Business Process Outsourcing (BPO) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 300 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.3% |

| Market growth 2026-2030 | USD 1632.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.1% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, Poland, The Netherlands, India, China, Japan, Philippines, Australia, South Korea, UAE, Saudi Arabia, South Africa, Egypt, Kenya, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The insurance business process outsourcing (BPO) market has matured beyond simple labor arbitrage, evolving into a landscape of strategic partnerships focused on deep digital integration. Insurers now leverage claims processing automation, sophisticated policy administration systems, and robotic process automation (RPA) to drive efficiency and enhance customer experiences.

- The adoption of generative AI in insurance operations is a pivotal trend, compelling executive leadership to re-evaluate long-term IT investment strategies and decide between building in-house capabilities or relying on specialized partners for comprehensive digital transformation services. Key enablers include advanced fraud detection, predictive analytics for insurance, and the implementation of cloud-native insurance platforms that offer superior agility.

- Partnerships focused on actuarial data management have enabled some carriers to improve loss ratio prediction accuracy by as much as 15%. This transition toward knowledge process outsourcing (KPO) and human-centric service design, supported by virtual agent implementation and back-office insurance operations, underscores the market's shift toward delivering tangible business value rather than mere cost savings.

What are the Key Data Covered in this Insurance Business Process Outsourcing (BPO) Market Research and Growth Report?

-

What is the expected growth of the Insurance Business Process Outsourcing (BPO) Market between 2026 and 2030?

-

USD 1.63 billion, at a CAGR of 4.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Life and pension, and Property and casualty), End-user (Insurance companies, and Brokers and agents), Type (Claims management, Customer service, Policy administration, IT and technological support, and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Rising imperative for scalable pension and retirement risk transfer solutions, Digital transformation and legacy system integration obstacles

-

-

Who are the major players in the Insurance Business Process Outsourcing (BPO) Market?

-

Accenture Plc, Capgemini SE, Cogneesol BPO Pvt. Ltd., Cognizant Technology Solution, Concentrix Corp., DXC Technology Co., ExlService Holdings Inc., Genpact Ltd., HCL Technologies Ltd., Hinduja Global Solutions Ltd., Infosys BPM Ltd., Invensis Technologies Pvt. Ltd., Mphasis Ltd., NTT DATA Corp., Solartis LLC, Tata Consultancy Services, Tech Mahindra Ltd., Teleperformance SE, Wipro Ltd. and WNS Holdings Ltd.

-

Market Research Insights

- The market dynamic is shifting from labor arbitrage to value-driven partnerships, where insurance IT outsourcing drives measurable outcomes. Third-party policy servicing and intelligent automation in insurance are central to modernizing operations. For example, firms leveraging digital claims management have reported a 40% reduction in processing times.

- Concurrently, AI-powered consulting is reshaping strategies, with carriers that adopt comprehensive technology transformation programs showing a 25% improvement in operational efficiency. Customer experience (CX) outsourcing initiatives are also critical, contributing to a 15-point average increase in policyholder satisfaction scores by providing seamless, omnichannel support.

- This evolution underscores a strategic move toward specialized insurance operations management to achieve both cost control and competitive differentiation in a rapidly changing landscape.

We can help! Our analysts can customize this insurance business process outsourcing (bpo) market research report to meet your requirements.

RIA -

RIA -