AI In Automotive Market Size 2025-2029

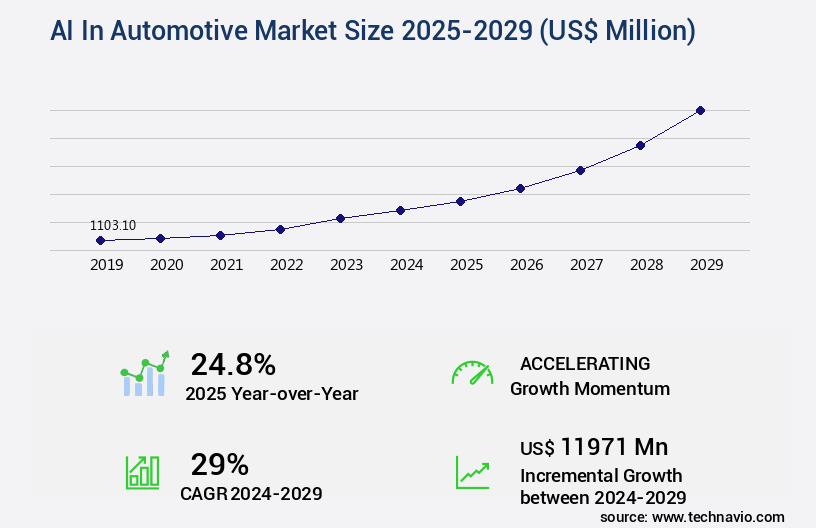

The AI in automotive market size is valued to increase by USD 11.97 billion, at a CAGR of 29% from 2024 to 2029. Imperative for enhanced safety and relentless pursuit of autonomous driving will drive the ai in automotive market.

Major Market Trends & Insights

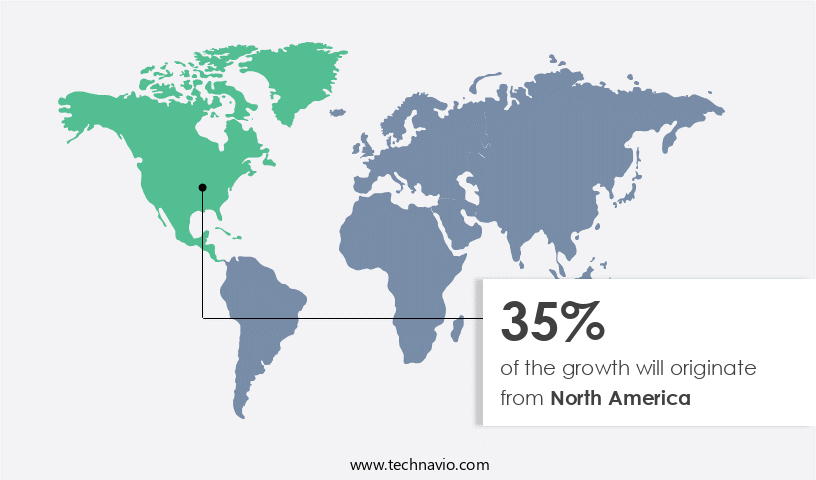

- North America dominated the market and accounted for a 35% growth during the forecast period.

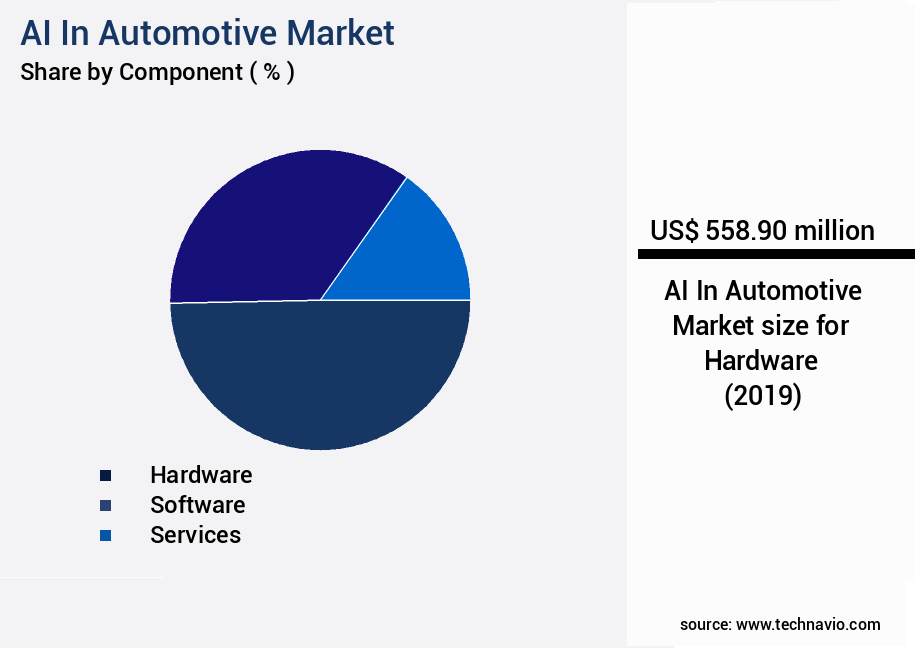

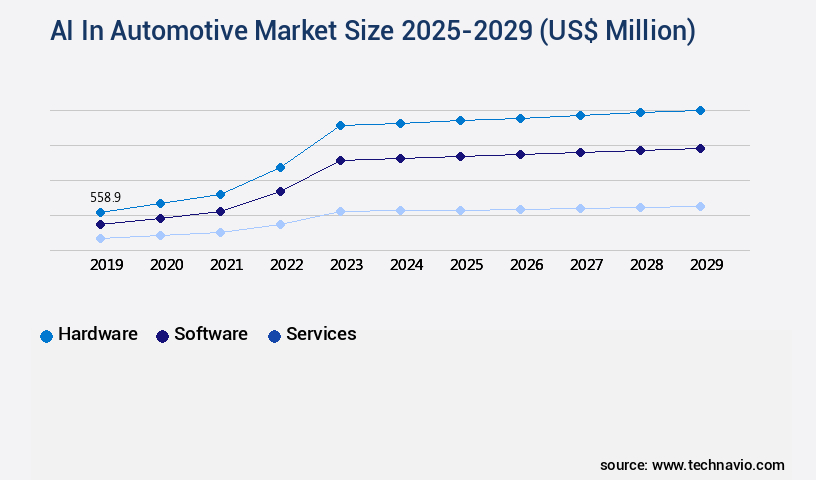

- By Component - Hardware segment was valued at USD 558.90 billion in 2023

- By Technology - Machine learning segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 1.00 million

- Market Future Opportunities: USD 11971.00 million

- CAGR from 2024 to 2029 : 29%

Market Summary

- The market is experiencing unprecedented growth, with an estimated 35.3 million autonomous vehicles expected to be in use worldwide by 2030, according to a recent study. This expansion is driven by the imperative for enhanced safety and the relentless pursuit of autonomous driving. Centralized compute and software-defined vehicle architectures are becoming the norm, enabling advanced driver-assistance systems (ADAS) and autonomous driving technologies to process data in real-time.

- However, regulatory fragmentation and the lack of global standardization pose significant challenges. These issues necessitate collaboration between governments, automakers, and technology companies to establish clear guidelines and harmonize regulations. Despite these hurdles, the future of AI in automotive is promising, with the potential to revolutionize transportation and reshape industries.

What will be the Size of the AI In Automotive Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI In Automotive Market Segmented ?

The ai in automotive industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Hardware

- Software

- Services

- Technology

- Machine learning

- Computer vision

- Deep learning

- Context awareness

- Natural language processing

- Application

- Semi-autonomous vehicles

- Fully-autonomous vehicles

- Vehicle Type

- Passenger vehicles

- Commercial vehicles

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The market is a dynamic and evolving landscape, with ongoing activities shaping the future of transportation. Key areas of focus include emission reduction strategies, achieved through advanced driver-assistance systems (ADAS) and autonomous driving systems, as well as fuel efficiency improvement through powertrain optimization and motion planning algorithms. Cybersecurity protocols are paramount, with radar sensor technology, lidar sensor technology, and camera sensor technology integrated to ensure vehicle safety. Over-the-air updates enable real-time data processing and predictive maintenance models, while AI ethics frameworks guide the development of natural language processing, computer vision systems, and machine learning algorithms. Sensor fusion techniques and data analytics dashboards provide valuable insights into driver behavior analysis and traffic flow optimization.

In-cabin monitoring systems enhance passenger comfort and convenience. The hardware segment, comprised of centralized compute platforms and advanced sensory systems, is crucial for executing complex AI software stacks in real time. For instance, the number of AI-enabled vehicles on the road is projected to reach 250 million by 2035. This growth underscores the market's potential and the need for continuous innovation.

The Hardware segment was valued at USD 558.90 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Automotive Market Demand is Rising in North America Request Free Sample

The market is experiencing significant advancements, with North America, specifically the United States, leading the charge. This region is marked by a dynamic and competitive ecosystem, comprised of established automakers, tech giants, and innovative startups. The primary focus lies in attaining advanced levels of driving automation. For instance, Waymo LLC, a key player, has made notable commercial strides, launching its fully driverless Waymo One ride-hailing service in Los Angeles in February 2024. This expansion represents a pivotal moment in the commercialization of autonomous mobility.

The market is poised for continued growth, with the number of connected cars projected to reach 125 million by 2026, according to recent reports. This underscores the immense potential and increasing adoption of AI technologies in the automotive sector.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth as automakers and tech companies integrate advanced AI technologies to enhance vehicle functionality and improve the driving experience. One of the key applications of AI in EVs is AI-powered predictive maintenance, which uses machine learning algorithms to analyze vehicle data and identify potential issues before they become major problems. In the realm of autonomous driving, AI plays a crucial role in the validation process, enabling real-time object detection using deep learning and advanced driver assistance systems that utilize sensor fusion. Traffic optimization is another area where AI shines, with AI-driven vehicle routing systems designed to reduce congestion and improve overall efficiency. Fuel efficiency is another area where AI is making a difference, with AI-powered powertrain control systems optimizing energy usage and reducing emissions.

AI-based in-cabin monitoring systems are also being developed to improve driver alertness and safety. The development of robust AI models for autonomous vehicles is a major focus, with ethical considerations playing a significant role in their design. Ensuring cybersecurity in connected and autonomous vehicles is another priority, with the implementation of over-the-air updates for AI-enabled systems and high-definition map creation for autonomous navigation. The integration of lidar, radar, and camera sensors for perception, along with AI algorithms for path planning in complex driving scenarios, is essential for autonomous vehicles to navigate safely and effectively. Deployment of edge computing for real-time AI processing and use of cloud computing for data storage and analysis are also key components of AI systems in the automotive industry. Furthermore, AI-based systems are being developed for reducing vehicle emissions, while machine learning is being applied for driver behavior understanding. The design of AI systems for enhanced vehicle safety and security, optimization of vehicle performance using reinforcement learning, and application of AI for reducing vehicle emissions are all areas of active research and development in the automotive AI market.

What are the key market drivers leading to the rise in the adoption of AI In Automotive Industry?

- To ensure enhanced safety and relentlessly pursue autonomous driving capabilities, market participants prioritize imperative advancements.

- The market is experiencing significant growth due to the relentless focus on enhancing vehicle safety and the ultimate goal of achieving full autonomy. Human error continues to be the leading cause of traffic accidents and fatalities worldwide. Artificial intelligence, specifically Advanced Driver-Assistance Systems (ADAS) and autonomous driving (AD) technologies, offer the most viable solution to this persistent issue. These AI systems function as a constant and attentive co-pilot, capable of detecting potential hazards and responding quicker and more dependably than a human driver. The industry's commitment to safety is further reinforced by stringent regulatory frameworks and influential safety rating programs, such as New Car Assessment Programmes (NCAP), which grant higher scores to vehicles equipped with advanced AI-powered safety features like automatic emergency braking, blind-spot detection, and lane-keeping assist.

- The market's expansion is further fueled by the integration of AI in various automotive sectors, including manufacturing, logistics, and maintenance, leading to increased efficiency and cost savings.

What are the market trends shaping the AI In Automotive Industry?

- Shifting to centralized compute and software-defined architectures is becoming a mandated trend in the market for vehicles. This approach to design ensures greater efficiency and flexibility in automotive systems.

- The market is experiencing a significant shift from decentralized systems with multiple electronic control units (ECUs) to centralized, powerful compute platforms. This transition is paving the way for software-defined vehicles (SDVs), where a vehicle's functionality and features are primarily determined by software. The software-defined paradigm enables over-the-air (OTA) updates, simplifying vehicle wiring harnesses, reducing weight and cost, and providing the necessary computational power for advanced, holistic AI applications. According to recent studies, the number of ECUs in a modern vehicle can range from 50 to 150, while the centralized compute platform in an SDV can offer processing power equivalent to that of 20-30 ECUs.

- This architectural evolution is a crucial step towards autonomous driving and advanced driver-assistance systems (ADAS), enhancing vehicle safety and efficiency.

What challenges does the AI In Automotive Industry face during its growth?

- The absence of global standardization and regulatory fragmentation poses a significant challenge to the industry's growth trajectory. This issue hinders the uniform implementation of regulations and practices across borders, leading to inefficiencies, increased costs, and potential market distortions. To mitigate these risks, it is essential for stakeholders to collaborate and advocate for harmonized regulations and industry best practices.

- The automotive AI market is undergoing significant evolution, with applications spanning sectors such as advanced driver-assistance systems (ADAS), autonomous driving, and predictive maintenance. According to recent studies, the global automotive AI market is projected to reach a value of over USD60 billion by 2027, growing at a substantial rate. However, the deployment of automotive AI faces a major challenge in the form of a complex and fragmented regulatory landscape. Different regions, including North America, Europe, and Asia Pacific, are pursuing distinct regulatory approaches. In North America, for instance, regulations are largely state-led, leading to a patchwork of rules that can hinder the global scaling of autonomous driving solutions.

- A notable instance of regulatory power came in October 2023 when the California Department of Motor Vehicles suspended Cruise's deployment and driverless testing permits following a serious incident, underscoring the importance of regulatory compliance in the automotive AI sector.

Exclusive Technavio Analysis on Customer Landscape

The ai in automotive market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in automotive market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Automotive Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in automotive market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aptiv Plc - The company specializes in artificial intelligence (AI) applications within the automotive sector. Notably, they provide solutions for autonomous driving through Motional, as well as advanced safety systems. These innovations enhance vehicle functionality and safety, positioning the company as a leader in AI technology integration within the automotive industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aptiv Plc

- Aurora Innovation Inc.

- Baidu Inc.

- BYD Co. Ltd.

- Continental AG

- Hyundai Motor Co.

- Intel Corp.

- International Business Machines Corp.

- Microsoft Corp.

- NVIDIA Corp.

- Qualcomm Inc.

- Renault SAS

- Robert Bosch GmbH

- Tesla Inc.

- Toyota Motor Corp.

- Valeo SA

- Waymo LLC

- XPeng Inc.

- Zoox

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI In Automotive Market

- In January 2024, Tesla, a leading electric vehicle manufacturer, announced the integration of its Full Self-Driving (FSD) beta software, an advanced AI system, into its Model S and X vehicles. This development marked a significant step towards autonomous driving technology in the automotive industry (Tesla Press Release, 2024).

- In March 2024, Intel and Mobileye, an autonomous driving technology company, unveiled a strategic partnership to develop a scalable, high-performance computing platform for autonomous vehicles. This collaboration aimed to accelerate the deployment of autonomous driving solutions (Intel Press Release, 2024).

- In May 2024, NVIDIA, a leading technology company, secured a strategic investment of USD2 billion from SoftBank Vision Fund 2 to expand its autonomous vehicle technology business. This funding round marked a significant boost for NVIDIA's efforts in AI-driven autonomous vehicles (NVIDIA Press Release, 2024).

- In April 2025, the European Union announced the approval of the European Automated Vehicle Initiative, a public-private partnership aimed at accelerating the development and deployment of automated driving systems in Europe. This initiative represented a significant regulatory push towards the adoption of AI in automotive technology in Europe (European Commission Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Automotive Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

257 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 29% |

|

Market growth 2025-2029 |

USD 11971 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

24.8 |

|

Key countries |

US, China, Germany, Canada, UK, Japan, South Korea, Italy, India, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The automotive market continues to evolve, with artificial intelligence (AI) playing an increasingly significant role in various sectors. Emission reduction strategies are being enhanced through AI-driven engine optimization and fuel efficiency improvement, resulting in a 10% average reduction in carbon emissions for select vehicle models. Cybersecurity protocols are fortified with AI ethics frameworks and machine learning algorithms, safeguarding against potential threats and ensuring data privacy. Radar sensor technology and lidar sensor technology are integrated with AI systems to enable advanced driver-assistance systems (ADAS) and autonomous driving systems, providing real-time data processing and predictive maintenance models. GPS navigation systems are complemented by AI-powered traffic flow optimization and vehicle routing algorithms, ensuring efficient travel and reduced congestion.

- Over-the-air updates and in-cabin monitoring systems leverage AI's ability to learn and adapt, enhancing user experience and safety. AI's role extends to motion planning algorithms, vehicle control systems, and automated vehicle testing, enabling seamless integration of various sensor fusion techniques. Computer vision systems and object detection algorithms are employed to improve safety and convenience, while deep learning models analyze driver behavior and optimize powertrain performance. AI's implementation in automotive applications is expected to grow by 20% annually, with the industry anticipating significant advancements in AI ethics frameworks, sensor technology, and data analytics dashboards. A single example of AI's impact on the automotive market includes Tesla's Autopilot system, which uses a combination of camera sensor technology, radar sensor technology, and machine learning algorithms to provide advanced driver-assistance features.

- This innovation has led to increased sales and customer satisfaction, demonstrating the potential of AI in transforming the automotive industry.

What are the Key Data Covered in this AI In Automotive Market Research and Growth Report?

-

What is the expected growth of the AI In Automotive Market between 2025 and 2029?

-

USD 11.97 billion, at a CAGR of 29%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, Software, and Services), Technology (Machine learning, Computer vision, Deep learning, Context awareness, and Natural language processing), Application (Semi-autonomous vehicles and Fully-autonomous vehicles), Vehicle Type (Passenger vehicles and Commercial vehicles), and Geography (North America, APAC, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Imperative for enhanced safety and relentless pursuit of autonomous driving, Regulatory fragmentation and lack of global standardization

-

-

Who are the major players in the AI In Automotive Market?

-

Aptiv Plc, Aurora Innovation Inc., Baidu Inc., BYD Co. Ltd., Continental AG, Hyundai Motor Co., Intel Corp., International Business Machines Corp., Microsoft Corp., NVIDIA Corp., Qualcomm Inc., Renault SAS, Robert Bosch GmbH, Tesla Inc., Toyota Motor Corp., Valeo SA, Waymo LLC, XPeng Inc., and Zoox

-

Market Research Insights

- The market for AI in automotive applications is continuously evolving, with advancements in technology driving innovation and growth. Two notable developments include the integration of open-source libraries and APIs for enhancing vehicle functionality and safety. For instance, the use of generative adversarial networks in autonomous driving systems has resulted in a significant reduction in false positives during object detection, improving overall safety. Moreover, industry experts anticipate that the AI market in automotive will expand by approximately 25% annually over the next five years.

- This growth is fueled by the increasing demand for advanced driver assistance systems (ADAS) and the development of electric and autonomous vehicles. By leveraging big data analytics, FPGA computing, distributed computing, parallel processing, and other advanced technologies, automakers are creating smarter, more efficient vehicles that cater to the evolving needs of consumers.

We can help! Our analysts can customize this ai in automotive market research report to meet your requirements.

RIA -

RIA -