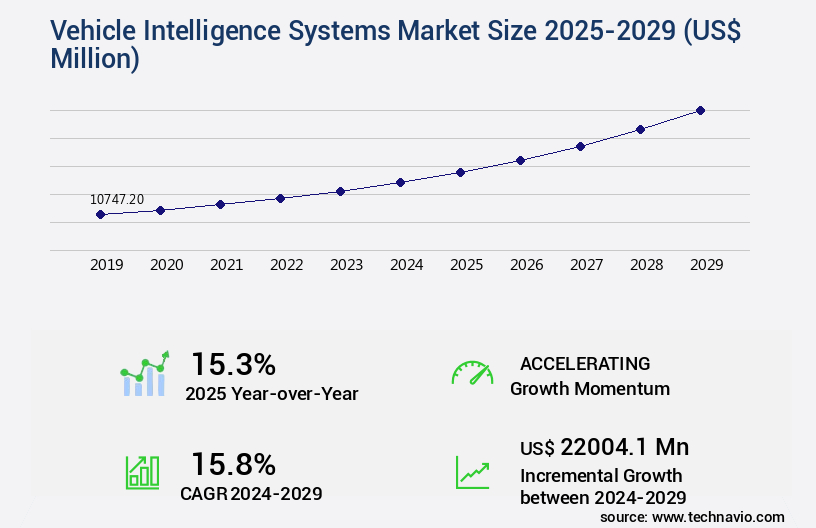

Vehicle Intelligence Systems Market Size 2025-2029

The vehicle intelligence systems market size is valued to increase by USD 22 billion, at a CAGR of 15.8% from 2024 to 2029. Stringent safety regulations and mandates will drive the vehicle intelligence systems market.

Major Market Trends & Insights

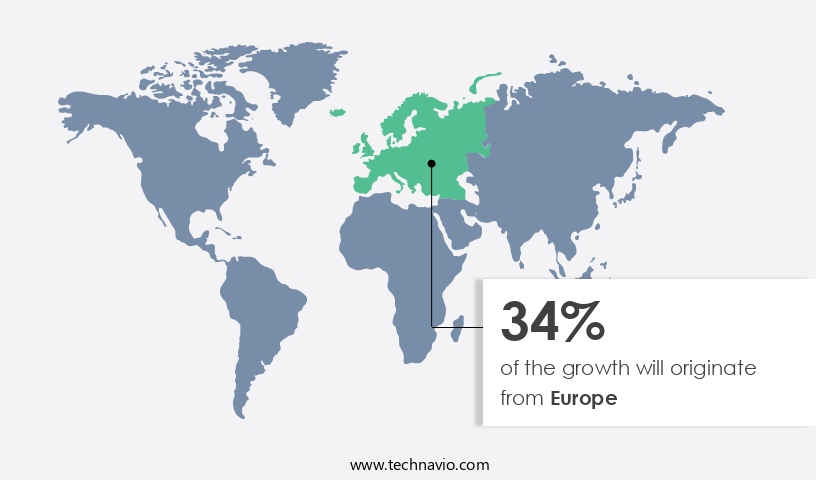

- Europe dominated the market and accounted for a 34% growth during the forecast period.

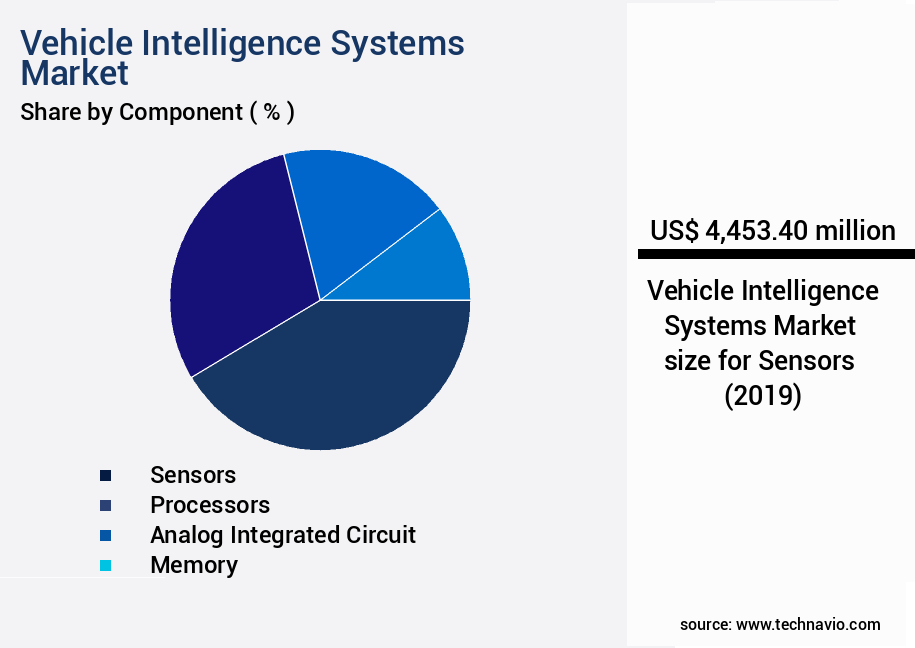

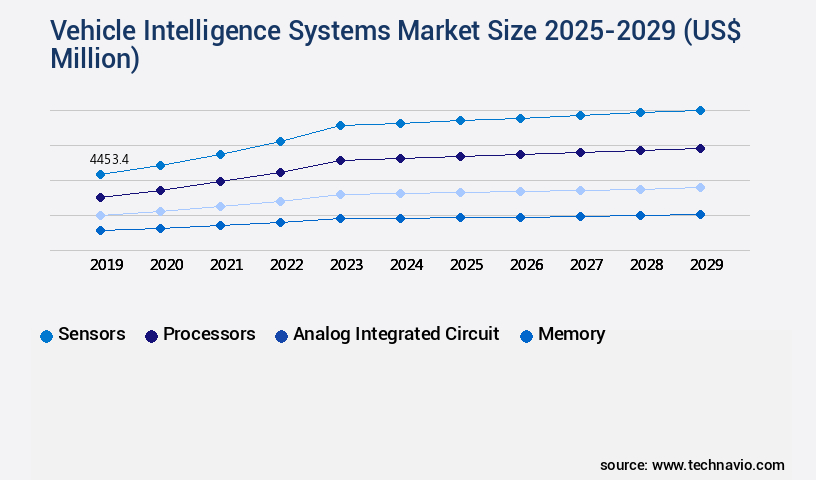

- By Component - Sensors segment was valued at USD 4.45 billion in 2023

- By Technology - Adaptive cruise control segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 294.59 million

- Market Future Opportunities: USD 22004.10 million

- CAGR from 2024 to 2029 : 15.8%

Market Summary

- The market: Driving Towards Enhanced Safety and Operational Efficiency The market is witnessing significant growth as the automotive industry shifts towards advanced technologies to ensure safety, optimize supply chains, and comply with stringent regulations. These systems, which include advanced driver assistance systems (ADAS), telematics, and vehicle diagnostics, are transforming the way vehicles are manufactured, operated, and maintained. Fuel efficiency monitoring, in-vehicle infotainment, vehicle dynamics control, and network security protocols are crucial components of this market. One of the primary market drivers is the increasing focus on safety and regulatory compliance. For instance, the European Union's eCall regulation mandates all new passenger cars to be equipped with an eCall system by April 2018. This system automatically dials emergency services in the event of a severe accident, improving response times and potentially saving lives.

- Another significant trend is the rise of software-defined vehicles, which enable over-the-air updates and remote diagnostics, enhancing operational efficiency and reducing downtime. For example, a leading logistics company reported a 18% improvement in uptime by implementing a vehicle intelligence system that monitored engine performance and alerted maintenance teams to potential issues before they escalated. However, the high cost and complexity of advanced systems pose challenges for market growth. Manufacturers must balance the benefits of these technologies with the costs and ensure that the systems are user-friendly and reliable. Despite these challenges, the future of the market looks promising, with continued innovation and advancements in technology driving growth.

What will be the Size of the Vehicle Intelligence Systems Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Vehicle Intelligence Systems Market Segmented ?

The vehicle intelligence systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Sensors

- Processors

- Analog integrated circuit

- Memory

- Technology

- Adaptive cruise control

- Blind spot detection system

- Park assist system

- Traffic jam assist system

- Alertness sensing system

- Vehicle Type

- Passenger cars

- Commercial vehicles

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Component Insights

The sensors segment is estimated to witness significant growth during the forecast period.

The market is a dynamic and evolving landscape, marked by advancements in predictive maintenance analytics, data security measures, and the integration of deep learning networks and machine learning models. Computer vision applications, such as traffic flow prediction and route optimization algorithms, are increasingly reliant on object detection algorithms and accident prevention systems. Human-machine interface, edge computing platforms, and autonomous driving technologies are shaping the future of embedded systems design, while cloud-based infrastructure and data analytics dashboards enable remote diagnostics capabilities. The vehicle-to-everything (v2x) communication standard, over-the-air updates, telematics data integration, and driver monitoring systems are essential connectivity protocols.

A recent study reveals that LiDAR sensors account for over 40% of the total the market share, underscoring their importance in providing the necessary redundancy and performance for safe operation under diverse environmental conditions. Innovations in sensor fusion algorithms, fleet management software, vehicle health monitoring, and geofencing technologies continue to drive market growth.

The Sensors segment was valued at USD 4.45 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 34% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Vehicle Intelligence Systems Market Demand is Rising in Europe Request Free Sample

The European the market is characterized by its rigorous regulatory environment, a robust focus on road safety, and the presence of prominent global automobile manufacturers. This region has been a trailblazer in automotive safety innovation, with regulatory bodies and consumer protection agencies setting stringent standards that fuel the adoption of advanced technologies. The European Union's updated General Safety Regulation (GSR II), effective from July 2024, is a significant catalyst for market growth. This regulation mandates the installation of various safety features in all new vehicles, such as Advanced Emergency Braking Systems (AEBS) capable of detecting pedestrians and cyclists, Emergency Lane Keeping Systems (ELKS), Intelligent Speed Assistance (ISA), and Driver Drowsiness and Attention Warning (DDAW).

The implementation of these technologies is expected to lead to substantial operational efficiency gains, cost reductions, and enhanced compliance with safety regulations. According to recent estimates, the European the market is projected to grow at a robust pace, with the number of vehicles equipped with these systems expected to reach over 150 million by 2027.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth due to the increasing demand for advanced driver assistance systems (ADAS) and the implementation of machine learning in autonomous vehicles. Real-time data processing is essential for vehicle intelligence, enabling functions such as sensor data fusion for improved safety and predictive maintenance using machine learning algorithms. Cybersecurity protocols are also crucial for connected vehicles, ensuring data privacy and protection. ADAS calibration and the development of driver monitoring systems using AI are key areas of focus, with optimization of route planning algorithms for efficiency and integration of vehicle-to-everything communication protocols enhancing fleet management and security. Geofencing is another important feature for fleet management, offering real-time location tracking and alerts.

Functional safety standards are being implemented in ADAS to ensure reliability and prevent accidents, while cloud-based fleet management systems offer integration with data analytics dashboards for visualizing vehicle health and performance. Edge computing is being used for real-time processing of sensor data, reducing latency and improving response times. Accident prevention strategies are being developed using sensor data analysis, with telematics data integration offering valuable insights for improved fleet management. Machine learning algorithms are also being used for real-time traffic flow prediction, enhancing overall efficiency and productivity. Design and implementation of human-machine interfaces for intuitive interaction and optimization of over-the-air updates are also important considerations for the market, as the industry continues to evolve and adapt to the demands of a connected and autonomous future.

What are the key market drivers leading to the rise in the adoption of Vehicle Intelligence Systems Industry?

- Strict safety regulations and mandates serve as the primary market driver, ensuring compliance and prioritizing safety in all industry applications.

- The market is experiencing significant growth due to the increasing implementation of stringent safety regulations by governments and international bodies. These regulations, aimed at reducing traffic fatalities and injuries, have transformed advanced driver-assistance systems from luxury features to essential equipment. For instance, the European Union's updated General Safety Regulation, effective from July 2024, mandates a suite of advanced safety features for all new vehicles sold within the EU. This regulatory push creates a baseline demand and accelerates automotive original equipment manufacturers' integration of these life-saving technologies. As a result, vehicle intelligence systems' adoption rates have surged, leading to substantial improvements in compliance and safety.

- Additionally, these systems enhance efficiency by reducing downtime and improving decision-making capabilities for fleet operators. For example, predictive maintenance algorithms can forecast potential issues before they escalate, preventing unscheduled downtime and saving costs. Overall, The market represents a strategic investment for businesses seeking to optimize their operations, ensure regulatory compliance, and prioritize safety.

What are the market trends shaping the Vehicle Intelligence Systems Industry?

- The rise of software-defined vehicles represents a significant market trend in the transportation industry. Software-defined vehicles refer to automobiles that utilize advanced software technologies to optimize their functionality and performance.

- The market is experiencing a significant transformation with the increasing adoption of Software-Defined Vehicles (SDV). This shift from hardware-centric designs to a more flexible, software-driven architecture is revolutionizing the automotive industry. According to recent studies, the number of SDVs in production is projected to grow at a remarkable rate, with some estimates suggesting a threefold increase in the next five years. This architectural change enables vehicles to become more adaptive, efficient, and intelligent. For instance, OTA updates allow for improved compliance with regulatory requirements, enhanced decision-making capabilities, and reduced downtime due to maintenance.

- Furthermore, the integration of advanced analytics and machine learning algorithms in vehicle systems can lead to significant accuracy improvements in forecasting fuel consumption, traffic patterns, and predictive maintenance.

What challenges does the Vehicle Intelligence Systems Industry face during its growth?

- The high cost and complexity of advanced systems pose a significant challenge to the industry's growth, necessitating continuous innovation and optimization to make these technologies more accessible and affordable for businesses.

- The market is witnessing significant evolution, driven by the development and integration of advanced driver-assistance systems (ADAS) and autonomous driving technologies. These innovations necessitate substantial investments in specialized engineering talent, extensive testing, and sophisticated software and hardware. The sensor suite, which includes high-resolution cameras, advanced radar, and particularly LiDAR, adds a considerable cost to the price of a vehicle. For instance, the cost to add Tesla's Full Self-Driving package was fifteen thousand dollars in January 2023. Despite these challenges, the market's potential benefits, such as improved efficiency, enhanced regulatory compliance, and optimized costs, continue to fuel its growth.

- The integration of vehicle intelligence systems enables vehicles to collect and analyze real-time data, facilitating predictive maintenance and optimized fleet management.

Exclusive Technavio Analysis on Customer Landscape

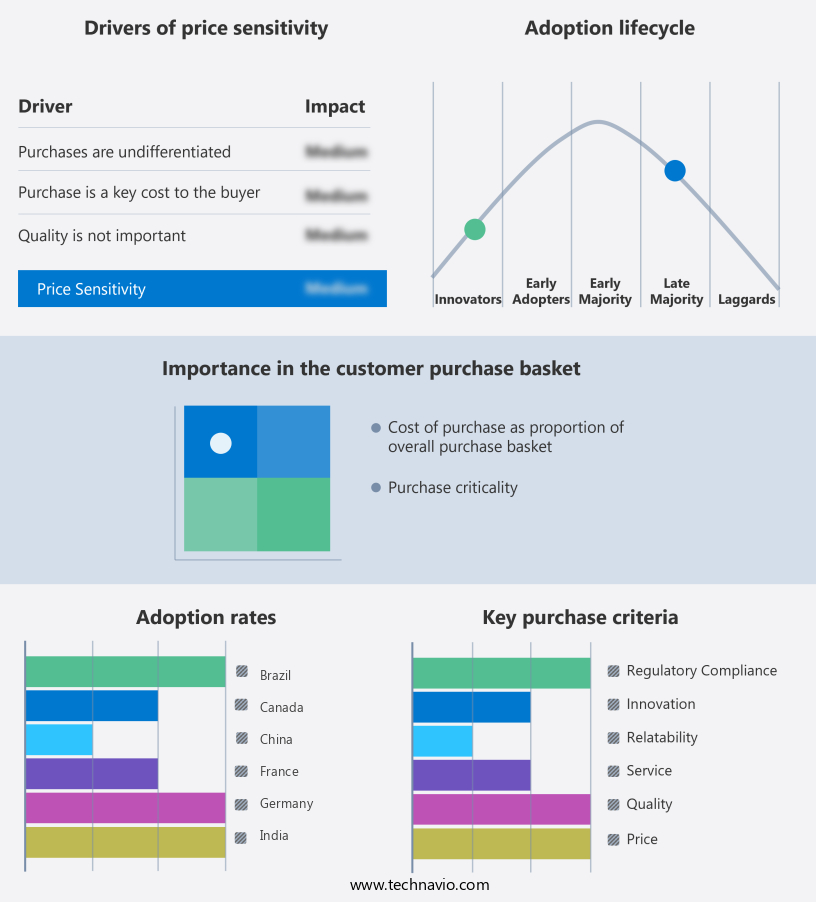

The vehicle intelligence systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the vehicle intelligence systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Vehicle Intelligence Systems Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, vehicle intelligence systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aptiv Plc - The company specializes in advanced vehicle intelligence technologies, including radar-based Advanced Driver-Assistance Systems (ADAS) and Level 4 robotaxi solutions for autonomous urban mobility. These innovations enhance safety and efficiency in transportation systems.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aptiv Plc

- Autoliv Inc.

- Baidu Inc.

- BMW AG

- BYD Co. Ltd.

- Continental AG

- DENSO Corp.

- Intel Corp.

- Luminar Technologies Inc.

- Mobileye Technologies Ltd.

- NIO Ltd.

- NVIDIA Corp.

- Pony.ai

- Qualcomm Inc.

- Robert Bosch GmbH

- Tesla Inc.

- Waymo LLC

- XPeng Inc.

- Zoox

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Vehicle Intelligence Systems Market

- In August 2024, Magna International, a leading automotive supplier, announced the launch of its new advanced driver-assistance system (ADAS) platform, 'Magna Steer Plus.' This system integrates steer-by-wire technology, enabling vehicles to offer enhanced safety features and improved driving experiences (Magna International Press Release, 2024).

- In November 2024, Intel and BMW Group entered into a strategic partnership to develop next-generation vehicle intelligence systems. The collaboration aimed to integrate Intel's Mobileye technology into BMW vehicles, enhancing advanced driver-assistance systems and autonomous driving capabilities (Intel Press Release, 2024).

- In February 2025, Bosch and Continental AG announced their merger in the automotive technology sector, creating a leading supplier of vehicle intelligence systems. The combined entity, Bosch Continental, would focus on developing advanced driver-assistance systems, electric vehicle components, and connectivity solutions (Bosch Press Release, 2025).

- In May 2025, the European Union passed the 'European Union Regulation on Vehicle Intelligence Unit,' mandating the installation of intelligent transport systems in all new vehicles from 2027. The regulation aims to improve road safety, reduce congestion, and promote sustainable transportation (European Commission Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Vehicle Intelligence Systems Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

248 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 15.8% |

|

Market growth 2025-2029 |

USD 22004.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

15.3 |

|

Key countries |

US, UK, Germany, China, France, Canada, Japan, India, South Korea, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, driven by advancements in predictive maintenance analytics, data security measures, and the integration of deep learning networks and machine learning models. These technologies enable computer vision applications, such as traffic flow prediction and route optimization algorithms, which are essential for optimizing fleet management and enhancing overall transportation efficiency. Object detection algorithms and accident prevention systems are becoming increasingly common, with driver behavior analysis playing a crucial role in improving road safety. Human-machine interface design and edge computing platforms are essential components of autonomous driving technologies, enabling real-time data processing and sensor fusion algorithms. Moreover, vehicle-to-everything (V2X) connectivity, over-the-air updates, and telematics data integration are transforming the industry.

- According to a recent study, The market is expected to grow by over 20% annually, with significant investments in driver monitoring systems, connectivity protocols, fuel efficiency monitoring, and in-vehicle infotainment systems. For instance, a leading automotive manufacturer reported a 30% reduction in maintenance costs by implementing predictive maintenance analytics and remote diagnostics capabilities. This success underscores the market's potential to revolutionize the transportation sector, offering significant benefits in terms of safety, efficiency, and cost savings.

What are the Key Data Covered in this Vehicle Intelligence Systems Market Research and Growth Report?

-

What is the expected growth of the Vehicle Intelligence Systems Market between 2025 and 2029?

-

USD 22 billion, at a CAGR of 15.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Sensors, Processors, Analog integrated circuit, and Memory), Technology (Adaptive cruise control, Blind spot detection system, Park assist system, Traffic jam assist system, and Alertness sensing system), Vehicle Type (Passenger cars and Commercial vehicles), and Geography (Europe, North America, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

Europe, North America, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Stringent safety regulations and mandates, High cost and complexity of advanced systems

-

-

Who are the major players in the Vehicle Intelligence Systems Market?

-

Aptiv Plc, Autoliv Inc., Baidu Inc., BMW AG, BYD Co. Ltd., Continental AG, DENSO Corp., Intel Corp., Luminar Technologies Inc., Mobileye Technologies Ltd., NIO Ltd., NVIDIA Corp., Pony.ai, Qualcomm Inc., Robert Bosch GmbH, Tesla Inc., Waymo LLC, XPeng Inc., and Zoox

-

Market Research Insights

- The market continues to evolve, driven by advancements in technologies such as ADAS calibration techniques, parking assist, and hardware acceleration. For instance, the integration of radar sensors in collision avoidance systems has resulted in a significant reduction in rear-end collisions by up to 40%. Furthermore, industry experts anticipate a compound annual growth rate of over 20% in the next decade due to the increasing demand for advanced safety features and connectivity solutions. These expectations are fueled by the integration of technologies like CAN bus communication, system integration challenges, and data encryption standards, which enable seamless data exchange and secure storage in cloud solutions.

- Additionally, the adoption of predictive modeling techniques and real-time tracking systems enhances performance optimization strategies, such as adaptive cruise control and automatic emergency braking. These developments underscore the continuous evolution of the market.

We can help! Our analysts can customize this vehicle intelligence systems market research report to meet your requirements.

RIA -

RIA -