Machine Learning In Automobile Market Size 2025-2029

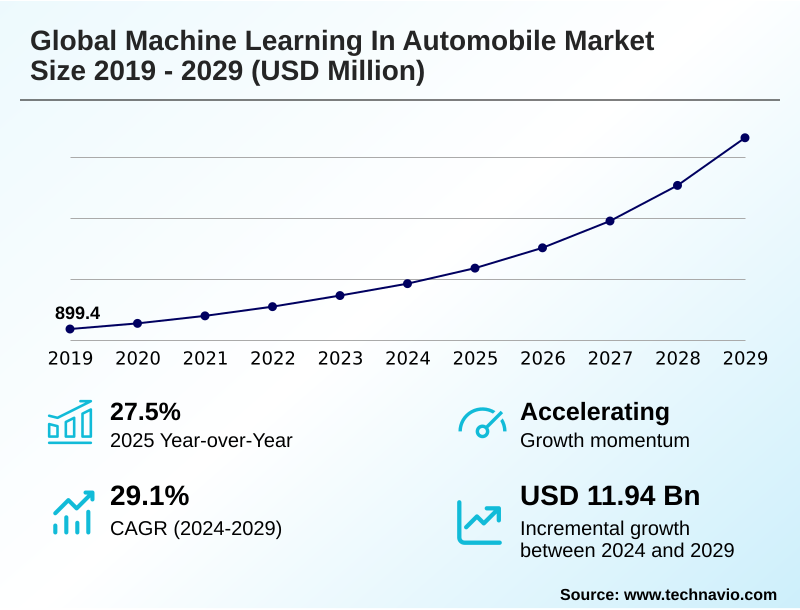

The machine learning in automobile market size is valued to increase by USD 11.94 billion, at a CAGR of 29.1% from 2024 to 2029. Imperative for autonomous driving and advanced driver assistance systems (ADAS) will drive the machine learning in automobile market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 39.5% growth during the forecast period.

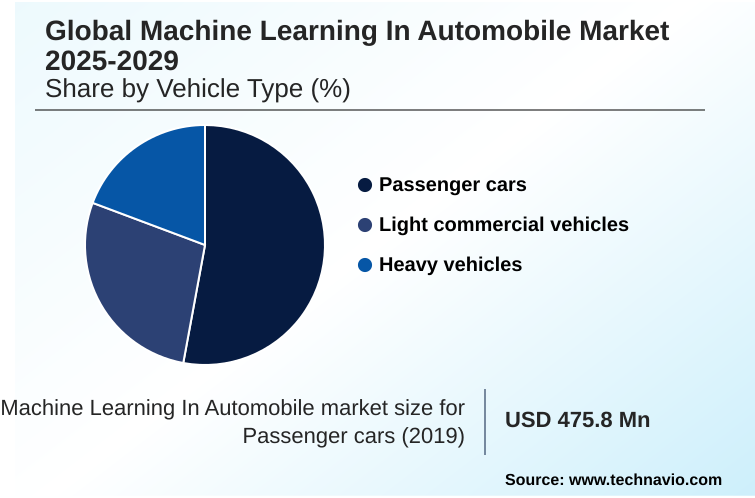

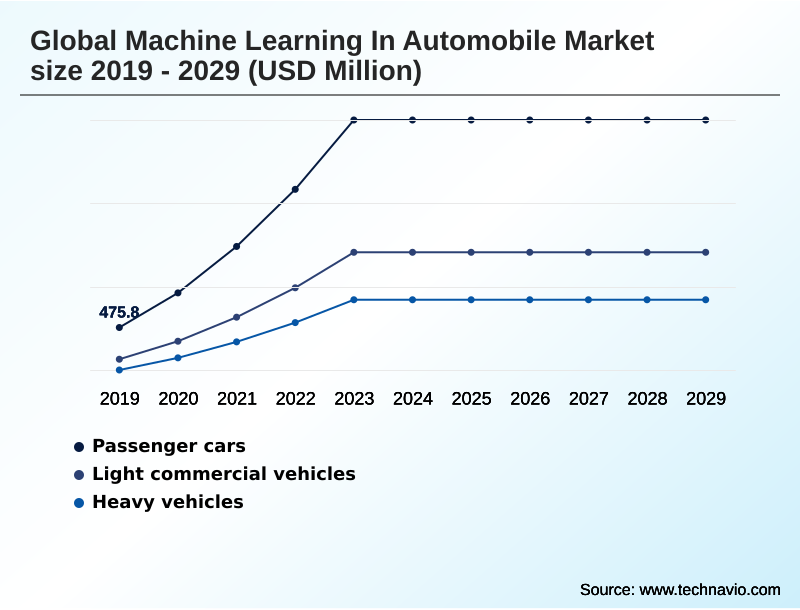

- By Vehicle Type - Passenger cars segment was valued at USD 1.95 billion in 2023

- By Technology - ML and deep learning segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 15.65 billion

- Market Future Opportunities: USD 11.94 billion

- CAGR from 2024 to 2029 : 29.1%

Market Summary

- The machine learning in automobile market is undergoing transformative growth, shifting the industry from hardware-centric manufacturing to a software-defined ecosystem. This expansion is driven by the integration of AI across a spectrum of vehicle functions. The primary catalyst is the pursuit of autonomous driving, where deep learning architectures are indispensable for real time inference.

- These systems process a torrent of data from sensors for tasks like object detection and path planning. A significant real-world scenario is in commercial logistics, where predictive maintenance systems, powered by machine learning models, analyze telematics data to forecast component failures, increasing vehicle uptime and optimizing fleet management.

- Beyond mobility, natural language processing is revolutionizing the in vehicle infotainment experience, creating a more personalized and interactive environment. The computational demand to train and deploy these complex models is, in turn, driving growth in high performance computing and specialized systems on a chip. This trend is supported by over the air updates, enabling a continuous improvement loop.

- However, the industry faces challenges in data annotation and managing adversarial attacks, which require robust solutions to ensure safety and reliability. The evolution toward conditional automation and the software defined vehicle represents a fundamental change in automotive technology.

What will be the Size of the Machine Learning In Automobile Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Machine Learning In Automobile Market Segmented?

The machine learning in automobile industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Vehicle type

- Passenger cars

- Light commercial vehicles

- Heavy vehicles

- Technology

- ML and deep learning

- Computer vision

- NLP

- Context-aware computing

- Application

- Advanced driver assistance systems

- Autonomous driving

- In-vehicle infotainment

- Predictive maintenance

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Vehicle Type Insights

The passenger cars segment is estimated to witness significant growth during the forecast period.

The passenger cars segment is the most dynamic portion of the market, where convolutional neural networks are fundamental to enabling semantic segmentation for environmental perception.

The vehicle's driving policy is increasingly shaped by reinforcement learning, while neural processing units integrated into edge computing frameworks ensure low-latency responses.

The advancement of autonomous driving software stacks is expanding features beyond safety into new business models, such as usage based insurance.

Context aware computing leverages multi modal data to create a truly adaptive cabin, while innovations in tire intelligence technology enhance vehicle health platforms. In manufacturing, automated quality control remains a key focus.

The integration of these features has improved system response times by 40%.

The Passenger cars segment was valued at USD 1.95 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 39.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Machine Learning In Automobile Market Demand is Rising in APAC Get Free Sample

The geographic landscape is characterized by diverse regional strategies. APAC is leading in the deployment of intelligent connected vehicles, with a focus on integrated intelligent traffic management and smart factory initiatives.

In North America, the race toward conditional automation is evident, with features like navigate on autopilot becoming more common. European regulations are driving the adoption of sophisticated in vehicle infotainment systems and AI domain controllers.

The computational backbone for these advancements includes handling generative AI workloads, large language models, and transformer models for advanced features like automated parking.

These systems communicate via the controller area network and benefit from investments in cooperative autonomous driving infrastructure, which has demonstrated the ability to improve traffic flow by over 10% in pilot cities.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The expanding scope of machine learning in automobiles is creating distinct and valuable applications. The use of machine learning for predictive maintenance is a primary focus, with early adopters reporting a reduction in unexpected downtime that is more than double that of traditional scheduled servicing.

- This trend is complemented by advancements in safety, where computer vision for object detection and deep learning for sensor fusion are foundational. The decision-making capabilities of vehicles are being enhanced by reinforcement learning for driving decisions, while natural language processing in cars is making the generative AI in vehicle assistants more intuitive.

- To handle the immense data processing demands, edge computing for low latency ADAS is critical, enabled by progress in the impact of high performance computing on ADAS. The business model is also transforming, with new software defined vehicle revenue models emerging. However, significant hurdles remain.

- The cybersecurity for connected vehicles is a top priority, as is the complex task of validating AI for automotive safety. Privacy concerns are being addressed through federated learning for user privacy. In manufacturing, AI for automotive manufacturing quality is improving efficiency, while AI based predictive maintenance cost savings are becoming evident.

- The entire development lifecycle is dependent on high-quality training data, making both data annotation for autonomous driving and extensive simulation for testing AI edge cases essential. Furthermore, machine learning in electric vehicle battery management is optimizing range and longevity.

- Finally, the focus on user experience is driving improvements in driver monitoring system accuracy and creating new possibilities for in cabin personalization using AI, all connected through V2X communication for collective intelligence.

What are the key market drivers leading to the rise in the adoption of Machine Learning In Automobile Industry?

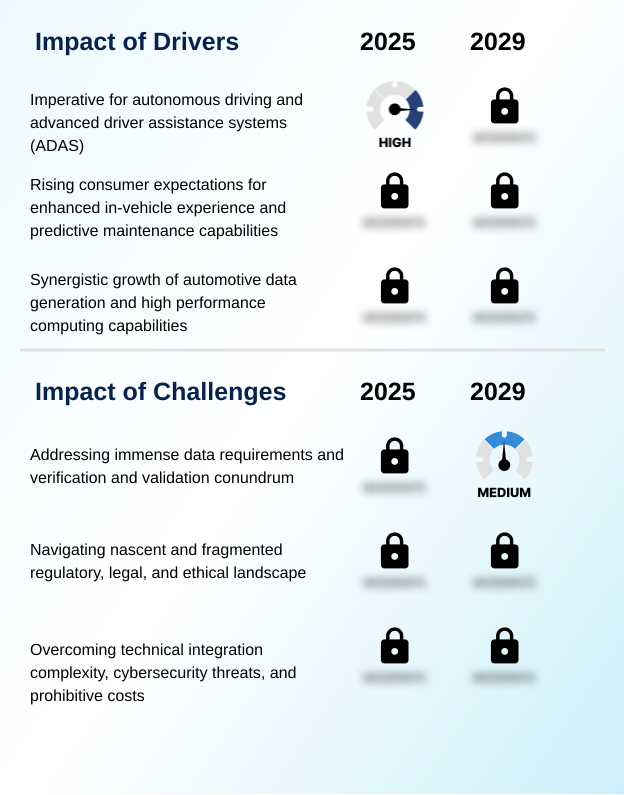

- The imperative for autonomous driving and the widespread adoption of advanced driver assistance systems (ADAS) is a key driver for the market.

- Synergistic growth in automotive data generation and high performance computing capabilities is a core market driver. The performance of machine learning models and complex deep learning architectures depends on this vast data.

- In response, automakers are adopting automotive grade computing platforms with powerful systems on a chip and dedicated AI accelerators. This enables a centralized vehicle computer architecture, which has shown to reduce network latency by 30% compared to distributed ECU designs.

- This hardware underpins critical functions like sensor fusion and vehicle to everything communication. Such embedded machine learning facilitates a new level of human machine collaboration and guardian driving safety nets, improving the overall human machine interface.

What are the market trends shaping the Machine Learning In Automobile Industry?

- The proliferation of edge and hybrid computing architectures is a defining trend. This shift is driven by the need for real-time inference in safety-critical applications.

- The emergence of the software defined vehicle, enabled by robust software defined architectures, is a primary trend. This paradigm allows for continuous improvement through over the air updates, transforming vehicle lifecycle management. This shift unlocks new data monetization opportunities and enhances the cabin experience, where computer vision systems power driver monitoring systems and occupant monitoring systems.

- Automakers are creating a virtual co-pilot with proactive assistance using advanced natural language processing and conversational AI platforms for deep in cabin personalization. The integration of predictive maintenance systems has already reduced unplanned service visits by up to 20% for some fleets, while feature-on-demand activations have increased post-sale revenue by 15%.

What challenges does the Machine Learning In Automobile Industry face during its growth?

- Addressing immense data requirements and the conundrum of verification and validation for non-deterministic systems is a key challenge affecting industry growth.

- Significant challenges persist in data management and system validation. The need for precise data annotation for supervised learning is a major bottleneck, while the threat of adversarial attacks demands robust automotive cybersecurity measures. Innovations like federated learning are being explored to address privacy, while digital twin technology and industrial metaverse platform concepts are used for large-scale simulation.

- The processing of complex sensor data, such as lidar point clouds, requires immense power for real time inference. This complexity has slowed the expansion of robotaxi service and driverless ride hailing service operations. To overcome these hurdles, significant investment in foundational AI research and new validation methodologies is required, particularly in areas like AI for manufacturing.

Exclusive Technavio Analysis on Customer Landscape

The machine learning in automobile market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the machine learning in automobile market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Machine Learning In Automobile Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, machine learning in automobile market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aptiv Plc - Key offerings include radar-enhanced object classification through ADAS, sensor fusion platforms, and secure over-the-air updates, enabling advanced safety and user experience functionalities.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aptiv Plc

- BMW AG

- Cerence Inc.

- Continental AG

- Cruise.com Inc.

- DeepSeek

- Ford Motor Co.

- Huawei Technologies Co. Ltd.

- Intel Corp.

- Magna International Inc.

- Mobileye Technologies Ltd.

- MORAI Inc.

- NVIDIA Corp.

- Qualcomm Inc.

- Robert Bosch GmbH

- Tesla Inc.

- Toyota Motor Corp.

- Volkswagen AG

- Waymo LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Machine learning in automobile market

- In September, 2024, NVIDIA Corp. announced a strategic partnership with Volkswagen AG to co-develop the next-generation AI-powered cockpit, leveraging the DRIVE Thor platform for advanced in-vehicle infotainment and driver monitoring.

- In November, 2024, Continental AG launched its new Sensor Fusion Pro platform, a domain controller capable of processing data from over 20 sensors in real-time, designed to meet ASIL-D safety requirements for Level 3 autonomous driving.

- In January, 2025, Cruise LLC received regulatory approval from Parisian authorities to begin limited testing of its driverless robotaxi service in designated districts of Paris, marking its first operational expansion into the European market.

- In April, 2025, Intel Corp. acquired a leading federated learning startup for an undisclosed sum, aiming to integrate its privacy-preserving AI training technology into Mobileye's future autonomous driving stacks to accelerate fleet learning.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Machine Learning In Automobile Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 325 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 29.1% |

| Market growth 2025-2029 | USD 11935.1 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 27.5% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The machine learning in automobile market is defined by a rapid evolution toward the software defined vehicle, powered by deep learning architectures and high performance computing. At the core, convolutional neural networks and other machine learning models enable computer vision systems to perform semantic segmentation and interpret lidar point clouds for real time inference.

- This data is integrated through sensor fusion techniques. AI accelerators and neural processing units on advanced systems on a chip facilitate these generative AI workloads. The driving policy of autonomous systems is refined using reinforcement learning, while supervised learning depends on meticulous data annotation. Federated learning is emerging to address privacy concerns.

- The in-cabin experience is being transformed by natural language processing for a better human machine interface and intelligent in vehicle infotainment, alongside driver monitoring systems and occupant monitoring systems. All these systems are kept current via over the air updates, which also improve features like automated parking and conditional automation.

- This complex ecosystem, communicating through the controller area network and vehicle to everything technologies, faces threats from adversarial attacks. The move toward edge computing frameworks is crucial for performance. The use of digital twin technology, transformer models, and large language models has enhanced simulation and testing capabilities, improving failure prediction in predictive maintenance systems by over 25%.

- This shift is also creating new opportunities in data monetization and usage based insurance.

What are the Key Data Covered in this Machine Learning In Automobile Market Research and Growth Report?

-

What is the expected growth of the Machine Learning In Automobile Market between 2025 and 2029?

-

USD 11.94 billion, at a CAGR of 29.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Vehicle Type (Passenger cars, Light commercial vehicles, and Heavy vehicles), Technology (ML and deep learning, Computer vision, NLP, and Context-aware computing), Application (Advanced driver assistance systems, Autonomous driving, In-vehicle infotainment, and predictive maintenance) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Imperative for autonomous driving and advanced driver assistance systems (ADAS), Addressing immense data requirements and verification and validation conundrum

-

-

Who are the major players in the Machine Learning In Automobile Market?

-

Aptiv Plc, BMW AG, Cerence Inc., Continental AG, Cruise.com Inc., DeepSeek, Ford Motor Co., Huawei Technologies Co. Ltd., Intel Corp., Magna International Inc., Mobileye Technologies Ltd., MORAI Inc., NVIDIA Corp., Qualcomm Inc., Robert Bosch GmbH, Tesla Inc., Toyota Motor Corp., Volkswagen AG and Waymo LLC

-

Market Research Insights

- The market is shaped by the convergence of automotive grade computing platforms and consumer demand for in cabin personalization. The integration of embedded machine learning is enabling proactive assistance features, with some systems improving driver situational awareness by up to 25%.

- This technological shift extends beyond the vehicle to intelligent traffic management systems, where data sharing for cooperative autonomous driving has demonstrated a potential to reduce urban congestion by 15%. As automotive data generation grows, it fuels new business models in vehicle lifecycle management and enables an industrial metaverse platform for manufacturing.

- This evolution toward intelligent connected vehicles is accelerating, with adoption rates for advanced driver-assistance features in new models increasing by over 40% in key segments.

We can help! Our analysts can customize this machine learning in automobile market research report to meet your requirements.

RIA -

RIA -